|

시장보고서

상품코드

2072592

자기 주권 신원(SSI) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Self-Sovereign Identity (SSI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

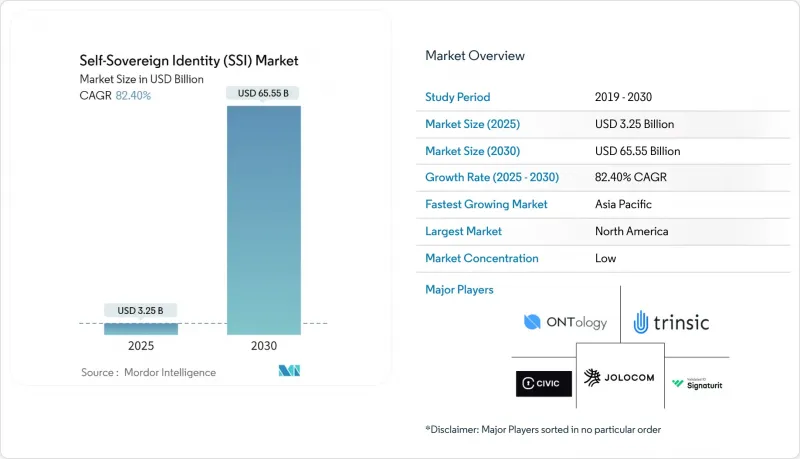

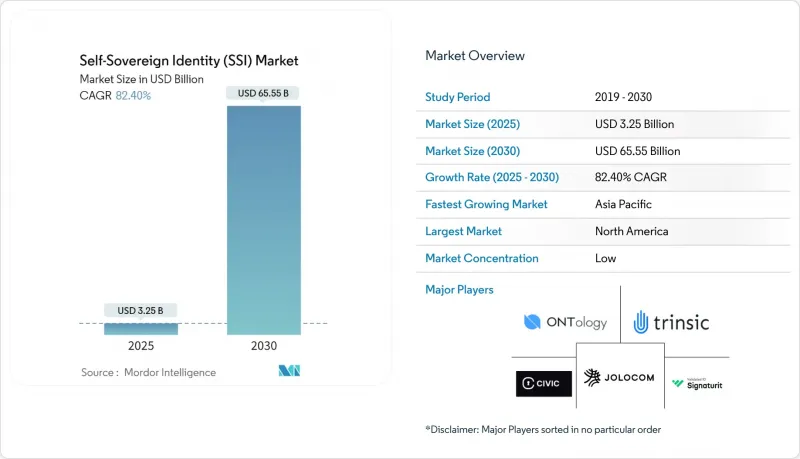

Mordor Intelligence에 의하면, 자기 주권 신원(SSI) 시장 규모는 2025년에 32억 5,000만 달러로 평가되었고, 2030년까지 655억 5,000만 달러까지 확대될 것으로 예측되며, CAGR은 82.40%라고 하는 경이적인 성장을 나타낼 전망입니다.

본 보고서는 제공 분야별(플랫폼 및 소프트웨어, 서비스), ID 유형별(개인 ID, 조직 ID 등), 용도별(인증 및 접근 관리, 결제 및 금융 서비스 등), 최종 사용자 산업별(정부 및 공공 부문, 의료 및 생명과학 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자기 주권 신원(SSI) 시장 동향 및 인사이트

정부 기관에서 분산형 디지털 ID에 대한 수요가 증가하고 있습니다.

개인정보 보호 규제가 강화되고 서비스 제공 비용에 대한 압박이 커지는 가운데, 국가 및 주 정부 기관들은 SSI 시범 사업을 본격적인 운영 단계로 확대되고 있습니다. 미국의 연방 정부 현대화 프로그램은 NIST 800-63-4를 기반으로 한 아키텍처를 채택하고 있으며, 이를 통해 각 기관이 중앙 집중식 데이터 사일로에 의존하지 않고도 높은 보증 수준의 인증 정보를 발급할 수 있도록 하고 있습니다. 이와 더불어, eIDAS 2.0은 모든 EU 회원국에 2026년까지 상호 운용 가능한 디지털 지갑을 배포할 것을 의무화하고 있으며, 시민들에게 국경을 초월한 서비스를 이용하기 위한 단일 인증 정보를 제공합니다. 일본의 마이넘버 카드는 현재 Apple Wallet에 직접 등록할 수 있게 되었으며, 이는 기존의 ID 체계가 규제 기준을 충족하면서도 시민이 관리하는 저장 공간으로 전환될 수 있음을 보여줍니다. 정부의 도입은 민간 부문의 보급을 위한 임계 질량을 확보하고, 핀테크 기업, 항공사, 의료 서비스 제공업체를 끌어들이는 네트워크 효과를 촉진할 것입니다. 점점 더 많은 관할 구역이 지갑 도입 기한을 정함에 따라, SSI는 실험적인 기술에서 표준적인 신원 확인 인프라로 전환되고 있습니다.

SSI와 각국의 전자 신분증 및 여행 인증 프로그램 간의 통합

국제항공운송협회(IATA)의 디지털 여행 인증 정보 이니셔티브는 여권을 사용자의 디지털 지갑에 저장함으로써 몇 초 만에 서류 확인이 가능하게 하여 공항의 혼잡을 완화하고 있습니다. 유럽의 디지털 ID 지갑은 쉔겐 지역 전역에서 사용될 수 있도록 구축되어 있어, 시민들은 동일한 인증 정보를 사용하여 독일에서 은행 계좌를 개설하거나, 프랑스에서 의료 서비스를 받거나, 지역 전역에서 항공기에 탑승할 수 있게 됩니다. 미국 교통안전청(TSA)이 실시한 모바일 운전면허증 시범 운영은 국내 신분증이 국제 항공 요건을 충족할 수 있음을 보여주며, 탑승 수속부터 탑승구까지 원활한 경험을 위한 길을 열어주고 있습니다. 국제민간항공기구(ICAO) 등 국제 표준화 기구가 제시한 상호운용성 요건이 현재 지갑의 사양을 형성하고 있으며, 국경 관리 기관 간의 표준 조화를 가속화하고 있습니다.

W3C의 VC/DID를 뛰어넘는 정의되지 않은 세계의 상호운용성 표준

W3C는 2024년에 'Verifiable Credential Data Model 2.0'을 최종 확정했으나, 만료 처리, 크로스체인 증명 및 신뢰 프레임워크 탐색에 관한 사양은 아직 완성되지 않았습니다. 각 벤더사는 독자적인 확장 기능을 통해 그 격차를 메우고 있지만, 그 결과 SSI가 내세우는 '보편적인 휴대성'라는 비전을 저해하는 사일로화가 발생하고 있습니다. 락인 현상을 우려하는 기업들은 추가 표준이 안정화될 때까지 여러 공급업체를 통한 도입을 미루고 있습니다. 또한, 통합 업체가 호환되지 않는 스택 간에 브리지를 구축해야 하기 때문에 분할 현상은 구현 비용 증가로 이어집니다. Decentralized Identity Foundation은 보충 지침을 작성 중이지만, 합의 도출이 지연됨에 따라 기업의 조달 주기가 예측 기간을 초과하여 지연될 위험이 있습니다.

부문별 분석

2024년, 플랫폼 및 소프트웨어 제품은 자기 주권 신원(SSI) 시장의 61.43% 점유율을 차지했으며, 이는 얼리 어답터들이 핵심 인프라를 우선시했음을 입증했습니다. 그러나 서비스 분야는 연평균 성장률(CAGR) 83.14%를 나타낼 것으로 전망됩니다. 이는 기업이 복잡하고 여러 관할 구역에 걸쳐 있는 네트워크 전반에서 지갑을 운영하기 위해 통합, 맞춤화, 거버넌스에 관한 전문 지식이 필요하기 때문입니다. 서비스 계층에는 인증 정보 발급 오케스트레이션, 제로 지식 증명 설정, 지속적인 규정 준수 감사 등이 포함되어 있으며, 이를 통해 일회성 라이선스 비용을 상회하는 지속적인 수익원이 창출됩니다. Dock Labs와 cheqd의 제휴와 같은 협력 관계는 제품 스택과 컨설팅의 전문성을 결합하여 대규모 확장을 가속화하고 있습니다. 규제가 엄격한 분야에서 SSI 도입이 확대됨에 따라, 시스템 통합사업자, 사이버 보안 기업, 전문 자문 회사 등 전문 서비스의 제공 범위가 넓어지고 있습니다.

서비스로의 전환에 따라 조달 주기 내의 예산 배분이 변화하고 있습니다. 의사결정권자들은 벤더에 대한 보상을 온보딩 비용 절감이나 부정행위로 인한 손실 방지와 연계하는 성과 기반 계약을 점점 더 선호하고 있습니다. 클라우드 네이티브 제공 모델을 통해 업그레이드가 원활하게 이루어지기 때문에 매니지드 서비스 공급업체는 규제 변화에 발맞추어 지속적인 규정 준수 추적을 입증해야 합니다. 그 결과, 플랫폼 부문의 가격 경쟁은 치열해지는 반면, 서비스의 이익률은 견조하게 유지되고 있습니다. 이러한 추세로 인해 소프트웨어가 일반화되더라도 컨설팅 중심의 서비스 제공업체는 지속적인 수익성을 유지할 수 있습니다.

2024년에는 개인의 정체성과 관련된 활용 사례가 상업적 기반을 확립했습니다. 이는 대부분의 지갑 프로그램이 일반 시민이나 소매 금융 고객을 대상으로 하고 있기 때문입니다. 개인 인증 정보 분야의 자기 주권 신원 확인 시장 규모는 향후 기업 및 기기 분야로의 확장을 뒷받침하는 기반이 되고 있습니다. IoT 및 기기 식별 관련 용도는 커넥티드카 보안, 스마트 그리드 관리, 산업용 센서 인증에 힘입어 2030년까지 연평균 성장률(CAGR) 82.87%를 나타낼 것으로 전망됩니다. 자동차 제조업체들은 현재 소유자의 개인정보를 보호하는 동시에, 무선(OTA) 업데이트를 승인할 수 있는 검증 가능한 기기 인증 정보를 탑재하고 있습니다. 스마트 미터, 라우터, 드론 제조업체들도 마찬가지로, 인증 기관(CA)에 의한 단일 장애 지점을 제거하기 위해 분산형 온보딩을 채택하고 있으며, 이는 기기 ID가 수익 다각화를 촉진한다는 점을 시사합니다.

개인 인증 정보와 기기 인증 정보의 상호 작용을 통해 새로운 경험을 할 수 있게 됩니다. 운전자는 검증 가능한 인증 정보와 연동된 얼굴 인식을 통해 카셰어링 차량에 로그인할 수 있으며, 반면 가족 구성원은 배송 로봇에 대해 기간 한정 접근 권한을 위임할 수 있습니다. 이러한 도메인을 아우르는 워크플로우로 인해, 벤더들은 초기 소비자용 지갑에서는 필요하지 않았던 위임 프로토콜이나 다중 서명 방식을 구축해야 하는 상황에 직면해 있습니다. 그 결과, 아이덴티티 플랫폼의 로드맵에는 자동차, 산업, 소비자용 전자기기 등 각 공급망 전반에 걸친 계층적 키 관리 및 보안 요소의 통합이 점점 더 많이 포함되고 있습니다.

지역별 분석

2024년, 북미는 자기 주권 신원(SSI) 시장 규모의 44.87%를 계속 차지했습니다. 이는 연방 및 주 기관들이 NIST 800-63-4에 기반한 지갑 시범 사업을 도입했기 때문입니다. 교통안전청(TSA)의 모바일 운전면허증 검증 프로그램 등은 공항 보안 검색대를 현대화하는 동시에 국내 지갑 생태계를 활성화시키고 있습니다. 뉴욕과 샌프란시스코의 핀테크 허브에서는 검증 가능한 자격 정보를 네오뱅크의 온보딩 과정에 통합함으로써, 개인 투자자, 긱 경제 플랫폼, 의료 포털 전반에 걸쳐 플랫폼 이용을 촉진하는 선순환을 만들어내고 있습니다. 캐나다의 민관 합동 기구인 '디지털 ID 및 인증 협의회'는 미국의 규격과 부합하는 주를 아우르는 인증 체계를 구축하고 있으며, 멕시코의 핀테크법은 챌린저 뱅크의 전자지갑 도입을 뒷받침하고 있습니다. 스마트폰의 높은 보급률과 개발 인력의 집중이 이 지역의 리더십을 더욱 뒷받침하고 있습니다.

유럽은 2026년까지 모든 회원국이 최소 한 개의 디지털 지갑을 발행하도록 법적 의무를 규정한 'eIDAS 2.0' 덕분에 시장 규모 면에서 2위를 차지할 전망입니다. 독일은 행정 서비스를 위한 블록체인 기반 신원 등록 시스템에 투자하고 있으며, 프랑스는 건강보험증을 시민용 지갑에 통합하고, 영국은 브렉시트 이후 신뢰 프레임워크의 인증을 추진하고 있습니다. 유럽의 블록체인 서비스 인프라는 국경을 초월한 신원 확인을 지원하며, 이를 통해 주민들은 종이 신분증을 다시 제시할 필요 없이 해외에서 은행 계좌를 개설하거나, 부동산 권리증서에 서명하거나, 사회보장 급여를 청구할 수 있게 됩니다. GDPR(EU 개인정보보호규정) 등 EU의 데이터 주권 관련 규범은 서버에 저장되는 개인 데이터를 최소화한 사용자 중심의 지갑을 권장하며, 자기 주권 신원(SSI)의 설계 원칙을 강화하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 82.47%를 기록하며, 해당 지역 내에서 가장 빠른 성장세를 보이고 있습니다. 일본은 마이넘버 카드를 주요 스마트폰 지갑에 통합하고, 개인정보를 보호하는 컨테이너 내에서 소비자에게 연령, 주소, 납세자 번호를 즉시 증명해줌으로써 이 분야를 선도하고 있습니다. 인도는 Aadhaar 인프라 위에 SSI를 중첩하는 방안을 검토 중이며, 신용 평가 및 긱 워커 보험 분야에서 선택적 정보 공개를 통한 증명을 가능하게 하려고 하고 있습니다. 한국에서는 디지털 운전면허증 시범 사업이 주요 은행의 앱과 연동되어 있으며, 호주의 '신뢰할 수 있는 디지털 신원 프레임워크'는 의료 및 교육 분야에서 지갑의 도입을 확대되고 있습니다. 중국은 국가가 관리하는 디지털 신분증에 주력하고 있지만, 홍콩의 시범 구역에서는 핀테크 샌드박스 내에서 국경을 초월한 전자 KYC(e-KYC)를 위한 분산형 인증 시험이 진행되고 있습니다. 지역 컨소시엄은 동남아시아국가연합(ASEAN) 내 국경을 초월한 무역을 지원하기 위한 상호운용성 프로파일을 수립하고 있으며, 이를 통해 도입이 더욱 가속화되고 있습니다.

중동 및 아프리카 및 남미는 새로운 주목받는 지역이 되고 있습니다. 브라질은 2032년까지 블록체인 기반의 시민 신분증을 도입하겠다고 약속했으며, 이를 통해 공공 서비스 이용 절차를 간소화하고 서류 위조를 줄이는 것을 목표로 하고 있습니다. 남아프리카공화국은 스마트 ID 카드를 모바일 인증 정보로 확대하여, 복지 급여 지급을 위한 자기 주권 신원(SSI)의 시범 운영을 진행하고 있습니다. 걸프협력회의(GCC) 회원국들은 외국인 근로자 채용 절차를 효율화하기 위해 블록체인 여권 시범 사업을 진행하고 있습니다. 스마트폰 보급률이 낮고 인터넷 접속 환경이 불안정한 점은 단기적인 걸림돌이 되고 있지만, 4G 및 5G 네트워크에 대한 투자가 증가하고 있는 만큼 단말기 가격이 하락하면 급속한 '도약적 도입'이 진행될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the self-sovereign identity (SSI) market size reached USD 3.25 billion in 2025 and is projected to climb to USD 65.55 billion by 2030, delivering an exceptional 82.40% CAGR.

This report is Segmented by Offering (Platform/Software, and Services), Identity Type (Individual Identity, Organizational Identity, and More), Application (Authentication/Access Management, Payments and Financial Services, and More), End-User Industry (Government and Public Sector, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Self-Sovereign Identity (SSI) Market Trends and Insights

Growing demand for decentralized digital IDs among governments

National and state agencies are scaling SSI pilots into full production as privacy regulation tightens and cost-to-serve pressures mount. The U.S. federal modernization program anchors its architecture on NIST 800-63-4, letting agencies issue high-assurance credentials without central data silos. In parallel, eIDAS 2.0 compels every EU member state to distribute interoperable digital wallets by 2026, providing citizens with one credential for cross-border services. Japan's My Number card now loads directly into Apple Wallet, illustrating how legacy ID schemes can migrate to citizen-controlled storage while meeting regulatory criteria. Government adoption establishes critical mass for private-sector uptake, spurring network effects that attract fintechs, airlines, and healthcare providers. As more jurisdictions declare wallet deadlines, SSI transitions from exploratory technology to default identity infrastructure.

Integration of SSI with national eID and travel credential programs

The International Air Transport Association's Digital Travel Credentials initiative stores passports inside user wallets, permitting document verification in seconds and lowering airport congestion. European Digital Identity wallets are built for Schengen-wide acceptance, enabling citizens to open bank accounts in Germany, receive healthcare in France, and board aircraft across the region using the same credential. Transportation Security Administration pilots of mobile driver's licenses show domestic IDs can fit global aviation requirements, paving the way for frictionless corridor-to-gate experiences. Interoperability mandates from international civil aviation standards bodies now shape wallet specifications, accelerating standard alignment among border agencies.

Undefined global interoperability standards beyond W3C VC/DID

W3C finalized Verifiable Credential Data Model 2.0 in 2024, yet specifications for revocation, cross-chain proofs, and trust-framework discovery remain unfinished. Vendors are filling gaps with proprietary extensions, creating silos that undermine the universal portability vision of SSI. Enterprises wary of lock-in postpone multi-vendor rollout until additional standards stabilize. Fragmentation also increases implementation costs because integrators must build bridges between incompatible stacks. The Decentralized Identity Foundation is drafting supplemental guidance, but slow consensus risks delaying enterprise procurement cycles beyond the forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Rapid rise of Web3 wallets as universal identity managers

- Compliance push from EU eIDAS 2.0 and U.S. NIST 800-63-4

- Reliance on smartphone penetration for credential custody

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform and software products captured 61.43% of the self-sovereign identity market share in 2024, confirming that early adopters prioritized core infrastructure. Services, however, are projected to post an 83.14% CAGR because enterprises now need integration, customization, and governance expertise to operationalize wallets across complex, multi-jurisdiction networks. The services layer includes credential issuance orchestration, zero-knowledge proof configuration, and ongoing compliance audits, yielding recurring revenue streams that outstrip one-time license fees. Alliances such as Dock Labs partnering with cheqd fuse product stacks with consulting depth to accelerate large-scale rollouts. As more regulated sectors adopt SSI, the professional-services pool widens across system integrators, cybersecurity firms, and specialty advisory boutiques.

The shift to services alters budget allocations in procurement cycles. Decision-makers increasingly seek outcome-based contracts that tie vendor remuneration to onboarding-cost reductions or fraud-loss avoidance. Cloud-native delivery models make upgrades seamless, meaning managed services vendors must demonstrate continuous compliance tracking as regulations evolve. Consequently, price competition in the platform tier intensifies while service margins remain resilient. This dynamic supports sustained profitability for consulting-led providers even as software commoditizes.

Individual identity use cases established the commercial baseline in 2024 because most wallet programs target citizens and retail banking clients. The self-sovereign identity market size for individual credentials underpins subsequent extensions into enterprise and device realms. IoT and device identity applications are poised for an 82.87% CAGR to 2030, driven by connected-car security, smart-grid management, and industrial sensor authentication. Automotive manufacturers now embed verifiable device credentials that authorize over-the-air updates while protecting owner privacy. Manufacturers of smart meters, routers, and drones are likewise adopting decentralized onboarding to neutralize certificate-authority single points of failure, signaling that device identity will broaden revenue diversity.

Interplay between personal and device credentials unlocks novel experiences. Drivers can authenticate to shared vehicles with a face scan that resolves to a verifiable credential, while household members delegate limited-time access rights to delivery robots. These cross-domain workflows push vendors to build delegation protocols and multi-signature schemes that were unnecessary in early consumer wallets. In turn, identity-platform roadmaps increasingly include hierarchical key management and secure-element integration across automotive, industrial, and consumer electronics supply chains.

Complete Report Scope:

- By Offering

- Platform / Software

- Services

- By Identity Type

- Individual Identity

- Organizational / Enterprise Identity

- IoT / Device Identity

- By Application

- Authentication / Access Management

- Payments and Financial Services

- Verifiable Credentials and e-KYC

- Supply-Chain and Provenance

- Other Applications

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Healthcare and Life Sciences

- IT and Telecom

- Retail and e-Commerce

- Mobility and Transportation

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America retained 44.87% of the self-sovereign identity market size in 2024 because federal and state agencies embraced wallet pilots under NIST 800-63-4. Programs such as the Transportation Security Administration's mobile driver's license verification modernize airport security checkpoints while feeding domestic wallet ecosystems. Fintech hubs in New York and San Francisco integrate verifiable credentials into neobank onboarding, creating a virtuous loop that drives platform utilization across retail investors, gig-economy platforms, and healthcare portals. Canada's public-private Digital Identity and Authentication Council cultivates cross-province credential frameworks that dovetail with U.S. specifications, and Mexico's fintech law spurs wallet deployment among challenger banks. High smartphone penetration and developer talent density further sustain the region's leadership.

Europe ranks second in value terms thanks to eIDAS 2.0, which establishes a binding obligation for every member state to issue at least one digital wallet by 2026. Germany invests in blockchain-backed identity registries for public-administration services, France integrates health-insurance cards into citizen wallets, and the United Kingdom advances post-Brexit trust-framework certifications. The European Blockchain Services Infrastructure underpins cross-border verification, letting residents open bank accounts, sign property deeds, or claim social benefits abroad without re-presenting paper ID. EU data-sovereignty norms such as GDPR favor user-centric wallets that store minimal personal data on servers, reinforcing SSI design principles.

Asia-Pacific posts the fastest regional trajectory with an 82.47% CAGR. Japan leads with My Number card integration into major smartphone wallets, providing consumers instant proof of age, address, and tax identification within a privacy-preserving container. India explores SSI overlays on its Aadhaar infrastructure to enable selective-disclosure proofs in credit scoring and gig-worker insurance. South Korea's digital-driver-license pilot couples with major bank apps, while Australia's Trusted Digital Identity Framework expands wallet-acceptance in healthcare and education. China focuses on state-controlled digital ID, but pilot zones in Hong Kong test decentralized proofs for cross-border e-KYC within fintech sandboxes. Regional consortiums craft interoperability profiles to support cross-border trade in the Association of Southeast Asian Nations, further intensifying adoption.

The Middle East and Africa, and South America form emerging hot spots. Brazil committed to blockchain-based citizen ID by 2032, aiming to simplify public-service access and reduce document forgery. South Africa expands smart-ID cards into mobile credentials and pilots SSI for welfare disbursement. Gulf Cooperation Council countries experiment with blockchain passports to streamline expatriate labor onboarding. Limited smartphone reach and patchy internet coverage act as near-term brakes, yet rising investment in 4G and 5G networks points toward rapid leapfrog adoption once device costs decline.

- Evernym, Inc.

- Civic Technologies, Inc.

- Validated ID, S.L.

- Trinsic, Inc.

- Jolocom GmbH

- Ontology Foundation Ltd.

- Dock Labs AG

- SelfKey Foundation

- cheqd Ltd.

- Spruce Systems, Inc.

- GATACA Digital Identity Solutions S.L.

- Keyp GmbH

- Veres One Foundation

- Affinidi Pte Ltd.

- Serto Labs, Inc.

- R3 LLC

- uPort by ConsenSys AG

- ID2020 Alliance, Inc.

- Obsidian Systems LLC

- Tykn B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for decentralized digital IDs among governments

- 4.2.2 Integration of SSI with national eID and travel credential programs

- 4.2.3 Rapid rise of Web-3 wallets as universal identity managers

- 4.2.4 Compliance push from EU eIDAS 2.0 and U.S. NIST 800-63-4

- 4.2.5 Gen-AI-driven identity proofing reducing onboarding friction

- 4.2.6 SSI-enabled reusable KYC networks lowering bank onboarding cost

- 4.3 Market Restraints

- 4.3.1 Undefined global interoperability standards beyond W3C VC/DID

- 4.3.2 Reliance on smart-phone penetration for credential custody

- 4.3.3 Token-economics sustainability risks for incentive-based SSI ledgers

- 4.3.4 High liability exposure for issuers under revocation disputes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Platform / Software

- 5.1.2 Services

- 5.2 By Identity Type

- 5.2.1 Individual Identity

- 5.2.2 Organizational / Enterprise Identity

- 5.2.3 IoT / Device Identity

- 5.3 By Application

- 5.3.1 Authentication / Access Management

- 5.3.2 Payments and Financial Services

- 5.3.3 Verifiable Credentials and e-KYC

- 5.3.4 Supply-Chain and Provenance

- 5.3.5 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Government and Public Sector

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 IT and Telecom

- 5.4.5 Retail and e-Commerce

- 5.4.6 Mobility and Transportation

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Evernym, Inc.

- 6.4.2 Civic Technologies, Inc.

- 6.4.3 Validated ID, S.L.

- 6.4.4 Trinsic, Inc.

- 6.4.5 Jolocom GmbH

- 6.4.6 Ontology Foundation Ltd.

- 6.4.7 Dock Labs AG

- 6.4.8 SelfKey Foundation

- 6.4.9 cheqd Ltd.

- 6.4.10 Spruce Systems, Inc.

- 6.4.11 GATACA Digital Identity Solutions S.L.

- 6.4.12 Keyp GmbH

- 6.4.13 Veres One Foundation

- 6.4.14 Affinidi Pte Ltd.

- 6.4.15 Serto Labs, Inc.

- 6.4.16 R3 LLC

- 6.4.17 uPort by ConsenSys AG

- 6.4.18 ID2020 Alliance, Inc.

- 6.4.19 Obsidian Systems LLC

- 6.4.20 Tykn B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment