|

시장보고서

상품코드

2066767

공공 부문 컨설팅 및 자문 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Public Sector Consulting And Advisory Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

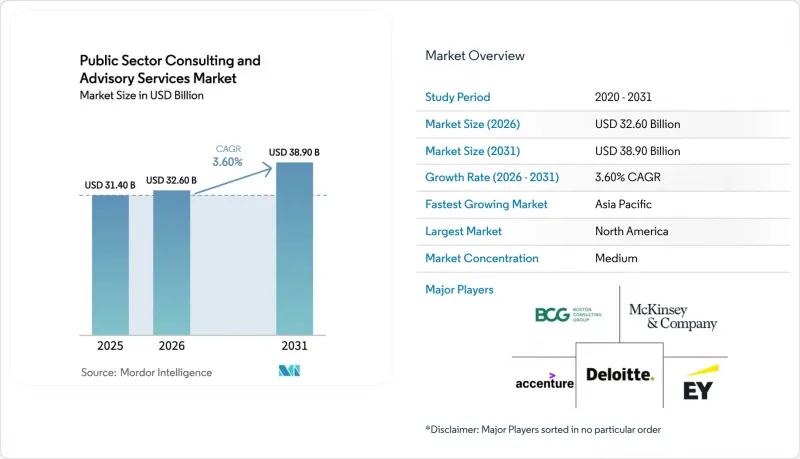

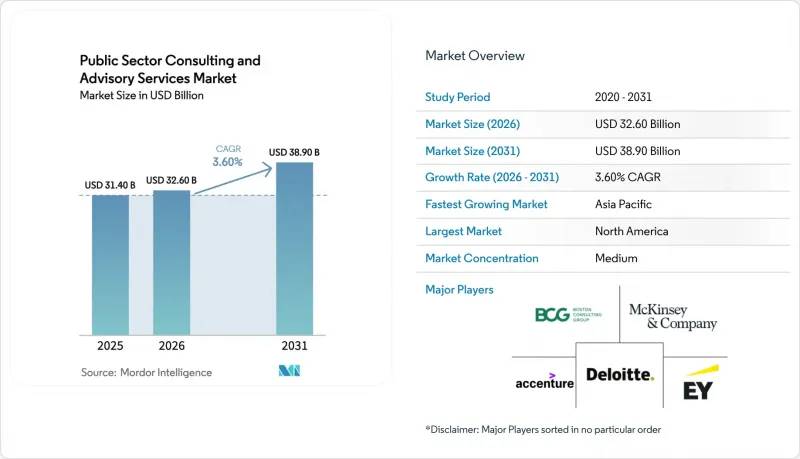

Mordor Intelligence에 의하면, 공공 부문 컨설팅 및 자문 서비스 시장 규모는 2025년 314억 달러로 평가되었고, 2026년에는 326억 달러로 추정되고, 2026-2031년 CAGR 3.60%로 성장을 지속할 전망이며, 2031년에는 389억 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형별(전략, 경영, 기술, 인사, 재무 자문, 기타 서비스), 최종 사용자별(중앙 정부, 주·지방 자치단체, 교육 기관, 의료 기관, 법 집행 기관, 기타 사용자) 및 지역별(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 공공 부문 컨설팅 및 자문 서비스 시장 동향과 인사이트

각 기관에서의 제로 트러스트 및 AI 기반 사이버 보안 의무화

각 기관은 제로 트러스트 대책의 성숙화와 AI 도입에 따른 보안 확보를 요구받고 있으며, 이에 따라 엔터프라이즈 규모에서 사이버 아키텍처, 도구, 거버넌스를 제공할 수 있는 보안 인증을 이미 취득한 기업에 대한 수요가 지속되고 있습니다. NASA 감사총감실은 2024 회계연도부터 2029 회계연도에 걸쳐 사이버 보안 인프라에 대한 지출이 2억 1,100만 달러에 달할 것으로 전망하고 있으며, 이는 컨설팅 기업이 도입 및 운영을 지원하는 방어적 현대화에 대한 연방 정부의 지속적인 투자를 시사합니다. CISA(사이버보안·인프라보안청)는 2025년 9월까지 연방 민간 행정 기관에서 엔드포인트 감지 및 대응(EDR)과 보호형 DNS가 널리 도입될 것이라고 보고했으며, 이를 통해 초기 도입이 아닌 통합, 모니터링, 지속적인 개선에 초점을 맞춘 자문 업무 범위에 대한 기준이 설정될 것입니다. 2025년 4월 OMB(행정관리예산국)의 각서에 따라 AI의 안전성과 감독에 관한 책임이 공식적으로 규정됨에 따라, 각 기관은 아직 대부분 마련하지 못한 역할, 자산 목록 및 심사 절차의 정의를 서둘러 마련해야 하는 상황에 놓여 있습니다. 기밀 정보 취급 허가 제도의 현대화는 수년에 걸친 도입 지연으로 인해 심사 기간이 길어지고, 기밀성이 높은 프로그램에 대한 인력 배치가 복잡해지고 있습니다. 그 결과, 이미 심사를 마친 인재를 다수 보유한 기존 컨설팅 기업들이 유리한 입장에 서 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 사이버 엔지니어링, AI 리스크 프레임워크, 그리고 기밀 정보 취급 허가를 취득한 실행 팀을 결합할 수 있는 기업에 지출이 집중되고 있으며, 이로 인해 공공 부문 대상 컨설팅 및 자문 서비스 시장에서 프리미엄 부문이 더욱 강화되고 있습니다.

eIDAS 2.0/EUDI 지갑, 국경을 초월한 디지털 ID 구축을 추진

eIDAS 2.0 규정은 2026년 12월까지 정부가 발급하는 디지털 ID 지갑을 이용할 수 있도록 하고, 2027년 12월까지 규제 대상 부문에서 널리 수용될 수 있도록 법적 구속력이 있는 기한을 정하고 있습니다. 이로 인해 수년 단위의 로드맵이 단기간으로 압축되면서, 아키텍처, 적합성, 상호운용성 솔루션에 대한 자문 수요가 증가하고 있습니다. 유럽연합 집행위원회는 공공 및 민간 서비스 분야에서 EUDI 지갑의 활용 사례를 확대하기 위해 시범 사업에 자금을 지원했습니다. 이로 인해 표준 조화, 인증 및 국경을 초월한 수용에 관한 노력과 관련된 단기 업무량이 증가하고 있습니다. 정부는 개인정보 보호와 보안을 유지하면서 ID를 지갑 생태계로 전환하기 위해 법적, 기술적, 그리고 변경 관리 역량을 필요로 하고 있으며, 많은 기관이 기한을 준수하기 위해 이러한 역량을 외부 컨설턴트에게 위탁하고 있습니다. 각 부처와 기관이 지갑을 기존 서비스와 통합하고, 국경을 초월한 상호 인정을 실현하기 위해 다양한 분야의 전문 지식을 확보함에 따라, 공공 부문 대상 컨설팅 및 자문 서비스 시장이 혜택을 볼 것으로 전망됩니다. 대규모 ID 관리 경험과 여러 관할 구역을 아우르는 팀을 보유한 컨설팅 기업은 규제 준수와 사용자 경험 향상을 위해 정책과 엔지니어링을 융합할 수 있으므로 경쟁 우위를 확보하게 됩니다.

데이터 현지화 및 주권 클라우드의 제약과 슈렘스 II의 위험

각국 정부는 기밀 데이터의 이동 및 처리에 대한 규제를 강화하고 있으며, 이로 인해 정부 기관과 공급업체는 워크로드를 현지화하고 주권 환경을 구축할 수밖에 없게 되었습니다. 미국 법무부는 2025년 4월, 우려 대상국이 대량의 기밀 개인 데이터에 접근하는 것을 제한하는 규정을 발표했습니다. 이로 인해 국경을 초월한 업무 및 솔루션 호스팅과 관련된 규정 준수 문제가 더욱 복잡해지고 있습니다. 유럽에서는 각 하이퍼스케일러 기업들이 유럽이 관리하는 환경에 막대한 투자를 하고 있으며, 이는 주권으로의 지속적인 전환을 시사하는 것으로, 공공 프로그램의 비용 구조와 도입 전략을 재구축하게 될 것입니다. 컨설팅 기업의 경우, 이러한 규제를 준수하기 위해서는 관할 구역을 넘나드는 데이터 보관 요건 및 접근 제어를 충족하기 위해 병렬 아키텍처와 분리된 전달 팀이 필요합니다. 공공 부문 대상 컨설팅 및 자문 서비스 시장은 다층적인 규정 준수 요건과 인프라 중복 가능성에 대응해야 하며, 이로 인해 이익률이 압박받고 도입 일정이 지연될 가능성이 있습니다.

부문별 분석

기술 컨설팅은 2025년에 공공 부문 대상 컨설팅 및 자문 서비스 시장의 36.5% 점유율을 차지한 것으로 평가되었으며, 클라우드 현대화, 제로 트러스트 제어, AI 거버넌스, 엔터프라이즈급 시스템 통합에 힘입어 2026-2031년 연평균 성장률(CAGR) 9.0%로 확대되고 있습니다. 공공 부문 컨설팅 및 자문 서비스 시장 내 기술 컨설팅 시장 규모는 각 기관이 변화하는 규제 및 프로그램의 감독 하에 AI를 상용화하고 사이버 보안 기준을 강화함에 따라 2026-2031년 연평균 성장률(CAGR) 9.0%로 확대될 것으로 전망됩니다. 최근의 대규모 수주 사례는 엔터프라이즈 통합 및 혁신 업무의 규모를 여실히 보여주고 있습니다. 그 예로, 전미 규모의 시스템 통합과 AI를 활용한 임상 워크플로우를 핵심으로 하는 재향군인부의 전자건강기록(EHR) 현대화 프로그램을 지원하는 4.5년 계약을 들 수 있습니다. 이러한 수요는 엄격한 개인정보 보호, 보안 및 복원력 요건 하에서 운영되는 미션 크리티컬 시스템에 대해 아키텍처, 제공 및 규정 준수를 통합할 수 있는 공급업체에 집중되고 있습니다. 공공 부문 컨설팅 및 자문 서비스 업계에서 경영 컨설팅은 조직 설계나 운영 모델 측면에서 여전히 중요하지만, 구매자들이 측정 가능한 성과를 입증할 수 있고 즉시 도입 가능한 솔루션을 선호하는 경향이 있어 가격 및 업무 범위에 대한 압박에 직면해 있습니다. 업무 및 인사 컨설팅은 지속적인 심사 체계 구축, 보안 승인 자격을 갖춘 인재 확보, 관리 업무의 워크플로우 자동화 측면에서 특정한 역할을 수행하고 있으며, 정부 기관은 이를 기술 주도형 프로그램을 보완하는 역량으로 외부에서 조달하는 경우가 많습니다.

시장 역학은 AI 리스크 프레임워크, 컴플라이언스 액셀러레이터, 그리고 가치 창출까지의 시간을 단축하고 성과 리스크를 줄여주는 독자적인 아키텍처 등 체계화된 제공 자산을 보유한 기업들을 뒷받침하고 있습니다. 공공 부문 컨설팅 및 자문 서비스 업계에서는 대기업들이 연방 및 주 정부의 조달 모델에 맞춘 ‘프로그램 팩토리’와 ‘솔루션 액셀러레이터’를 통해 사업을 확장하는 한편, 부티크형 기업들은 알고리즘 감사, 프라이버시 엔지니어링, 또는 주권 클라우드에 대한 심도 있는 전문 지식을 바탕으로 차별화를 꾀하고 있습니다. 계약 모델은 시간·재료비 기반에서 성과에 연동된 고정 보수형이나 인센티브형으로 전환되고 있으며, 거버넌스와 자동화를 통해 영향을 측정하고 제공 위험을 흡수할 수 있는 공급자에게 보수가 지급되는 구조로 되어 있습니다. 기술 컨설팅은 사이버 및 데이터 플랫폼, 전자건강기록(EHR) 및 사례 관리 시스템, 그리고 유럽에서의 디지털 지갑 보급과 아시아에서의 DPI(데이터 보호 인프라) 도입과 관련된 디지털 ID 이니셔티브를 핵심으로 하고 있으며, 이를 통해 초기 도입 후에도 수년에 걸친 사업 범위가 확보됩니다. 정부 기관이 지속적인 규제나 높은 보증 수준 요구를 예상하는 경우, 보안 승인을 취득한 인력, 규정 준수 인증, 그리고 유사한 환경에서 감사 및 승인을 통과한 참조 아키텍처를 보유한 통합 업체를 선호하는 경향이 있습니다.

지역별 분석

2025년, 북미는 공공 부문 대상 컨설팅 및 자문 서비스 시장 점유율 64.5%를 유지했습니다. 이는 연방 및 지방 자치 단체의 프로그램이 자금을 실제 포트폴리오로 전환하고, 각 기관이 진화하는 지침에 따라 사이버 보안 및 AI 거버넌스를 추진했기 때문입니다. 『인프라 투자·고용법』에 따른 자금은 2024년 중반까지 수만 건의 프로젝트에 승인되었으며, 이에 따라 계획, 규정 준수 및 실행에 걸친 자문 업무의 범위가 유지되고 있습니다. 조달 개혁 및 효율화 노력은 계약 구조와 경쟁 환경에 영향을 미치고 있으며, 이로 인해 일정이 장기화되거나 가격 책정 경향이 고정 가격 모델이나 인센티브 연동형 모델로 전환될 가능성이 있습니다. 의회 감사를 통해 지적된 기밀 정보 취급 허가 시스템의 지연은 기밀 프로그램의 인력 배치를 계속해서 제약하고 있으며, 이로 인해 기존 사업자의 우위가 강화되고 기밀성이 높은 분야의 전반적인 성장 속도가 제한되는 경향이 있습니다. 캐나다와 멕시코는 각국의 디지털화 및 에너지 전환 프로그램을 통해 선택적으로 기여하고 있지만, 미국 연방 정부 및 주 정부의 사업 포트폴리오가 폭넓고 심도 깊기 때문에 북미는 공공 부문 컨설팅 및 자문 서비스 시장의 중심지로 자리매김하고 있습니다.

아시아태평양은 각국이 신원 확인, 결제, 데이터 교환 분야의 디지털 공공 인프라 모델을 모방하고 있기 때문에 2026-2031년 연평균 성장률(CAGR) 17.9%를 나타낼 것으로 예측되며, 가장 빠르게 성장하고 있는 지역입니다. 인도의 UPI 거래 규모와 아다하르(Aadhaar) ID 보급률은 다른 국가 정부가 공동 시범 사업, 기술 지원, 단계적 운영 개시를 통해 도입하는 데 참고 모델이 되고 있습니다. 필리핀의 국민 신분증 도입과 케냐의 디지털 신분증 등록은 역량 강화 파트너십 및 기부자 지원 프로그램을 통해 주변 국가들로도 확산될 기세를 반영하고 있습니다. 일본과 한국은 신뢰성이 높은 공공 플랫폼과 통합된 디지털 서비스를 중시하고 있으며, 이에 따라 아키텍처 현대화, 상호 운용성, 개인정보 보호형 분석에 관한 컨설팅 수요가 발생하고 있습니다. 호주 및 뉴질랜드는 기후 변화 적응과 원주민의 데이터 주권에 중점을 두고 있으며, 이를 통해 공동 설계와 문화적 배려를 중시하는 거버넌스를 위한 자문 요건이 마련되고 있습니다. 이 지역의 성장은 조직의 역량에 따라 규모를 확대할 수 있는 모듈형 접근 방식을 통해 이루어지고 있으며, 이는 공공 부문 팀에 맞춘 반복 가능한 템플릿과 교육 프로그램을 갖춘 컨설팅 기업에 적합합니다.

유럽에서는 초국가적 규제와 각국의 이행상 제약이 복합적으로 작용하고 있으며, 이로 인해 규정 준수, 테스트, 상호 운용성과 관련된 컨설팅에 대한 지속적인 수요가 발생하고 있습니다. eIDAS 2.0의 일정은 각국의 전자 지갑 준비 상황과 국경을 초월한 수용을 위한 노력을 추진하고 있으며, 이를 위해서는 엄격한 기한 내에 법적 및 기술적 역량 모두를 갖추어야 합니다. 기밀성이 높은 워크로드에 대해 관할 구역에서 유럽이 관리하는 데이터 환경을 요구하는 가운데, 소버린 클라우드 이니셔티브가 공공 시장을 활성화시키고 있으며, 아키텍처, 이식성 및 ‘컴플라이언스 바이 디자인’에 관한 컨설팅 수요가 발생하고 있습니다. 사내 디지털 역량이 잘 갖춰진 시장에서는 고위험 AI 분류, 접근성, 개인정보 보호 엔지니어링과 같은 틈새 컨설팅에 중점을 두고 있는 반면, 기타 시장에서는 종합적인 현대화를 추진하기 위해 외부 공급업체에 의존하고 있습니다. 유럽 공공 부문 대상 컨설팅 및 자문 서비스 시장 규모는 규제 일정 및 자금 조달 주기와 밀접한 관련이 있으며, 이러한 요인들이 수주량과 규정 준수 대응 업무 및 시스템 구축 업무의 비율을 좌우하고 있습니다. 라틴아메리카, 중동 및 아프리카에서는 국가 예산이나 다자간 융자를 통해 지원되는 인프라, 스마트 시티, 행정 현대화 프로그램을 통해 시장이 점진적으로 확대되고 있으며, 이러한 프로젝트에서는 프로그램 관리, 규정 준수 체계, 역량 이전 등의 요소가 종종 요구됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the public sector consulting and advisory services market size is expected to grow from USD 31.40 billion in 2025 to USD 32.60 billion in 2026 and is forecast to reach USD 38.90 billion by 2031 at 3.60% CAGR over 2026-2031.

This report is Segmented by Service Type (Strategy, Management, Technology, Human Resource, Financial Advisory, and Other Services), End User (Central Government, State and Local Government, Educational, Healthcare, Law Enforcement, and Other Users), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). Market Forecasts are in Value (USD).

Global Public Sector Consulting And Advisory Services Market Trends and Insights

Zero-Trust and AI-Ready Cybersecurity Mandates Across Agencies

Agencies are under pressure to mature zero-trust controls and secure AI deployments, which sustains demand for cleared firms that can deliver cyber architecture, tooling, and governance at enterprise scale. NASA's Office of Inspector General projected USD 211 million in cybersecurity infrastructure spending for fiscal 2024 through 2029, signaling persistent federal investment into defensive modernization that consultancies help implement and operationalize. CISA reported broad uptake of endpoint detection and response and protective DNS among Federal Civilian Executive Branch agencies by September 2025, which sets a baseline for advisory scope focused on integration, monitoring, and continuous improvement rather than first-time deployment. The April 2025 OMB memoranda formalized responsibilities for AI safety and oversight, prompting agencies to define roles, inventories, and review processes that most do not yet have in place. Clearance system modernization has experienced multi-year implementation delays, which prolong adjudications and complicate staffing of sensitive programs, thereby favoring incumbent consultants with benches of adjudicated personnel. Together, these factors concentrate spend on firms that can combine cyber engineering, AI risk frameworks, and cleared delivery teams, which reinforces a premium tier in the Public Sector Consulting and Advisory Services market.

eIDAS 2.0/EUDI Wallets Driving Cross-Border Digital Identity Build-Outs

The eIDAS 2.0 Regulation sets binding deadlines for government-issued digital identity wallets to be available by December 2026 and widely accepted in regulated sectors by December 2027, compressing a multi-year roadmap into a short window that grows advisory demand for architecture, conformance, and interoperability solutions. The European Commission funded pilots to accelerate EUDI wallet use cases across public and private services, which increases the near-term volume of work on standards alignment, certification, and cross-border acceptance pathways. Governments need legal, technical, and change-management capacity to replatform identity into wallet ecosystems while preserving privacy and security, which many agencies source from external consultants to meet deadlines. The Public Sector Consulting and Advisory Services market stands to benefit as ministries and agencies procure multi-domain expertise to integrate wallets with legacy services and enable mutual recognition across borders. Consulting firms with prior large-scale identity experience and cross-jurisdictional teams gain an advantage because they can combine policy and engineering in service of regulatory conformance and user experience.

Data Localization/Sovereign Cloud Constraints and Schrems II Risk

Governments are tightening controls on the movement and processing of sensitive data, which compels agencies and vendors to localize workloads and create sovereign environments. The U.S. Department of Justice issued a rule in April 2025 restricting access to bulk sensitive personal data by countries of concern, which increases compliance complexity for cross-border engagements and solution hosting. In Europe, hyperscalers are committing significant investment to European-controlled environments, signaling a durable shift toward sovereignty that reshapes cost structures and deployment strategies for public programs. For consultancies, these rules require parallel architectures and segregated delivery teams to satisfy residency and access controls across jurisdictions. The Public Sector Consulting and Advisory Services market must adapt to layered compliance and potential duplication of infrastructure, which can compress margins and slow implementation timelines.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Stimulus Delivery and Resilience Programs

- Outcome-Based Procurement and Results-Driven Contracting

- Procurement Reform Scrutiny and Consulting Spend Rationalization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technology consulting captured 36.5% of the Public Sector Consulting and Advisory Services market share in 2025 and is expanding at 9.0% CAGR from 2026 to 2031, driven by cloud modernization, zero-trust controls, AI governance, and enterprise-scale system integration. The Public Sector Consulting and Advisory Services market size for technology consulting is projected to expand at 9.0% CAGR between 2026 and 2031 as agencies operationalize AI and tighten cybersecurity baselines under evolving rules and program oversight. Recent large-scale wins highlight the scope of enterprise integration and transformation work, including a 4.5-year engagement supporting the Veterans Affairs EHR modernization program that centers on system integration and AI-enabled clinical workflows across a national footprint. This demand concentrates on providers that can fuse architecture, delivery, and compliance for mission-critical systems operating under strict privacy, security, and resiliency requirements. Within the Public Sector Consulting and Advisory Services industry, management consulting remains important for organization design and operating models but faces pricing and scope pressures as buyers favor implementation-ready solutions that can demonstrate measurable outcomes. Operations and HR consulting play targeted roles in continuous-vetting readiness, cleared talent pipelines, and workflow automation for administrative functions, which agencies often source as adjunct capabilities to technology-led programs.

Market dynamics favor firms with codified delivery assets, including AI risk frameworks, compliance accelerators, and proprietary architectures that reduce time to value and de-risk outcomes. The Public Sector Consulting and Advisory Services industry sees larger players expand through program factories and solution accelerators tailored to federal and state procurement models, while boutiques differentiate through deep expertise in algorithmic auditing, privacy engineering, or sovereign cloud. Engagement models shift from time and materials to fixed or incentive structures aligned to results, which reward providers that can measure impact and absorb delivery risk through governance and automation. Technology consulting is anchored by cyber and data platforms, EHR and case systems, and digital identity initiatives tied to wallet adoption in Europe and DPI replication in Asia, which ensures multi-year scopes beyond initial launches. Where agencies anticipate persistent regulation and high assurance demands, they tend to prefer integrators with cleared benches, compliance certifications, and reference architectures that have passed audit and authorization in similar environments.

Geography Analysis

North America retained 64.5% of the Public Sector Consulting and Advisory Services market share in 2025 as federal and subnational programs translated funding into active portfolios and as agencies advanced cybersecurity and AI governance under evolving mandates. Funding under the Infrastructure Investment and Jobs Act was authorized into tens of thousands of projects by mid-2024, which sustains advisory scopes across planning, compliance, and delivery. Procurement reforms and streamlining efforts influence award structures and competition, which can extend timelines and shift pricing preferences toward fixed or incentive-aligned models. Clearance-system delays highlighted in congressional oversight continue to constrain staffing for classified programs, which tends to reinforce incumbency and limit overall growth velocity in sensitive domains. Canada and Mexico contribute selectively through national digital and energy transition programs, but the breadth and depth of U.S. federal and state portfolios keep North America at the center of the Public Sector Consulting and Advisory Services market.

Asia-Pacific is the fastest-growing region with a projected 17.9% CAGR over 2026-2031 as countries replicate digital public infrastructure patterns in identity, payments, and data exchange. India's UPI transaction scale and Aadhaar identity coverage form reference models that other governments adapt through collaborative pilots, technical assistance, and staged operationalization. The Philippines' national ID rollout and Kenya's digital ID enrollment reflect momentum that often extends to neighboring countries through capacity-building partnerships and donor-supported programs. Japan and South Korea emphasize high-assurance public platforms and integrated digital services, which generate consulting demand for architecture modernization, interoperability, and privacy-preserving analytics. Australia and New Zealand focus on climate adaptation and Indigenous data sovereignty, which shape advisory requirements toward co-design and culturally sensitive governance. The region's growth comes through modular engagements that scale with institutional capacity, which suits consultancies with repeatable templates and training programs tailored to public-sector teams.

Europe combines supranational regulation with national delivery constraints, which creates sustained demand for conformance, testing, and interoperability advisory. The eIDAS 2.0 schedule drives country-by-country wallet readiness and cross-border acceptance work that requires both legal and technical capabilities within tight timelines. Sovereign cloud initiatives are galvanizing public markets as jurisdictions require European-controlled data environments for sensitive workloads, prompting consulting requirements in architecture, portability, and compliance-by-design. Markets with strong in-house digital capabilities focus on niche consulting for high-risk AI classification, accessibility, and privacy engineering, while others rely on external providers to guide holistic modernization. The Public Sector Consulting and Advisory Services market size in Europe is closely tied to regulatory timelines and funding cycles, which shape engagement volumes and the mix of conformance versus build work. Latin America and the Middle East and Africa contribute episodically through infrastructure, smart city, and administrative modernization programs supported by sovereign budgets and multilateral financing, which often require program controls, compliance frameworks, and capability transfer components.

- Accenture

- Deloitte

- PwC

- EY

- KPMG

- McKinsey & Company

- Boston Consulting Group (BCG)

- Bain & Company

- Booz Allen Hamilton

- Guidehouse

- IBM Consulting

- Capgemini

- CGI

- ICF

- PA Consulting

- Oliver Wyman

- Roland Berger

- Protiviti

- Alvarez & Marsal

- SAIC

- Leidos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Zero-trust and AI-ready cybersecurity mandates across agencies

- 4.2.2 eIDAS 2.0/EUDI wallets driving cross-border digital identity build-outs

- 4.2.3 Infrastructure stimulus delivery (e.g., IIJA) and resilience programs

- 4.2.4 Outcome-based procurement and results-driven contracting

- 4.2.5 Digital Public Infrastructure (DPI) replication and GovTech platforms

- 4.2.6 Algorithmic accountability and AI-governance requirements

- 4.3 Market Restraints

- 4.3.1 Data localization/sovereign cloud constraints and Schrems II risk

- 4.3.2 Procurement reform scrutiny and consulting spend rationalization

- 4.3.3 Complex grants/FAR/Uniform Guidance compliance burdens

- 4.3.4 Scarcity of cleared and specialist public-sector talent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Strategy Consulting

- 5.1.2 Management Consulting

- 5.1.3 Technology Consulting

- 5.1.4 Human Resource Consulting

- 5.1.5 Financial Advisory

- 5.1.6 Other Service Types (Risk & Compliance Advisory & Operations Consulting)

- 5.2 By End User

- 5.2.1 Central Government

- 5.2.2 State and Local Government

- 5.2.3 Educational Institutions

- 5.2.4 Healthcare Organizations

- 5.2.5 Law Enforcement and Judiciary Services

- 5.2.6 Other End Users (Transportation Services & Utilities And Environmental Projects)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Uruguay

- 5.3.4.4 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Accenture

- 6.4.2 Deloitte

- 6.4.3 PwC

- 6.4.4 EY

- 6.4.5 KPMG

- 6.4.6 McKinsey & Company

- 6.4.7 Boston Consulting Group (BCG)

- 6.4.8 Bain & Company

- 6.4.9 Booz Allen Hamilton

- 6.4.10 Guidehouse

- 6.4.11 IBM Consulting

- 6.4.12 Capgemini

- 6.4.13 CGI

- 6.4.14 ICF

- 6.4.15 PA Consulting

- 6.4.16 Oliver Wyman

- 6.4.17 Roland Berger

- 6.4.18 Protiviti

- 6.4.19 Alvarez & Marsal

- 6.4.20 SAIC

- 6.4.21 Leidos

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment