|

시장보고서

상품코드

2072501

1,6-헥산디올 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)1,6-Hexanediol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

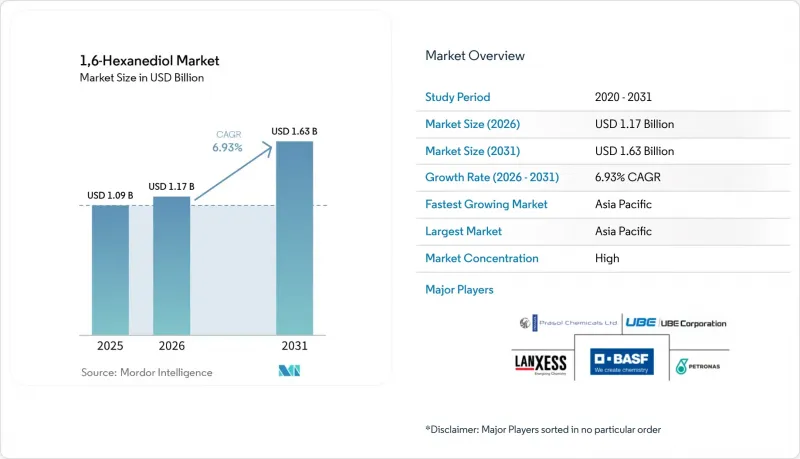

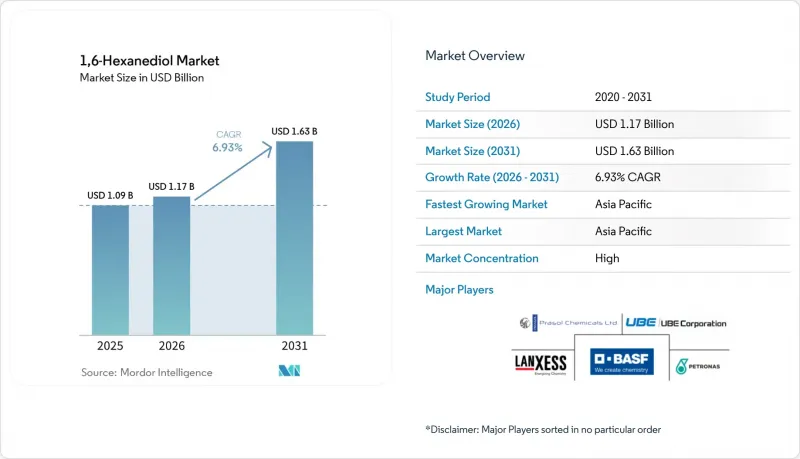

Mordor Intelligence에 의하면, 1,6-헥산디올 시장 규모는 2025년에 10억 9,000만 달러로 평가되었습니다. 2026년 11억 7,000만 달러에서 2031년까지 16억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.93%를 나타낼 전망입니다.

본 보고서는 원료(시클로헥산, 아디핀산), 제조 공정(2단계법 : 시클로헥사논-아디핀산 수소화법 등), 순도 등급(99% 이상의 고순도, 99% 미만의 산업용 등급), 용도(폴리우레탄, 코팅, 아크릴레이트 등), 그리고 지역(아시아태평양, 북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 1,6-헥산디올 시장 동향 및 분석

풍력 터빈 블레이드용 복합재료에서 폴리우레탄 수요 증가

세계의 육상 및 해상 풍력 발전 설비에서는 더 긴 블레이드와 더 높은 선단 속도가 요구되고 있으며, 이에 따라 복합재료 매트릭스에 대한 피로 및 내후성 요구 사항이 높아지고 있습니다. 1,6-헥산디올로 가공된 폴리우레탄은 우수한 엘라스토머로서의 인성을 발휘하여, 내구성을 저해하지 않으면서 프로파일을 얇게 만들 수 있습니다. 기기 OEM 제조업체들은 재활용성을 최우선으로 고려하고 있으며, 이 지올을 함유한 재활용 가능한 폴리우레탄 화학 물질이 프로토타입 블레이드에서 에폭시계 시스템을 점차 대체하고 있습니다. 정부의 청정 에너지 의무화 정책과 기업의 탄소중립 목표에 힘입어, 터빈 부품에 대한 수년에 걸친 조달 파이프라인이 유지되고 있으며, 이는 소재 혁신이 단기적인 대량 수주로 이어지고 있습니다. 라이프사이클 분석에 따르면, 폴리우레탄 재질의 블레이드는 에폭시 재질에 비해 질량을 10% 줄일 수 있는 가능성이 있으며, 이를 통해 소폭의 비용 증가를 상쇄하고도 남을 만큼 물류 측면에서의 이점과 타워에 가해지는 부하 경감이라는 이점을 얻을 수 있습니다. 수명 연장과 더불어, 이러한 기술적 진보는 고기능성 폴리우레탄에 대한 수요를 높임으로써, 결과적으로 1,6-헥산디올 시장 수요를 끌어올리고 있습니다.

확대되는 분말 및 UV 경화형 산업용 코팅 시장

각 제조업체는 VOC 배출량 감축과 타크트 타임 단축을 위해 UV 경화식 및 분체 도장 라인을 도입하고 있습니다. 1,6-헥산디올로 합성된 올리고머는 높은 가교 밀도를 보이며, LED 램프 아래에서 수 초 이내에 경화되는 한편, 63 MPa를 초과하는 인장 강도에 도달합니다. 각 제조업체는 VOC 배출량 감축과 타크트 타임 단축을 위해 UV 경화형 및 분체 도장 라인을 도입하고 있습니다. 1,6-헥산디올로 합성된 올리고머는 높은 가교 밀도를 보이며, LED 램프 아래에서 수 초 이내에 경화되면서 63 MPa를 초과하는 인장 강도에 도달합니다. 아시아태평양의 가전·가구 제조업체들은 연속식 분체 도장 라인을 확대하고 있으며, 북미의 자동차 제조업체들은 범퍼 및 트림의 제조 공정에 UV 터널을 도입하여 설비를 개조하고 있어, 이에 따라 해당 시장 규모가 확대되고 있습니다. 에너지 소비량이 많은 오븐이 필요 없어짐에 따라 투자 회수 기간이 단축되어, 비용 절감과 지속가능성 목표를 동시에 달성하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 코팅용 디올에 대한 수요가 산업 생산 전체의 성장률을 웃도는 속도로 증가하고 있습니다.

아디핀산 및 사이클로헥산 가격 변동

1,6-헥산디올의 가격은 현물 시장의 아지핀산 및 벤젠 가격 변동에 뒤이어 변동하기 때문에 원자재 가격 변동이 이익률을 위협하고 있습니다. 중국에서 가동을 시작한 연간 생산량 1,180만 톤 규모의 신규 방향족 복합 시설은 통합 제조업체의 비용을 절감하는 한편, 전 세계적인 공급 과잉을 더욱 심화시켜 가격을 최저 수준으로 떨어뜨리고, 독립 생산 업체들을 불안에 빠뜨리고 있습니다. 생산자들은 장기 계약을 통한 헤지나 선택적인 후방 통합을 통해 대응하고 있지만, 특히 시판되는 아지핀산에 의존하는 아시아 수출업체들에게는 재고 위험이 여전히 남아 있습니다. 정유시설 통합 및 생산 능력 합리화를 통해 중기적인 안정성이 예상되는 반면, 단기적인 가격 변동으로 인해 재무 측면에서 보수적인 태도가 요구됨에 따라, 1,6-헥산디올 시장에서 재량적인 생산 능력 확충이 지연될 가능성이 있습니다.

부문별 분석

2025년 생산량 중 시클로헥산이 54.12%를 차지했습니다. 이는 수직 통합형 석유화학 단지가 원료의 안정적인 공급과 규모의 경제를 보장하고 있으며, 이것이 해당 부문의 1,6-헥산디올 시장 규모를 뒷받침하고 있기 때문입니다. 시클로헥산의 전환율을 60.6%로 높이고, 아디핀산의 선택성을 85%로 끌어올리는 VPO 복합 촉매를 포함한 기술 혁신을 통해 N2O 배출량이 억제되고, 경쟁력이 유지되고 있습니다.

마이크로 리액터를 이용한 산화법에서는 체류 시간 단축과 배기가스량 감소를 통해 93%의 수율을 달성할 수 있기 때문에 아디핀산을 원료로 사용하는 양은 연평균 성장률(CAGR) 7.18%를 기록하며 더욱 빠르게 증가하고 있습니다. FDCA를 원료로 하는 바이오 유래 아디핀산은 재생 가능 자원으로의 전환을 더욱 촉진하고 있지만, 비용은 여전히 시클로헥산 유래 경로보다 높은 임베디드니다. 발효에서 유래한 디올은 현재 틈새 시장이지만, 벤처 자금 조달과 파일럿 라인 확장이 잇따르고 있으며, 탄소 가격 제도가 강화될 경우 2030년 이후 시클로헥산 시장 점유율을 잠식할 가능성이 있습니다. 그 결과, 원자재 동향은 1,6-헥산디올 시장을 형성하는 광범위한 변화의 힘을 반영하고 있습니다.

2단계 사이클로헥사논-아디핀산 수소화 공정은 2025년 생산량의 83.75%를 차지하며, 수십 년에 걸친 촉매 개선과 플랜트의 병목 현상 해소를 통해 확립된 1,6-헥산디올 시장 점유율을 뒷받침했습니다. 이 생산 경로가 지닌 학습 곡선의 우위 덕분에, 에너지 가격 변동에도 불구하고 현금 비용 측면에서 우위를 유지하고 있으며, 기존 공장의 개조를 통한 생산 능력 확대에 따라 2031년까지 연평균 성장률(CAGR)은 7.42%를 나타낼 것으로 전망됩니다. BASF의 샬람 복합 시설 등, 헥사메틸렌디아민 제조 설비와의 통합을 통해 제품별 부가가치 창출과 유틸리티 공유가 촉진될 것입니다.

카프로락톤의 직접 1단계 수소화 공정은 단위 조작을 단순화하지만, 선택성 저하 및 촉매 수명 단축이라는 과제에 직면해 있어, 그 적용은 초고순도 등급을 목표로 하는 특수 플랜트로 제한되고 있습니다. 바이오 발효 및 촉매를 통한 업그레이드 공정은 원료 가격이 낮은 경우 가장 높은 성장률을 보이고 있으며, 유럽과 북미에서는 생산자들이 당을 디올로 전환하는 제조 공정을 시범적으로 도입하고 있습니다. 에보닉의 난징에 위치한 특수 아민 생산 기지에서는 친환경 전력과 첨단 자동화 기술을 도입하고 있으며, 이는 디지털화와 재생에너지가 신기술 공정의 비용 격차를 해소할 수 있음을 보여주고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 47.05%를 차지했으며, 연평균 성장률(CAGR)은 7.86%로 전망됩니다. 중국의 통합형 방향족 화합물 허브는 비용 경쟁력의 기반이 되고 있지만, 배출 규제가 강화됨에 따라 생산자들은 촉매를 이용한 N2O 저감 기술을 도입하거나 바이오 시범 생산 라인에 투자해야 하는 상황에 직면해 있습니다. 일본과 한국은 광학용 폴리머 및 배터리용 바인더에 사용되는 고순도 등급에 대한 수요를 창출함으로써, 해당 지역의 부가가치 밀도를 높이고 있습니다. 아세안 국가들은 가전제품용 단열재 및 신발용 폴리우레탄 폼 공장을 확대하고 있지만, 여전히 지올의 순수입국으로 남아 있습니다.

북미에서는 풍력 터빈 블레이드 건설 확대와 적층 가공의 확산이 호재로 작용하며 생산량 증가를 이끌고 있습니다. UBE 코퍼레이션이 루이지애나주에서 추진 중인, 탄산염 용매 및 업스트림 공정용 디올 중간체를 생산하는 5억 달러 규모의 프로젝트는 미국의 청정 에너지 우대 조치에 따른 해외 자본 유입을 여실히 보여주고 있습니다.

유럽은 비용 면에서의 불리함을 극복해 나가면서도, 공정의 집약화와 지속가능성에 관한 혁신을 통해 기술적 리더십이라는 틈새 시장을 유지하고 있습니다. BASF사의 샬람프(Chalampe) 공장 가동 개시와 알사시미에(Alsachimie)와의 합작 사업 통합으로 원료 선택의 폭이 넓어지는 한편, 스코프 3 보고가 고객 계약에 포함되고 있습니다.

남미 및 중동 및 아프리카에서 사우디아라비아의 석유화학 사업 다각화와 브라질의 폴리우레탄 하류 부문 확충은 장기적인 성장 여지가 더욱 확대될 것임을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the 1,6-Hexanediol market size was valued at USD 1.09 billion in 2025 and estimated to grow from USD 1.17 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 6.93% during the forecast period (2026-2031).

This report is Segmented by Raw Material (Cyclohexane, Adipic Acid), Manufacturing Process (Two-Step Cyclohexanone - Adipic-Acid Hydrogenation, and More), Purity Grade (More Than or Equal To 99% High-Purity, Less Than 99% Industrial-Grade), Application (Polyurethane, Coatings, Acrylates, and More) and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global 1,6-Hexanediol Market Trends and Insights

Rising Polyurethane Demand in Wind-Turbine Blade Composites

Global onshore and offshore wind installations specify longer blades and higher tip speeds, heightening fatigue and weathering requirements for composite matrices. Polyurethanes extended with 1,6-hexanediol supply superior elastomeric toughness, enabling thinner profiles without sacrificing durability. Equipment OEMs prioritize recyclability, and recyclable polyurethane chemistries incorporating the diol increasingly displace epoxy systems in prototype blades. Government clean-energy mandates and corporate net-zero targets sustain multiyear procurement pipelines for turbine components, converting material innovations into near-term volume orders. Lifecycle models show polyurethane blades may reduce mass by 10% versus epoxy, yielding logistics and tower-load benefits that outweigh marginal cost increases. Coupled with service-life extensions, these technical gains lift demand for high-functionality polyurethanes and, by extension, the 1,6-hexanediol market.

Expanding Powder and UV-Curable Industrial Coatings Market

Manufacturers adopt UV-curable and powder-coating lines to cut VOC emissions and accelerate takt times. Oligomers synthesized from 1,6-hexanediol demonstrate high crosslink density, reaching tensile strengths above 63 MPa while curing within seconds under LED lamps. Manufacturers adopt UV-curable and powder-coating lines to cut VOC emissions and accelerate takt times. Oligomers synthesized from 1,6-hexanediol demonstrate high crosslink density, reaching tensile strengths above 63 MPa while curing within seconds under LED lamps. Asia-Pacific appliance and furniture plants scale continuous powder-coat lines, and North American automakers retrofit bumpers and trim operations with UV tunnels, enlarging the addressable base. Capital payback improves as energy-intensive ovens are eliminated, aligning cost savings with sustainability targets. These factors converge to elevate coating-grade diol demand ahead of broader industrial output growth.

Volatility in Adipic-Acid and Cyclohexane Prices

Feedstock swings threaten margins because 1,6-hexanediol pricing lags spot adipic acid and benzene cycles. China's new 11.8 million tons/year aromatics complexes narrow integrators' costs but also amplify global oversupply, triggering price troughs that unsettle independent producers. Producers respond through term-contract hedging and selective backward integration, yet inventory risk persists, particularly for Asian exporters reliant on merchant adipic acid. Although refinery consolidation and capacity rationalization promise medium-term stability, near-term volatility compels balance-sheet conservatism and may delay discretionary capacity additions in the 1,6-hexanediol market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in TPU-Based 3D-Printing Filaments

- Transition Toward Bio-Based C6 Diols from Oil-Seed Feedstocks

- N2O-Emission Regulations on Adipic-Acid Producers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cyclohexane accounted for 54.12% of 2025 volumes as vertically integrated petrochemical complexes guarantee feed continuity and scale economies that anchor the 1,6-hexanediol market size for this segment. Technology upgrades, including VPO composite catalysts that push 60.6% cyclohexane conversion with 85% adipic-acid selectivity, temper N2O emissions and sustain competitiveness.

Adipic-acid feedstock usage climbs faster at 7.18% CAGR as microreactor oxidation achieves 93% yields with shortened residence times and reduced off-gas streams. Bio-derived adipic acid sourced from FDCA furthers the renewable pivot, but costs remain above cyclohexane routes. Fermentation-based diols, though currently a niche, draw venture funding and pilot-line expansions that could erode cyclohexane's share beyond 2030 if carbon-pricing schemes intensify. Consequently, raw-material dynamics embody the wider transition forces shaping the 1,6-hexanediol market.

The two-step cyclohexanone - adipic-acid hydrogenation route generated 83.75% of 2025 output, anchoring a 1,6-hexanediol market share entrenched by decades of catalyst refinement and plant debottlenecking. This pathway's learning-curve advantages keep cash-cost leadership despite energy-price volatility, fostering a 7.42% CAGR to 2031 as brownfield upgrades stretch capacity. Integration with hexamethylenediamine facilities, such as BASF's Chalampe complex, enhances by-product valorization and utilities sharing.

Direct one-step hydrogenation of caprolactone simplifies unit operations but battles lower selectivity and shorter catalyst life, limiting uptake to specialty plants targeting ultra-high-purity grades. Bio-fermentation and catalytic upgrading deliver the highest growth, albeit from a low base, as producers trial sugar-to-diol routes in Europe and North America. Evonik's specialty amine unit in Nanjing uses green electricity and advanced automation, illustrating how digitalization and renewable power can close cost gaps in emerging processes.

Complete Report Scope:

- By Raw Material

- Cyclohexane

- Adipic Acid

- By Manufacturing Process

- Two-step Cyclohexanone - Adipic-Acid Hydrogenation

- Direct One-step Hydrogenation of Caprolactone

- Bio-fermentation and Catalytic Upgrading

- By Purity Grade

- Greater than equal to 99% (High-Purity)

- Less than 99% (Industrial-Grade)

- By Application

- Polyurethane

- Coatings

- Acrylates

- Adhesives

- Polyester Resins

- Plasticizers

- Other Applications (3D-Printing Photopolymers, etc.)

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific generated 47.05% of global revenue in 2025, and a 7.86% CAGR outlook. China's integrated aromatics hubs anchor cost leadership, yet stricter emission norms push producers to adopt catalytic N2O abatement and invest in bio-based pilot lines. Japan and South Korea channel demand into high-purity grades used in optical polymers and battery binders, reinforcing the region's value density. ASEAN nations scale polyurethane foam plants for appliance insulation and footwear, but remain net importers of the diol.

North America is leveraged by wind-turbine blade buildouts and additive-manufacturing expansion, driving incremental volumes. UBE Corporation's USD 500 million Louisiana project to produce carbonate solvents and upstream diol intermediates underscores overseas capital inflows tied to U.S. clean-energy incentives.

Europe, while battling cost disadvantages, preserves a technological-leadership niche through process-intensification and sustainability innovation. BASF's Chalampe start-up and Alsachimie joint-venture consolidation broaden feedstock optionality while embedding Scope 3 reporting into customer contracts.

South America, and the Middle East and Africa's petrochemical diversification in Saudi Arabia and Brazil's polyurethane downstream build-out hint at higher long-term growth runways.

- BASF

- Central Drug House

- Evonik Industries AG

- Hefei TNJ Chemical Industry Co.,Ltd.

- LANXESS

- PETRONAS Chemicals Group Berhad

- Prasol Chemicals Ltd.

- Santa Cruz Biotechnology Inc.

- Shandong Haili Chemical Industry

- UBE Corporation

- Weicheng New Materials (Shandong) Co., Ltd

- Zhejiang Boju New Materials Co., Ltd.

- Zhejiang Lishui Nanming Chemical

- Zhengzhou Meiya Chemical Products Co.,Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Polyurethane Demand in Wind-Turbine Blade Composites

- 4.2.2 Expanding Powder and UV-Curable Industrial Coatings Market

- 4.2.3 Growth in TPU-Based 3D-Printing Filaments

- 4.2.4 Transition toward Bio-Based C6 Diols from Oil-Seed Feedstocks

- 4.2.5 High-Refractive-Index Optical Polymers for AR/VR Lenses

- 4.3 Market Restraints

- 4.3.1 Volatility in Adipic-Acid and Cyclohexane Prices

- 4.3.2 Availability of Functional Substitutes (1,5-Pentanediol, 1,4-Butanediol)

- 4.3.3 N?O-Emission Regulations on Adipic-Acid Producers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Price Trend Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Cyclohexane

- 5.1.2 Adipic Acid

- 5.2 By Manufacturing Process

- 5.2.1 Two-step Cyclohexanone - Adipic-Acid Hydrogenation

- 5.2.2 Direct One-step Hydrogenation of Caprolactone

- 5.2.3 Bio-fermentation and Catalytic Upgrading

- 5.3 By Purity Grade

- 5.3.1 Greater than equal to 99% (High-Purity)

- 5.3.2 Less than 99% (Industrial-Grade)

- 5.4 By Application

- 5.4.1 Polyurethane

- 5.4.2 Coatings

- 5.4.3 Acrylates

- 5.4.4 Adhesives

- 5.4.5 Polyester Resins

- 5.4.6 Plasticizers

- 5.4.7 Other Applications (3D-Printing Photopolymers, etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JV, Capacity Expansions, Off-take)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Central Drug House

- 6.4.3 Evonik Industries AG

- 6.4.4 Hefei TNJ Chemical Industry Co.,Ltd.

- 6.4.5 LANXESS

- 6.4.6 PETRONAS Chemicals Group Berhad

- 6.4.7 Prasol Chemicals Ltd.

- 6.4.8 Santa Cruz Biotechnology Inc.

- 6.4.9 Shandong Haili Chemical Industry

- 6.4.10 UBE Corporation

- 6.4.11 Weicheng New Materials (Shandong) Co., Ltd

- 6.4.12 Zhejiang Boju New Materials Co., Ltd.

- 6.4.13 Zhejiang Lishui Nanming Chemical

- 6.4.14 Zhengzhou Meiya Chemical Products Co.,Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Advancement in Technology and Development of Bio-Based Raw Material