|

시장보고서

상품코드

2072491

거대세포바이러스 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cytomegalovirus Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

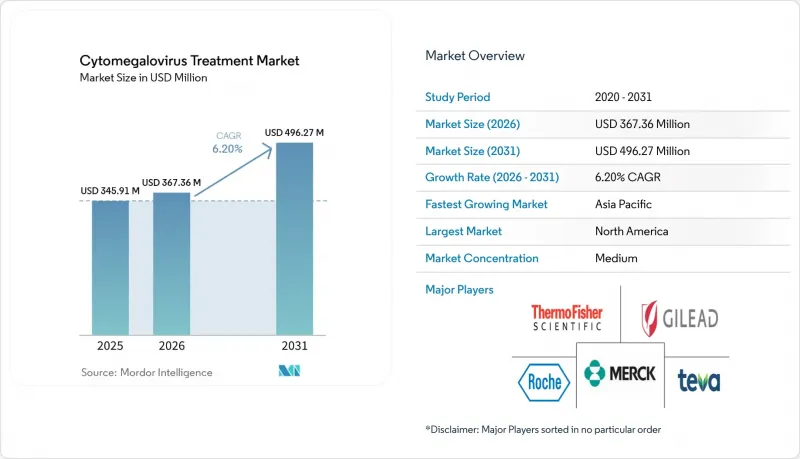

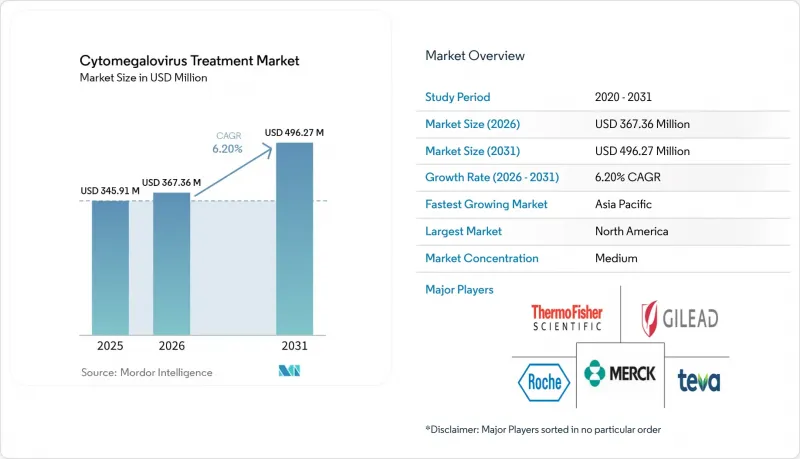

Mordor Intelligence에 의하면, 2026년 거대세포바이러스 치료 시장 규모는 3억 6,736만 달러로 추정되고 2025년 3억 4,591만 달러에서 확대해, 2031년에는 4억 9,627만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.20%로 성장할 것으로 전망됩니다.

본 보고서는 약물 분류별(DNA 중합효소 억제제, 종결효소 억제제, 기타 약물 분류), 용도별(조혈모세포 이식 등), 투여 경로별(경구 투여 등), 유통 채널별(병원 약국 등) 및 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 거대세포바이러스 치료 시장 동향 및 인사이트

조혈모세포 이식(HSCT) 및 고형 장기 이식(SOT) 시술 확대가 예방적 처방을 뒷받침하고 있습니다.

조혈모세포 이식 및 고형 장기 이식 건수가 증가함에 따라, 위험에 노출된 환자층이 확대되고 있으며, 레텔모빌 등의 약물을 이용한 일상적인 예방 조치가 확대되고 있습니다. 전 세계적으로 조혈모세포 이식 수술 건수가 증가하고 있는 만큼, 효과적인 거대세포바이러스(CMV) 예방 및 치료법에 대한 수요는 계속해서 높아지고 있습니다. 이식 후 시클로포스파미드 요법이나 부분적 일치 기증자 프로토콜의 도입으로 기증자 후보의 폭은 넓어졌으나, CMV 재활성화 위험도 높아지면서 저독성 예방제에 대한 수요가 더욱 증가하고 있습니다. 머크사가 신장 이식 분야에서 발표한 3상 임상시험 데이터는 레텔모빌의 임상적 유용성을 확대하는 동시에, 평균 12일의 입원 기간을 단축하는 우수한 안전성 프로파일을 보여주었으며, 광범위한 사용을 뒷받침하는 설득력 있는 약제경제학적 근거를 제시했습니다.

선천성 CMV에 대한 신생아 선별 검사 프로그램 확대

미국에서는 일부 주에서 신생아 CMV 선별검사가 시범 단계에서 벗어나 정책으로 자리 잡아가고 있습니다. 미네소타주에서는 도입 첫해에 184건의 사례가 확인되었으며, 유병률이 0.3%인 것으로 밝혀졌습니다. 또한, 타액 풀 검사의 효율성이 입증되었으며, 개별 검사 횟수를 83% 줄일 수 있음이 확인되었습니다. 조기 발견을 통해 증상이 있는 영아에게 발가시클로비르 치료를 적시에 시작할 수 있게 되었으며, 이는 거대세포바이러스 치료 시장에서 아직 발전 단계에 있는 소아 분야의 성장을 가속하고 있습니다.

기존 항바이러스제의 독성 및 이상반응 프로파일

발가시클로비르로 인한 백혈구 감소증 및 호중구 감소증은 여전히 투여량 감량이나 입원을 초래하고 있으며, 신장 이식 환자의 각각 24.4%와 69.7%에게 영향을 미치고 있습니다. 그 결과 발생하는 의료 자원에 대한 부담은 내약성이 뛰어난 테르미네제 억제제의 경쟁 우위를 강화하는 한편, 거대세포바이러스 치료 시장의 보급 곡선에 단기적인 마찰을 초래하고 있습니다.

부문별 분석

DNA 중합효소 억제제는 2025년 매출의 57.66%를 차지해, 수십 년에 걸쳐 임상 현장에서 확고히 자리 잡았음을 알 수 있습니다. 그러나 임상의들이 골수 독성이 극히 미미하다는 점을 이유로 예방 요법으로 레텔모빌로의 전환을 권장하고 있는 탓에, 터미네제 억제제 시장은 연평균 성장률(CAGR) 11.32%를 기록하며 성장하고 있습니다. 터미네제 억제제를 이용한 거대세포바이러스 치료 시장 규모는 새로운 적응증 승인과 함께 대폭 확대될 것으로 전망됩니다. 한편, UL97 키나아제 억제제나 세포 치료제는 시장 규모는 작지만, 난치성 또는 내성 사례에 대한 전략적 대안이 되어, 첨단 바이오 제조 역량을 갖춘 기업들의 투자를 유치하고 있습니다.

신생 세포 치료 기업들은 생산상의 병목 현상을 극복하기 위해 수탁 제조업체와의 제휴를 추진하고 있습니다. 물류 측면에서 복잡성이 있기는 하지만, 상용화에 성공한다면 근본적인 치료가 가능하며 환자 개개인에 최적화된 솔루션을 제공함으로써 거대세포바이러스 치료 시장을 재정의할 가능성이 있습니다. 이는 기존 항바이러스제 제조업체들에게 파이프라인 다각화를 촉진하고 시장을 뒤흔들 만한 전망입니다.

2025년에도 조혈모세포 이식의 점유율은 45.35%를 유지했으나, 신장, 간, 폐 이식이 전 세계적으로 증가하고 있는 데 따라 고형 장기 이식은 연평균 성장률(CAGR) 12.65%로 확대되고 있습니다. 이러한 성장은 보다 안전한 장기 예방 요법에 대한 수요를 뒷받침하는 한편, 각 개발사들로 하여금 장기별 면역억제 프로토콜에 맞추어 투여량을 조정하도록 유도함으로써, 거대세포바이러스 치료 시장에서 맞춤형 관리로의 전환을 촉진하고 있습니다.

보편적인 선별 검사를 통해 조기 발견이 가능해진 선천성 CMV는 소아 분야라는 새로운 틈새 시장을 개척하고 있습니다. 증상이 있는 영아는 조기 발가시클로비르 투여를 통해 신경 발달 측면에서 측정 가능한 이점을 얻고 있으며, 한편 무증상 사례도 더 조기에 확인될 수 있게 됨에 따라, 거대세포바이러스 치료 시장 전망 잠재 고객 기반이 확대되고 있습니다. 동시에, HIV 및 기타 면역결핍 상태는 안정적인 하위 시장을 형성하고 있으며, 레테르모빌은 전신 염증을 완화하고 면역 지표를 개선할 가능성을 보여주고 있습니다.

지역별 분석

북미는 2025년에 전 세계 매출의 41.12%를 차지했으며, 선진적인 이식 인프라, 풍부한 보험 급여, 그리고 신생아 보편적 선별검사에서 선도적인 입지를 활용하고 있습니다. 신장 이식용 ‘프레비미스(Prevymis)’ 등의 FDA 승인은 해당 지역의 혁신적 우위를 강조하는 동시에, 예방 의학을 더 폭넓은 환자층으로 확대되고 있습니다.

이에 이어 유럽은 성숙한 이식 네트워크와 비용 대비 효과를 고려한 EMA(유럽의약품청) 준수 프로토콜을 갖추고 있습니다. 레테르모빌이 EU 전역에서 빠르게 보급되고 있는 것은 그 안전성과 경제적 가치에 대한 임상의들의 신뢰를 반영하는 한편, 실세계 증거(REW) 프로그램을 통해 전 세계 진료 지침 수립에 도움이 되는 데이터가 도출되고 있습니다. 브렉시트 이후의 조정 과정에도 불구하고 규제 조화는 계속되고 있으며, 다국적 기업들에게 유럽은 거대세포바이러스 치료제의 주요 시장으로서의 위상을 유지하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 11.98%로, 가장 빠르게 성장하고 있는 지역입니다. 2024년 일본에서 ‘리브텐시티’가 승인됨에 따라 최첨단 치료법으로 가는 길이 열렸으며, 중국과 인도에서의 프로그램 확대는 수요가 증가하고 있음을 보여줍니다. 현지 제조 제휴를 통해 비용 경쟁력 있는 공급이 확보되는 한편, 각국의 보험 급여 제도도 고부가가치 항바이러스제를 포함하도록 점차 조정되고 있습니다. 중동 및 아프리카 및 남미는 규모는 작지만, 이식 역량의 향상과 CMV에 대한 인식 제고가 나타나고 있어 장기적인 성장 전망을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, cytomegalovirus treatment market size in 2026 is estimated at USD 367.36 million, growing from 2025 value of USD 345.91 million with 2031 projections showing USD 496.27 million, growing at 6.20% CAGR over 2026-2031.

This report is Segmented by Drug Class (DNA-Polymerase Inhibitors, Terminase Inhibitors, Other Drug Class), Application (Hematopoietic Stem-Cell Transplantation, and More), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cytomegalovirus Treatment Market Trends and Insights

Expansion of HSCT & SOT Procedures Fuelling Prophylactic Prescriptions

Rising hematopoietic stem-cell and solid-organ transplant volumes are enlarging the at-risk population, prompting routine prophylaxis with agents such as letermovir. The increasing number of Hematopoietic Stem Cell Transplantation procedures worldwide continues to strengthen demand for effective cytomegalovirus prevention and treatment therapies. Adoption of post-transplant cyclophosphamide and haploidentical protocols widens donor pools yet heightens CMV reactivation risk, reinforcing demand for low-toxicity prophylactics. Merck's Phase 3 data in kidney transplantation broadened letermovir's clinical utility and showcased superior safety profiles that reduce hospital stays by an average 12 days, creating a compelling pharmacoeconomic case for widespread use.

Expanding Newborn Screening Programs for Congenital CMV

Universal newborn screening has moved from pilot to policy in several US states. Minnesota identified 184 cases during its first year, revealing a 0.3% prevalence and validating pooled-saliva testing efficiencies that cut individual assays by 83%. Early detection permits timely valganciclovir therapy for symptomatic infants and catalyzes a nascent pediatric segment within the cytomegalovirus treatment market.

Toxicity & Adverse-Event Profile of Existing Antivirals

Valganciclovir-induced leukopenia and neutropenia continue to prompt dose reductions and hospitalizations, affecting 24.4% and 69.7% of kidney transplant patients, respectively. The resultant resource burden strengthens the competitive positioning of better-tolerated terminase inhibitors, but it also imposes near-term friction on adoption curves for the cytomegalovirus treatment market.

Other drivers and restraints analyzed in the detailed report include:

- FDA & EMA Approvals of Novel Antivirals

- Shift to Home/Ambulatory Infusion Lowering Treatment Barriers

- Rising Antiviral-Resistant CMV Strains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DNA-polymerase inhibitors accounted for 57.66% of 2025 revenue, underscoring decades of clinical familiarity. Yet, terminase inhibitors are growing at 11.32% CAGR as clinicians pivot to letermovir for prophylaxis, citing negligible myelotoxicity. The cytomegalovirus treatment market size for terminase inhibitors is forecast to swell meaningfully as new indications win approval. Meanwhile, UL97 kinase inhibitors and cell-based therapies, though smaller, provide strategic options for refractory or resistant cases and attract investment from firms with advanced biomanufacturing capacity.

Emerging cell-therapy entrants are forging alliances with contract manufacturers to overcome production bottlenecks. Despite intricate logistics, successful commercialization could redefine the cytomegalovirus treatment market by offering curative, patient-specific solutions, a disruptive prospect that incentivizes incumbent antiviral producers to diversify pipelines.

Hematopoietic stem-cell transplantation maintained a 45.35% share in 2025, yet solid-organ transplantation is advancing at a 12.65% CAGR as kidney, liver, and lung transplants rise globally. This growth underpins demand for safer long-term prophylaxis regimens and pushes developers to tailor dosing to organ-specific immunosuppression protocols, reinforcing the cytomegalovirus treatment market's shift toward personalized management.

Congenital CMV, catalyzed by universal screening, opens a pediatric niche. Symptomatic infants derive measurable neurodevelopmental benefit from early valganciclovir, while asymptomatic cases are now flagged earlier, expanding the cytomegalovirus treatment market's future addressable base. Concurrently, HIV and other immunocompromised conditions represent a steady-state submarket where letermovir shows potential to reduce systemic inflammation and improve immune metrics.

Complete Report Scope:

- By Drug Class

- DNA-Polymerase Inhibitors

- Terminase Inhibitors

- Other Drug Class

- By Application

- Hematopoietic Stem-Cell Transplantation

- Solid-Organ Transplantation

- Congenital CMV Infection

- HIV/AIDS & Other Immunocompromised Conditions

- By Route of Administration

- Oral

- Intravenous

- Topical / Intra-ocular

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-commerce & Specialty Infusion Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.12% of global revenue in 2025, leveraging advanced transplant infrastructure, generous reimbursement, and leadership in universal newborn screening. FDA approvals such as Prevymis for kidney transplantation underscore the region's innovation edge and expand preventive care to broader patient cohorts.

Europe follows with mature transplant networks and EMA-aligned protocols that integrate cost-effectiveness considerations. Rapid pan-EU uptake of letermovir reflects clinician confidence in its safety and economic value, while real-world evidence programs generate data that inform global practice guidelines. Regulatory harmonization continues despite post-Brexit adjustments, sustaining Europe's position as a key cytomegalovirus treatment market for multinational players.

Asia-Pacific is the fastest-growing region at 11.98% CAGR through 2031. Japan's 2024 Livtencity approval opened the gate for cutting-edge therapies, and expanding programs in China and India signal rising demand. Local manufacturing partnerships provide cost-competitive supply, while national reimbursement schemes gradually adjust to include high-value antivirals. Middle East & Africa and South America, though smaller, exhibit improving transplant capabilities and rising CMV awareness, presenting long-term expansion prospects.

- Merck

- Roche

- Gilead Sciences

- Pfizer

- Takeda Pharmaceutical Co.

- Chimerix Inc.

- Clinigen Group

- Fresenius

- Teva Pharmaceutical Industries

- Thermo Fisher Scientific

- Astellas Pharma

- CSL Behring

- AiCuris Anti-infective Cures AG

- Atara Biotherapeutics Inc.

- Moderna

- Abbvie

- Mylan N.V. (Viatris)

- Genentech

- Vical Inc.

- Shionogi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of HSCT & SOT Procedures Fuelling Prophylactic Prescriptions

- 4.2.2 Expanding Newborn-Screening Programs for Congenital CMV

- 4.2.3 FDA & EMA Approvals of Novel Antivirals

- 4.2.4 Shift to Home/Ambulatory Infusion Lowering Treatment Barriers

- 4.2.5 Adoption of CMV-Specific T-Cell Therapies for Refractory Disease

- 4.2.6 Hospital Budget Savings Data Accelerating Letermovir Uptake

- 4.3 Market Restraints

- 4.3.1 Toxicity & Adverse-Event Profile of Existing Antivirals

- 4.3.2 Rising Antiviral-Resistant CMV Strains

- 4.3.3 Reimbursement Hurdles for Novel Prophylaxis

- 4.3.4 Manufacturing Complexity for Cell-Based CMV Therapies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Drug Class

- 5.1.1 DNA-Polymerase Inhibitors

- 5.1.2 Terminase Inhibitors

- 5.1.3 Other Drug Class

- 5.2 By Application

- 5.2.1 Hematopoietic Stem-Cell Transplantation

- 5.2.2 Solid-Organ Transplantation

- 5.2.3 Congenital CMV Infection

- 5.2.4 HIV/AIDS & Other Immunocompromised Conditions

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

- 5.3.3 Topical / Intra-ocular

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 E-commerce & Specialty Infusion Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Merck & Co. Inc.

- 6.3.2 F. Hoffmann-La Roche Ltd

- 6.3.3 Gilead Sciences Inc.

- 6.3.4 Pfizer Inc.

- 6.3.5 Takeda Pharmaceutical Co.

- 6.3.6 Chimerix Inc.

- 6.3.7 Clinigen Group PLC

- 6.3.8 Fresenius Kabi

- 6.3.9 Teva Pharmaceutical Industries Ltd

- 6.3.10 Thermo Fisher Scientific Inc.

- 6.3.11 Astellas Pharma Inc.

- 6.3.12 CSL Behring

- 6.3.13 AiCuris Anti-infective Cures AG

- 6.3.14 Atara Biotherapeutics Inc.

- 6.3.15 Moderna Inc.

- 6.3.16 AbbVie Inc.

- 6.3.17 Mylan N.V. (Viatris)

- 6.3.18 Genentech Inc.

- 6.3.19 Vical Inc.

- 6.3.20 Shionogi & Co. Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment