|

시장보고서

상품코드

2072586

냉동 쿨러 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Refrigeration Coolers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

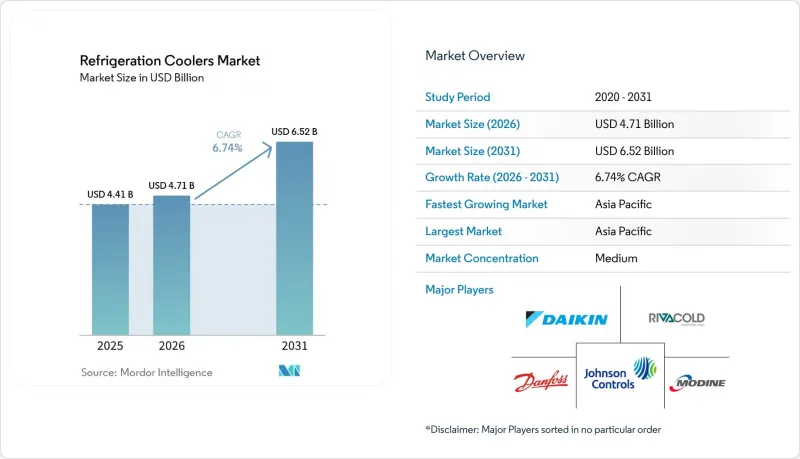

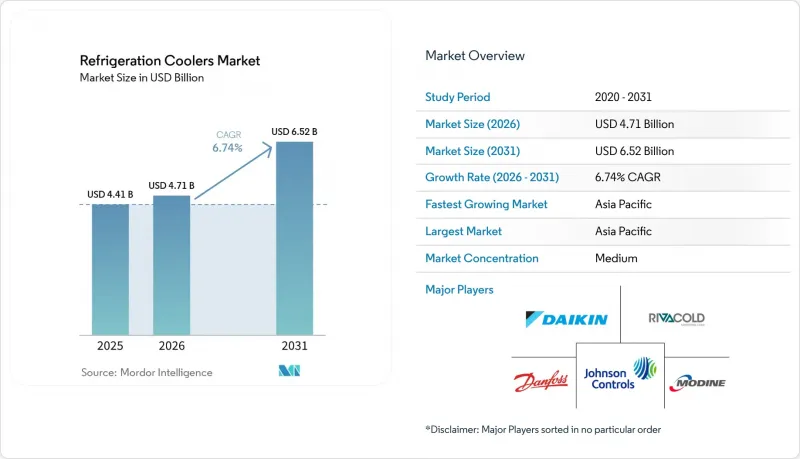

Mordor Intelligence에 의하면, 냉동 쿨러 시장 규모는 2025년 44억 1,000만 달러로 평가되었습니다. 2026년 47억 1,000만 달러에서 2031년까지 65억 2,000만 달러로 확대되며 2026-2031년까지 연평균 복합 성장률(CAGR)은 6.74%를 나타낼 전망입니다.

본 보고서는 제품 유형(증발기 및 공기 냉각기, 응축기, 기타), 냉매 유형(암모니아, 이산화탄소, 기타), 최종 사용자 산업(식음료 가공, 냉장·물류, 기타), 시스템 유형(셀프 컨테이너형, 원격 응축 유닛, 집중형 랙 시스템, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 냉동 쿨러 시장 동향 및 인사이트

콜드체인 창고 및 라스트마일 냉장 물류의 확대

냉동 쿨러 시장은 아시아, 아프리카, 남미의 일부 지역에서 오랫동안 투자가 부족했던 점을 감안할 때, 온도 관리 인프라 분야의 명확한 설비 투자 주기의 혜택을 누리고 있습니다. Lineage는 2025년 12월 31일 기준으로 미국과 유럽의 그린필드 프로젝트 및 자동화 프로젝트를 모두 아우르며, 추정 총액 10억 9,500만 달러 규모의 83개 자동화 물류센터와 개발 파이프라인을 보고했습니다. 그 후, 2026년 5월, Americold와 EQT는 13억 달러 규모의 북미 냉장 창고 합작 사업을 발표했습니다. 이는 기관 투자자들의 자본이 여전히 수년에 걸친 생산 능력 확대를 뒷받침하고 있음을 보여줍니다. 또한, 자동화 시설에서는 기존 창고보다 더 엄격한 온도 관리가 요구되기 때문에 단순히 설비를 늘리는 것뿐만 아니라 고성능 증발기, 제어 시스템, 모니터링 시스템에 대한 수요가 증가하고 있습니다. 따라서 콜드체인의 확충은 향후 10년 동안 냉동 쿨러 시장에 지속적인 수요원이 될 것으로 보입니다.

HFC의 단계적 감축 기준 강화 및 저GWP 냉매로의 전환

주요 지역의 저 GWP 규제 준수 기한이 강화됨에 따라, 냉동 쿨러 시장 수요가 앞당겨지고 있습니다. 개정된 EU의 F가스 규제 체계에 따라 단계적 감축 일정이 앞당겨졌으며, 40 kW를 초과하는 새로운 중앙 냉동 시스템의 경우 2032년까지 평균 GWP를 150 이하로 유지해야 합니다. 이번 전환은 시스템 전체의 구성에 영향을 미칩니다. 이는 사업자가 HFC 집중형 랙에서 CO₂ 트랜스크리티컬 시스템이나 암모니아 기반 시스템으로 전환할 때, 압축기, 열교환기, 제어 장치, 배관을 교체해야 하는 경우가 많기 때문입니다. 독일 식품 소매 업계에서는 2026년 초, 에너지 효율화 투자액의 60%를 냉장 기술에 할당한 사실이, 규제 준수 압력이 설비 투자의 우선순위를 얼마나 좌우하고 있는지를 보여주었습니다. 미국에서는 EPA가 2026년 5월 AIM법의 특정 일정을 개정하여 일부 식료품점용 설비의 기한을 2032년까지 연장했으나, 대형 소매업체들은 이미 이산화탄소(CO2) 기준에 따른 신규 건설을 결정한 상태이며, 이는 냉장 진열장 시장 수요가 이미 정책상 최소 요건을 상회하고 있음을 보여줍니다.

규제 대응 시스템에 따른 높은 개조 비용과 초기 비용 부담

냉장 진열장 시장에서는 사업자들이 HFC 집중형 시스템에서 CO₂ 트랜스크리티컬 방식 또는 암모니아 기반 시스템으로 전환할 때 여전히 뚜렷한 초기 비용 장벽에 직면하고 있습니다. 댄포스(Danfoss)에 따르면, 트랜스크리티컬 CO₂ 부스터 시스템의 초기 비용은 동등한 HFC 랙 시스템에 비해 일반적으로 15-25% 더 높으며, 효율 향상을 위한 추가 하드웨어가 필요한 따뜻한 기후에서는 그 차이가 더욱 커집니다. 이러한 부담은 소규모 식품 소매업체에게 특히 큰 부담이 됩니다. 독일 EHI 소매 연구소의 기록에 따르면, 2025년 투자액은 평방미터당 961유로(1,040달러)이었으며, 제출된 초안에서는 2025년 환율을 적용하여 평방미터당 1,057달러로 환산되어 있습니다. 일본 환경성은 최대 5억 엔(346만 달러)의 보조금을 제공하고 있으며, 제출된 초안에서는 IRS의 2024년 연평균 환율인 1달러=151.98엔(1.06달러)를 적용해 330만 달러로 환산되었으나, 보조금의 적용 범위는 여전히 모든 사업자를 포괄하고 있지는 않습니다. 이 때문에 냉장 냉각기 시장은 양극화된 양상을 보이고 있으며, 대형 체인점이나 물류 사업자들은 일찍부터 움직이기 시작한 반면, 소규모 사업자들은 여전히 교체 결정을 미루고 있습니다.

부문별 분석

2025년, 증발기와 공랭식 냉각기는 냉동 쿨러 시장의 36.24%를 차지하며, 제품 유형 중 가장 높은 점유율을 기록했습니다. 이 리드는 자립형 진열 케이스부터 중앙 집중식 산업용 냉장실에 이르기까지 모든 시스템 아키텍처에서 널리 사용되고 있음을 반영하고 있습니다. 냉장 산업 분야에서 창고, 슈퍼마켓 또는 제약용 냉장실에서 냉각 설비의 추가나 교체가 이루어질 때마다, 그 입지는 더욱 공고해집니다. 시스템 전체의 업데이트가 연기되더라도, 냉매 전환에는 부품 수준의 업그레이드가 필요한 경우가 많기 때문에 압축기, 응축기, 부속품이 여전히 잔여 수요의 대부분을 차지하고 있습니다.

자기 냉각 모듈은 2031년까지 연평균 성장률(CAGR) 6.81%를 나타낼 것으로 예측되며, 냉장 진열장 시장에서 가장 빠르게 성장하는 제품 유형이 될 전망입니다. MAGNOTHERM Solutions는 2026년에 REWE 매장에 냉매를 사용하지 않는 진열장 ‘ECLIPSE”의 시범 도입을 시작했습니다. REWE는 10-20대를 도입할 계획이며, 매장 내 초기 테스트 결과, 동급의 R290 냉장고와 비교해 에너지 소비량을 15% 절감하면서도 상품 온도를 목표 범위 내로 유지할 수 있는 것으로 확인되었습니다. 이 부문은 절대 수치로 볼 때 여전히 규모가 작지만, 냉장 진열장 시장에서는 고효율 상업용 사례에 적용할 수 있는 신뢰할 수 있는 장기적 대안으로서 솔리드 스테이트 냉각 기술이 주목받기 시작하고 있습니다.

2025년 냉장 냉각기 시장에서 암모니아는 29.11%라는 최대 점유율을 유지했습니다. 이는 산업용 냉동 창고, 식품 가공, 지역 냉방 분야에서 암모니아가 차지하는 확고한 역할을 반영한 것입니다. 대부분의 NH3 시스템은 가혹한 조건에서 20-40년간 가동되도록 설계되어 있기 때문에 도입 대수는 안정적인 임베디드니다. LU-VE는 재순환 비율이 1.8인 저충전량의 새로운 암모니아 유닛 쿨러를 발표했습니다. 이는 공급업체가 완전한 교체를 강요하는 것이 아니라, 암모니아 시스템의 가동 범위를 확대하고 있음을 보여줍니다. HFC와 HFO의 혼합은 예산 제약이 있는 사업자들 사이에서 여전히 일정한 위치를 차지하고 있지만, 단계적 감축이 진행됨에 따라 냉동 쿨러 시장에서의 그 위상은 계속해서 하락하고 있습니다.

이산화탄소(CO2)는 2031년 연평균 성장률(CAGR)이 6.95%로, 가장 빠르게 성장하고 있는 냉임베디드니다. 유럽의 트랜스크리티컬 CO₂ 시스템 도입 건수는 2025년에 11만 1,650곳에 달했으며, 유럽 식품 소매 업계에서의 보급률은 점포 수의 34%까지 상승했습니다. 북미에서는 2025년에 식품 소매점 및 산업 시설이 6,360곳에 달하며 전년 대비 28%의 성장률을 기록했습니다. 또한 ALDI 미국, 코스트코, 크로거, 로블로, 대상 등 대형 체인점들은 이미 신규 건설에 CO2를 도입하기로 결정했습니다. 코플랜드사가 2025년 12월에 다이내믹 베이퍼 인젝션 기능을 갖춘 초임계 CO2 스크롤 압축기를 출시한 것은 냉동 쿨러 시장에서 이러한 전환이 더 이상 단순한 규제 대응에 그치지 않고, 부품 및 서비스 모델에 걸친 광범위한 플랫폼의 변혁으로 인식되고 있음을 보여줍니다.

지역별 분석

2025년, 아시아태평양은 냉동 쿨러 시장의 43.33%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.88%로 성장할 것으로 전망됩니다. 해당 지역의 냉동 쿨러 시장 지위는 냉장 창고 건설 확대, 조직적인 소매업의 확장, 정책에 뒷받침된 냉매 전환이 모두 동시에 진행되고 있음에 따라 형성되고 있습니다. 일본에서는 2025년 기준으로 트랜스크리티컬 CO₂ 시스템을 도입한 식품 소매점이 1만 4,350개 점포에 달하며, 편의점 및 슈퍼마켓에서의 보급률은 2024년 16%에서 18%로 상승했습니다. 2025년 7월, 이온은 2040년까지 국내 모든 매장의 냉장 설비를 천연 냉매로 전환하겠다는 목표를 세웠습니다. 일본 콜드체인 분야에서 불소계 냉매 대체를 위한 보조금 제도와 롯데 월드 로지스틱스가 2026년 5월에 베트남의 동나이 콜드체인 센터를 완공했다는 사실은 공공 지원과 민간 물류 투자 모두가 여전히 해당 지역 수요를 확대시키고 있음을 보여줍니다.

유럽은 냉동 쿨러 시장에서 성숙기에 접어들었음에도 여전히 매우 활발한 지역으로, 이미 10만 6,000개의 식품 소매점이 CO₂ 랙 방식 또는 응축 유닛 방식 시스템을 도입하고 있으며, EU 전체의 보급률은 34%에 달할 전망입니다. 또한, 랙식 설치 건수는 2024년 7만 6,200곳에서 2025년에는 8만 8,000곳으로 증가했습니다. METRO의 전 세계 자연 냉매 보급률은 59%에 달하며, EU 내 매장의 73%에서는 이미 자연 냉매가 도입되어 있고, 2026년에는 40건의 추가 프로젝트가 계획되어 있습니다. 독일에서는 식품 소매 업계가 에너지 효율화 투자액의 60%를 냉장 설비에 할당하고 있다는 점이 두드러지며, 이 설비 부문이 매장 현대화의 핵심으로 자리 잡고 있습니다. 제곱미터당 전력 소비량은 2018년 317kWh에서 2025년에는 289kWh로 감소했으나, 그럼에도 불구하고 냉장 설비는 식품 소매 산업의 총 전력 소비량의 52%를 차지하고 있으며, 이는 냉장 시장에서 현대화가 여전히 활발하게 진행되고 있는 이유를 뒷받침하고 있습니다.

북미에서는 지역별로 서로 다른 속도로 발전하고 있으며, 이 지역의 냉장 진열장 시장은 일부 카테고리에 대한 연방 정부의 기한 연장보다는 오히려 소매업체의 전략에 의해 형성되고 있습니다. EPA(미국 환경보호청)가 2026년 5월에 시행한 AIM법 개정으로 인해 특정 식품점용 설비의 기한이 2032년까지 연장되었으나, 대형 소매업체들의 자발적인 노력에 힘입어 신규 점포용 우선 플랫폼으로서 CO₂ 트랜스크리티컬 방식이 계속해서 지지를 받고 있습니다. 아메리콜드의 포트세인트존 프로젝트와 아메리콜드 및 EQT의 합작 사업은 해당 지역 전체의 냉장 인프라에 대한 투자가 계속해서 견조한 추세를 보이고 있음을 보여줍니다. 남미 시장은 여전히 규모는 작지만 꾸준히 성장하고 있으며, 5개국에 걸쳐 사업을 전개하고 있는 센코스드사의 행보는 자연 냉매 모델의 보급이 확대되고 있음을 보여줍니다. 또한 중동 및 아프리카에서는 일부 저개발 시장에서 전력망의 신뢰성이 여전히 실질적인 제약 요인으로 작용하고 있지만, 식량 안보를 원동력으로 한 잠재적인 성장 기회는 계속해서 존재하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the refrigeration coolers market size is projected to expand from USD 4.41 billion in 2025 and USD 4.71 billion in 2026 to USD 6.52 billion by 2031, registering a CAGR of 6.74% between 2026 and 2031.

This report is Segmented by Product Type (Evaporators and Air Coolers, Condensers, and More), Refrigerant Type (Ammonia, Carbon Dioxide, and More), End-User Industry (Food and Beverage Processing, Cold-Storage and Logistics, and More), System Type (Self-Contained, Remote Condensing Units, Centralized Rack Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Refrigeration Coolers Market Trends and Insights

Expansion Of Cold-Chain Warehousing And Last-Mile Cold Logistics

The refrigeration coolers market is benefiting from a clear capital-spending cycle in temperature-controlled infrastructure, following years of underinvestment across parts of Asia, Africa, and South America. Lineage reported 83 automated warehouses and a development pipeline with an estimated total cost of USD 1.095 billion on December 31, 2025, covering both greenfield and automated projects in the United States and Europe. Americold and EQT then announced a USD 1.3 billion North American cold-storage joint venture in May 2026, which showed that institutional capital was still backing multi-year capacity growth. Automated sites also require tighter temperature consistency than conventional warehouses, which lifts demand for higher-specification evaporators, controls, and monitoring layers rather than just more equipment. This makes cold-chain build-out a durable demand source for the refrigeration coolers market through the rest of the decade.

Tightening HFC Phase-Down And Low-GWP Refrigerant Migration

Tighter low-GWP compliance deadlines in major regions are also pulling forward the refrigeration coolers market. The revised EU F-Gas framework has accelerated phase-down timelines and is pushing new centralized refrigeration systems above 40 kW toward an average GWP below 150 by 2032. That shift affects full system architecture because compressors, heat exchangers, controls, and piping often need replacement when operators move from HFC centralized racks to CO2 transcritical or ammonia-based systems. Germany's food retail sector directed 60% of its energy efficiency investment to refrigeration technology in early 2026, demonstrating how compliance pressure is shaping capex priorities. In the United States, the EPA revised certain AIM Act timelines in May 2026 and extended some grocery equipment deadlines to 2032, but large retailers were already moving ahead with CO2-based new-build decisions, indicating that market demand in the refrigeration cooler market is now running ahead of minimum policy requirements.

High Retrofit And First-Cost Burden For Compliant Systems

The refrigeration coolers market still faces a clear first-cost barrier when operators move from HFC centralized systems to CO2 transcritical or ammonia-based architectures. Danfoss noted that a transcritical CO2 booster system typically costs 15-25% more upfront than a comparable HFC rack, and the gap widens further in warm climates that require extra efficiency-support hardware. That burden is especially hard on smaller food retail operators, where Germany's EHI Retail Institute recorded investment rates of EUR 961 (USD 1,040) per square meter in 2025, which the supplied draft converted to USD 1,057 per square meter using 2025 exchange rates. Japan's Ministry of Environment offers grants of up to JPY 500 million (USD 3.46 million), which the supplied draft converted to USD 3.3 million using the IRS 2024 yearly average rate of JPY 151.98 (USD 1.06) per USD, but subsidy coverage is still not universal. This leaves the refrigeration cooler market on a two-speed path, with large chains and logistics owners moving earlier, while smaller operators continue to delay replacement decisions.

Other drivers and restraints analyzed in the detailed report include:

- Growth In Retail Food Merchandising And Convenience Formats

- AI-Enabled Monitoring And Predictive Maintenance Adoption

- Shortage Of Technicians Certified For CO2, Ammonia, And Hydrocarbons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Evaporators and air coolers accounted for 36.24% of the refrigeration cooler market in 2025, the largest share among product types. Their lead reflects their widespread use across every system architecture, from self-contained display cases to centralized industrial cold rooms. In the refrigeration coolers industry, that position is reinforced every time a warehouse, supermarket, or pharmaceutical cold room adds or replaces cooling equipment. Compressors, condensers, and accessories still account for much of the remaining demand because refrigerant transitions often require component-level upgrades, even when full-system replacement is delayed.

Magnetic cooling modules are projected to grow at a 6.81% CAGR through 2031, making them the fastest-growing product type in the refrigeration coolers market. MAGNOTHERM Solutions launched a pilot deployment of its ECLIPSE refrigerant-free cabinet in REWE stores in 2026. REWE planned 10-20 installations, and earlier in-store testing showed that the unit used 15% less energy than a comparable R290 cabinet while maintaining product temperature within the target range. The segment remains small in absolute terms, but the refrigeration coolers market is beginning to treat solid-state cooling as a credible long-range option for high-efficiency commercial use cases.

Ammonia retained the largest share at 29.11% of the refrigeration coolers market in 2025, reflecting its entrenched role in industrial cold storage, food processing, and district cooling. That installed base remains stable because many NH3 systems are designed to operate for 20-40 years under heavy-duty conditions. LU-VE reported new low-charge ammonia unit coolers with recirculation ratios as low as 1.8, demonstrating that suppliers are extending the operating range of ammonia systems rather than forcing full replacement. HFC and HFO blends still hold a place among budget-constrained operators, but the phase-down path continues to erode that position in the refrigeration coolers market.

Carbon Dioxide (CO2) is the fastest-growing refrigerant type with a 6.95% CAGR through 2031. European transcritical CO2 installations reached 111,650 sites in 2025, and penetration in European food retail rose to 34% of stores. North America reached 6,360 food retail and industrial sites in 2025 with 28% year-over-year growth, and major chains, including ALDI US, Costco, Kroger, Loblaws, and Target, had already committed to CO2 for new builds. Copeland's December 2025 launch of a transcritical CO2 scroll compressor with dynamic vapor injection showed that the refrigeration coolers market is no longer treating this shift as a narrow compliance response, but as a broader platform change across components and service models.

Complete Report Scope:

- By Product Type

- Evaporators and Air Coolers

- Condensers

- Compressors

- Magnetic Cooling Modules

- Controls and Accessories

- Other Product Types

- By Refrigerant Type

- Ammonia (NH3)

- Carbon Dioxide (CO2)

- HFC/HFO Blends

- Hydrocarbons (R-290, R-600a)

- Other Refrigerant Types

- By End-user Industry

- Food and Beverage Processing

- Cold-Storage and Logistics

- Supermarkets and Hypermarkets

- Pharmaceuticals and Life-Sciences

- Data Centres and Electronics Cooling

- Other End-user Industries

- By System Type

- Self-Contained (Plug-in)

- Remote Condensing Units

- Centralised Rack Systems

- Hybrid / Transcritical CO2 Systems

- Other System Types

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific accounted for 43.33% of the refrigeration coolers market in 2025 and is projected to grow at a 6.88% CAGR through 2031. The region's position in the refrigeration coolers market is being shaped by cold-storage build-out, organized retail expansion, and policy-backed refrigerant transitions, all occurring simultaneously. Japan had 14,350 food retail stores using transcritical CO2 systems in 2025, and penetration in convenience stores and supermarkets rose to 18% from 16% in 2024. In July 2025, AEON said it aims to shift all domestic store refrigeration equipment to natural refrigerants by 2040. Japan's cold-chain de-fluorination subsidy and Lotte Global Logistics' May 2026 completion of its Dong Nai Cold Chain Center in Vietnam show that both public support and private logistics investment are still expanding regional demand.

Europe is a mature but still very active part of the refrigeration coolers market, with 106,000 food retail outlets already using CO2 rack or condensing-unit systems and EU-wide penetration at 34%, while rack installations rose from 76,200 sites in 2024 to 88,000 in 2025. METRO's global natural refrigerant penetration reached 59%, and 73% of its EU stores were already on natural refrigerants, with 40 more projects planned in 2026. Germany stands out because food retail directed 60% of energy-efficiency investment to refrigeration, keeping this equipment category at the center of store modernization. Electricity use per square meter fell from 317 kWh in 2018 to 289 kWh in 2025, yet refrigeration still accounted for 52% of total food retail electricity use, underscoring why modernization remains active in the refrigeration market.

North America is moving at a differentiated pace, and the refrigeration coolers market there is being shaped more by retailer strategy than by the extended federal timelines in some categories. The EPA's May 2026 AIM Act revision extended certain grocery equipment deadlines to 2032, but voluntary commitments from large retailers continued to support CO2 transcritical as the preferred platform for new stores. Americold's Port Saint John project and the Americold-EQT joint venture point to continued strength in cold-storage infrastructure spending across the region. South America remains smaller but is still advancing, while Cencosud's rollout across 5 countries shows the natural-refrigerant model is spreading, and the Middle East and Africa continue to offer food security-led potential even as grid reliability remains a real constraint in several underdeveloped markets.

- Daikin Industries, Ltd.

- Rivacold S.r.l.

- Danfoss A/S

- Johnson Controls International plc

- Modine Manufacturing Company

- GEA Group Aktiengesellschaft

- Hillphoenix, Inc.

- BITZER Kuhlmaschinenbau GmbH

- Guntner GmbH & Co. KG

- EVAPCO, Inc.

- Baltimore Aircoil Company, Inc.

- LU-VE S.p.A.

- Mayekawa Mfg. Co., Ltd.

- Hussmann Corporation

- Panasonic Holdings Corporation

- Frascold S.p.A.

- Advansor A/S

- Arctic Industries, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Cold-Chain Warehousing and Last-Mile Cold Logistics

- 4.2.2 Tightening HFC Phase-Down and Low-GWP Refrigerant Migration

- 4.2.3 Growth in Retail Food Merchandising and Convenience Formats

- 4.2.4 AI-Enabled Monitoring and Predictive Maintenance Adoption

- 4.2.5 Higher R290 Charge Limits Enabling Larger Plug-In Cabinets

- 4.2.6 Public Funding and Retail Rollouts Accelerating CO2 Refrigeration Adoption

- 4.3 Market Restraints

- 4.3.1 High Retrofit and First-Cost Burden for Compliant Systems

- 4.3.2 Shortage of Technicians Certified for CO2, Ammonia, and Hydrocarbons

- 4.3.3 Patchy Building Code Adoption for Larger Hydrocarbon Charges

- 4.3.4 Grid Instability in Emerging Cold Chains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Evaporators and Air Coolers

- 5.1.2 Condensers

- 5.1.3 Compressors

- 5.1.4 Magnetic Cooling Modules

- 5.1.5 Controls and Accessories

- 5.1.6 Other Product Types

- 5.2 By Refrigerant Type

- 5.2.1 Ammonia (NH3)

- 5.2.2 Carbon Dioxide (CO2)

- 5.2.3 HFC/HFO Blends

- 5.2.4 Hydrocarbons (R-290, R-600a)

- 5.2.5 Other Refrigerant Types

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage Processing

- 5.3.2 Cold-Storage and Logistics

- 5.3.3 Supermarkets and Hypermarkets

- 5.3.4 Pharmaceuticals and Life-Sciences

- 5.3.5 Data Centres and Electronics Cooling

- 5.3.6 Other End-user Industries

- 5.4 By System Type

- 5.4.1 Self-Contained (Plug-in)

- 5.4.2 Remote Condensing Units

- 5.4.3 Centralised Rack Systems

- 5.4.4 Hybrid / Transcritical CO2 Systems

- 5.4.5 Other System Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Rivacold S.r.l.

- 6.4.3 Danfoss A/S

- 6.4.4 Johnson Controls International plc

- 6.4.5 Modine Manufacturing Company

- 6.4.6 GEA Group Aktiengesellschaft

- 6.4.7 Hillphoenix, Inc.

- 6.4.8 BITZER Kuhlmaschinenbau GmbH

- 6.4.9 Guntner GmbH & Co. KG

- 6.4.10 EVAPCO, Inc.

- 6.4.11 Baltimore Aircoil Company, Inc.

- 6.4.12 LU-VE S.p.A.

- 6.4.13 Mayekawa Mfg. Co., Ltd.

- 6.4.14 Hussmann Corporation

- 6.4.15 Panasonic Holdings Corporation

- 6.4.16 Frascold S.p.A.

- 6.4.17 Advansor A/S

- 6.4.18 Arctic Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment