|

시장보고서

상품코드

2072513

미국의 벙커 연료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

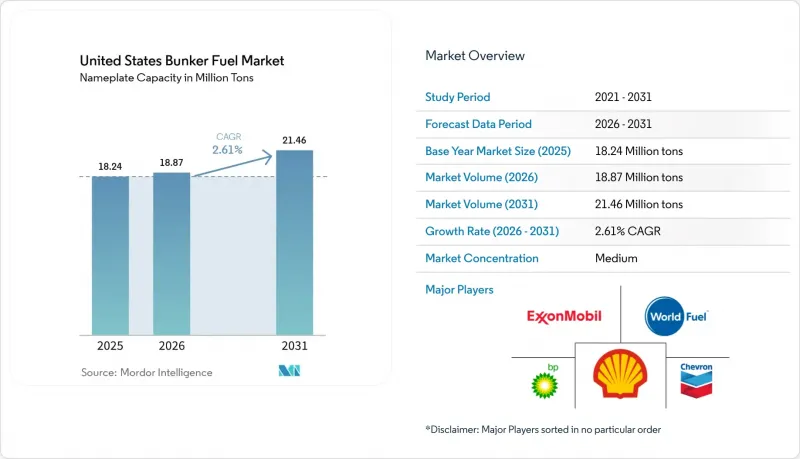

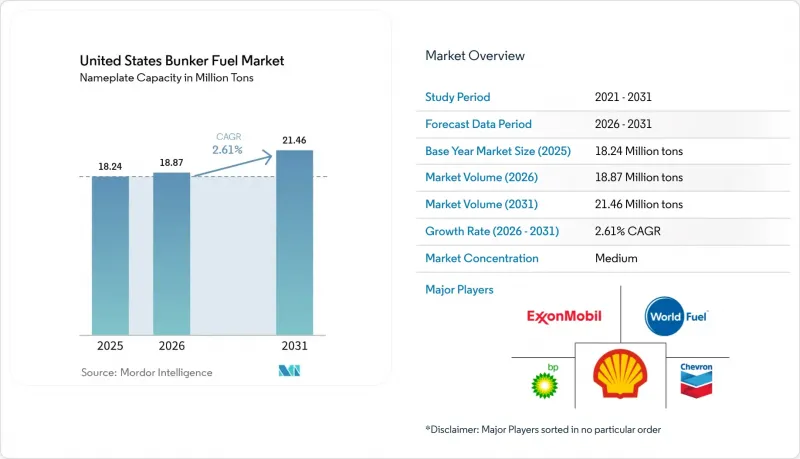

Mordor Intelligence에 의하면, 미국의 벙커 연료 시장 규모(정격 용량 기반)는 2025년에 1,824만 톤으로 평가되었습니다. 2026년 1,887만 톤에서 2031년까지 2,146만 톤에 이를 것으로 예상되며, 예측 기간(2026-2031년) 중에 CAGR 2.61%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 연료 유형(HSFO, VLSFO, ULSFO, MGO, LNG, 메탄올, 바이오/합성 연료, 암모니아 등), 급유 방법(선박 대 선박, 항만 대 선박, LNG 바지선 대 선박, 이동식 탱크·컨테이너), 그리고 선박 유형(컨테이너선, 유조선, 벌크선, 일반 화물선, 여객·로팍스선, 해양·특수선)별로 분류되어 있습니다. 시장 규모 및 전망은 수량(MT) 기준으로 제시되어 있습니다.

미국의 벙커 연료 시장 동향 및 인사이트

IMO 2020년 황 함량 규제에 따른 수요 급증

동해안 정유시설의 설비 구성 미비로 인해, 잔류유 개질 설비를 갖춘 멕시코만 연안 정유시설로 공급을 재편할 수밖에 없게 되었으며, 이에 따라 현물 구매 리드타임이 길어졌습니다. HSFO와 VLSFO의 가격 차이가 좁혀져 현재 1미터톤당 50달러 가까이 되었기 때문에 신규 스크러버 후설치 개조에 대한 투자의 타당성이 사라지면서 더 많은 선사들이 규제 준수 연료 사용을 선택할 수밖에 없는 상황에 처해 있습니다. 이미 운항 중인 스크러버 장착 선박은 계속해서 HSFO를 소비하고 있지만, 캘리포니아주와 코네티컷주의 세정수 규제 강화로 인해 오픈 루프 시스템의 사용이 제한되면서 지리적 유연성이 떨어지고 있습니다. 2025년에는 미국 해안경비대 검사관들이 주요 컨테이너선 및 유조선의 입항 항구에서 시료 채취를 강화한 결과, 유황 규제 위반으로 인한 억류 건수가 18% 증가했습니다. 이러한 요인들이 복합적으로 작용하여, 미국 내 선박용 연료 시장에서 VLSFO 수요의 기반이 되는 규정 준수 프리미엄이 안정적으로 유지되고 있습니다.

미국의 LNG 벙커링 인프라 확충

6,500만 달러가 넘는 연방 및 주 정부 보조금을 통해 로스앤젤레스와 잭슨빌의 육상 LNG 시설 착공이 촉진되었으며, 2026년 이후 취항할 듀얼 연료 방식의 컨테이너선 및 크루즈선의 운항이 지원되고 있습니다. 휴스턴 선박 수로공급업체는 기존 액화 터미널을 활용하여 해상에서 선박 간 이송을 진행하고 있으며, 이를 통해 바지선을 이용한 배송에 비해 LNG 공급 비용을 15% 절감하고 있습니다. 2025년 3월, 잭슨빌에서 존스법에 부합하는 최초의 1만 2,000입방미터급 LNG 벙커 바지가 취항하여, 급유 시간을 40% 단축함으로써 연안 지역의 효율성에 새로운 기준을 세웠습니다. 메탄 누출에 대한 우려를 반영하여 미국 환경보호청(EPA)은 엔진 탑재형 모니터링 시스템의 도입을 제안했으나, 이로 인해 신조선의 비용이 50만 달러 증가할 가능성이 있습니다. 그러나 OEM 각사는 미끄러짐을 70% 줄일 수 있다고 내세우는 폐쇄형 연소 시스템을 도입하고 있습니다. 카니발 코퍼레이션과 로얄 캐리비안이 향후 취항 예정인 12척의 크루즈선에 LNG를 조기에 도입함으로써 수요 기반이 확보되었고, 추가 인프라 투자에 따른 위험이 완화되었습니다.

LNG 벙커링 자산의 높은 자본 비용

전용 설계된 LNG 바지의 건설비는 4,000만-6,000만 달러, 육상 시설은 8,000만 달러를 초과하지만, 중소규모 항만에서는 운송량의 확실성이 보장되지 않으면 이러한 막대한 자본 비용을 충당하기 어렵습니다. 2026년 초, 존스법에 부합하는 LNG 바지선은 단 3척밖에 운항하지 않아, 연안 항로에서 공급 부족이 발생했으며, 트럭에서 선박으로 화물을 환적할 수밖에 없는 상황이었습니다. 이로 인해 납품 가격이 최대 30%까지 급등하고 있습니다. 대출 기관들이 암모니아나 수소로 인한 시장 혼란의 위험을 반영한 결과, 대출 조건이 엄격해졌으며, 자기자본비율은 40% 이상으로 상향 조정되었고, 허들 레이트는 15% 가까이 상승했습니다. 휴스턴에서는 수요의 불확실성을 이유로 2025년 말 예정이던 9,000만 달러 규모의 LNG 터미널 건설이 연기되었으며, 항만 당국 사이에서는 여전히 신중한 태도를 보였습니다. 보다 장기적인 공급 계약이 체결될 때까지는 주요 허브 이외의 지역에서 LNG 인프라 확충이 시장 전체 수요를 따라가지 못하는 상황이 지속될 것입니다.

부문별 분석

2025년, VLSFO는 미국의 벙커 연료 시장 규모의 40.63%를 차지하며, 광범위한 선단의 규제 준수 수요를 뒷받침했습니다. LNG 시장은 듀얼 연료 신조선의 인도와 2028년까지 예정된 3척의 신규 벙커 바지선 취항에 힘입어 연평균 9.1%의 성장세가 예상되며, 이를 통해 운항 사업자들에게는 2030년 배출 목표를 달성하기 위한 현실적인 로드맵이 제시되고 있습니다. MGO 및 ULSFO는 엔진의 단순성이 추가 비용을 상쇄하는 해양 지원선 분야에서 틈새 시장에서의 입지를 유지하고 있습니다. HSFO 수요는 스크러버를 장착한 유조선과 벌크선을 중심으로 안정적이지만, 연안 배출 규제가 강화됨에 따라 시장 규모가 축소되고 있습니다. 메탄올과 암모니아는 여전히 상용화 전 단계에 있지만, 멕시코만 연안 지역에서는 30억 달러 이상의 생산 능력이 발표된 바 있어, 2028년 이후 미국 선박용 연료 시장의 구도가 재편될 가능성을 시사하고 있습니다.

LNG의 낮은 에너지 밀도는 풍부한 국내 가스 공급으로 인한 낮은 공급 비용 덕분에 부분적으로 상쇄되고 있습니다. VLSFO의 성장세가 둔화되고 있는데, 이는 선주들이 장기적인 탄소 관련 책임과 단기적인 자본 유연성 사이에서 균형을 맞추고 있기 때문입니다. 이러한 갈등은 예측 기간 동안 선단 전체의 조달 방침에 큰 영향을 미칠 가능성이 높습니다. 그린 메탄올은 마스크사와 체결한 20만 메트르톤 규모의 인수 계약을 계기로 신뢰도를 높이고 있으며, 이 계약은 향후 계약 체결을 위한 가격 기준이 되고 있습니다. 바이오블렌드 연료는 서부 해안 지역에서 경쟁력 있는 공급 비용을 지원하는 LCFS 크레딧의 대상이 되지만, 원료 부족으로 인해 당분간 공급량이 제한되고 있습니다. 이러한 다연료화의 현실을 감안할 때, 공급업체들은 미국의 선박용 연료 시장에서 다양한 연료 포트폴리오를 유지할 필요성이 강조되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the united states bunker fuel market size in terms of nameplate capacity was valued at 18.24 million tons in 2025 and is estimated to grow from 18.87 million tons in 2026 to reach 21.46 million tons by 2031, at a CAGR of 2.61% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (HSFO, VLSFO, ULSFO, MGO, LNG, Methanol, Bio-/Synthetic Fuels, Ammonia, and More), Bunkering Method (Ship-To-Ship, Port-To-Ship, LNG Barge-To-Ship, and Portable Tanks and Containers), and Vessel Type (Container, Tanker, Bulk Carrier, General Cargo, Passenger/Ro-Pax, and Offshore and Specialized). The Market Sizes and Forecasts are Provided in Terms of Volume (MT)

United States Bunker Fuel Market Trends and Insights

IMO 2020 sulfur-cap compliance surge

Refinery configuration gaps on the East Coast forced supply realignment toward Gulf plants that possess residue-upgrading hardware, creating longer lead times for spot purchases. The narrowing HSFO-VLSFO spread, now near USD 50 per metric ton, has erased the investment case for new scrubber retrofits, locking more operators into compliant fuels. Scrubber-equipped vessels already on the water continue to consume HSFO, but stricter wash-water restrictions in California and Connecticut are curbing open-loop systems and reducing geographic flexibility. Detentions for sulfur violations rose 18% in 2025 as U.S. Coast Guard inspectors intensified sampling at major container and tanker gateways. Collectively, these factors stabilize the compliance premium that underpins VLSFO demand inside the United States bunker fuel market.

Expansion of U.S. LNG Bunkering Infrastructure

Federal and state grants exceeding USD 65 million have catalyzed groundbreaking for shore-based LNG facilities at Los Angeles and Jacksonville, supporting dual-fuel container and cruise tonnage arriving from 2026 onward. Houston Ship Channel suppliers exploit existing liquefaction terminals for offshore ship-to-ship transfers, shaving 15% from delivered LNG costs relative to barge deliveries. The first 12,000-cubic-meter Jones Act-compliant LNG bunker barge entered service at Jacksonville in March 2025 and cut fueling time by 40%, setting a new benchmark for coastal efficiency. Methane-slip concerns prompted the Environmental Protection Agency to propose on-engine monitoring that could add USD 0.5 million to newbuilds, but OEMs are rolling out closed-loop combustion systems that claim 70% slip reduction. Early LNG adoption by Carnival Corporation and Royal Caribbean for twelve forthcoming cruise ships secures a demand anchor that de-risks additional infrastructure commitments.

High Capital Cost of LNG Bunkering Assets

Purpose-built LNG barges cost USD 40-60 million while shore installations exceed USD 80 million, capital levels that smaller ports struggle to underwrite without volume certainty. Only three Jones Act-compliant LNG barges were in service by early 2026, creating supply gaps on coastal trades and forcing truck-to-ship transfers that inflate delivered prices by up to 30%. Financing terms have tightened as lenders factor in ammonia and hydrogen disruption risk, pushing equity requirements above 40% and hurdle rates toward 15%. Houston deferred a USD 90 million LNG terminal in late 2025 over demand uncertainty, signaling continued caution among port authorities. Until more long-term offtake contracts materialize, LNG infrastructure growth outside core hubs will lag broader market needs.

Other drivers and restraints analyzed in the detailed report include:

- Growing U.S. Tanker and Container Traffic

- Renewable Bio-Blend Bunkers Driven by California LCFS

- Crude-Price Volatility Impacting Fuel Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VLSFO accounted for 40.63% of the United States bunker fuel market size in 2025, anchoring compliance demand for the broader fleet. LNG is forecast to expand at 9.1% annually, supported by dual-fuel newbuild deliveries and three new bunker barges scheduled before 2028, giving operators a viable pathway to meet 2030 emissions targets. MGO and ULSFO retain niche roles among offshore support vessels where engine simplicity outweighs the cost premium. HSFO demand has stabilized around scrubber-equipped tankers and bulk carriers but faces geographic shrinkage as coastal discharge rules tighten. Methanol and ammonia remain pre-commercial yet have more than USD 3 billion in announced capacity along the Gulf Coast, signaling a potential reshuffling of the United States bunker fuel market landscape after 2028.

LNG's energy-density disadvantage is partially offset by lower delivered costs linked to abundant domestic gas. VLSFO growth is slowing as owners weigh long-term carbon liability against short-term capital flexibility, a tension likely to define fleet-wide procurement through the forecast horizon. Green methanol gains credibility following Maersk's 200,000-metric-ton offtake deal, which sets a pricing benchmark for additional contracts. Bio-blends qualify for LCFS credits that subsidize a competitive delivered cost on the West Coast, yet feedstock scarcity caps immediate volume. The multi-fuel reality underscores the need for suppliers to maintain diversified fuel portfolios within the United States bunker fuel market.

Complete Report Scope:

- By Fuel Type

- High-Sulfur Fuel Oil (HSFO)

- Very-Low-Sulfur Fuel Oil (VLSFO)

- Ultra-Low-Sulfur Fuel Oil (ULSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Bio-/Synthetic Fuels

- Ammonia

- Other Fuel Types

- By Bunkering Method

- Ship-to-Ship

- Port-to-Ship (Truck/Pipeline)

- LNG Barge-to-Ship

- Portable Tanks and Containers

- By Vessel Type

- Container

- Tanker

- Bulk Carrier

- General Cargo

- Passenger/Ro-Pax

- Offshore and Specialized

List of Companies Covered in this Report:

- Exxon Mobil Corporation

- Shell Plc

- Chevron Corporation

- BP Plc

- TotalEnergies SE

- World Fuel Services Corp.

- NUStar Energy L.P.

- Phillips 66

- Marathon Petroleum Corp.

- Valero Energy Corp.

- Trafigura Group Pte. Ltd.

- Glencore Plc

- Peninsula Petroleum

- Crowley Maritime Corp.

- Seacor Holdings

- Kinder Morgan Inc.

- Global Gas & Oil Trading LLC

- Clipper Oil

- Sprague Operating Resources

- Pilot Thomas Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IMO 2020 sulfur-cap compliance surge

- 4.2.2 Expansion of U.S. LNG bunkering infrastructure

- 4.2.3 Growing U.S. tanker & container traffic

- 4.2.4 Cruise-line demand for low-sulfur fuels

- 4.2.5 Renewable bio-blend bunkers driven by California LCFS

- 4.2.6 IRA tax credits catalyzing green-methanol supply

- 4.3 Market Restraints

- 4.3.1 High capital cost of LNG bunkering assets

- 4.3.2 Crude-price volatility impacting fuel economics

- 4.3.3 Retrofit scrubbers reducing LS-fuel consumption

- 4.3.4 Prospective carbon-levy shifting investment away

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 High-Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-Low-Sulfur Fuel Oil (VLSFO)

- 5.1.3 Ultra-Low-Sulfur Fuel Oil (ULSFO)

- 5.1.4 Marine Gas Oil (MGO)

- 5.1.5 Liquefied Natural Gas (LNG)

- 5.1.6 Methanol

- 5.1.7 Bio-/Synthetic Fuels

- 5.1.8 Ammonia

- 5.1.9 Other Fuel Types

- 5.2 By Bunkering Method

- 5.2.1 Ship-to-Ship

- 5.2.2 Port-to-Ship (Truck/Pipeline)

- 5.2.3 LNG Barge-to-Ship

- 5.2.4 Portable Tanks and Containers

- 5.3 By Vessel Type

- 5.3.1 Container

- 5.3.2 Tanker

- 5.3.3 Bulk Carrier

- 5.3.4 General Cargo

- 5.3.5 Passenger/Ro-Pax

- 5.3.6 Offshore and Specialized

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corporation

- 6.4.2 Shell Plc

- 6.4.3 Chevron Corporation

- 6.4.4 BP Plc

- 6.4.5 TotalEnergies SE

- 6.4.6 World Fuel Services Corp.

- 6.4.7 NuStar Energy L.P.

- 6.4.8 Phillips 66

- 6.4.9 Marathon Petroleum Corp.

- 6.4.10 Valero Energy Corp.

- 6.4.11 Trafigura Group Pte. Ltd.

- 6.4.12 Glencore Plc

- 6.4.13 Peninsula Petroleum

- 6.4.14 Crowley Maritime Corp.

- 6.4.15 Seacor Holdings

- 6.4.16 Kinder Morgan Inc.

- 6.4.17 Global Gas & Oil Trading LLC

- 6.4.18 Clipper Oil

- 6.4.19 Sprague Operating Resources

- 6.4.20 Pilot Thomas Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment