|

시장보고서

상품코드

2072566

인쇄 연포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Printed Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

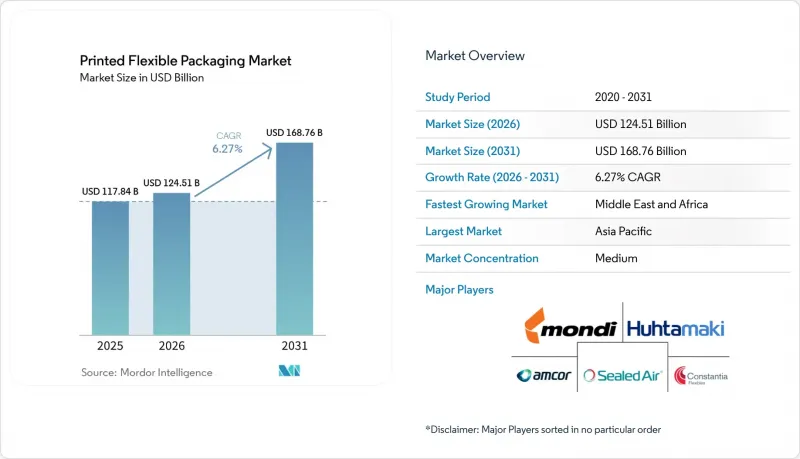

Mordor Intelligence에 의하면, 인쇄 연포장 시장 규모는 2025년 1,178억 4,000만 달러로 평가되었습니다. 2026년 1,245억 1,000만 달러에서 2031년까지 1,687억 6,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 6.27%를 나타낼 것으로 예측됩니다.

본 보고서는 인쇄 기술(플렉소 인쇄, 그라비아 인쇄, 기타), 포장 유형(롤 스톡 및 필름, 봉지·자루, 라벨 및 수축 슬리브, 기타), 최종 사용자 산업(식음료, 가정용 및 산업용, 기타), 기재(플라스틱(PE, PP, PET, 기타), 종이·종이계, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인쇄 연포장 시장 동향 및 인사이트

매장 진열용 소매 포장에 대한 수요 증가

소매업체들이 운송부터 진열에 이르는 전 과정에서 취급 횟수를 최소화할 수 있는 포장을 요구하는 가운데, 진열용 포장은 인쇄 연포장 시장에서 더욱 강력한 수요 견인 역할을 하고 있습니다. 이러한 변화로 인해 인쇄 그래픽의 역할은 더욱 중요해지고 있습니다. 이는 컨버터가 동일한 구조 내에서 시각적 효과, 가독성, 운영의 일관성을 제공할 것으로 기대되기 때문입니다. 유럽의 주요 식료품 체인들은 진열용 사양의 표준화를 지속적으로 추진하고 있으며, 이에 따라 별도의 라벨을 사용하는 대신 연질 기판에 직접 고품질 인쇄를 해야 할 필요성이 커지고 있습니다. 또한, 이로 인해 아트워크 승인부터 매장 진열까지의 기간이 단축되어, 인쇄 연포장 시장에서 보다 신속하고 빈번한 생산 주기를 관리할 수 있는 공급업체가 유리한 입장에 서게 됩니다. 계절 한정, 프로모션, 지역 한정 포장 변경을 실시하는 브랜드 소유주가 늘어나는 가운데, 플렉소 인쇄와 디지털 인쇄 능력을 갖춘 컨버터는 재주문을 확보하고 가격을 유지하는 데 유리한 입장에 있습니다.

차단성이 뛰어난 단일 소재 구조의 급속한 보급

인쇄 연포장 시장은 재활용 가능성 목표가 소재 선택과 인쇄용 화학 물질 모두에 영향을 미치게 됨에 따라, 높은 차단성을 지닌 단일 소재 구조로 빠르게 전환되고 있습니다. 2025년 9월, Siegwerk, Borouge, TPN Food Packaging은 산소 투과율이 1 cc/m²/일 이하이며, 잉크를 완전히 제거할 수 있는 단일 PE 소재의 스탠드업 파우치를 상품화했습니다. 이를 통해 재활용이 가능한 설계에서도, 기존에는 더 복잡한 적층 소재에서만 볼 수 있었던 차단 성능을 실현할 수 있게 되었음이 입증되었습니다. 또한, BOBST는 자사의 “"oneBARRIER PrimeCycle" 단일 PE 구조가 평가 대상이었던 모든 범주에서 호일 기반 대체재보다 환경 부하가 낮다는 사실이 보고되었으며, 이는 컨버터들이 재활용 가능한 필름 솔루션에 투자할 상업적 근거를 강화해 줍니다. EU의 포장 및 포장 폐기물 관련 규제는 대규모 재활용을 전제로 한 포장 설계를 의무화함으로써 이러한 변화를 뒷받침하고 있습니다. 그 결과, 인쇄용 연포장 시장에서는 인쇄에 적합한 단일 소재 필름, 탈잉크 코팅, 외관과 재활용성을 모두 충족시키는 표면 처리 기술로 자본이 이동하고 있습니다.

변동이 심한 수지, 필름, 잉크의 투입 비용

변환기는 수지, 필름, 호일, 잉크의 가격 변동에 큰 영향을 받기 때문에 원자재 비용의 변동은 인쇄 연포장 시장에서 여전히 가장 뚜렷한 제약 요인 중 하나입니다. 폴리에틸렌과 폴리프로필렌의 원가는 여전히 원자재 및 에너지 가격의 영향을 받기 쉬우며, 이러한 영향은 수입 폴리머 공급에 의존하는 지역에서 더욱 두드러집니다. 잉크 시스템 역시 컨버터가 성능, 규정 준수, 공급 안정성을 동시에 충족시켜야 하기 때문에 큰 압박을 받고 있습니다. 지크베르크사는 폴리올레핀계 기재의 표면 인쇄용으로 NC가 포함되지 않은 잉크 컬러 시스템을 도입했는데, 이러한 움직임은 규정 준수를 위한 배합 변경이 인쇄 연포장 시장에서 원자재 비용 관리의 일환이 되어가고 있음을 보여줍니다. 원자재나 잉크 변경을 미루는 변환업체는 비용 변동성과 재활용 가능성에 대한 위험이라는 두 가지 문제에 동시에 직면할 가능성이 있어, 더욱 어려운 처지에 놓이게 됩니다.

부문별 분석

2025년, 플렉소 인쇄는 인쇄 연포장 시장의 49.34%를 차지하며, 식품, 개인 위생 용품, 재택치료 부문에서의 장기적인 활용 측면에서 계속해서 선두 자리를 지켰습니다. 각 변환기 제조업체들이 미터당 비용 측면에서의 우위, 다양한 기판과의 호환성, 인쇄 품질의 꾸준한 향상을 계속해서 중시함에 따라 그 입지는 견고하게 유지되었습니다. 2020년 이후 선수 능력 향상, 컬러 시스템 확충, 판 교체 방법의 고속화를 통해, 과거 플렉소 인쇄와 그라비아 인쇄를 명확히 구분하던 품질 격차는 줄어들었습니다. 2026년 4월, 암콜(Amcor)은 네덜란드 하덴베르그에 위치한 새로운 플렉소 인쇄 라인에 수백만 유로를 투자하기로 결정하여, 연간 최대 6,000톤의 생산 능력을 추가했습니다. 이는 대규모 플렉소 인쇄 생산에 대한 지속적인 신뢰를 보여주는 것입니다.

디지털 인쇄는 2031년까지 연평균 성장률(CAGR) 11.71%로 확대될 것으로 예상되며, 이에 따라 인쇄 기술 중 연포장 시장에서 가장 빠르게 성장하는 공정이 되고 있습니다. 그 주된 이유는 디지털 시스템이 소량 생산, 다양한 포장 형태, 가변적인 컨텐츠 및 신속한 납기가 요구되는 프로젝트에 적합하기 때문입니다. 이에 따라 인쇄 연포장 시장에서 공급업체 선정 기준이 변화하고 있습니다. 왜냐하면, 현재 더 많은 구매자들이 동일한 플랫폼에서 대량 생산에 필요한 아날로그 작업과 단기 납기가 요구되는 디지털 작업을 모두 관리할 수 있는 컨버터를 찾고 있기 때문입니다. 그라비아 인쇄는 매우 안정적인 잉크 도포와 매우 높은 라인 속도가 요구되는 고급 용도, 특히 장기간에 걸쳐 시각적 일관성이 극히 중요한 분야에서 여전히 확고한 입지를 유지하고 있습니다. 하이브리드 시스템이나 특수 시스템을 포함한 기타 기술들은 보안 인쇄 효과나 촉감 마감과 같은 보다 제한적인 요구를 계속해서 충족시키고 있지만, 플렉소그래피가 차지하는 시장 규모나 현재 디지털 인쇄가 보여주고 있는 성장 속도에는 미치지 못하는 상황입니다.

2025년, 파우치는 인쇄 연포장 시장의 35.98%를 차지하며, 식품, 헬스케어, 퍼스널케어 제품 분야에서 널리 사용되고 있음을 반영했습니다. 스탠드업형, 플랫형, 스파우트가 달린 파우치 등 각 디자인은 진열대에서의 높은 가시성과 원재료 사용량 절감, 뛰어난 취급 편의성을 모두 갖추고 있어 계속해서 수요가 증가하고 있습니다. 스탠드업 파우치는 유리나 경질 플라스틱, 혹은 무게가 무겁거나 디자인의 자유도가 낮은 구식 포장 형태에서 전환하려는 브랜드에게 일반적인 업그레이드 수단이 되고 있습니다. 2025년 9월, 지크베르크(Siegwerk), 보루지(Borouge), TPN 푸드 패키징(TPN Food Packaging)은 재활용이 가능한 고차단성 단일 소재 스탠드업 파우치를 출시했습니다. 이는 인쇄 연포장 시장에서 파우치의 성장이 편의성과 재활용성 향상이라는 두 가지 요소와 밀접한 관련이 있음을 보여줍니다.

롤 스톡과 필름은 대량 생산을 위한 성형·충전·밀봉(FFS) 공정을 뒷받침하고, 수많은 컨버터 네트워크의 효율을 유지하는 생산 기반을 제공함으로써, 인쇄용 연포장 시장에서 여전히 핵심적인 역할을 수행하고 있습니다. 단위당 가치는 일부 기성 제품보다 낮지만, 롤 스톡은 컨버터에 안정적인 수량과 장기적인 생산 기회를 제공하며, 디지털 인쇄기, 코팅, 재활용 가능한 라미네이트에 대한 투자 자금을 조달하는 데 일조하고 있습니다. 가방이나 자루는 인쇄 요건이 비교적 단순하지만 출하량이 막대한 산업용 및 농업용 대량 용도 분야에서 여전히 중요한 역할을 하고 있습니다. 라벨과 수축 슬리브는 그래픽 중심의 틈새 시장으로서 여전히 중요하며, CCL 인더스트리즈는 2026년 6월, 쓰리바 인터내셔널을 인수함으로써 이 부문을 확장하고, 전 세계 포장 시장에서 소비재 및 헬스케어 용도 전반에 걸친 연질 필름 및 슬리브의 입지를 강화했습니다. 이에 따라 각 변환기 제조업체들은 인쇄 연포장 시장에서 명확한 균형 감각을 갖추어야 합니다. 왜냐하면 파우치 제조의 성장이 자본을 유치하는 한편, 롤 스톡은 여전히 공장 차원의 가동률과 현금 창출을 뒷받침하는 형태인 경우가 많기 때문입니다.

지역별 분석

2025년, 아시아태평양은 인쇄 연포장 시장 점유율의 37.89%를 차지하며 최대 지역 시장이 되었습니다. 이 지역은 중국의 거대한 컨버터 기반, 인도의 확대되는 식품 가공 활동, 그리고 일본에서 프리미엄급이며 엄격한 사양이 요구되는 포장 용도에 대한 활발한 수요의 혜택을 받고 있습니다. 중국은 전자상거래, 식품, 소비재 등 각 유통 채널에서 신속한 생산 대응과 현지 상황에 맞춘 포장 디자인이 점점 더 중요시되고 있기 때문에 여전히 중요한 시장입니다. 인도에서는 도시 및 준도시 시장에서 포장 식품과 일용소비재의 유통이 확대됨에 따라, 파우치, 라미네이트, 롤 스톡에 대한 수요를 통해 시장 규모가 지속적으로 확대되고 있습니다. 일본에서는 의약품 및 고급 식품 부문에서 높은 인쇄 품질, 규제 준수, 일관성이 지속적으로 요구되고 있어, 인쇄 연포장 시장의 고부가가치 부문을 뒷받침하고 있습니다.

유럽은 인쇄 연포장 시장에서 여전히 2위의 규모를 자랑하고 있으며, 엄격한 지속가능성 관련 규제와 까다로운 인쇄 기준에 따라 시장이 지속적으로 형성되고 있습니다. “‘EU 포장 및 포장 폐기물 규정’ 이는 컨버터 투자를 주도하는 주요 요인으로 작용하고 있으며, 해당 지역에서 재활용이 불가능한 다층 구조에서 기능성 코팅이 적용된 단일 소재 필름으로의 전환을 촉진하고 있습니다. 독일과 이탈리아는 여전히 중요한 생산 거점이며, 한편 폴란드는 연포장 가공 분야의 경쟁 제조 거점으로서 계속해서 주목을 받고 있습니다. 북미는 헬스케어용 포장, 브랜드 홍보용 인쇄, 특수 필름 등의 용도가 첨단 인쇄 및 소재 기술에 대한 투자를 지속적으로 뒷받침하고 있어, 인쇄 연포장 시장에서 확고한 입지를 유지하고 있습니다.

중동 및 아프리카는 2031년까지 연평균 성장률(CAGR) 7.04%로 확대될 것으로 예측되며, 인쇄 연포장 시장에서 가장 빠르게 성장하는 지역 블록으로 자리매김하고 있습니다. 사우디아라비아는 하류 제조업에 대한 관심을 높이고 있으며, 이에 따라 식품, 유제품, 스낵, 퍼스널케어 부문에서 연포장 생산을 위한 현지 기반이 강화되고 있습니다. 튀르키예는 특히 롤 스톡 및 기성 파우치의 유통 분야에서 북아프리카로공급 및 무역 거점으로서의 역할을 강화하고 있습니다. 남아프리카공화국과 나이지리아는 여전히 사하라 이남 아프리카의 주요 수요 축을 이루고 있지만, 남미에서는 브라질이 식품 포장 형태의 현대화를 추진하고 소비자용 및 전자상거래 채널에서 디지털 인쇄의 활용 범위를 지속적으로 확대하고 있음에도 불구하고 성장 속도는 완만합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

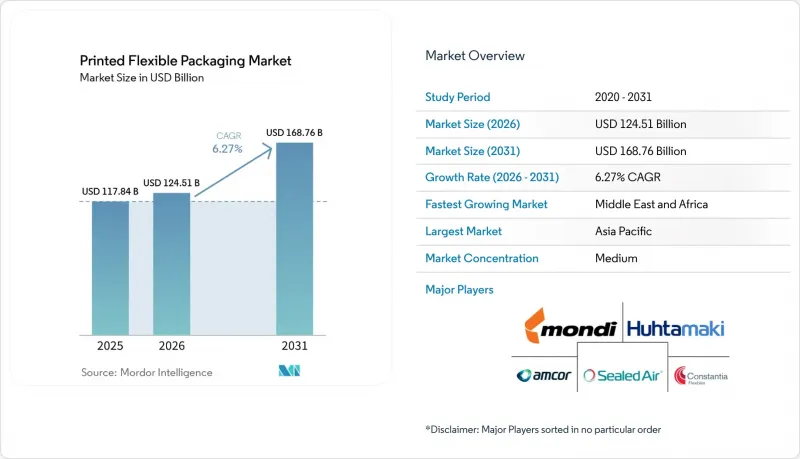

KTHAccording to Mordor Intelligence, the printed flexible packaging market size is projected to expand from USD 117.84 billion in 2025 and USD 124.51 billion in 2026 to USD 168.76 billion by 2031, registering a CAGR of 6.27% between 2026 and 2031.

This report is Segmented by Printing Technology (Flexography, Rotogravure, and More), Packaging Type (Rollstock and Films, Bags and Sacks, Labels and Shrink Sleeves, and More), End-User Industry (Food and Beverage, Home Care and Industrial, and More), Substrate [Plastics (PE, PP, PET, Others), Paper and Paper-Based, and More], and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Printed Flexible Packaging Market Trends and Insights

Rising Demand for Shelf-Ready Retail Packaging

Shelf-ready formats are becoming a stronger demand driver in the printed flexible packaging market, as retailers seek packs that move from transit to display with less handling. That change gives printed graphics a more central role because converters are expected to deliver visual impact, legibility, and operational consistency on the same structure. Large grocery chains in Europe have continued to standardize on display-ready specifications, which has increased the need for high-quality print directly on flexible substrates rather than on separate labels. It also shortens the time between artwork approval and store placement, favoring suppliers that can manage faster, more frequent production cycles in the printed flexible packaging market. As more brand owners run seasonal, promotional, and regional pack changes, converters with flexographic and digital capability are better placed to retain repeat work and protect pricing.

Faster Adoption of High-Barrier Mono-Material Structures

The printed flexible packaging market is moving more quickly toward high-barrier mono-material structures because recyclability targets now affect both material choice and print chemistry. In September 2025, Siegwerk, Borouge, and TPN Food Packaging commercialized a fully de-inkable mono-PE stand-up pouch with an oxygen transmission rate below 1 cc/m2/day, demonstrating that recyclable designs can now deliver barrier performance previously associated with more complex laminates. BOBST also reported that its oneBARRIER PrimeCycle mono-PE structure had a lower environmental impact than foil-based alternatives across all assessed categories, which strengthens the commercial case for converters investing in recyclable film solutions. The EU packaging and packaging waste rules are reinforcing this shift by requiring packaging to be designed for recyclability at scale. As a result, the printed flexible packaging market is seeing capital move toward print-compatible mono-material films, de-inking coatings, and surface treatments that preserve both appearance and recyclability.

Volatile Resin, Film, and Ink Input Costs

Input cost swings remain one of the clearest constraints on the printed flexible packaging market because converters are heavily exposed to resin, film, foil, and ink pricing. Polyethylene and polypropylene costs remain sensitive to feedstock and energy prices, and that exposure is stronger in regions that depend on imported polymer supply. Ink systems are also under pressure because converters must balance performance, compliance, and availability simultaneously. Siegwerk introduced an NC-free ink color system for surface printing on polyolefin-based structures, and that move showed how compliance-driven reformulation is also becoming part of input cost management in the printed flexible packaging market. Converters that delay material and ink changes face a more difficult position because they may face both cost volatility and recyclability risk simultaneously.

Other drivers and restraints analyzed in the detailed report include:

- Growth In Short-Run Digital and Versioned Printing

- Expansion of Packaged Food and Convenience Consumption

- Recycling Complexity of Multilayer Laminate Structures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexography held 49.34% of the printed flexible packaging market in 2025, which kept it in the lead across long-run applications in food, personal care, and home care. Its position remained strong because converters continued to rely on favorable cost-per-meter economics, broad substrate compatibility, and steady improvements in print quality. Post-2020 progress in line-screen capability, expanded color systems, and faster plate change methods reduced the older quality gap that had once separated flexography more clearly from gravure. In April 2026, Amcor committed a multi-million-euro investment in a new flexographic printing line at Hardenberg in the Netherlands, adding capacity for up to 6,000 metric tonnes per year, which showed continued confidence in large-scale flexographic output.

Digital printing is projected to expand at an 11.71% CAGR through 2031, which makes it the fastest-growing process in the printed flexible packaging market size among printing technologies. The main reason is that digital systems are better suited to short runs, versioned packs, and jobs that need variable content or faster turnaround. That is changing supplier selection in the printed flexible packaging market because more buyers now want a converter that can manage both large-volume analog work and quick-turn digital work from the same platform. Rotogravure still retains a strong position in premium applications that demand very stable ink laydown and very high line speeds, especially where visual consistency remains critical over long runs. Other technologies, including hybrid and specialty systems, continue to serve narrower needs such as security print effects or tactile finishes, but they do not challenge the scale held by flexography and the growth pace now seen in digital.

Pouches accounted for 35.98% of the printed flexible packaging market in 2025, reflecting their widespread use across food, healthcare, and personal care products. Stand-up, flat, and spouted pouch designs continue to attract demand because they combine strong shelf visibility with lower material use and good handling convenience. The stand-up pouch has become a common upgrade route for brands moving away from glass, rigid plastic, or older pack types that carry higher weight or less flexible design space. In September 2025, Siegwerk, Borouge, and TPN Food Packaging introduced a recyclable high-barrier mono-material stand-up pouch, showing that pouch growth in the printed flexible packaging market is now tied to both convenience and improved recyclability.

Rollstock and films remain central to the printed flexible packaging market because they support high-volume form-fill-seal operations and provide the production base that keeps many converter networks efficient. While the value per unit is lower than in several pre-made formats, rollstock provides converters with steady volume and longer runs that help fund investment in digital presses, coatings, and recycle-ready laminates. Bags and sacks still serve bulk industrial and agricultural use where print requirements are simpler but shipment volumes are large. Labels and shrink sleeves stay important as a graphics-led niche, and CCL Industries expanded that area in June 2026 through its acquisition of Sleever International, strengthening its flexible film and sleeve position across consumer goods and healthcare uses in global packaging. This leaves converters with a clear balancing act in the printed flexible packaging market because pouch-making growth attracts capital, while rollstock remains the format that often supports plant-level utilization and cash generation.

Complete Report Scope:

- By Printing Technology

- Flexography

- Rotogravure

- Digital (Inkjet, Electrophotography)

- Other Printing Technologies

- By Packaging Type

- Pouches (Stand-up, Flat, Spouted)

- Rollstock and Films

- Bags and Sacks

- Labels and Shrink Sleeves

- Other Packaging Types

- By End-User Industry

- Food and Beverage

- Healthcare and Pharmaceuticals

- Personal Care and Cosmetics

- Home Care and Industrial

- Other End-User Industries

- By Substrate

- Plastics (PE, PP, PET, Others)

- Paper and Paper-based

- Aluminum Foil and Metallised Films

- Other Substrate Types

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Thailand

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific accounted for 37.89% of the printed flexible packaging market share in 2025, making it the largest regional market. The region benefits from China's large converting base, India's expanding food processing activity, and Japan's strong demand for premium and tightly specified packaging applications. China remains important because fast production response and localized pack design are increasingly valued across e-commerce, food, and consumer goods channels. India continues to add volume through pouch, laminate, and rollstock demand as packaged food and fast-moving consumer goods distribution deepen across urban and semi-urban markets. Japan supports the higher-value side of the printed flexible packaging market because pharmaceutical and premium food categories continue to require strong print quality, compliance, and consistency.

Europe remained the second-largest region in the printed flexible packaging market, and it continues to be shaped by strict sustainability rules and demanding print standards. The EU Packaging and Packaging Waste Regulation is a major driver of converter investment, pushing the region away from non-recyclable multilayer structures toward mono-material films with functional coatings. Germany and Italy remain important production centers, while Poland continues to attract activity as a competitive manufacturing base for flexible packaging conversion. North America keeps a strong position in the printed flexible packaging market because healthcare packaging, promotional brand runs, and specialty film applications continue to support investment in advanced print and material capability.

The Middle East and Africa is projected to expand at a 7.04% CAGR through 2031, which makes it the fastest-growing regional block in the printed flexible packaging market. Saudi Arabia is directing more attention toward downstream manufacturing, and that is improving the local base for flexible pack production in food, dairy, snacks, and personal care. Turkey is strengthening its role as a supply and trade link into North Africa, especially in rollstock and pre-made pouch movement. South Africa and Nigeria remain the main Sub-Saharan demand anchors, while South America is growing at a slower pace as Brazil continues to modernize food packaging formats and add more digitally printed applications in consumer and e-commerce channels.

- Amcor plc

- Mondi plc

- Huhtamaki Oyj

- Sealed Air Corporation

- Constantia Flexibles Group GmbH

- Sonoco Products Company

- UFlex Limited

- Printpack Inc.

- Glenroy, Inc.

- CCL Industries Inc.

- Winpak Ltd.

- Coveris Holdings S.A.

- Sudpack Verpackungen GmbH & Co. KG

- Bischof + Klein SE & Co. KG

- ePac Holdings, LLC

- Clondalkin Group Holdings B.V.

- Goglio S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Shelf-Ready Retail Packaging

- 4.2.2 Shift Toward Lightweight and Material-Efficient Packs

- 4.2.3 Faster Adoption of High-Barrier Mono-Material Structures

- 4.2.4 Growth in Short-Run Digital and Versioned Printing

- 4.2.5 Expansion of Packaged Food and Convenience Consumption

- 4.2.6 Sustainability-Led Conversion from Rigid to Flexible Formats

- 4.3 Market Restraints

- 4.3.1 Volatile Resin, Film, and Ink Input Costs

- 4.3.2 Recycling Complexity of Multilayer Laminate Structures

- 4.3.3 Capital Intensive Migration to Advanced Printing Lines

- 4.3.4 Food Contact and Extended Producer Responsibility Compliance Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Flexography

- 5.1.2 Rotogravure

- 5.1.3 Digital (Inkjet, Electrophotography)

- 5.1.4 Other Printing Technologies

- 5.2 By Packaging Type

- 5.2.1 Pouches (Stand-up, Flat, Spouted)

- 5.2.2 Rollstock and Films

- 5.2.3 Bags and Sacks

- 5.2.4 Labels and Shrink Sleeves

- 5.2.5 Other Packaging Types

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare and Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Home Care and Industrial

- 5.3.5 Other End-User Industries

- 5.4 By Substrate

- 5.4.1 Plastics (PE, PP, PET, Others)

- 5.4.2 Paper and Paper-based

- 5.4.3 Aluminum Foil and Metallised Films

- 5.4.4 Other Substrate Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Thailand

- 5.5.4.7 Indonesia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 Huhtamaki Oyj

- 6.4.4 Sealed Air Corporation

- 6.4.5 Constantia Flexibles Group GmbH

- 6.4.6 Sonoco Products Company

- 6.4.7 UFlex Limited

- 6.4.8 Printpack Inc.

- 6.4.9 Glenroy, Inc.

- 6.4.10 CCL Industries Inc.

- 6.4.11 Winpak Ltd.

- 6.4.12 Coveris Holdings S.A.

- 6.4.13 Sudpack Verpackungen GmbH & Co. KG

- 6.4.14 Bischof + Klein SE & Co. KG

- 6.4.15 ePac Holdings, LLC

- 6.4.16 Clondalkin Group Holdings B.V.

- 6.4.17 Goglio S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment