|

시장보고서

상품코드

2072583

애플리케이션 프로그래밍 인터페이스(API) 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Application Programming Interface Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

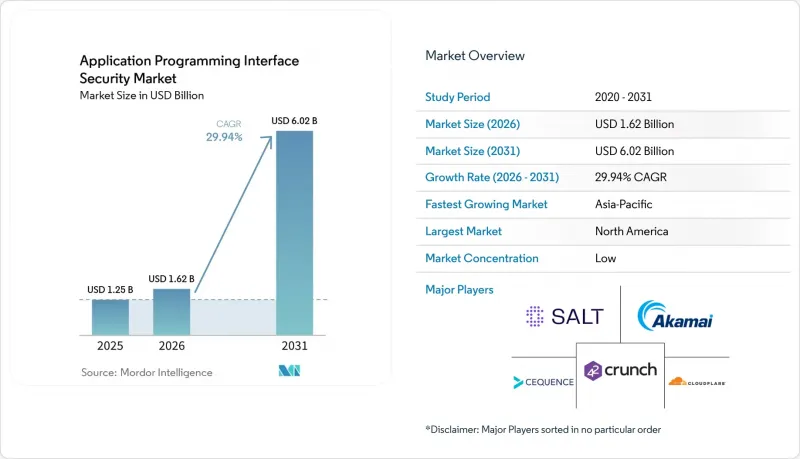

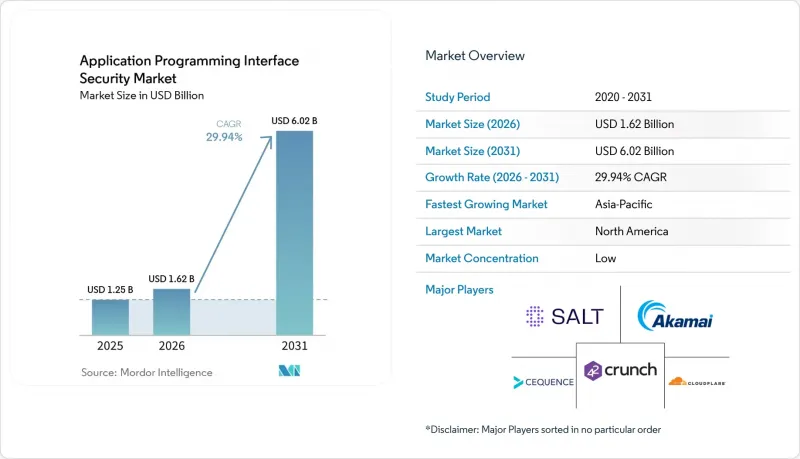

Mordor Intelligence에 의하면, 애플리케이션 프로그래밍 인터페이스(API) 보안 시장 규모는 2025년 12억 5,000만 달러로 평가되었습니다. 2026년에는 16억 2,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 29.94%로 성장을 지속하여, 2031년에는 60억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(솔루션, 서비스(도입·통합 등)), 도입 형태별(On-Premise, 클라우드, 하이브리드), 기업 규모별(중소기업(SME), 대기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 제조업, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 애플리케이션 프로그래밍 인터페이스(API) 보안 시장 동향 및 인사이트

API 공격 빈도와 침해로 인한 비용 증가

API(애플리케이션 프로그래밍 인터페이스) 보안 시장은 확대 추세를 보이고 있습니다. 이는 API 공격이 빈번하게 발생하게 되면서, 보안 담당자에게 예산 측면에서 시급한 과제가 되고 있기 때문입니다. 아카마이의 보고서에 따르면, 조사 대상인 전 세계 조직의 87%가 2025년에 API 관련 보안 사고를 겪었습니다. 해당 보도자료에 따르면, 조직당 일일 평균 API 공격 건수는 2024년 121건에서 2025년에는 258건으로 증가하여 전년 대비 113% 증가했습니다. 또한 아카마이는 API 엔드포인트나 용도 리소스를 표적으로 삼는 경우가 많은 레이어 7 DDoS 공격이 지난 2년 동안 104% 증가했다는 점도 지적하고 있습니다. 이러한 경향이 중요하게 여겨지는 이유는 보안 팀이 더 이상 고립된 부정 이용 사례를 처리하는 것이 아니라, 용도 로직, 속도 제한, 액세스 제어를 기계의 속도로 테스트하는 자동화된 공격 캠페인을 처리하고 있기 때문입니다. 그 결과, API 보안 시장은 단순히 도구를 구매하는 것보다는 손실 방지, 가동 시간 확보, 규제 관련 위험 대응과 점점 더 밀접하게 연결되고 있습니다.

클라우드 네이티브 아키텍처에서 API의 급속한 증가

애플리케이션 프로그래밍 인터페이스(API) 보안 시장은 클라우드 네이티브 아키텍처가 거버넌스가 필요한 새로운 인터페이스를 빠르게 만들어내고 있다는 점에 힘입어 성장하고 있습니다. Salt Security에 따르면, 응답자의 47% 가까이가 전년 대비 API가 51%에서 100%까지 증가했다고 보고했으며, 이는 엔드포인트 수가 급속히 늘어나고 있음을 보여줍니다. 마이크로서비스 환경에서는 새로운 서비스가 추가될 때마다 개별 엔드포인트, ID, 동서 방향 트래픽 채널이 도입될 가능성이 있지만, 기존 모니터링 도구는 이러한 요소를 상세하게 분석하도록 설계되지 않았습니다. 컨테이너의 자동 스케일링으로 인해 이 문제는 더욱 심각해지고 있습니다. API는 정적 문서나 수동 검토가 따라잡을 수 없을 만큼 빠른 속도로 등장하고, 이동하며, 폐지될 가능성이 있기 때문입니다. 이 운영 모델에서는 인프라 자체가 끊임없이 변화하기 때문에 엔지니어링 실무가 성숙한 기업 내에서도 섀도우 API나 관리 대상에서 제외된 API의 수가 증가하게 됩니다. 이것이 바로 API 보안 시장에서 감지, 포지션 관리, 행동 기반 모니터링이 단순한 선택적 부가 기능이 아니라 핵심 제어 계층으로 자리 잡은 이유입니다.

하이브리드 및 멀티 클라우드 환경에서의 통합 복잡성

애플리케이션 프로그래밍 인터페이스(API) 보안 시장은 여전히 여러 과제에 직면해 있습니다. 많은 기업이 클라우드, On-Premise, 프라이빗 인프라에 걸쳐 동시에 제어를 수행해야 하기 때문입니다. 이러한 환경에서는 서로 다른 게이트웨이, 인증 방식, 검사 지점, 로그 형식이 사용되는 경우가 많아, 통일된 대책을 적용하기 어렵게 만들고 있습니다. 또한, 트래픽이나 소유자가 여러 도구로 분산되어 있으면 보안 팀은 API의 동작 중 일부만 파악할 수 있기 때문에 런타임 컨텍스트도 약화됩니다. Harness는 “Traceable Cloud WAAP”를 통합된 디스커버리, 런타임 보호, 봇 대응, DDoS 방어를 핵심으로 삼아 자리매김하고 있으며, 이는 고객이 여전히 연동되지 않은 여러 제어 수단을 실용적인 공통 레이어로 대체하고자 하고 있음을 보여줍니다. 아카마이의 “코드에서 런타임으로의 매핑”도 동일한 논리에 기반을 두고 있으며, 가동 중인 API의 감지 결과를 코드 소유자와 연결함으로써 개발자와 보안 팀 간의 협업 격차를 줄입니다. 이러한 연계 구축이 용이해질 때까지는 통합을 위해 시행된 조치들이 API 보안 시장 전반의 도입 속도를 계속해서 제한할 것으로 보입니다.

부문별 분석

2025년, 솔루션은 애플리케이션 프로그래밍 인터페이스(API) 보안 시장 점유율의 62.44%를 차지하며, 구성 요소 중 주도적인 위치를 유지했습니다. 이 리드는 대규모 API 환경 전반에 걸친 지속적인 감지, 런타임 보호, 포지션 관리 및 거버넌스의 필요성을 반영하고 있습니다. API 보안 시장에서는 알려지지 않은 엔드포인트를 식별하고, 실시간 트래픽을 모니터링하며, 악용이 침해로 확대되기 전에 비정상적인 행동을 감지할 수 있는 솔루션이 주목받고 있습니다. 2026년에는 서비스 간 트래픽이나 AI를 활용한 워크플로우를 정적인 규칙만으로는 판단하기 어려워지고 있기 때문에 행동 분석의 중요성이 커지고 있습니다. 또한 구매자들은 감지 결과를 코드 소유자나 시정 조치와 연계하는 워크플로우 기능을 더욱 중요하게 여기게 되었으며, 이는 플랫폼 기능 확충을 위한 움직임을 뒷받침하고 있습니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 29.98%를 나타낼 것으로 예측되며, 이는 플랫폼 도입에 여전히 막대한 구현 작업이 수반됨을 보여줍니다. 고객은 혼합 환경 전반에 걸쳐 API 보안 도구를 게이트웨이, CI/CD 워크플로우, ID 관리 및 보안 운영 프로세스와 연동하기 위한 지원을 필요로 하는 경우가 많습니다. API 보안 업계에서 이 서비스에 대한 수요는 규정 준수 프로그램 및 하이브리드 환경으로 인해 통합이 미흡할 경우 비용 증가로 이어지는 부문에서 가장 두드러지게 나타나고 있습니다. 또한, 많은 팀이 여전히 감지 설정 조정, 경보 우선순위 지정, 담당자 지정 등에서 지원이 필요하기 때문에 교육 및 컨설팅의 중요성도 커지고 있습니다. 그럼에도 불구하고, API 보안 시장에서는 상업적 가치의 상당 부분이 여전히 확장 가능한 소프트웨어 플랫폼에 집중되어 있지만, 서비스는 도입의 품질과 장기적인 고객 유지를 좌우하는 역할을 하고 있습니다.

2025년에는 애플리케이션 프로그래밍 인터페이스(API) 보안 시장의 58.31%를 클라우드 배포가 차지했으며, SaaS 제공이 가장 큰 도입 형태가 되었습니다. 이러한 상황은 출시 후 몇 시간 이내에 새로운 API가 등장할 수 있는 환경에서 배포 속도 향상, 업데이트 용이성, 정책 배포의 간소화가 실현되고 있음을 반영합니다. API 보안 시장은 벤더가 로컬 업그레이드 주기를 기다릴 필요 없이, 중앙 집중식으로 감지 모델을 개선하고 적용 범위를 확대할 수 있다는 점에서도 클라우드 제공의 이점을 누리고 있습니다. 한편, On-Premise 구축은 로컬에서의 검사 및 기밀 트래픽에 대한 보다 엄격한 통제가 여전히 중요한 규제 환경에서 여전히 중요한 역할을 수행하고 있습니다. 벤더는 단일 운영 모델이 모든 기업에 적합하다고 가정할 수 없기 때문에 이러한 이분법을 통해 제공 전략의 유연성이 유지되고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 30.41%를 나타낼 것으로 예측되며, 이는 다양한 도입 방식 중 가장 빠르게 성장하는 대안이 될 것입니다. 대규모 조직이 장기간에 걸쳐 완전히 클라우드 기반 또는 완전히 On-Premise 방식으로 운영되는 경우는 드물기 때문에 하이브리드 환경용 API 보안 시장 규모는 확대되고 있습니다. 구매자들은 각 계층별로 개별 도구를 관리하는 대신, WAF, DDoS 대응, 봇 관리, API 보안을 아우르며 통합적으로 제어할 수 있는 기능을 점점 더 요구하고 있습니다. Harness는 “Traceable Cloud WAAP”에서 이러한 통합 접근 방식을 채택한 반면, Cloudflare는 “API Shield”에 능동적인 취약점 스캔 기능을 확대하여, 수동적인 모니터링과 직접적인 익스플로잇 테스트 간의 격차를 줄였습니다. 예측 기간 동안 고객의 환경이 하이브리드 상태를 유지하는 가운데, 실행 시 가시성과 개발자 워크플로우를 모두 지원할 수 있는 벤더는 API 보안 시장에서 더 큰 점유율을 확보할 가능성이 높을 것으로 보입니다.

지역별 분석

2025년, 북미는 애플리케이션 프로그래밍 인터페이스(API) 보안 시장 점유율의 38.74%를 차지하며 해당 지역 1위 자리를 유지했습니다. 이 분야의 대부분은 미국이 주도하고 있으며, 미국의 대기업들은 클라우드의 광범위한 도입과 함께 결제 및 의료 관련 규제로 인한 강력한 규정 준수 압박을 동시에 받고 있습니다. 또한, 이 지역에는 전문 벤더와 플랫폼 제공업체를 모두 아우르는 탄탄한 벤더 기반이 구축되어 있어, 고객은 성숙한 제품과 통합 파트너를 활용할 수 있다는 이점도 있습니다. 보고되는 사고의 빈도가 경영진의 관심을 높이고 있으며, 이것이 API의 감지, 모니터링 및 대응에 사용되는 안정적인 예산을 뒷받침하고 있습니다. 이러한 수요의 성숙도, 공급업체의 입지, 규제 압력이 복합적으로 작용함에 따라 북미는 API 보안 시장에서 지속적인 선두 위치를 유지하고 있습니다.

2026년에도 유럽은 API 보안 시장에서 전략적으로 중요한 두 번째 지역으로 자리매김했습니다. DORA(디지털 운영 리스크 관리 규정)는 규제 대상 금융기관 전반에 걸쳐 지속적인 ICT 리스크 관리 및 제3자 감독에 관한 기준을 강화함으로써, API의 현황 파악, 모니터링 및 관리에 대한 증거에 대한 수요를 직접적으로 뒷받침하고 있습니다. 또한, 각 지역의 구매 담당자들은 감사 가능성과 문서화된 운영 관리를 중시하고 있으며, 이에 따라 감지 결과를 거버넌스 프로세스와 연동할 수 있는 플랫폼이 선호되고 있습니다. 따라서 유럽에서의 지출은 단일 운영 모델 내에서 파트너 API 및 규정 준수 요건을 관리할 수 있는 통합 플랫폼에 계속 집중되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 30.15%를 기록하며 성장할 것으로 예상되며, API 보안 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 아카마이(Akamai)의 조사에 따르면, 인도 조사 대상 기관의 93%, 싱가포르의 90%가 전년도에 적어도 한 건의 API 보안 사고를 보고한 것으로 나타나, API 사용이 보안 통제의 성숙도를 얼마나 빠르게 앞지르고 있는지가 여실히 드러났습니다. 해당 조사에 따르면, API 보안 사고로 인한 일본 기업 1곳당 평균 손실액은 건당 2억 4,600만 엔(171만 달러)에 달했으며, 한편 중국 응답자들만이 API 위협 대응을 사이버 보안의 최우선 과제로 꼽았습니다. 이러한 급속한 디지털 성장, 높은 위험 노출, 경영진의 강력한 관심 등이 결합되어 아시아태평양은 API 보안 시장에서 가장 역동적인 성장 동력이 되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the application programming interface security market size is expected to grow from USD 1.25 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at a CAGR of 29.94% over 2026-2031.

This report is Segmented by Component (Solutions, and Services [Implementation and Integration, and More]), Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), End-User Industry (BFSI, Retail and ECommerce, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Application Programming Interface Security Market Trends and Insights

Rising API Attack Frequency And Breach Costs

The application programming interface security market is moving higher because API attacks are now frequent enough to create direct budgetary urgency for security leaders. Akamai reported that 87% of surveyed global organizations experienced an API-related security incident in 2025. The same release said average daily API attacks per organization rose to 258 in 2025 from 121 in 2024, which marked a 113% year-over-year increase. Akamai also noted that Layer 7 DDoS attacks, which commonly target API endpoints and application resources, climbed 104% over the prior 2 years. This pattern matters because security teams are no longer dealing with isolated misuse, but with automated campaigns that test application logic, rate limits, and access controls at machine speed. As a result, the API security market is increasingly tied to loss prevention, uptime protection, and regulatory exposure instead of discretionary tool spending.

Rapid API Proliferation Across Cloud-Native Architectures

The application programming interface security (API) market is also being driven by the speed at which cloud-native architectures create new interfaces that require governance. Salt Security said nearly 47% of respondents reported API growth of 51%-100% over the prior year, indicating that endpoint inventories are expanding rapidly. In microservices environments, each new service can introduce separate endpoints, identities, and east-west traffic paths that legacy monitoring tools were not designed to interpret in depth. Auto-scaling containers make the problem harder because APIs can appear, move, and retire faster than static documentation or manual reviews can keep pace. That operating model increases the number of shadow and unmanaged APIs, even within firms with mature engineering practices, because the infrastructure itself changes continuously. This is why discovery, posture management, and behavior-based monitoring have become core control layers in the API security market rather than optional add-ons.

Integration Complexity Across Hybrid And Multi-Cloud Estates

The application programming interface security market still faces friction because many enterprises need to enforce controls across cloud, on-premises, and private infrastructure simultaneously. Those environments often rely on different gateways, identity methods, inspection points, and logging formats, which makes uniform policy enforcement difficult. Fragmentation also weakens runtime context because security teams may see only a slice of API behavior when traffic and ownership are split across multiple tools. Harness positioned Traceable Cloud WAAP around unified discovery, runtime protection, bot mitigation, and DDoS defense, which shows that customers are still trying to replace several disconnected controls with a workable common layer. Akamai's code-to-runtime mapping follows the same logic by linking live API findings to code ownership and reducing the coordination gap between developers and security teams. Until these connections become easier to deploy, integration efforts will continue to limit the pace of adoption across the API security market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Compliance And Data Governance Obligations

- Growth Of Partner, Fintech, And Ecosystem APIs

- Shortage Of Specialized API Security Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 62.44% of the application programming interface security market share in 2025, maintaining its leading position within the component mix. That lead reflects the need for continuous discovery, runtime protection, posture management, and governance across large API estates. The API security market favors solutions that can identify unknown endpoints, monitor live traffic, and surface unusual behavior before misuse escalates into a breach. Behavioral analytics has become more important in 2026 because service-to-service traffic and AI-assisted workflows are harder to judge with static rules alone. Buyers are also placing more weight on workflow features that connect findings to code ownership and remediation, which supports the shift toward broader platform functionality.

Services are projected to grow at a 29.98% CAGR through 2031, underscoring the significant implementation work still surrounding platform adoption. Customers often need support to connect API security tools to gateways, CI/CD workflows, identity controls, and security operations processes across mixed environments. In the API security industry, this service pull is strongest where compliance programs and hybrid estates raise the cost of poor integration. Training and consulting are also becoming increasingly relevant, as many teams still need help with discovery tuning, alert triage, and ownership mapping. Even so, the API security market continues to place the bulk of commercial value in scalable software platforms, while services shape deployment quality and long-term account retention.

Cloud deployment accounted for 58.31% of the application programming interface (API) security market in 2025, making SaaS delivery the largest deployment mode. This position reflects faster rollout, easier updates, and simpler policy distribution in environments where new APIs can appear within hours of a release. The API security market also benefits from cloud delivery because vendors can improve detection models centrally and extend coverage without waiting for local upgrade cycles. At the same time, on-premises deployments remain relevant in regulated settings where local inspection and tighter control over sensitive traffic still matter. That split keeps delivery strategy flexible, because vendors cannot assume that one operating model fits every enterprise.

Hybrid deployment is forecast to grow at a 30.41% CAGR through 2031, which makes it the fastest-growing option in the mix. The API security market size for hybrid environments is expanding because large organizations rarely operate fully in the cloud or fully on premises for long periods. Buyers increasingly want combined control across WAF, DDoS mitigation, bot management, and API security rather than maintaining separate tools for each layer. Harness used that combined approach in Traceable Cloud WAAP, while Cloudflare extended API Shield with active vulnerability scanning to narrow the gap between passive observation and direct exploit testing. Vendors that can support both runtime visibility and developer workflows are likely to capture a larger share of the API security market as customer estates remain mixed through the forecast period.

Complete Report Scope:

- By Component

- Solutions

- Services

- Implementation and Integration

- Training and Consulting

- Support and Maintenance

- By Deployment Mode

- On-Premises

- Cloud

- Hybrid

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- BFSI

- Retail and eCommerce

- Healthcare and Life Sciences

- IT and Telecom

- Government and Public Sector

- Manufacturing

- Media and Entertainment

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.74% of the application programming interface security market share in 2025, maintaining the region's lead. The United States drove most of that position because large enterprises there combine deep cloud adoption with strong compliance pressure from payment and healthcare rules. The region also benefits from a dense vendor base that includes both specialists and platform providers, enabling customers to access mature products and integration partners. Reported incident frequency has kept executive attention high, which supports steady budgets for API discovery, monitoring, and response. This combination of demand maturity, vendor presence, and regulatory pressure gives North America a durable lead in the API security market.

Europe remained a strategically important secondary region for the API security market in 2026. DORA raised the standard for continuous ICT risk management and third-party oversight across regulated financial entities, which directly supports demand for API inventory, monitoring, and control evidence. Regional buyers also place strong weight on auditability and documented operational control, which favors platforms that can connect detection outcomes to governance processes. That keeps European spending focused on consolidated platforms that can manage partner APIs and compliance requirements within a single operating model.

Asia-Pacific is projected to grow at a 30.15% CAGR through 2031, making it the fastest-growing region in the API security market. Akamai found that 93% of surveyed organizations in India and 90% in Singapore reported at least 1 API security incident in the prior year, underscoring how quickly API use has outpaced control maturity. The same research said API security incidents cost Japanese enterprises JPY 246 million (USD 1.71 million) per incident on average, while Chinese respondents were the only group to rank API threat protection as their top cybersecurity priority. This mix of rapid digital growth, high exposure, and stronger executive focus makes Asia-Pacific the most dynamic regional growth engine for the API security market.

- Salt Security Inc.

- Akamai Technologies Inc.

- Cequence Security Inc.

- 42Crunch Ltd.

- Cloudflare Inc.

- Wallarm Inc.

- Wib Security Ltd.

- Data Theorem Inc.

- Imperva Inc.

- Traceable AI Inc.

- Datadog Inc.

- Kong Inc.

- Tyk Technologies Ltd.

- Axway Software SA

- MuleSoft LLC (Salesforce)

- Google LLC (APIgee)

- Rapid7 Inc.

- Sensedia S.A.

- Forum Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising API Attack Frequency and Breach Costs

- 4.2.2 Rapid API Proliferation Across Cloud-Native Architectures

- 4.2.3 Expanding Compliance and Data Governance Obligations

- 4.2.4 Growth of Partner, Fintech, and Ecosystem APIs

- 4.2.5 AI Agents and LLM Workflows Making APIs the AI Control Plane

- 4.2.6 Shadow, Zombie, and Unmanaged APIs Forcing Discovery-Led Security Spend

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across Hybrid and Multi-Cloud Estates

- 4.3.2 Shortage of Specialized API Security Talent

- 4.3.3 False Confidence in Legacy WAF and Authentication-Centric Controls

- 4.3.4 Evolving MCP and Agentic AI Security Standards and Ownership Gaps

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Training and Consulting

- 5.1.2.3 Support and Maintenance

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Retail and eCommerce

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 IT and Telecom

- 5.4.5 Government and Public Sector

- 5.4.6 Manufacturing

- 5.4.7 Media and Entertainment

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salt Security Inc.

- 6.4.2 Akamai Technologies Inc.

- 6.4.3 Cequence Security Inc.

- 6.4.4 42Crunch Ltd.

- 6.4.5 Cloudflare Inc.

- 6.4.6 Wallarm Inc.

- 6.4.7 Wib Security Ltd.

- 6.4.8 Data Theorem Inc.

- 6.4.9 Imperva Inc.

- 6.4.10 Traceable AI Inc.

- 6.4.11 Datadog Inc.

- 6.4.12 Kong Inc.

- 6.4.13 Tyk Technologies Ltd.

- 6.4.14 Axway Software SA

- 6.4.15 MuleSoft LLC (Salesforce)

- 6.4.16 Google LLC (Apigee)

- 6.4.17 Rapid7 Inc.

- 6.4.18 Sensedia S.A.

- 6.4.19 Forum Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment