|

시장보고서

상품코드

2072580

HVAC 모터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)HVAC Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

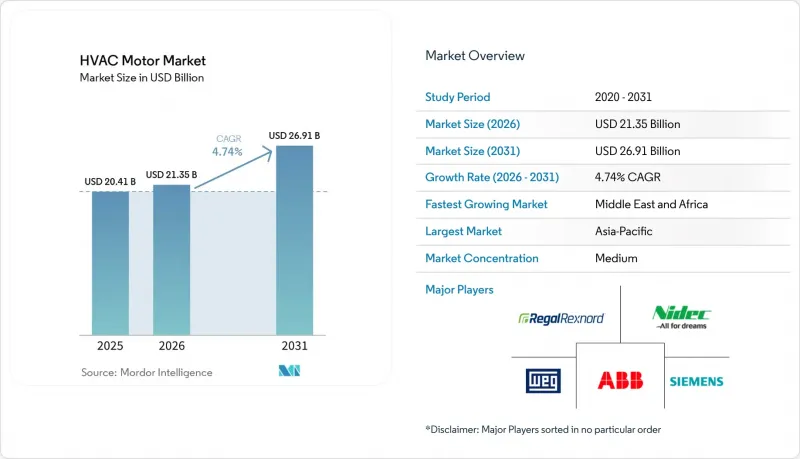

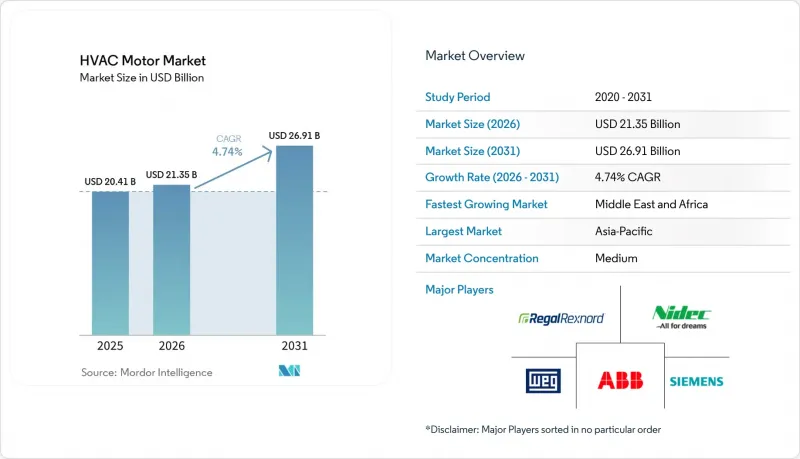

Mordor Intelligence에 의하면, HVAC 모터 시장 규모는 2025년 204억 1,000만 달러로 평가되었습니다. 2026년에는 213억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 4.74%로 성장을 지속하여, 2031년에는 269억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 모터의 유형(AC 유도 모터, 전자 정류(EC) 모터, 브러쉬리스 DC 모터 등), 정격 출력(1 HP 미만, 1 HP-5 HP 등), HVAC 장비의 유형(에어컨 및 히트 펌프, 환기 팬 및 송풍기 등), 최종 용도 분야(주거용, 상업용 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HVAC 모터 시장 동향 및 분석

모터 및 팬의 효율 기준 강화가 규정 준수에 기반한 업그레이드를 촉진

2025년 미국 에너지부(DOE)가 공표한 최종 규정에 따라, 0.25-3 HP 범위의 전기 모터에 대한 최소 효율 기준의 적용 범위가 확대되었습니다. 이는 HVAC 모터 시장에서 널리 사용되는 주거용 및 소규모 상업용 모터 부문에 직접적인 영향을 미치며, 2029년 1월 1일부터 준수가 의무화됩니다. DOE에 따르면, 이 규정에 따라 2058년까지 연료 주기 전체에서 8.8 쿼드의 에너지 절감 효과와 소비자에게 211억-475억 달러의 순현재가치 이익이 발생할 것으로 예상되는 반면, 제조업체의 총 전환 비용은 3억 6,000만 달러로 추산됩니다. 또 다른 직접 최종 규정에서는 이미 1-200 HP 범위의 일반용 전기 모터에 대해 2027년 6월 1일을 준수 기한으로 설정했으며, 이를 통해 많은 대형 상업용 HVAC 모터가 더 완화된 기준 하에 머물러 있던 큰 허점이 해소되었습니다. HVAC 모터 시장은 소형 주거용 팬 시스템부터 대형 상업용 송풍 설비에 이르기까지 광범위하게 아우르고 있기 때문에 이러한 기한이 겹치는 것은 중요한 문제이며, 그 결과 규정 준수 부담이 한 번에 매우 광범위한 설치 기반에 미치게 됩니다. 실질적인 영향으로, 구매자가 기존에는 효율 향상보다 초기 비용의 저렴함을 중시하던 용도에서도 PSC(고정 속도)나 쉐이드 폴형 모터의 조기 퇴출이 진행되고 있습니다. 이 규정에 따른 재편으로 인해, HVAC 모터 시장은 이미 더 엄격한 효율 요건을 충족하고 있는 EC(유도 전동기), PMSM(영구자석 동기 모터) 및 기타 가변 속도 플랫폼으로 나아가는 더 명확한 방향이 제시되고 있습니다.

열펌프 및 인버터식 HVAC의 보급에 따라, 시스템당 가변속 모터의 채택률이 확대되고 있습니다.

2024년과 2025년에는 전 세계 열펌프 판매가 주춤했으나, 미국에서는 2024년에도 여전히 성장세를 기록했으며, 열펌프 판매 대수는 천연가스 난방기를 계속해서 앞지르고 있습니다. 이는 주요 경제국의 HVAC 모터 시장에서 전기 난방이 여전히 견조한 수요의 견인차 역할을 하고 있음을 보여줍니다. 또한, IEA 보고서에 따르면 2024년 전 세계 히트펌프 판매 대수는 2020년 대비 27% 증가했으며, 이는 인버터식 기기의 도입 대수가 불과 몇년전과 비교해 시장에서 훨씬 더 확대되었음을 보여줍니다. 이 전망에 따르면, 2035년까지 일본과 미국의 공간 난방 수요의 40%를 히트펌프가 충당하게 될 것으로 예상되며, 단기적인 변동이 있더라도 중기적인 추세는 확고합니다. 최신 인버터 구동식 히트 펌프에는 가변속 압축기 모터 외에도 공기 순환, 밸브 제어, 보조 펌프용으로 여러 개의 브러쉬리스 모터와 영구자석 모터가 탑재되어 있어, 이로 인해 기존의 단속식 장치에 비해 시스템 1대당 모터 관련 부가가치가 높아지고 있습니다. 미국 환경보호청(EPA)의 ‘기술 전환(Technology Transitions)’ 프로그램에 따라, 2025년 1월 1일부터 주거용 에어컨 및 히트펌프에 GWP(지구온난화지수) 제한이 적용되었으며, 각 OEM 업체들은 R-32나 R-454B 등 A2L 냉매에 대응하는 제품의 재설계를 불가피하게 진행하고 있습니다. 이러한 재설계 작업을 통해, 단기적인 장비 출하 상황에 변동이 있는 분야라 하더라도 HVAC 모터 시장 전체에서 가변 속도 및 토크 매칭형 모터 플랫폼의 역할이 확대되고 있습니다.

고효율 모터의 높은 초기 비용이 보급을 저해하고 있습니다.

HVAC 모터 시장에서 높은 초기 비용은 여전히 실질적인 장벽으로 작용하고 있습니다. 이는 EC 모터, PMSM, 스위치드 릴랙턴스 모터가 동등한 정격 출력을 가진 표준 AC 유도 모터에 비해 여전히 현저히 비싸기 때문입니다. 이 문제는 신축 주택이나 그 밖의 가격에 민감한 판매 채널에서 가장 두드러지게 나타납니다. 이러한 채널에서는 개발업체나 OEM이 모터를 선정하지만, 전기 요금을 지불하는 것은 나중에 건물의 소유주나 거주자가 되기 때문입니다. 이러한 비용 부담 분담 구조는 특히 리베이트 제도나 에너지 성능 계약이 널리 보급되지 않은 신흥 시장에서 수명 주기 비용 절감의 이점을 주장하는 근거를 약화시키고 있습니다. 이 제약이 특히 중요한 이유는 유닛의 성장 속도가 가장 빠른 분야가 여전히 초기 비용의 압박을 가장 많이 받고 있는 대량 판매 부문에 집중되어 있기 때문입니다. 미국 에너지부(DOE)가 적용 범위를 확대한 모터 기준에 따르면, 2029년 이후 대상 제품은 더욱 엄격한 효율 기준을 충족해야 하므로, 이러한 개선 방향은 경제적 요인이라기보다는 규제적 요인에 기인한 것입니다. 규모 확대, 규제, 그리고 조달 노하우의 축적을 통해 가격 차이가 줄어들기 전까지는 HVAC 모터 시장에서 비용 중심의 응용 분야에 대한 하이엔드 설계의 확산은 계속해서 완만한 양상을 보일 것입니다.

부문별 분석

2025년, HVAC 모터 시장 매출의 63.55%를 AC 유도 모터가 차지하며, HVAC 모터 시장에서 가장 큰 점유율을 유지했습니다. 이는 OEM 조달 관행, 기존 설비와의 호환성, 그리고 매우 낮은 단위 제조 비용 덕분에 이 유형이 여전히 유리한 위치를 차지하고 있기 때문입니다. 이러한 규모는 미래의 강력한 입지 확보라기보다는 기존 설비 기반에 기인한 것입니다. 많은 구매자들은 여전히 배선 호환성이나 현장에서의 간편한 교체를 우선시하고 있기 때문입니다. EC 모터는 2031년까지 연평균 성장률(CAGR)이 5.54%로, 가장 빠르게 성장하고 있는 모터 유형입니다. 이는 빌딩 자동화 시스템에서 모터의 전자 장치가 수동적인 구성 요소가 아니라 운영 데이터 포인트로 취급되고 있기 때문입니다. HVAC 모터 업계에서는 이러한 변화로 인해 순수한 효율성뿐만 아니라 원격 측정, 변조 정밀도, 통합 제어의 가치도 변화하고 있습니다.

PMSM 및 브러쉬리스 DC 모터는 VRF 압축기 구동 및 정밀 공조 분야에서 여전히 최고의 성능을 자랑하고 있습니다. 이러한 분야에서는 토크 밀도, 소음 성능, 부분 부하 제어가 높은 가격 책정을 뒷받침하고 있습니다. ABB는 2026년 5월, 위험 구역용 ATEX 및 IECEx 인증을 획득한 세계 최초의 자석 없는 IE6 모터를 출시했습니다. 이는 공급업체가 희토류를 사용하지 않는 고효율 플랫폼을 활용하여 프리미엄 틈새 시장을 지키려 하고 있음을 보여줍니다. 스위치드 릴랙턴스 모터는 부분 부하 시 발생하는 소음에 대한 우려가 여전히 남아 있어, 개발이 진행되고 있음에도 불구하고 그 보급을 저해하는 요인이 되고 있습니다.

2025년 기준으로 1 HP 미만의 모터는 HVAC 모터 시장 규모의 58.89%를 차지했으며, 연평균 성장률(CAGR) 5.26%로 확대될 것으로 전망됩니다. 이는 팬 코일, 에너지 회수 환기 장치, 미니 스플릿 실내기, 플레넘 팬 등에서 소형 모터가 널리 사용되고 있음을 반영합니다. 또한, 멀티존 VRF나 덕트리스 시스템의 경우, 단일 대형 중앙 송풍기 대신 공조 대상 구역마다 전용 모터가 사용되기 때문에 이 부문 수요도 증가하고 있습니다. 이러한 구성 덕분에 설치 프로젝트당 모터 수가 두 배로 증가했으며, 최소 출력 대역은 교체용 및 신규 설치 모두에서 여전히 핵심적인 위치를 차지하고 있습니다. HVAC 모터 업계에서 더욱 중요한 변화는 이 출력 대역 내의 제품 구성이 PSC 제품에서 EC 및 PMSM 설계로 전환되고 있다는 점이며, 이로 인해 판매 대수 증가세가 완만하더라도 평균 판매 가격이 상승하고 있습니다.

1-5 HP 범위는 소규모 상업용 에어 핸들러 및 데이터센터의 인로우 냉각 장치로부터 이점을 얻고 있습니다. 이러한 시스템에서는 중복성과 부분 부하 제어를 위해, 하나의 대형 모터를 여러 개의 소형 모터로 구성한 팬 어레이가 채택되고 있습니다. 5-20 HP 범위는 옥상형 유닛, 냉각탑 및 대규모 공기 처리 시스템에서 여전히 중요하며, 이러한 시스템은 가동 시간이 길기 때문에 효율 향상을 위한 투자 회수를 정당화하기 쉽습니다. ABB는 2026년 1분기 모션 사업 부문에서 전년 동기 대비 9%의 수주 증가를 기록했다고 밝혔습니다. 이는 20 HP를 초과하는 대형 모터 용도를 포함하여, HVAC 및 빌딩 최종 시장 수요가 지속되고 있음을 반영합니다. 따라서 정격 출력 구성을 살펴보면, HVAC 모터 시장은 장비 판매 증가뿐만 아니라 시스템 전체의 기류 및 냉각 부하 배분 방식의 재검토를 통해서도 성장하고 있음을 알 수 있습니다.

지역별 분석

2025년, 아시아태평양은 HVAC 모터 시장 점유율의 45.54%를 차지하며, 생산과 수요 양면에서 가장 규모가 큰 지역 거점으로 자리매김했습니다. 중국은 여전히 중심적인 역할을 하고 있습니다. 이 나라의 HVAC 공급망은 모터, 압축기, 전자기기 및 최종 장비의 조립을 대규모로 연계하고 있으며, 이를 통해 해당 지역은 비용 경쟁력을 유지하고 신속하게 대응할 수 있게 되었습니다. 또한, 대규모 기존 설비에서 고효율 인버터 시스템이 구형 단속 기기를 대체하고 있는 만큼, 해당 지역의 동향은 단순한 수량 확대에서 더 우수한 제품 구성으로 전환되고 있습니다. 인도에서는 가정용 에어컨 보급률의 상승과 현지 생산 능력의 추가 확대로 인해 이러한 추세가 더욱 가속화되고 있습니다. ABB는 인도가 현재 자사의 4위 시장이라고 밝히며, 2026년까지 모든 사업 분야에서 7,500만 달러 규모의 제조 투자를 계획하고 있다고 밝혔습니다. 이는 남아시아에서 수요와 생산이 갖는 전략적 중요성을 뒷받침하는 것입니다.

북미에서는 규제 중심의 교체 주기가 진행되고 있으며, 2027년과 2029년에 예정된 미국 에너지부(DOE)의 규제 준수 기한이 이미 상업용 및 주거용 기기의 사양 결정에 영향을 미치고 있습니다. 국제에너지기구(IEA) 보고서에 따르면, 2024년 미국의 히트펌프 판매 대수는 15% 증가했으며, 냉매 전환에 따라 총 판매 대수는 감소했음에도 불구하고 2025년에도 히트펌프 판매 대수는 가스식 난방기를 계속해서 앞질렀습니다. 유럽도 비슷한 추세를 보이고 있으며, 더욱 엄격해진 에코디자인 요건과 건축물 성능 목표에 따라 구매자들은 고효율 모터와 통합형 드라이브를 선택하고 있습니다. WEG사는 2025년 10월, IE5+ 효율과 소형 폼 팩터를 갖춘 축류형 모터 ‘W80 AXgen’을 출시했습니다. 이는 공급업체가 에어 핸들러나 송풍기 등 효율을 중시하는 용도를 위해 얼마나 선진적인 플랫폼을 구축하고 있는지를 보여줍니다.

중동 및 아프리카는 GCC(걸프협력회의)의 메가 프로젝트, 높은 냉방 수요, 그리고 상업용 시스템에 대한 수요 증가에 힘입어 2031년까지 연평균 성장률(CAGR)이 4.96%에 달하며, 가장 빠르게 성장하고 있는 지역 부문입니다. 만안 시장의 극심한 주변 온도, 급속한 도시 개발, 그리고 건축 규제의 강화로 인해 장시간 가동 및 높은 냉각 부하에 대응할 수 있는 모터에 대한 수요가 지속되고 있습니다. 남미는 여전히 비교적 완만한 성장세를 보이는 시장이지만, 브라질은 국내 제조거점이 탄탄하여 상업시설 및 산업 시설공급 안정성과 리모델링 수요를 뒷받침하고 있어 여전히 중요한 시장입니다. 전반적으로 지역별 동향을 살펴보면, HVAC 모터 시장은 선진국 시장의 규제 기반 설비 교체와 성장세가 빠른 지역의 구조적인 냉방 수요가 결합되어 지탱되고 있음을 알 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the HVAC motor market size is expected to grow from USD 20.41 billion in 2025 to USD 21.35 billion in 2026 and is forecast to reach USD 26.91 billion by 2031 at 4.74% CAGR over 2026-2031.

This report is Segmented by Motor Type (AC Induction Motors, Electronically Commutated (EC) Motors, Brushless DC Motors, and More), Power Rating (Less Than 1 HP, 1 HP To 5 HP, and More), HVAC Equipment Type (Air Conditioner and Heat Pumps, Ventilation Fans and Blowers, and More), End-Use Sector (Residential, Commercial, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HVAC Motor Market Trends and Insights

Tightening Motor and Fan Efficiency Standards Drive Compliance-Mandated Upgrades

The US DOE final rule issued in 2025 expanded minimum efficiency standards to expanded scope electric motors in the 0.25-3 HP range, which directly affects the residential and light commercial motor categories widely used across the HVAC motor market, with compliance required from January 1, 2029. DOE said the rule will deliver 8.8 quads of full-fuel-cycle energy savings and USD 21.1-47.5 billion in consumer net present value benefits through 2058, while total manufacturer conversion costs are estimated at USD 360 million. A separate direct final rule already set a June 1, 2027, compliance date for general electric motors in the 1-200 HP range, which closes a major gap that had allowed many larger commercial HVAC motors to remain under weaker standards. These overlapping deadlines matter because the HVAC motor market serves both small residential fan systems and large commercial air-moving equipment, so the compliance burden is reaching a very broad installed base at once. The practical effect is faster retirement of PSC and shaded-pole designs, even in applications where buyers had historically favored low first cost over efficiency improvement. This rule-led reset is giving the HVAC motor market a clearer path toward EC, PMSM, and other variable-speed platforms that already align better with tighter efficiency expectations.

Heat Pump and Inverter HVAC Adoption Expand Variable-Speed Motor Content Per System

Global heat pump sales weakened in 2024 and 2025, but the United States still recorded growth in 2024, and heat pumps continued to outsell natural gas furnaces, which shows that electrified heating remains a durable demand driver for the HVAC motor market in major economies. The IEA also reported that global heat pump sales in 2024 were 27% above 2020 levels, which points to a much larger installed base of inverter-led equipment than the market had just a few years ago. The same outlook indicates that heat pumps will meet 40% of space heating demand in Japan and the United States by 2035, which keeps the medium-term direction intact even after short-term volatility. Each modern inverter-driven heat pump uses a variable-speed compressor motor and several additional brushless or permanent magnet motors for air movement, valve control, and auxiliary pumping, which raises motor content value per system versus older single-speed units. The US EPA Technology Transitions program applied GWP limits to residential air conditioners and heat pumps from January 1, 2025, forcing OEMs to redesign products around A2L refrigerants such as R-32 and R-454B. That redesign work is expanding the role of variable-speed and torque-matched motor platforms across the HVAC motor market, even where near-term equipment shipments have been uneven.

High Upfront Cost of Premium-Efficiency Motors Limits Adoption

High first cost remains a real barrier in the HVAC motor market because EC, PMSM, and switched reluctance units still carry a clear premium over standard AC induction motors at similar power ratings. This issue is most visible in new residential construction and other price-sensitive channels where the developer or OEM selects the motor, but the building owner or occupant pays the power bill later. That split weakens the case for lifecycle savings, especially in emerging markets where rebate programs and energy performance contracts are less common. The restraint is especially important because the fastest unit growth is still concentrated in the same high-volume segments that are most exposed to upfront cost pressure. The correction path is more regulatory than economic, since the US DOE expanded-scope motor standards will require covered products to meet tighter efficiency levels from 2029. Until scale, regulation, and procurement learning lower the premium, the HVAC motor market will continue to see slower penetration of top-end designs in cost-led applications.

Other drivers and restraints analyzed in the detailed report include:

- Commercial Retrofit Payback Compression Speeds Forced Upgrade Cycles

- Data Center Precision Cooling Creates Specification-Led Demand

- Control Electronics and Semiconductor Bottlenecks Slow Premium Motor Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC induction motors held 63.55% of the HVAC motor market revenue in 2025, keeping the largest position in the HVAC motor market because OEM sourcing habits, installed-base compatibility, and very low unit manufacturing costs still favor them. This scale came more from the legacy installed base than from stronger future positioning, since many buyers still prioritize wiring compatibility and simple field replacement. EC motors are the fastest-growing motor type at a 5.54% CAGR through 2031, as building automation systems increasingly treat motor electronics as operating data points rather than passive components. In the HVAC motor industry, that shift is changing the value of telemetry, modulation accuracy, and integrated controls alongside pure efficiency.

PMSM and brushless DC motors continue to hold the highest-performance positions in VRF compressor drives and precision air handling, where torque density, acoustics, and part-load control support higher prices. ABB launched the world's first magnet-free IE6 motor certified to ATEX and IECEx for hazardous areas in May 2026, which showed how suppliers are using rare-earth-free high-efficiency platforms to defend premium niches. Switched reluctance motors still face acoustic concerns at partial load, which is limiting broader use even as development work continues.

Less than 1 HP motors accounted for 58.89% of the HVAC motor market size in 2025 and are anticipated to expand at 5.26% CAGR, reflecting the heavy use of small motors in fan coils, energy recovery ventilators, mini-split indoor units, and plenum fans. Demand in this class is also rising because multi-zone VRF and ductless systems use dedicated motors in each conditioned zone rather than a single large central blower. That architecture multiplies motor count per installed project and keeps the smallest power band central to both replacement and new installations. Within the HVAC motor industry, the more important change is the mix shift inside this band from PSC products toward EC and PMSM designs, which lifts average selling prices even when unit growth is moderate.

The 1-5 HP range is gaining from light commercial air handlers and data center in-row cooling units, where fan arrays replace one larger motor with several smaller ones for redundancy and part-load control. The 5-20 HP band remains important in rooftop units, cooling towers, and larger air handling systems, where efficiency-upgrade payback is easier to justify under long operating hours. ABB reported 9% comparable order growth in its Motion business in Q1 2026, reflecting continued demand from HVAC and buildings end markets, including large-motor applications above 20 HP. The power-rating mix, therefore, shows that the HVAC motor market is growing not only through more equipment sales but also through a redesign of how airflow and cooling loads are distributed across systems.

Complete Report Scope:

- By Motor Type

- AC Induction Motors

- Electronically Commutated (EC) Motors

- Brushless DC Motors

- Permanent Magnet Synchronous Motors

- Switched Reluctance Motors

- By Power Rating

- Less than 1 HP

- 1 HP to 5 HP

- 5 HP to 20 HP

- Above 20 HP

- By HVAC Equipment Type

- Air Conditioners and Heat Pumps

- Ventilation Fans and Blowers

- Furnaces and Boilers

- Chillers and Cooling Towers

- By End-Use Sector

- Residential

- Commercial

- Industrial and Institutional

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific held 45.54% of the HVAC motor market share in 2025, making it the largest regional base for both production and demand. China remains central because its HVAC supply chains connect motors, compressors, electronics, and final equipment assembly at scale, which keeps the region cost-competitive and highly responsive. The regional story is also moving from pure volume toward better product mix, as higher-efficiency inverter systems replace older single-speed equipment across a large installed base. India is adding to this momentum through rising residential air conditioning penetration and a broader expansion of local manufacturing capacity. ABB said India is now tied as its fourth-largest market and outlined planned 2026 manufacturing investment of USD 75 million across its businesses, which underscores the strategic weight of South Asian demand and production.

North America is moving through a rule-led upgrade cycle, with DOE compliance dates in 2027 and 2029 already shaping specification decisions in commercial and residential equipment. The IEA reported that US heat pump sales rose 15% in 2024 and that heat pumps continued to outsell gas furnaces in 2025, even though overall sales volumes weakened during the refrigerant transition. Europe is following a parallel path, where tighter ecodesign expectations and building performance targets are pushing buyers toward premium-efficiency motors and integrated drives. WEG launched its W80 AXgen axial flux motor in October 2025 with IE5+ efficiency and a smaller form factor, showing how suppliers are positioning advanced platforms for efficiency-led applications such as air handlers and blowers.

The Middle East and Africa are the fastest-growing regional segments at a 4.96% CAGR through 2031, supported by GCC megaprojects, high cooling intensity, and rising demand for commercial-grade systems. Extreme ambient temperatures, rapid urban development, and tighter building rules in Gulf markets are sustaining demand for motors built for long operating hours and heavy cooling loads. South America remains a more measured growth market, but Brazil still matters because domestic manufacturing depth supports supply availability and replacement demand across commercial and industrial installations. Overall, the regional mix shows that the HVAC motor market is being supported by a combination of rule-driven upgrades in developed markets and structural cooling demand in faster-growing climates.

- Regal Rexnord Corporation

- Nidec Corporation

- WEG S.A.

- ABB Ltd.

- Siemens AG

- Johnson Electric Holdings Ltd.

- AMETEK, Inc.

- Toshiba International Corp.

- TECO-Westinghouse Motor Co.

- Mitsubishi Electric Corp.

- Emerson Electric Co. (Copeland)

- Danfoss A/S

- Hitachi, Ltd.

- Brook Crompton UK Ltd.

- Genteq

- Grundfos

- Infinitum

- Wolong Electric Group Co. Ltd.

- Yaskawa Electric Corp.

- Schneider Electric SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Motor and Fan Efficiency Standards

- 4.2.2 Commercial Retrofit Payback Compression

- 4.2.3 Heat Pump and Inverter HVAC Adoption

- 4.2.4 Indoor Air Quality and Ventilation Upgrades

- 4.2.5 Data Center Precision Cooling and Fan-Wall Retrofits

- 4.2.6 Low-GWP Refrigerant Transition Re-Engineering

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Premium-Efficiency Motors

- 4.3.2 Control Electronics and Semiconductor Bottlenecks

- 4.3.3 Installer and Commissioning Gaps for Advanced Retrofits

- 4.3.4 Refrigerant Transition Timing and Enforcement Uncertainty

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 AC Induction Motors

- 5.1.2 Electronically Commutated (EC) Motors

- 5.1.3 Brushless DC Motors

- 5.1.4 Permanent Magnet Synchronous Motors

- 5.1.5 Switched Reluctance Motors

- 5.2 By Power Rating

- 5.2.1 Less than 1 HP

- 5.2.2 1 HP to 5 HP

- 5.2.3 5 HP to 20 HP

- 5.2.4 Above 20 HP

- 5.3 By HVAC Equipment Type

- 5.3.1 Air Conditioners and Heat Pumps

- 5.3.2 Ventilation Fans and Blowers

- 5.3.3 Furnaces and Boilers

- 5.3.4 Chillers and Cooling Towers

- 5.4 By End-Use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial and Institutional

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Regal Rexnord Corporation

- 6.4.2 Nidec Corporation

- 6.4.3 WEG S.A.

- 6.4.4 ABB Ltd.

- 6.4.5 Siemens AG

- 6.4.6 Johnson Electric Holdings Ltd.

- 6.4.7 AMETEK, Inc.

- 6.4.8 Toshiba International Corp.

- 6.4.9 TECO-Westinghouse Motor Co.

- 6.4.10 Mitsubishi Electric Corp.

- 6.4.11 Emerson Electric Co. (Copeland)

- 6.4.12 Danfoss A/S

- 6.4.13 Hitachi, Ltd.

- 6.4.14 Brook Crompton UK Ltd.

- 6.4.15 Genteq

- 6.4.16 Grundfos

- 6.4.17 Infinitum

- 6.4.18 Wolong Electric Group Co. Ltd.

- 6.4.19 Yaskawa Electric Corp.

- 6.4.20 Schneider Electric SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment