|

시장보고서

상품코드

2072552

독일의 ICT : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

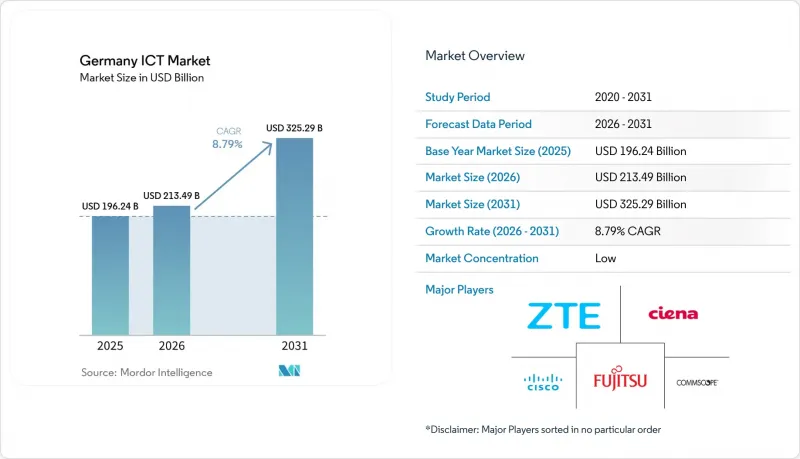

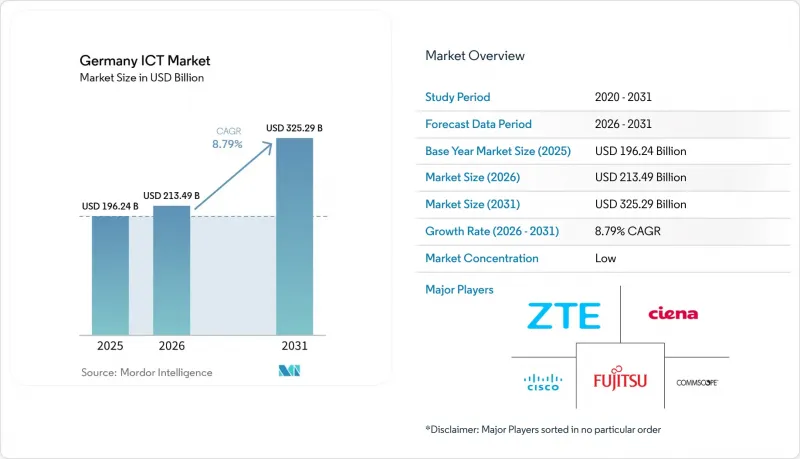

Mordor Intelligence에 의하면, 독일의 ICT 시장 규모는 2025년에 1,962억 4,000만 달러로 평가되었습니다. 2026년 2,134억 9,000만 달러에서 2031년까지 3,252억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.79%를 나타낼 전망입니다.

본 보고서는 유형별(하드웨어, 소프트웨어, IT 서비스), 기업 규모별(중소기업, 대기업), 산업별(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 기타), 배포 모델별(On-Premise, 퍼블릭 클라우드, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

독일의 ICT 시장 동향 및 인사이트

기업의 디지털화가 급속히 진행되고 있습니다.

2024년까지 독일 기업 4곳 중 3곳이 디지털 전략을 명확히 수립했으며, 이 비율은 “‘디지털 운영 탄력성법’ 등과 같은 규제 체계에 따라 산업 전반에 걸쳐 기술 리스크 관리가 표준화됨에 따라, 계속해서 상승하고 있습니다. 지멘스를 비롯한 제조 산업의 선도 기업들은 에어랑겐의 “'라이트하우스 팩토리'디지털 트윈 워크플로우를 도입한 결과, 생산성이 70% 가까이 향상되었다고 보고하고 있습니다. 금융 기관들은 회복탄력성에 관한 규제 요건을 준수하기 위해 클라우드 및 사이버 보안에 대한 투자를 가속화하고 있습니다. 한편, 미텔슈탄트 기업들은 Open Telekom Cloud와 같은 주권 클라우드 서비스를 활용하여 과도한 자본 지출 없이도 이와 유사한 규정 준수를 달성하고 있습니다. 그 결과, 보안 인프라, 관리형 서비스, AI를 활용한 분석에 대한 수요가 급증하고 있으며, 이것이 독일의 ICT 시장의 구조적 성장을 뒷받침하고 있습니다.

5G 구축 및 사설 네트워크 시범 사업

2024년에는 전국적인 5G 커버리지율이 가구의 95%를 넘어섰으며, 도이체 텔레콤은 97%, 보다폰은 92%, O2는 96%를 기록했습니다. 자동차 및 물류 허브를 대상으로 한 사설 네트워크 시범 사업에서는 실시간 로봇 제어 및 고해상도 머신 비전과 같은 저지연 활용 사례가 실증되고 있습니다. Vodafone과 Autobahn GmbH의 제휴를 통해 총 길이 1만 3,200km에 달하는 고속도로망 연선에 150곳의 매크로 사이트가 추가되었으며, 이를 통해 교통 관리를 통한 지연을 줄여주는 V2I(차량과 인프라 간 통신) 용도이 가능해졌습니다. 네트워크 슬라이싱에 대한 기업 수요는 통신 사업자와 시스템 통합사업자에게 새로운 서비스 수익원이 되고 있으며, 독일의 ICT 시장을 고부가가치 연결성과 IoT 솔루션으로 이끌고 있습니다.

사이버 보안 및 AI 분야의 만성적인 인력 부족

IT 전문가 채용 공고 수는 2024년에 14만 9,000건에 달했으며, 노동 시장의 격차는 2026년까지 78만 건으로 확대되어 구조적인 채용 병목 현상을 초래할 가능성이 있습니다. 특히 사이버 보안 분야의 인력 부족이 심각합니다. 2024년에는 기업의 70%가 AI를 활용한 사이버 공격으로 인해 측정 가능한 비즈니스적 영향을 받았다고 보고했습니다. 임금 인플레이션이 심화되면서 중소기업들은 보안 체계를 타협하거나 핵심 기능을 외부에 위탁할 수밖에 없게 되어, 독일 ICT 시장의 성장 전망을 둔화시키고 있습니다.

부문별 분석

2025년, 레거시 아키텍처를 최신 클라우드 환경으로 통합하기 위해 필요한 프로젝트 덕분에 IT 서비스는 독일의 ICT 시장에서 31.72%라는 최대 점유율을 차지했습니다. 한편, 소프트웨어 부문은 기업들이 전 세계로 사업을 확장할 수 있고, AI가 기본으로 탑재된 기성 플랫폼으로 전환하고 있는 만큼 8.92%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 2025년, 소프트웨어 지출은 독일의 ICT 시장 규모에 520억 달러를 기여했으며, SaaS형 ERP로의 전환과 로우코드 개발 스위트의 보급에 힘입어 2031년까지 868억 4,000만 달러에 달할 전망입니다. 하드웨어 매출은 상품화 현상으로 인한 이익률 압박이 지속되고 있지만, EU의 ‘'팁법'이로 인해 현지 웨이퍼 제조 공장에 대한 투자가 촉진되어, 2027년 이후 반도체 제조 장비 수요가 증가 국면에 접어들 가능성이 있습니다. Siemens의 “"Xcelerator"이는 소프트웨어 중심의 포트폴리오가 산업 부문을 초월하여 확장될 수 있음을 보여주는 반면, 통신 서비스는 5G 기업용 계약을 통해 ARPU 증가를 달성하고 있습니다. 이러한 동향은 독일의 ICT 시장에서 맞춤형 서비스에서 재현성이 있는 클라우드 네이티브 소프트웨어로의 지속적인 전환을 여실히 보여주고 있습니다.

2차적인 영향 또한 마찬가지로 시사하는 바가 큽니다. ISV(독립 소프트웨어 공급업체)는 공장 운영, 고객 서비스, 규정 준수 모니터링 분야에서 의사 결정 시간을 단축하는 임베디드 AI 모듈을 도입하고 있습니다. 시스템 통합사업자들은 경쟁력을 유지하기 위해 패키지화된 마이그레이션 서비스를 제공하고 있으며, 채널 파트너들은 성과 기반 가격 책정을 추진하고 있습니다. 그 결과, 선순환이 이루어지고 있습니다. 소프트웨어의 보급이 지속적인 수익을 창출하고, 공급업체의 매출총이익률을 높이며, 투자 역량을 강화함으로써 독일의 ICT 시장의 성장을 더욱 가속화하고 있습니다.

2025년에도 대기업들이 독일의 ICT 시장 규모의 60% 이상을 계속 차지했으며, 이는 복잡한 다년간의 현대화 프로그램과 대규모 관리형 서비스 계약을 반영한 것입니다. 그러나 현재 중소기업이 성장의 최전선에 서 있으며, 연평균 성장률(CAGR)은 9.99%로 예측되어 시장 전체보다 120베이시스포인트 높은 수치를 기록하고 있습니다. 이러한 가속화의 배경에는 기존 CAPEX를 확장 가능한 OPEX로 전환하는 클라우드 운영 모델이 있으며, 이를 통해 AI 시범 도입, 전자상거래 통합, 사이버 보안 업그레이드에 필요한 자금이 확보되고 있습니다. 퍼블릭 클라우드 분야의 주요 하이퍼스케일러 기업들은 EU 시민이 근무하는 데이터센터 지역이나 프라이버시 실드(Privacy Shield)를 준수하는 지원 서비스 등 현지화 전략을 강화하며, 미텔슈탄트(Mittelstand)에 숨겨진 비즈니스 기회를 발굴하고 있습니다.

중소기업의 도입 양상 또한 생태계의 변화를 주도하고 있습니다. 특정 부문에 특화된 시장은 즉시 도입 가능한 마이크로 서비스를 제공함으로써 사내 개발자의 필요성을 줄이고, 디지털 기술 부족 문제를 완화하고 있습니다. 금융기관들은 제조업 수출업체를 위해 국경 간 거래를 간소화하는 내장형 금융 API를 도입하여 새로운 인프라 투자를 뒷받침하고 있습니다. 중소기업이 기술 성숙도 곡선을 따라 상승함에 따라, 독일의 ICT 시장은 수요의 다양화와 특정 부문의 경기 침체에 대한 저항력 강화라는 혜택을 누리고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the germany ICT market size was valued at USD 196.24 billion in 2025 and estimated to grow from USD 213.49 billion in 2026 to reach USD 325.29 billion by 2031, at a CAGR of 8.79% during the forecast period (2026-2031).

This report is Segmented by Type (Hardware, Software, IT Services), Enterprise Size (Small & Medium Enterprises, Large Enterprises), Industry Vertical (BFSI, IT & Telecom and More), Deployment Model (On-Premises, Public Cloud and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany ICT Market Trends and Insights

Rapid Rise in Enterprise Digitalisation

Three out of four German companies had fully articulated digital strategies by 2024, a proportion that continues to climb as regulatory regimes such as the Digital Operational Resilience Act standardise technology risk management across industries. Manufacturing leaders including Siemens report productivity uplifts of nearly 70% after embedding digital-twin workflows in their Erlangen Lighthouse Factory. Financial institutions accelerate cloud and cybersecurity spending to comply with resilience mandates, while Mittelstand firms exploit sovereign cloud offerings like Open Telekom Cloud to achieve similar compliance without prohibitive capital outlays. The resulting demand spike for secure infrastructure, managed services and AI-enabled analytics underpins a structural uplift in the Germany ICT market.

5G Rollout & Private-Network Pilots

Nationwide 5G coverage surpassed 95% of households in 2024, with Deutsche Telekom at 97%, Vodafone at 92% and O2 at 96%. Private-network pilots in automotive and logistics hubs validate low-latency use-cases such as real-time robotic control and high-definition machine vision. Vodafone's partnership with Autobahn GmbH added 150 macro sites along the 13,200 km highway grid, enabling vehicle-to-infrastructure applications that cut traffic-management delays. Enterprise appetite for network slicing is translating into fresh service-revenue pools for telcos and systems integrators, propelling the Germany ICT market toward higher-value connectivity and IoT solutions.

Persistent Skills Shortage in Cybersecurity & AI

Vacancies for IT professionals reached 149,000 in 2024, and the labour-market gap could balloon to 780,000 by 2026, creating structural hiring bottlenecks. Cybersecurity talent is in particularly short supply: 70% of organisations reported measurable business impact from AI-enabled cyberattacks in 2024. Rising wage inflation forces SMEs to compromise on security postures or outsource critical functions, tempering the growth outlook of the Germany ICT market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native Migration of Mittelstand

- Gen-AI Investment Boom Post-GPT

- High Energy Prices for Data-Centre Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT services held the largest Germany ICT market share of 31.72% in 2025 thanks to integration projects required to weave legacy architectures into modern cloud environments. The software segment, however, is charting the fastest 8.92% CAGR as enterprises pivot toward off-the-shelf platforms that scale globally and embed AI out of the box. Software spending contributed USD 52 billion to the Germany ICT market size in 2025 and is slated to reach USD 86.84 billion by 2031, buoyed by SaaS ERP conversions and low-code development suites. Hardware revenue remains pressured by commoditised margins, though the EU Chips Act has unlocked local wafer-fab investments that may induce an up-cycle in semiconductor equipment demand from 2027 onward. Siemens' Xcelerator illustrates how software-centric portfolios can stretch across industrial domains, while telecom services capture incremental ARPU from 5G enterprise contracts. Together, these dynamics underline an enduring shift from bespoke services to repeatable, cloud-native software within the Germany ICT market.

Second-order effects are equally telling. ISVs inject embedded AI modules that compress decision-making time in plant operations, customer service and compliance monitoring. Systems integrators respond with packaged migration services to preserve relevance, while channel partners push outcome-based pricing. The result is a virtuous cycle: software penetration fuels recurring revenues, improves vendor gross margins and reinforces investment capacity, further accelerating the Germany ICT market expansion.

Large corporates continued to generate more than 60% of the Germany ICT market size in 2025, reflecting complex multi-year modernisation programmes and sizeable managed-service contracts. Yet SMEs now represent the growth frontier, with a projected 9.99% CAGR that exceeds the overall market by 120 basis points. This acceleration stems from cloud operating models that turn traditional CAPEX into scalable OPEX, freeing cash for AI pilots, e-commerce integrations and cybersecurity upgrades. Public-cloud hyperscalers deepen localisation measures-data-centre regions staffed by EU citizens and privacy-shielded support-to unlock the latent Mittelstand opportunity.

SME adoption patterns also drive ecosystem change. Domain-specific marketplaces deliver drop-in microservices, reducing the need for in-house developers and smoothing digital skill deficits. Financial institutions roll out embedded-finance APIs that simplify cross-border trade for manufacturing exporters, nudging fresh infrastructure spend. As SMEs climb the technology maturity curve, the Germany ICT market benefits from broadened demand diversity and resilience against sector-specific downturns.

Complete Report Scope:

- By Type

- Hardware

- Software

- IT Services

- Telecommunication Services

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Industry Vertical

- BFSI

- IT and Telecom

- Government and Public Sector

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Healthcare and Life-Sciences

- By Deployment Model

- On-Premise

- Public Cloud

- Private/Sovereign Cloud

- Hybrid Cloud

List of Companies Covered in this Report:

- Amazon Web Services, Inc.

- Alphabet Inc. (Google Cloud Germany)

- SAP SE

- Microsoft Deutschland GmbH

- Deutsche Telekom AG (T-Systems)

- Vodafone GmbH

- Telefonica Germany GmbH and Co. OHG

- 1and1 AG

- IBM Deutschland GmbH

- Oracle Deutschland B.V. and Co. KG

- Cisco Systems GmbH

- Fujitsu Technology Solutions GmbH

- Nokia Solutions and Networks GmbH

- Huawei Technologies Deutschland GmbH

- HPE Deutschland GmbH

- Atos Information Technology GmbH

- Capgemini Deutschland GmbH

- Accenture GmbH

- ZF Friedrichshafen AG (Digital Services)

- Siemens AG (Digital Industries)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rise in enterprise digitalisation

- 4.2.2 5G rollout and private-network pilots

- 4.2.3 Cloud-native migration of Mittelstand

- 4.2.4 Gen-AI investment boom post-GPT

- 4.2.5 EU Chips Act-linked semiconductor CAPEX

- 4.2.6 Growth of sovereign-cloud and Gaia-X nodes

- 4.3 Market Restraints

- 4.3.1 Persistent skills shortage in cybersecurity and AI

- 4.3.2 High energy prices for data-center ops

- 4.3.3 Lagging FTTP coverage vs EU peers

- 4.3.4 Inflation-driven IT CAPEX deferrals by SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Threat of New Entrants

- 4.7.3 Threat of Substitutes

- 4.7.4 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 IT Services

- 5.1.4 Telecommunication Services

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Government and Public Sector

- 5.3.4 Retail and E-commerce

- 5.3.5 Manufacturing

- 5.3.6 Energy and Utilities

- 5.3.7 Healthcare and Life-Sciences

- 5.4 By Deployment Model

- 5.4.1 On-Premise

- 5.4.2 Public Cloud

- 5.4.3 Private/Sovereign Cloud

- 5.4.4 Hybrid Cloud

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Alphabet Inc. (Google Cloud Germany)

- 6.4.3 SAP SE

- 6.4.4 Microsoft Deutschland GmbH

- 6.4.5 Deutsche Telekom AG (T-Systems)

- 6.4.6 Vodafone GmbH

- 6.4.7 Telefonica Germany GmbH and Co. OHG

- 6.4.8 1and1 AG

- 6.4.9 IBM Deutschland GmbH

- 6.4.10 Oracle Deutschland B.V. and Co. KG

- 6.4.11 Cisco Systems GmbH

- 6.4.12 Fujitsu Technology Solutions GmbH

- 6.4.13 Nokia Solutions and Networks GmbH

- 6.4.14 Huawei Technologies Deutschland GmbH

- 6.4.15 HPE Deutschland GmbH

- 6.4.16 Atos Information Technology GmbH

- 6.4.17 Capgemini Deutschland GmbH

- 6.4.18 Accenture GmbH

- 6.4.19 ZF Friedrichshafen AG (Digital Services)

- 6.4.20 Siemens AG (Digital Industries)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment