|

시장보고서

상품코드

2072569

소비자용 드론 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Consumer Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

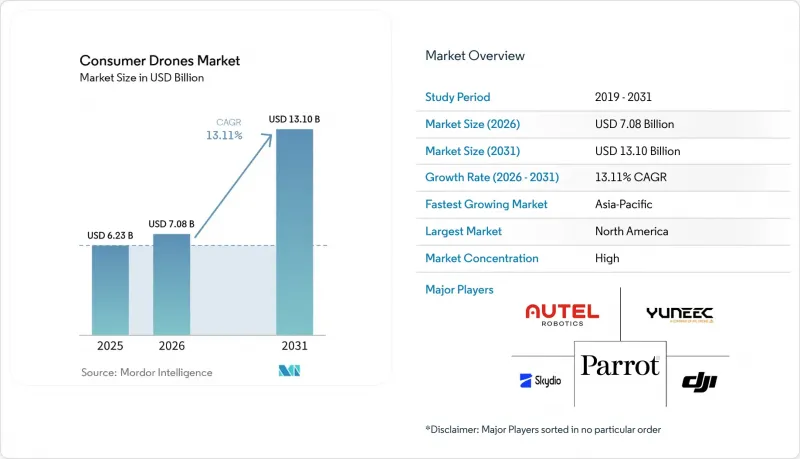

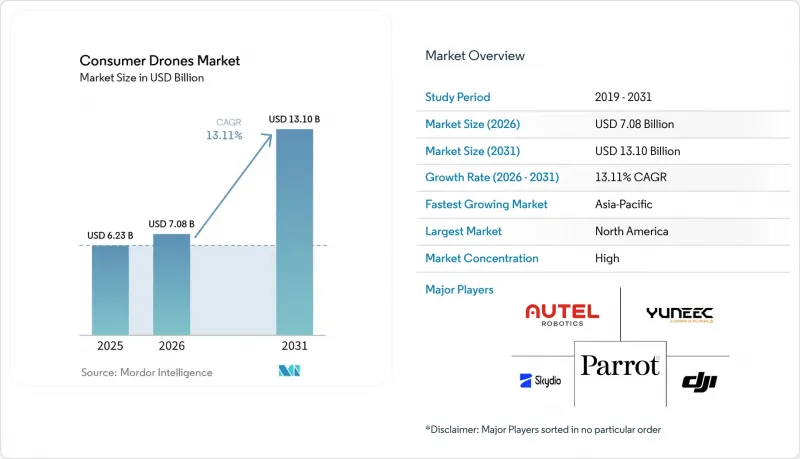

Mordor Intelligence에 의하면, 소비자용 드론 시장 규모는 2025년에 62억 3,000만 달러로 평가되었습니다. 2026년 70억 8,000만 달러에서 2031년까지 131억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 13.11%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(멀티로터, 고정익, 하이브리드), 비행 거리(4km 미만, 4km 이상), 중량 등급(나노/마이크로, 미니, 스몰, 미디엄), 용도(사진·동영상 촬영, 레이스·스포츠, 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소비자용 드론 시장 동향 및 인사이트

리튬 이온 배터리 비용의 급락이 드론의 경제성을 재정의하고 있습니다.

배터리 비용의 하락으로 인해 브랜드와 구매자 모두에게 소비자용 드론 시장 진출이 더욱 수월해지고 있습니다. 배터리 비용의 하락은 부품 원가를 절감하고, 소매 가격 상승을 초래하지 않으면서도 비행 시간 연장, 냉각 성능 향상, 보다 안전한 전력 관리를 실현할 여지를 마련해 주고 있습니다. 이는 미미한 하드웨어 비용의 변동이 제품이 첫 구매 고객에게 전달될지 여부를 좌우하는 보급형 및 중급 기기에서 가장 중요한 요소입니다. 또한, 이러한 경향은 브랜드가 액세서리를 바라보는 방식에도 변화를 가져오고 있습니다. 왜냐하면, 업그레이드용 배터리 팩은 번들로 제공되는 일회성 부속품이 아니라, 재구매 대상이 될 수 있기 때문입니다. DJI는 신제품 ‘Lito’ 시리즈를 위해 ‘Intelligent Flight Battery Plus’ 옵션을 적극 홍보하며, 이를 비행 시간 연장과 연계함으로써 배터리 설계가 가치 제안을 형성할 수 있음을 입증했습니다. 이러한 추세가 확산됨에 따라, 기능의 완성도를 저해하지 않으면서 시장은 더욱 폭넓은 가격대에 걸쳐 계속 확대될 것입니다.

범용 부품으로서의 카메라 모듈이 대중 시장을 확대되고 있습니다.

카메라 하드웨어는 몇년전과 비교해 훨씬 빠른 속도로 일반 시장에 보급되고 있으며, 이로 인해 소비자용 드론 시장의 가격 책정 및 패키지 구성에 변화가 일어나고 있습니다. DJI는 2025년 9월, 무게 약 249g의 본체에 1인치 CMOS 센서를 탑재한 ‘Mini 5 Pro’를 발표하며, 경량 소비자용 폼 팩터에 얼마나 고도의 촬영 기능을 집약할 수 있는지를 입증했습니다. 이러한 변화로 인해 프리미엄 제품과 대중형 제품 간의 기존 격차가 줄어들었고, 화질은 더 이상 프리미엄급 부가 기능이 아니라 기본 요건으로 인식되게 되었습니다. 구매자들이 저렴한 가격에도 고화질 동영상을 기대하게 되면, 각 브랜드는 카메라 하드웨어만으로 이익률을 유지할 여지가 좁아집니다. SkyRover는 2026년 3월, 전방 장애물 회피 기능, 4K/60fps 동영상 촬영, 12km HD 전송 기능을 갖추고, 가격이 300달러 미만이며 무게가 249g 미만인 모델을 발표함으로써 이러한 방향성을 더욱 공고히 했습니다. 그 결과, 현재의 소비자용 드론 시장에서는 센서의 사양 자체보다 소프트웨어의 사용 편의성, 자동 촬영 기능, 그리고 신뢰성이 높은 전송 기능이 더욱 중요시되고 있습니다.

주파수 대역의 혼잡이 밀집 환경에서의 신뢰성을 저해합니다.

소비자용 드론 시장은 여전히 Wi-Fi, 블루투스, 그리고 계속 늘어나는 연결 기기들과 공유되는 혼잡한 주파수 대역에 크게 의존하고 있습니다. 이로 인해 도심이나 공원, 행사장 등에서 신호 노이즈가 조종 정확도나 영상의 안정성에 영향을 미치는 실용적인 문제가 발생하고 있습니다. FCC는 2024년 7월, 5030-5091 MHz 대역에서의 드론 운용에 관한 초기 규정을 채택했으나, 이 규정의 틀은 일상적인 레크리에이션 비행이 아닌, 면허가 필요한 고도의 운용을 대상으로 한 것입니다. 그 결과, 정책 논의가 진행되고 있음에도 불구하고 주요 소비자층은 여전히 개방적인 ISM 환경의 한계에 노출된 상태입니다. 이것은 중요한 문제입니다. 왜냐하면 구매자들은 드론을 단순히 사양상의 비행 거리만으로 판단하는 것이 아니라, 일상적인 사용 시 연결이 얼마나 안정적인지에 따라 판단하기 때문입니다. 더 폭넓은 사용자층이 주파수 대역에 더 쉽게 접근할 수 있게 될 때까지, 소비자용 드론 시장은 밀집된 환경에서 신뢰성의 한계에 계속 직면할 것입니다.

부문별 분석

2025년에는 멀티로터형 드론이 매출의 70.11%를 차지하며, 소비자용 드론 시장의 중심적인 위치를 확고히 했습니다. 이 제품의 강점은 수직 이륙, 손쉬운 호버링, 컴팩트한 접이식 설계, 그리고 사진 촬영이나 일상적인 레저 활동에 적합한 비행 방식에 있습니다. 또한, 현재 주류 카테고리의 상당수를 특징짓는 ‘경량화’라는 제품 방향성과도 잘 부합합니다. 많은 구매자들에게 멀티로터형 플랫폼은 안정적인 영상 촬영이 가능하고 배우기 쉬운 점 때문에 여전히 가장 부담 없는 선택지로 남아 있습니다.

고정익 드론 시장은 2031년까지 연평균 성장률(CAGR) 15.22%를 나타낼 것으로 예측되며, 이는 소비자용 드론 시장의 일부가 더 긴 항속 거리와 비행 지속 시간을 원하고 있음을 보여줍니다. 이 제품들은 정지 호버링을 중시하는 사용자보다, 넓은 범위의 커버리지나 긴 비행 경로를 중시하는 프로슈머층에게 더 큰 매력을 발휘합니다. 하이브리드 설계는 이 두 가지 범주의 중간에 위치하며, 이동 효율과 호버링 능력을 모두 갖추고 있어 점차 그 존재감을 높여가고 있습니다. 주요 과제는 고정익 및 하이브리드 분야의 제품 파이프라인이 멀티로터 기반에 비해 여전히 부족한 점입니다. 그럼에도 불구하고, 자율 내비게이션 기술이 향상되고 고도의 기술을 갖춘 사용자들이 단시간의 근거리 영상 촬영 이상의 기능을 갖춘 기체를 요구하게 됨에 따라, 소비자용 드론 시장에서는 더욱 차별화가 진행될 것으로 보입니다.

2025년에는 비행 거리가 4km 미만인 드론이 매출의 57.62%를 차지하며, 소비자용 드론 시장이 여전히 인근 지역이나 여행 목적의 이용에 크게 의존하고 있음이 드러났습니다. 이 카테고리는 휴대성, 간편한 설치, 규제상의 번거로움이 적다는 점을 중요시하는 일반 사용자의 요구에 부합합니다. 또한, 가장 가볍고 널리 판매되고 있는 민간용 기체의 중량 프로파일에도 부합합니다. 일반 구매자에게는 극단적인 비행 거리보다 실용성이 더 중요하기 때문에 단거리 제품이 가장 폭넓은 판매량을 유지하고 있습니다.

8km를 초과하는 부문은 2031년까지 연평균 성장률(CAGR) 14.11%로 확대될 것으로 예상되며, 이는 소비자용 드론 시장에 확실한 프리미엄 성장 분야를 가져다줄 것입니다. 구매자가 여기서 진정으로 원하는 것은 패키지에 기재된 최대 비행 거리뿐만 아니라, 안정적인 실시간 영상과 더욱 신뢰할 수 있는 통신 연결입니다. DJI는 2026년 3월, 최대 20km 거리에서 1080p/60fps 동영상 전송이 가능한 O4+ 통신 기능을 탑재한 ‘Avata 360’을 출시하며, 이러한 프리미엄 전략을 강조했습니다. 이러한 기능 덕분에 장거리 주행 성능이 애호가들의 주류층에게도 친숙한 것이 되었습니다. 소비자용 드론 산업이 발전함에 따라, 단순히 통신 거리의 확대보다는 통신의 신뢰성이 더욱 중요시될 것입니다.

지역별 분석

2025년, 북미는 전 세계 매출의 37.65%를 차지하며 소비자용 드론의 최대 지역 시장이 되었습니다. 이 지역은 레크리에이션을 목적으로 하는 이용자들의 대규모 도입 실적은 물론, 여행, 아웃도어 활동, 디지털 컨텐츠 제작이 자연스럽게 융합되는 문화의 혜택을 누리고 있습니다. FAA(미국 연방항공청)는 ‘드론 통합 운용 개념(Drone Integration Concept of Operations)’을 통해 2024년 8월 기준으로 86만 대 이상의 무인항공기(UAS)가 등록되어 있다고 발표했으며, 이는 사용자 기반의 규모를 보여줍니다. 해당 문서에서는 향후 드론의 활용 사례를 확대할 가능성이 있는 운영 체계에 대해서도 언급하고 있습니다. 단기적으로는 북미 소비자용 드론 시장이 규제 요건, 업그레이드 주기, 그리고 크리에이터 가구들의 강력한 수요에 의해 계속해서 형성될 것으로 보입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.01%를 기록하며 성장할 것으로 예상되며, 소비자용 드론 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 중국은 여전히 민수용 드론의 주요 제조 및 제품 개발 거점으로서, 이 지역에 견고한 공급 기반과 신속한 제품 업데이트 주기를 제공합니다. 인도 역시 정책적 관심이 높아지고 사용자 기반이 확대됨에 따라 그 중요성이 커지고 있으며, 2025년 9월에는 민간항공부가 ‘2025년 민간 드론 법안(초안)’을 발표했습니다. 일본과 호주는 활발한 수요, 야외 레저 활동, 그리고 고급 전자제품에 대한 높은 수용성을 통해 시장을 지탱하고 있습니다.

유럽은 소비자용 드론 시장에서 성숙 단계에 접어들었음에도 꾸준히 성장을 이어가고 있는 지역입니다. 이는 구매자가 보다 명확한 국경을 초월한 운영 규정의 혜택을 누릴 수 있고, 규정을 준수하는 제품의 선택지가 풍부하기 때문입니다. 프랑스, 독일, 영국이 수요의 주축을 이루고 있는 반면, 동유럽은 국가마다 무역 조건과 구매력이 달라 수요의 편차가 큽니다. 남미는 매출 규모 면에서는 여전히 작지만, 수입 가격 하락과 합리적인 가격대의 모델에 대한 접근성 확대로 인해 시장 진입 여건이 점차 개선되고 있습니다. 중동 및 아프리카는 여전히 초기 단계에 있는 지역이지만, 광범위한 소비자용 드론 시장에서 걸프 연안 국가들과 남아프리카가 가장 뚜렷한 수요 집중 지역으로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the consumer drones market size was valued at USD 6.23 billion in 2025, and is projected to grow from USD 7.08 billion in 2026 to USD 13.10 billion by 2031, growing at a CAGR of 13.11% from 2026 to 2031.

This report is Segmented by Product Type (Multi-Rotor, Fixed-Wing, and Hybrid), Flight Range (Less Than 4 Km, and More), Weight Class (Nano/Micro, Mini, Small, and Medium), Application (Photography and Videography, Racing and Sports, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Consumer Drones Market Trends and Insights

Rapid Fall in Li-ion Battery Cost Redefines Drone Economics

Battery cost deflation is making the consumer drones market easier to enter for both brands and buyers. Lower battery costs reduce the bill of materials and create room for longer flight times, better cooling, and safer power management without forcing higher shelf prices, which matters most in entry and mid-range devices, where a small hardware cost change can decide whether a product reaches a first-time buyer. It also changes how brands think about accessories, because upgraded battery packs can become repeat purchases rather than bundled one-time items. DJI demonstrated that battery design can shape the value proposition by promoting an Intelligent Flight Battery Plus option for its new Lito series and tying it to extended flight time. As that pattern spreads, the market will continue to expand across a wider range of price points without sacrificing feature depth.

Camera Modules as Commodity Components Widen the Mass Market

Camera hardware has moved much faster into the mass market than it did a few years ago, changing how the consumer drones market is priced and packaged. DJI introduced the Mini 5 Pro in September 2025 with a 1-inch CMOS sensor in a near-249 g body, demonstrating how advanced imaging could be packed into a lightweight consumer form factor. That shift reduces the old gap between premium and mainstream products and makes image quality feel like a starting requirement rather than a premium add-on. Once buyers expect strong video quality at lower prices, brands have less room to defend margins with camera hardware alone. SkyRover reinforced this direction in March 2026 by introducing a sub-249 g model priced below USD 300 with forward obstacle avoidance, 4K/60fps video, and 12 km HD transmission. The result is that the consumer drones market now rewards software ease, automated shooting, and reliable transmission more than raw sensor bragging rights.

Spectrum Congestion Constrains Reliability in Dense Deployments

The consumer drones market still relies heavily on crowded spectrum bands shared with Wi-Fi, Bluetooth, and an ever-growing set of connected devices. That creates a practical problem for users in cities, parks, and event settings, where signal noise can affect control confidence and video stability. The FCC adopted initial rules in July 2024 for drone operations in the 5030 to 5091 MHz band, but that framework is aimed at licensed advanced operations rather than everyday recreational flying. As a result, the core consumer segment remains exposed to the limits of the open ISM environment, even as the policy discussion moves forward, which matters because buyers do not judge a drone solely by its listed range; they judge it by how stable the connection feels in ordinary use. Until spectrum access improves for a broader user base, the consumer drones market will continue to face a reliability ceiling in dense environments.

Other drivers and restraints analyzed in the detailed report include:

- FPV Drone Racing Leagues Institutionalize a New Consumer Demand Category

- Social-Media Influencer Culture Accelerates Aspirational Drone Consumption

- IATA Battery Shipping Rules Add Cross-Border Logistics Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-rotor drones accounted for 70.11% of revenue in 2025, keeping them firmly at the center of the consumer drones market. Their strength comes from vertical takeoff, easy hovering, compact folding designs, and a flight style that matches photography and everyday recreational use. They also fit well with the lightweight product direction that now defines much of the mainstream category. For most buyers, a multi-rotor platform remains the simplest path to stable video and low learning friction.

Fixed-wing drones are forecast to grow at a 15.22% CAGR through 2031, indicating that a smaller share of the consumer drones market is seeking greater range and endurance. These products appeal more to prosumer users who care about area coverage and longer flight paths than to those who care about stationary hovering. Hybrid designs sit between the two camps and are slowly building relevance because they combine transit efficiency with hover capability. The main challenge is that the fixed-wing and hybrid side still has a thinner product pipeline than the multi-rotor base. Even so, the consumer drones market is likely to see greater differentiation as autonomous navigation improves and higher-skilled users seek aircraft that do more than capture short, local footage.

Drones with flight ranges below 4 km accounted for 57.62% of revenue in 2025, underscoring how strongly the consumer drones market still depends on neighborhood- and travel-scale use. This part of the category fits the needs of casual users who want portability, easy setup, and less regulatory friction. It also fits the weight profile of the lightest and most widely sold consumer aircraft. For mainstream buyers, practical use matters more than extreme distance, so short-range products keep the broadest volume base.

The segment above 8 km is forecast to expand at a 14.11% CAGR through 2031, providing the consumer drones market with a clear premium growth lane. What buyers are really paying for here is stable live video and stronger link confidence, not only the maximum distance shown on a box. DJI highlighted that premium direction in March 2026 when it launched the Avata 360 with O4+ transmission capable of 1080p/60fps video at up to 20 km. That kind of feature set pulls long-range performance closer to the enthusiast mainstream. As the consumer drone industry moves forward, transmission reliability is likely to matter more than raw range escalation alone.

Complete Report Scope:

- By Product Type

- Multi-Rotor

- Fixed-Wing

- Hybrid

- By Flight Range

- Less than 4 km

- 4 to 8 km

- More than 8 km

- By Weight Class

- Nano/Micro (Less than 250 g)

- Mini (250 g to Less than 2 kg)

- Small (2 to Less than 5 kg)

- Medium (More than 5 kg)

- By Application

- Photography and Videography

- Racing and Sports

- Recreational

- Environmental and Wildlife Observation

- Education and Training

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 37.65% of global revenue in 2025, making it the largest regional market for consumer drones. The region benefits from a large installed base of recreational users and a culture that readily blends travel, outdoor activities, and digital content creation. The FAA said there were more than 860,000 registered UAS as of August 2024 in its Drone Integration Concept of Operations, which shows the scale of the underlying user base.[5] That same document also points toward a future operating framework that could widen drone use cases over time. In the near term, the consumer drones market in North America remains shaped by compliance requirements, upgrade cycles, and strong demand from creator households.

Asia-Pacific is forecast to grow at a 15.01% CAGR through 2031, making it the fastest-growing regional market for consumer drones. China remains the central manufacturing and product development base for consumer drones, providing the region with strong supply depth and rapid product refresh cycles. India is also becoming more relevant as policy attention increases, and the user base expands, with the Ministry of Civil Aviation releasing the Draft Civil Drone Bill 2025 in September 2025. Japan and Australia add support through enthusiastic demand, outdoor recreation, and higher acceptance of premium electronics.

Europe remains a mature yet steadily growing part of the consumer drones market because buyers benefit from clearer cross-border operating rules and a larger pool of compliant products. France, Germany, and the UK anchor demand, while Eastern Europe is more uneven because trade conditions and purchasing power differ by country. South America is still smaller in revenue terms, but falling import prices and wider access to affordable models are improving entry conditions. The Middle East and Africa remain the earliest-stage region, with Gulf markets and South Africa as the clearest demand pockets in the broader consumer drones market.

- SZ DJI Technology Co., Ltd.

- Parrot Drones SAS

- Autel Robotics Co., Ltd.

- Skydio, Inc.

- Yuneec (ATL Drone)

- Holy Stone

- RYZE Tech Co., Ltd.

- Freefly Systems Inc.

- Zero Zero Robotics

- WALKERA (Guangzhou Huake Technology Co., Ltd.)

- FIMI Technology Ltd.

- Shenzhen Potensic Intelligent Co., Ltd.

- BETAFPV

- Jianjian Technology Co., Ltd.

- Guangdong Syma Model Aircraft Industrial Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid fall in Li-ion battery cost and energy density gains

- 4.2.2 High quality camera modules becoming commodity components

- 4.2.3 Growing popularity of FPV drone racing leagues

- 4.2.4 Smartphone-like replacement cycles emerging

- 4.2.5 Youth-driven influencer culture on social-media platforms

- 4.2.6 Increased availability of affordable, user-friendly drones

- 4.3 Market Restraints

- 4.3.1 Spectrum congestion in 2.4 GHz and 5 GHz ISM bands

- 4.3.2 Lithium-battery shipping restrictions tighten

- 4.3.3 Consumer-privacy litigation risk

- 4.3.4 Shortage of drone-qualified repair technicians

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Multi-Rotor

- 5.1.2 Fixed-Wing

- 5.1.3 Hybrid

- 5.2 By Flight Range

- 5.2.1 Less than 4 km

- 5.2.2 4 to 8 km

- 5.2.3 More than 8 km

- 5.3 By Weight Class

- 5.3.1 Nano/Micro (Less than 250 g)

- 5.3.2 Mini (250 g to Less than 2 kg)

- 5.3.3 Small (2 to Less than 5 kg)

- 5.3.4 Medium (More than 5 kg)

- 5.4 By Application

- 5.4.1 Photography and Videography

- 5.4.2 Racing and Sports

- 5.4.3 Recreational

- 5.4.4 Environmental and Wildlife Observation

- 5.4.5 Education and Training

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 Parrot Drones SAS

- 6.4.3 Autel Robotics Co., Ltd.

- 6.4.4 Skydio, Inc.

- 6.4.5 Yuneec (ATL Drone)

- 6.4.6 Holy Stone

- 6.4.7 RYZE Tech Co., Ltd.

- 6.4.8 Freefly Systems Inc.

- 6.4.9 Zero Zero Robotics

- 6.4.10 WALKERA (Guangzhou Huake Technology Co., Ltd.)

- 6.4.11 FIMI Technology Ltd.

- 6.4.12 Shenzhen Potensic Intelligent Co., Ltd.

- 6.4.13 BETAFPV

- 6.4.14 Jianjian Technology Co., Ltd.

- 6.4.15 Guangdong Syma Model Aircraft Industrial Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment