|

시장보고서

상품코드

2066761

유럽의 전선 및 케이블 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Wire And Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

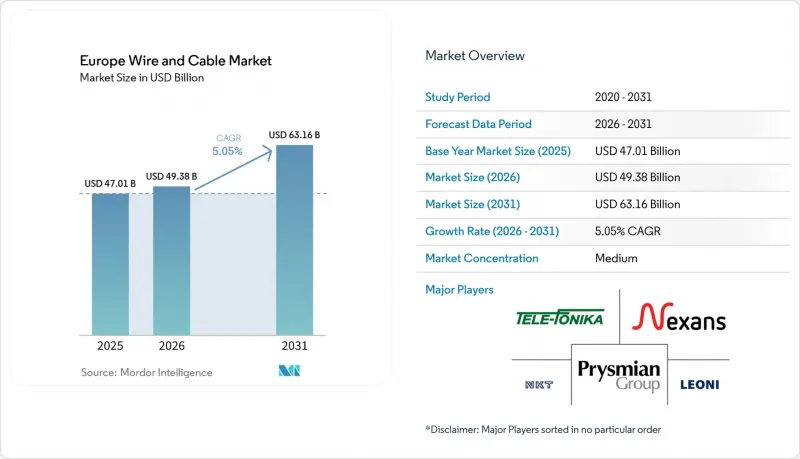

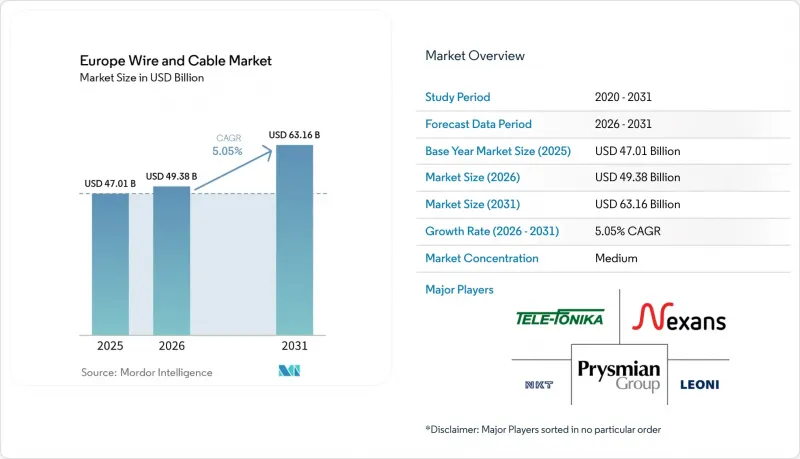

Mordor Intelligence에 의하면, 유럽의 전선 및 케이블 시장 규모는 2025년 470억 1,000만 달러로 평가되었고, 2026년에는 493억 8,000만 달러로 추정되고, 2026-2031년 CAGR 5.05%로 성장을 지속할 전망이며, 2031년에는 631억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 케이블 유형별(저전압 전력 케이블, 중전압 케이블 등), 정격 전압별(1 kV 이하, 1-35 kV 등), 설치 유형별(공중, 지하, 해저), 도체 재료별(구리, 알루미늄, 알루미늄 합금), 최종 사용자 산업별(건설, 전력 인프라·유틸리티, 기타), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 전선 및 케이블 시장 동향 및 인사이트

재생에너지용 케이블 수요의 급증

2045년까지 70 GW를 달성하겠다는 독일의 목표를 비롯한 해상 풍력 발전 목표에 따라, 송전 케이블과 어레이 케이블에 대한 전례 없는 수요가 발생하고 있습니다. 예를 들어, 50억 유로 규모의 Amprion 프로젝트에서는 4,400km에 달하는 ±525kV HVDC 송전선이 단일 계약으로 발주되었습니다. 티레니아 해역에서 수심 2,150미터라는 기록적인 해저 케이블 부설 사례가 보여주듯이, 초심해에서의 설치 작업은 기술적 복잡성이 증가하고 있음을 시사하며, 이는 전문 공급업체들의 프리미엄 가격 책정력을 더욱 강화하고 있습니다. 비스케이 만의 상호 연결선 외에도, 여러 ‘Connecting Europe Facility(CEF)’ 프로젝트에는 약 5,840억 유로(6,870억 달러) 규모의 송전망 자본 지출이 필요한 것으로 추정되며, 다중 전압 수요 파이프라인이 유지되고 있습니다. 각국의 재생에너지 통합법 및 EU 송전망 규정은 더욱 엄격한 손실 제한과 실시간 모니터링을 의무화하고 있으며, 전력 및 광섬유를 결합한 복합 솔루션의 도입을 촉진하고 있습니다. 전력 회사들이 스코프 3 탄소 감축 목표에 따라 대응을 추진하는 가운데, 재활용 소재를 사용한 친환경 인증을 획득한 설계를 제공하는 공급업체가 조달 과정에서 우선적으로 선정되고 있습니다.

송전망 현대화 및 고압(HV) 업그레이드 프로그램

유럽의 송전계통운영자(TSO)는 1970년대에 건설된 노후화된 설비를 교체하는 한편, 분산형 발전에 따른 양방향 전력 흐름에 대비하고 있습니다. 주목할 만한 프로젝트로는 아이젠푸텐슈타트와 프레비스카를 연결하는 제3 인터커넥터가 있으며, 이는 EU의 우선 인프라로 분류되어 결정 제1364/2006호에 따라 공동 자금 지원을 받고 있습니다. 각 제조업체들은 급증하는 수요에 대응하기 위해 사업을 확대하고 있으며, NKT사는 225 kV 이상의 수주에 대응하기 위해 쾰른에 1억 유로(1억 1,800만 달러), 에스포센데에 5,000만 유로(5,900만 달러)를 투자하고 있습니다. 디지털 공장에서는 전력 품질의 허용 범위가 더욱 엄격해짐에 따라, 산업 회랑 내 중전압 케이블의 교체가 시급한 과제가 되고 있습니다. 분산형 온도 측정 및 부분 방전 분석을 가능하게 하는 스마트 센서가 내장된 코어는 시범 단계에서 본격적인 도입 단계로 넘어가고 있으며, 케이블 OEM 제조업체에 장기적인 서비스 기회를 제공합니다. ENTSO-E의 10개년 계획에 따라 사양이 표준화되어, 규모의 경제를 활용한 다국간 일괄 입찰이 가능해졌습니다.

변동이 심한 구리·알루미늄 가격

2024년 5월, 구리 가격이 파운드당 5.20달러에 달하면서 고정 가격 프로젝트의 이익률을 압박하자, 중량을 15% 줄이고 재료비를 최대 25% 절감할 수 있는 알루미늄 합금 도체로 전환하는 움직임이 활발해지고 있습니다. 유럽의 각 제조업체들은 위험을 줄이기 위해 LME 선물 및 공공 입찰의 동적 지수 조항을 활용한 헤지 전략을 강화하고 있습니다. 송전망 운영 사업자는 수명 주기 등가성 분석을 평가하고, 개정된 IEC-60228 규격에 따라 132 kV 이상의 용도에서 합금 사용의 타당성을 검증하고 있습니다. 이와 동시에, EU의 ‘중요 원자재’ 관련 법규에 따라 수입 의존도를 낮추기 위해 국내 제련소 확충이 진행되고 있습니다. 재활용 금속의 사용률은 상승하고 있으며, 프리즈미안사는 2025년에 2차 구리의 사용률이 15.7%를 나타낼 것이라고 보고했는데, 이는 순환형 경제의 조달 평가 기준에 부합하는 것입니다.

부문별 분석

2025년에도 저전압 에너지 제품은 여전히 주력 부문으로, 유럽 전선 및 케이블 시장의 기반을 이루는 주택용 배선 및 상업 프로젝트에 공급되고 있습니다. 그러나 끊임없는 광대역 목표와 5G의 밀집화로 인해 광섬유 솔루션은 연평균 6.6%의 속도로 성장하고 있습니다. 전기차 충전 회랑에서는 도랑 파기 작업을 통합하기 위해, 전력 및 데이터를 통합한 하이브리드 구조가 지지를 얻고 있습니다. 새로운 건설제품규정(CPR)의 분류에 따라 저발연·무할로겐 피복재의 채택이 촉진되고 있어, 지하철 터널 개보수 공사에서 특수 내화 제품 수요가 급증하고 있습니다. 향후 전망으로 볼 때, 광섬유가 통합된 다심 복합 케이블이 단일 용도의 신호선을 점차 대체해 나감에 따라 평균 판매 가격(ASP)이 상승할 것으로 예측됩니다.

이와 동시에, 고전압 및 초고전압(EHV) 송전선은 티레니아 해 연동선 및 비스케이 만과 같은 주요 송전 회랑의 혜택을 받고 있으며, 400 kV 이상의 시스템에서 견조한 수주 잔고를 뒷받침하고 있습니다. 중전압 제품의 경우, 전력 품질 향상이 요구되는 ‘인더스트리 4.0’으로의 전환이 호재로 작용하고 있어, 온라인 온도 감지 기능을 결합한 가교 폴리에틸렌 절연재에 대한 수요를 촉진하고 있습니다. 신호·제어 케이블은 매출에서 차지하는 비중은 작지만, 자동화 업그레이드에는 여전히 필수적이며, 산업용 IoT 구축에 따른 연평균 성장률(CAGR) 5.85%의 성장세를 타고 성장할 것으로 보입니다.

1 kV 이하 구간은 2025년 지출의 39.30%를 차지했으며, 이는 유럽의 밀집된 주택 재고와 소규모 상업시설에서의 지속적인 전기화를 반영하고 있습니다. 중전압(1-35 kV) 시장 규모는 확대되고 있으며, 이는 도시 지역에서 이상 기후에 대한 내성을 높이는 지하 피더를 선호하는 경향이 있기 때문입니다. 유럽의 전선 및 케이블 시장에서 36-150 kV 대역 시장 규모는 지방자치단체의 변전소 확충 및 지역 밀착형 재생에너지 연결을 원동력으로 연평균 성장률(CAGR) 6.1%를 기록하며 확대될 것으로 전망됩니다.

150 kV를 초과하는 분야에서는 BalWin1 및 BalWin2와 같은 고전압 직류 송전(HVDC) 프로젝트의 확대로 인해 수주 전망은 견조한 추세를 보이고 있으나, 허가 취득에 시간이 걸리기 때문에 프로젝트 일정에 편차가 발생할 수 있습니다. ENTSO-E 규정에 따른 국경을 넘는 계통 연계는 사양의 통일을 촉진하고 있으며, 이를 통해 단위당 생산 비용이 감소하고 공급업체의 이익률 안정성이 향상되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the europe wire and cable market size is expected to grow from USD 47.01 billion in 2025 to USD 49.38 billion in 2026 and is forecast to reach USD 63.16 billion by 2031 at 5.05% CAGR over 2026-2031.

This report is Segmented by Cable Type (Low-Voltage Energy Cables, Medium-Voltage Cables, and More), Voltage Rating (<=1 KV, 1-35 KV, and More), Installation Type (Overhead, Underground, and Submarine), Conductor Material (Copper, Aluminium, and Aluminium-Alloy), End-User Industry (Construction, Power Infrastructure and Utilities, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Wire And Cable Market Trends and Insights

Surging Renewable-Power Cable Demand

Offshore-wind targets such as Germany's 70 GW objective by 2045 are creating unprecedented demand for export and array cables, with single awards like the EUR 5 billion Amprion package covering 4,400 km of +-525 kV HVDC lines. Ultra-deep installations demonstrated by a 2,150-meter record lay on the Tyrrhenian Link illustrate rising technical complexity and reinforce premium pricing power for specialized suppliers. The Biscay Gulf interconnector plus multiple Connecting-Europe-Facility projects require an estimated EUR 584 billion (USD 687 billion) in grid capital outlays, sustaining multi-voltage demand pipelines. National renewable-integration laws and EU Grid Codes mandate tighter loss limits and real-time monitoring, driving adoption of composite power-plus-fiber solutions. Vendors offering ECO-certified designs with recycled content gain procurement preference as utilities align with Scope 3 carbon-reduction targets.

Grid-Modernization and HV Upgrade Programmes

European TSOs are replacing ageing 1970s-era assets while preparing for bidirectional flows stemming from distributed generation. Highlights include the Third Interconnector linking Eisenhuttenstadt and Plewiska, categorized as EU priority infrastructure and co-funded under Decision 1364/2006. Manufacturers are expanding to meet the surge; NKT is investing EUR 100 million (USD 118 million) in Cologne and EUR 50 million (USD 59 million) in Esposende to support 225 kV-plus orders. Medium-voltage replacements in industrial corridors are gaining urgency as digital factories demand tighter power-quality tolerances. Smart-sensor embedded cores allowing distributed temperature and partial-discharge analytics are graduating from pilot to scaled roll-out, embedding long-term service opportunities for cable OEMs. ENTSO-E's ten-year plan is standardizing specs, enabling multi-country bulk tenders that reward scale economies.

Volatile Copper and Aluminium Prices

Copper hit USD 5.20 per lb in May 2024, eroding fixed-price project margins and prompting a pivot toward aluminum-alloy conductors that deliver 15% weight savings and up to 25% material-cost relief. European manufacturers intensify hedging with LME futures and dynamic-index clauses in public tenders to mitigate exposure. Grid operators evaluate life-cycle equivalence analyses, validating alloy usage for 132 kV-plus applications under updated IEC-60228 revisions. Concurrently, EU Critical Raw Materials legislation is spurring domestic smelter expansions to dilute import reliance. Recycled-metal content is rising, with Prysmian reporting 15.7% secondary copper usage in 2025, aligning with circular-economy procurement scoring.

Other drivers and restraints analyzed in the detailed report include:

- 5G and Fibre-to-the-Home Rollout

- EU Recovery Fund-Fuelled Undergrounding

- High Installation and Labour Cost (UG/Undersea)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-voltage energy products remained the workhorse segment in 2025, supplying residential wiring and commercial projects that still form the backbone of the European wire and cable market. However, fiber-optic solutions are accelerating at a 6.6% clip thanks to relentless broadband targets and 5G densification. Hybrid power-and-data constructions are gaining favor in electric-vehicle charging corridors to consolidate trenching efforts. Specialty fire-resistant products are soaring in metro-tunnel refurbishments as new Construction Products Regulation (CPR) classes drive adoption of low-smoke, zero-halogen sheaths. Over the outlook, multi-core composite cables embedding optical fibers will progressively cannibalize single-purpose signal lines, bolstering average selling prices (ASPs).

In parallel, high-voltage and extra-high-voltage (EHV) lines are benefiting from marquee transmission corridors such as the Tyrrhenian Link and Biscay Gulf, underpinning a robust backlog for 400 kV-plus systems. Medium-voltage offerings are receiving a lift from Industry 4.0 retrofits that require enhanced power quality, galvanizing demand for cross-linked polyethylene insulation paired with online temperature sensing. Signal and control cables, though smaller in revenue share, remain indispensable to automation upgrades and will ride the 5.85% CAGR wave tethered to the industrial IoT build-out.

The <=1 kV bracket captured 39.30% of 2025 outlays, mirroring Europe's dense residential stock and ongoing electrification of light-commercial premises. Medium-voltage (1-35 kV) funnels are widening as cities favor underground feeders that boost resilience against extreme weather. Europe wire and cable market size for the 36-150 kV tier is forecast to expand at a 6.1% CAGR, driven by municipal sub-station roll-outs and localized renewable hookups.

Above 150 kV, HVDC expansions such as BalWin1 and BalWin2 keep the order pipeline flush, though project timing can be lumpy due to lengthy permits. Cross-border synchronization under ENTSO-E rules is catalyzing spec harmonization, thereby lowering per-unit production costs and enhancing vendor margin stability.

List of Companies Covered in this Report:

- Prysmian S.p.A.

- Nexans S.A.

- NKT A/S

- Leoni AG

- TELE-FONIKA Kable S.A.

- TE Connectivity Ltd.

- British Cables Company Ltd.

- Habia Cable AB

- Waskonig + Walter Kabel-Werke GmbH and Co. KG

- Tratos Cavi S.p.A. Giancarlo De Nardis and C.

- Hellenic Cables S.A.

- La Triveneta Cavi S.p.A.

- HELUKABEL GmbH

- Silec Cable SAS

- Brugg Kabel AG

- Eland Cables Ltd.

- Reka Kaapeli Oy

- TKF B.V. (Twentsche Kabelfabriek)

- Top Cable S.A.

- Cabelte - Cabos Electricos e Telefonicos S.A.

- Elcowire Rail GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging renewable-power cable demand

- 4.2.2 Grid-modernisation and HV upgrade programmes

- 4.2.3 5G and fibre-to-the-home rollout

- 4.2.4 EU Recovery Fund-fuelled undergrounding

- 4.2.5 EV-charging-infrastructure fire-safety cables

- 4.2.6 Smart-sensor cables for Industry 4.0 plants

- 4.3 Market Restraints

- 4.3.1 Volatile copper and aluminium prices

- 4.3.2 High installation and labour cost (UG/undersea)

- 4.3.3 Environmental-permitting delays on subsea links

- 4.3.4 Polymer-compound supply bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Key Macroeconomic Trends on Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Cable Type

- 5.1.1 Low-Voltage Energy Cables

- 5.1.2 Medium-Voltage Cables

- 5.1.3 High-Voltage and EHV Cables

- 5.1.4 Fibre-Optic Cables

- 5.1.5 Signal and Control Cables

- 5.1.6 Specialty/Fire-Resistant Cables

- 5.2 By Voltage Rating

- 5.2.1 <=1 kV

- 5.2.2 1-35 kV

- 5.2.3 36-150 kV

- 5.2.4 >150 kV

- 5.3 By Installation Type

- 5.3.1 Overhead

- 5.3.2 Underground

- 5.3.3 Submarine

- 5.4 By Conductor Material

- 5.4.1 Copper

- 5.4.2 Aluminium

- 5.4.3 Aluminium-Alloy

- 5.5 By End-user Industry

- 5.5.1 Construction (Residential and Communication)

- 5.5.2 Power Infrastructure and Utilities

- 5.5.3 Telecommunications and Data Centres

- 5.5.4 Industrial Manufacturing

- 5.5.5 Transportation (Rail, EV, Marine)

- 5.5.6 Other End-user Industries

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Switzerland

- 5.6.7 Belgium

- 5.6.8 Netherlands

- 5.6.9 Poland

- 5.6.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Prysmian S.p.A.

- 6.4.2 Nexans S.A.

- 6.4.3 NKT A/S

- 6.4.4 Leoni AG

- 6.4.5 TELE-FONIKA Kable S.A.

- 6.4.6 TE Connectivity Ltd.

- 6.4.7 British Cables Company Ltd.

- 6.4.8 Habia Cable AB

- 6.4.9 Waskonig + Walter Kabel-Werke GmbH and Co. KG

- 6.4.10 Tratos Cavi S.p.A. Giancarlo De Nardis and C.

- 6.4.11 Hellenic Cables S.A.

- 6.4.12 La Triveneta Cavi S.p.A.

- 6.4.13 HELUKABEL GmbH

- 6.4.14 Silec Cable SAS

- 6.4.15 Brugg Kabel AG

- 6.4.16 Eland Cables Ltd.

- 6.4.17 Reka Kaapeli Oy

- 6.4.18 TKF B.V. (Twentsche Kabelfabriek)

- 6.4.19 Top Cable S.A.

- 6.4.20 Cabelte - Cabos Electricos e Telefonicos S.A.

- 6.4.21 Elcowire Rail GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment