|

시장보고서

상품코드

2072455

클라우드 기반 이메일 보안 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cloud-Based Email Security Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

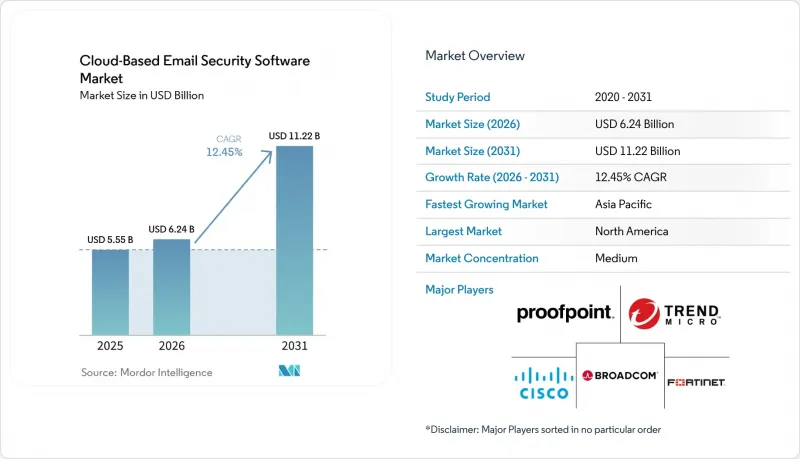

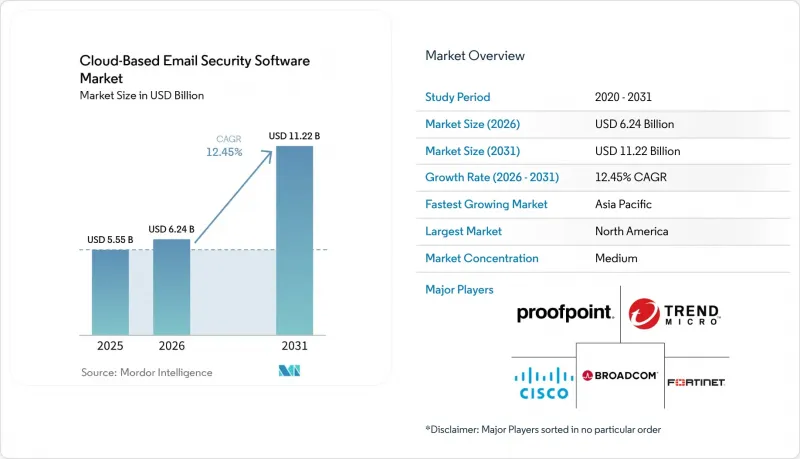

Mordor Intelligence에 의하면, 2026년 클라우드 기반 이메일 보안 소프트웨어 시장 규모는 62억 4,000만 달러로 추정되고 2025년 55억 5,000만 달러에서 확대해, 2031년에는 112억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 12.45%가 될 것으로 전망됩니다.

본 보고서는 서비스 유형(필터링 및 스팸 방지, 악성코드 및 고도화된 위협 방지 등), 플랫폼 통합(보안 메일 게이트웨이(SEG) 등), 조직 규모(대기업 및 중소기업(SME)), 산업 분야(은행, 금융서비스 및 보험(BFSI), 정부·국방 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 클라우드 기반 이메일 보안 소프트웨어 시장 동향 및 인사이트

AI를 활용한 피싱 및 BEC 공격 증가

생성형 AI 도구의 등장으로 공격자들은 경영진의 어조와 타이밍을 모방한 맞춤형 이메일을 작성할 수 있게 되었으며, 피싱 성공률은 60%에 달하고, 2024년 비즈니스 이메일 사기(BEC)로 인한 손실액은 29억 달러에 달했습니다. 다크웹에서 판매되는 피싱 키트의 75%가 AI 기능을 내세우고 있어, 위협 경제의 산업화가 진행되고 있음이 드러나고 있습니다. 의료 업계에서는 AI를 활용한 BEC(비즈니스 이메일 사기) 사고가 279% 급증했으며, 건당 평균 손실액은 12만 5,000달러에 달했습니다. 따라서 조직에서는 의사소통 패턴의 기준치를 확립하고, 언어적 이상을 감지하는 자연어 처리 엔진을 도입하고 있습니다. 교묘하게 설계된 함정에 대한 최종 점검 단계는 여전히 직원들이기 때문에 행동 인식 프로그램이 기술을 보완하는 역할을 하고 있습니다.

SEG에서 API 기반 ICES로의 급속한 전환

기업의 70%가 보안 메일 게이트웨이를 API를 통해 Microsoft 365 및 Google Workspace에 직접 연결하는 통합형 클라우드 이메일 보안(ICES) 플랫폼으로 적극적으로 교체하고 있습니다. API 통합을 통해 이메일 흐름을 우회하지 않고도 내부 트래픽과 사용자 행동을 가시화할 수 있어, 고객 환경에서의 감지 효율을 30% 향상시켰습니다. 클라우드 스위트에서 수집된 실시간 텔레메트리 데이터가 머신러닝 모델에 제공되어, 해킹당한 계정을 몇 분 이내에 격리합니다. Proofpoint와 Azure 보안 API의 통합과 같은 벤더 간 제휴를 통해 도입 기간이 수개월에서 수일로 단축되었으며, 아키텍처 전환이 가속화되고 있습니다.

클라우드 보안 운영 분야에서 만연한 기술 인력 부족

세계 사이버 보안 전문가의 수는 550만 명이지만, 480만 명에 달하는 인력 부족에 직면해 있으며, 기업의 90%는 클라우드 및 AI 보안 전문 지식을 갖춘 인재 채용이 가장 어렵다고 지적하고 있습니다. ENISA는 클라우드 보안 사고의 99%가 공급자의 결함이 아니라 고객 측의 설정 오류에서 비롯된다는 사실을 확인했습니다. 금융 서비스 및 기술 기업에서는 약 28%의 공석률이 지속되고 있어, 전문적인 조정이 필요한 행동 분석 도구의 도입이 지연되고 있습니다. 따라서 많은 조직이 인력 부족을 보완하기 위해 관리형 보안 서비스나 AI 지원형 도구로 전환하고 있지만, 자동화 분야에서도 정책 거버넌스를 위한 감독은 여전히 필요합니다.

부문별 분석

2025년, 필터링 및 스팸 방지 솔루션은 클라우드 기반 이메일 보안 소프트웨어 시장에서 41.02%의 점유율을 유지했습니다. 한편, 데이터 유출 방지(DLP)는 재택근무의 확산으로 인해 이메일 워크플로우에서 비정형 데이터의 노출이 가속화되고 있어, 연평균 성장률(CAGR) 13.22%로 가장 빠르게 성장할 것으로 전망됩니다. 현재 기업들은 기존의 정규 표현식을 이용한 패턴 매칭 대신, 컨텐츠, 사용자 및 위치에 대한 메타데이터를 실시간으로 추적하는 컨텍스트 인식형 DLP를 중시하고 있습니다. 악성코드 및 고도화된 위협 대응 서비스에는 대규모 언어 모델이 통합되어 있어, 정적 시그니처가 아닌 첨부 파일의 행동 지표를 스캔합니다. 선도적인 기업들이 포스트 양자 알고리즘을 도입함에 따라 암호화 및 토큰화 솔루션이 확대되고 있으며, 이는 고객들이 미국 국립표준기술연구소(NIST)의 전환 일정에 대비할 수 있도록 지원하고 있습니다. 이러한 변화들은 전반적으로 경계 방어에서 데이터 중심 통제로의 전환을 보여줍니다.

HIPAA 및 PCI-DSS와 같은 규제 체계의 확대에 따라, 기업들은 이메일을 통한 데이터 흐름에 대한 로그 기록 및 감사를 수행해야만 합니다. 구글이 Gmail 기업 사용자를 대상으로 종단 간암호화를 제공한 것은 공급업체가 규정 준수 기능을 기본 설정에 포함시키고 있음을 보여주는 좋은 예입니다. 조직이 외부 위협은 물론 내부 관계자에 의한 위험에도 대응해 나감에 따라, DLP(데이터 유출 방지) 중심의 클라우드 기반 이메일 보안 소프트웨어 시장 규모는 총 지출에서 차지하는 비중이 확대될 것으로 예측됩니다. 또한, 각 벤더사는 정책 준수를 강화하는 보안 인식 제고 교육 모듈을 포함시켜, 경보 피로와 규정 준수 부담을 줄여주는 통합 플랫폼을 구축하고 있습니다.

2025년에도 보안 메일 게이트웨이는 여전히 매출의 54.95%를 차지했지만, API를 지원하는 통합형 클라우드 이메일 보안(ICES) 솔루션은 연평균 성장률(CAGR) 13.55%로 성장할 것으로 전망됩니다. 이는 클라우드 네이티브 제품군의 게이트웨이 프록시 아키텍처상의 한계를 반영한 것입니다. ICES는 Microsoft 365 및 Google Workspace에 직접 연결하여 내부 트래픽을 분석함으로써, 소셜 엔지니어링 감지율을 30% 향상시킵니다. 또한, 클라우드 네이티브 이메일 보안 플랫폼은 자동 확장 기능을 갖추고 있어, 급증하는 워크로드나 지리적으로 분산된 팀에게 매력적인 선택지가 되고 있습니다. 규제가 엄격한 업계에서는 규정 준수 로그 기록을 위해 On-Premise 게이트웨이를 유지하면서, 행동 분석을 위해 API를 활용하는 하이브리드 방식이 여전히 채택되고 있습니다.

파트너십이 심화됨에 따라(마이크로소프트는 최근 Proofpoint와의 Azure 기반 위협 신호 공유를 확대했습니다), 고객은 하류 XDR 플랫폼에 정보를 제공할 수 있는 통합된 텔레메트리 데이터를 확보할 수 있게 됩니다. 그 결과, 효율성이 향상되어 사고의 평균 감지 시간(MTD)이 최대 40% 단축됩니다. API 퍼스트 도입에 따른 클라우드 기반 이메일 보안 소프트웨어 시장 규모는 교체 주기에 따라 어플라이언스 도입이 단계적으로 폐지됨에 따라 2029년까지 SEG(보안 에지) 시장 규모를 넘어설 것으로 예측됩니다.

지역별 분석

2025년, 북미는 클라우드 기반 이메일 보안 소프트웨어 시장을 주도하며 매출의 38.10%를 차지했습니다. Microsoft 365의 광범위한 도입과 높은 사고 공개율이 투자를 주도하는 한편, 정보 유출 통지 기한이 엄격해짐에 따라 자동화된 대응 도구의 신속한 도입이 요구되고 있습니다. 해당 지역에서 벤더 통합이 진행되면서 플랫폼의 범위가 확대되었으며, 단일 계약을 통해 이메일, 엔드포인트, ID 보안을 묶은 솔루션이 제공되고 있습니다. 미국의 사이버 보안 전략 등 정부 지침이 제로 트러스트형 이메일 아키텍처를 장려하고 있으며, 이것이 지속적인 수요를 뒷받침하고 있습니다.

아시아태평양은 급속한 디지털 전환이 진행되고 있을 뿐만 아니라, 전 세계 사이버 공격의 31%가 이 지역에서 발생하고 있는 점으로 미루어 볼 때, 2031년까지 연평균 성장률(CAGR) 12.74%로 가장 높은 성장률을 보일 것으로 전망됩니다. 중국과 일본을 합치면 2028년까지 연평균 성장률(CAGR) 16.9%로 확대될 것으로 예측됩니다. 이는 데이터 현지화 요건이 국가별 데이터센터에 이메일 보안 제어 기능을 통합한 소버린 클라우드 인스턴스에 대한 수요를 촉진하고 있기 때문입니다. 인도는 확대되는 IT 서비스 부문과 사이버 보안 투자에 대해 세제 혜택을 제공하는 정부 주도의 ‘ '디지털 인디아' 프로그램의 지원을 바탕으로 성장의 중심지로 부상하고 있습니다.

유럽의 성장세는 엄격한 규제에 힘입고 있습니다. 이메일을 통한 데이터 유출에 대한 GDPR(EU 개인정보보호규정)의 과징금과 새로운 NIS 2 지침으로 인해, 보안 지출은 IT 예산의 평균 9%까지 증가했습니다. 독일과 프랑스의 기관들은 공급업체들에게 양자 내성 암호화 및 ESG 인증을 받은 데이터센터의 도입을 요구하고 있습니다. 그 밖의 지역에서는 남미와 중동 및 아프리카가 여전히 개발도상 시장이지만, 클라우드 공급업체들의 지역 진출과 랜섬웨어 피해 증가가 맞물리면서 도입이 서서히 진행되고 있습니다. 하이퍼스케일러들이 현지 가용성 구역을 개설함에 따라 지연으로 인한 장벽은 줄어들고 있으며, 이메일 보안 서비스도 새로운 데이터 소재지 관련 법규를 준수하게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, cloud-based email security software market size in 2026 is estimated at USD 6.24 billion, growing from 2025 value of USD 5.55 billion with 2031 projections showing USD 11.22 billion, growing at 12.45% CAGR over 2026-2031.

This report is Segmented by Service Type (Filtering and Anti-Spam, Malware and Advanced Threat Protection, and More), Platform Integration (Secure Email Gateway (SEG), and More), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Industry Vertical (BFSI, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud-Based Email Security Software Market Trends and Insights

Rise in AI-driven phishing and BEC attacks

Generative-AI tooling now allows adversaries to craft tailored emails that mimic executive tone and timing, driving phishing success rates to 60% and pushing 2024 business email compromise losses to USD 2.9 billion. Seventy-five percent of phishing kits marketed on the dark web advertise AI functionality, underscoring an industrialized threat economy. Healthcare recorded a 279% jump in AI-enabled BEC incidents with average losses of USD 125,000 per case. Organizations therefore deploy natural-language processing engines that baseline communication patterns and flag linguistic anomalies. Behavioral awareness programs complement technology as employees remain the final checkpoint against well-crafted lures.

Rapid migration from SEG to API-based ICES

Seventy percent of enterprises are actively replacing secure email gateways with Integrated Cloud Email Security platforms that connect directly into Microsoft 365 or Google Workspace via APIs. API integration brings visibility into internal traffic and user behavior without mail-flow rerouting, improving detection efficacy by 30% in customer environments. Real-time telemetry from cloud suites feeds machine-learning models that isolate compromised accounts within minutes. Vendor alliances-such as Proofpoint's integration with Azure security APIs-lower deployment timelines from months to days, hastening the architectural shift.

Persistent skills gap in cloud-security operations

The global workforce counts 5.5 million cybersecurity professionals, yet faces a 4.8 million shortfall, and 90% of companies cite cloud and AI security expertise as the hardest to hire. ENISA confirms that 99% of cloud security failures originate from customer misconfigurations rather than provider flaws. Financial services and technology firms hold vacancy rates around 28%, slowing the rollout of behavioral analytics tools that demand specialized tuning. Many organizations therefore shift to managed security services and AI-assisted tooling to offset human shortages, though automation still requires oversight for policy governance.

Other drivers and restraints analyzed in the detailed report include:

- Cost and agility benefits of cloud delivery

- Generative-AI deepfake emails

- Latency and data-sovereignty compliance hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Filtering and Anti-Spam retained 41.02% of the cloud-based email security software market in 2025. Data Loss Prevention, however, is projected to grow fastest at 13.22% CAGR because remote work accelerates unstructured data exposure in email workflows. Organizations now value context-aware DLP that tracks content, user, and location metadata in real time, replacing legacy regex pattern matching. Malware and Advanced Threat Protection services integrate large language models that scan attachments for behavioral indicators rather than static signatures. Encryption and Tokenization offerings expand as early movers embed post-quantum algorithms, preparing customers for National Institute of Standards and Technology transition timelines. Collectively, these shifts mark a pivot from perimeter defense to data-centric controls.

Expanding regulatory frameworks such as HIPAA and PCI-DSS compel enterprises to log and audit email-borne data flows. Google's delivery of end-to-end encryption for Gmail enterprise users illustrates how vendors package compliance inside default settings. The cloud-based email security software market size for DLP-driven offerings is expected to capture a rising share of total spend as organizations tackle insider risk alongside external threat vectors. Vendors also bundle security-awareness training modules that reinforce policy adherence, creating unified platforms that reduce alert fatigue and compliance overhead.

Secure Email Gateways still controlled 54.95% revenue in 2025, yet API-enabled Integrated Cloud Email Security solutions are forecast to rise at 13.55% CAGR, reflecting architectural limitations of gateway proxies in cloud-native suites. ICES connects directly into Microsoft 365 and Google Workspace to analyze internal traffic, delivering 30% uplift in social-engineering detection rates. Cloud-native email security platforms also auto-scale, making them attractive for burst workloads and geographically distributed teams. Hybrid approaches persist where heavily regulated sectors maintain on-prem gateways for compliance logging but wrap APIs for behavioral analytics.

As partnerships deepen-Microsoft recently extended Azure-based threat-signal sharing with Proofpoint-customers gain unified telemetry that feeds downstream XDR platforms. Resulting efficiencies shorten mean-time-to-detect incidents by up to 40%. The cloud-based email security software market size attached to API-first deployments is projected to overtake SEG allocations before 2029 as refresh cycles retire appliance footprints.

Complete Report Scope:

- By Service Type

- Filtering and Anti-Spam

- Malware and Advanced Threat Protection

- Data Loss Prevention

- Encryption and Tokenization

- Others

- By Platform Integration

- Secure Email Gateway (SEG)

- Integrated Cloud Email Security (ICES/API)

- Cloud-Native Email Security Platform

- Hybrid Gateway and API

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- BFSI

- Government and Defense

- IT and Telecommunications

- Healthcare and Life Sciences

- Retail and E-Commerce

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America led the cloud-based email security software market with 38.10% revenue in 2025. Widespread Microsoft 365 adoption and high incident disclosure rates drive investment, while tight breach-notification windows compel rapid deployment of automated response tooling. Vendor consolidation in the region accelerates platform breadth, offering bundled email, endpoint, and identity security under single contracts. Government directives such as the US Cybersecurity Strategy promote zero-trust email architectures, underpinning continued demand.

Asia-Pacific is forecast for the highest 12.74% CAGR through 2031 amid rapid digital transformation and the region's 31% share of global cyberattacks. China and Japan together are projected to expand at 16.9% CAGR through 2028 as data-localization requirements fuel demand for sovereign cloud instances that embed email security controls in country-specific data centers. India emerges as a growth hotspot, buoyed by its expanding IT services sector and government-led "Digital India" program that offers tax incentives for cybersecurity investment.

Europe's momentum rests on stringent regulations: GDPR fines for data-exfiltration via email and the new NIS 2 Directive have elevated security spending to 9% of IT budgets on average. Organizations in Germany and France push suppliers for quantum-resilient encryption and ESG-validated data centers. Elsewhere, South America and the Middle East and Africa remain nascent markets, yet cloud vendor region launches combined with rising ransomware incidents foster gradual uptake. As hyperscalers open local availability zones, latency barriers fall, and email security services become compliant with emerging data-residency laws.

- Barracuda Networks Inc.

- Proofpoint Inc.

- Mimecast Ltd.

- Cisco Systems Inc.

- Trend Micro Inc.

- Microsoft Corporation

- Google LLC (Google Cloud)

- Fortinet Inc.

- Broadcom Inc. (Symantec)

- Check Point Software Technologies Ltd.

- Sophos Group PLC

- Forcepoint LLC

- Dell Technologies Inc.

- Zscaler Inc.

- Cloudflare Inc.

- Ironscales Ltd.

- Egress Software Technologies Ltd.

- Trellix (Musarubra US LLC)

- OpenText Cybersecurity

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in AI-driven phishing and BEC attacks

- 4.2.2 Rapid migration from SEG to API-based ICES

- 4.2.3 Cost and agility benefits of cloud delivery

- 4.2.4 Generative-AI-powered deepfake emails

- 4.2.5 Urgency around quantum-resilient encryption

- 4.2.6 ESG-driven demand for carbon-light email security

- 4.3 Market Restraints

- 4.3.1 Persistent skills gap in cloud-security ops

- 4.3.2 Latency and data-sovereignty compliance hurdles

- 4.3.3 Exploitable mis-configurations in multi-cloud

- 4.3.4 Emerging AI-based evasion of sandboxing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Filtering and Anti-Spam

- 5.1.2 Malware and Advanced Threat Protection

- 5.1.3 Data Loss Prevention

- 5.1.4 Encryption and Tokenization

- 5.1.5 Others

- 5.2 By Platform Integration

- 5.2.1 Secure Email Gateway (SEG)

- 5.2.2 Integrated Cloud Email Security (ICES/API)

- 5.2.3 Cloud-Native Email Security Platform

- 5.2.4 Hybrid Gateway and API

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 IT and Telecommunications

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Retail and E-Commerce

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Barracuda Networks Inc.

- 6.4.2 Proofpoint Inc.

- 6.4.3 Mimecast Ltd.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Trend Micro Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC (Google Cloud)

- 6.4.8 Fortinet Inc.

- 6.4.9 Broadcom Inc. (Symantec)

- 6.4.10 Check Point Software Technologies Ltd.

- 6.4.11 Sophos Group PLC

- 6.4.12 Forcepoint LLC

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Zscaler Inc.

- 6.4.15 Cloudflare Inc.

- 6.4.16 Ironscales Ltd.

- 6.4.17 Egress Software Technologies Ltd.

- 6.4.18 Trellix (Musarubra US LLC)

- 6.4.19 OpenText Cybersecurity

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment