|

시장보고서

상품코드

2072620

석탄 처리 장비 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Coal Handling Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

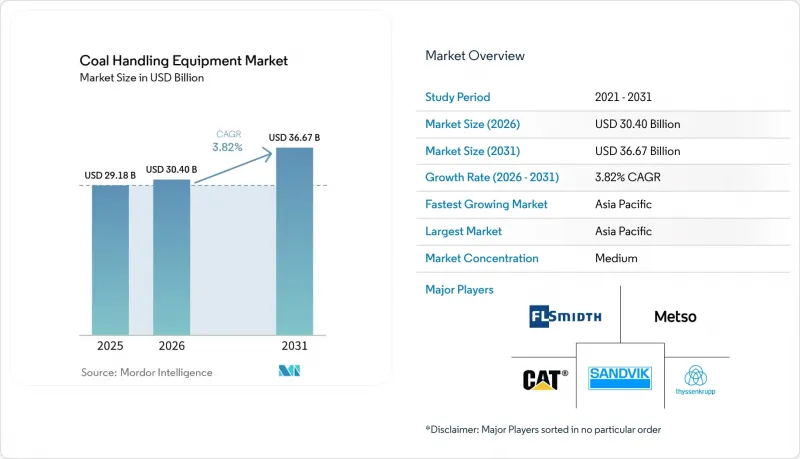

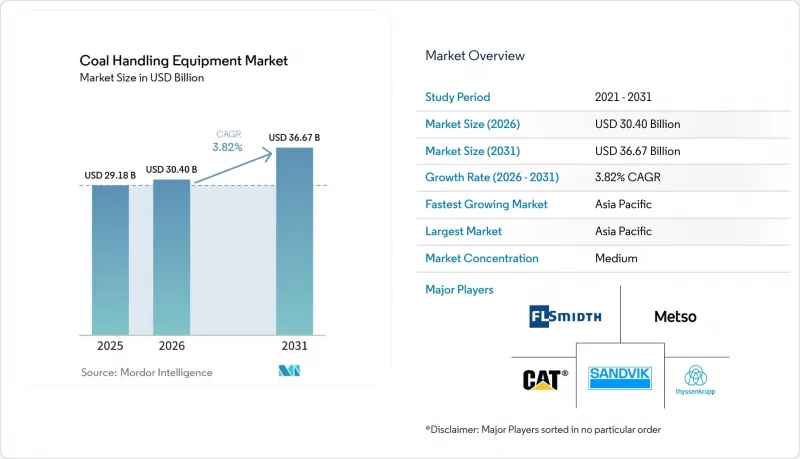

Mordor Intelligence에 의하면, 석탄 처리 장비 시장은 2025년에 291억 8,000만 달러로 평가되었고, 2026년에 304억 달러로 추정되고, 2031년까지 366억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 3.82%로 성장할 전망입니다.

본 보고서는 장비 유형별(컨베이어, 분쇄기, 피더, 스태커 등), 운영 유형별(자재 입고 등), 자동화 수준별(수동, 반자동, 완전 자동), 최종 사용자별(발전, 철강 등), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 석탄 처리 장비 시장 동향 및 인사이트

기존 플랜트의 노후화된 인프라 교체 주기

1990년대에 설치된 많은 컨베이어, 분쇄기, 적재기는 설계 수명을 초과했습니다. 인도의 '102 퍼스트 마일 연결성'이 이니셔티브에서는 소용량 벨트 컨베이어를 시간당 1만 톤 이상을 처리할 수 있는 디지털 감시 시스템으로 교체하는 데 중점을 두고 있습니다. 마틴 엔지니어링사는 작업자들이 손실을 줄이고 실시간 벨트 추적을 실현하기 위해 노력한 결과, 2025년에 벨트 클리너 개조 건수가 급증했다고 보고했습니다. 남아프리카공화국의 리처즈베이 석탄 터미널에서는 철도의 병목 현상을 해소하고 처리 능력을 회복하기 위해 스태커·리클레이머 개보수 작업을 진행하고 있습니다. 이러한 업그레이드 프로젝트는 안정적인 부품 및 서비스 수익을 창출하며, 각 OEM 업체가 지역별 수요 변동에 따른 영향을 완화하는 데 도움이 되고 있습니다.

대용량 컨베이어가 필요한 노천 채굴 석탄 생산량의 급증

노천 채굴은 채굴 비용이 저렴하고, 트럭을 이용한 운반이 필요 없는 초대용량 컨베이어를 도입함으로써 지하 채굴 시장 점유율을 점차 잠식하고 있습니다. 워리어 메트 콜(Warrior Met Cole)사의 블루크릭 제1광산은 10억 달러를 투자해 2025년에 가동을 시작할 예정이며, 셈퍼트랜스(Sempertrans)사의 ST7500 벨트와 BEUMER사의 9마일에 달하는 육상 컨베이어 시스템을 갖추고 있으며, 40년의 광산 수명 동안 연간 600만 쇼트톤의 처리 능력을 보유하고 있습니다. 피바디 에너지(Peabody Energy)사의 센츄리온 광산에서는 1,200만 달러를 투자해 총 길이 2.5킬로미터의 지하 컨베이어를 설치하고, 디젤 트럭을 이용한 운반을 대체함으로써 연료비와 배기가스를 줄였습니다. 인도네시아의 PT 부킷 아삼사는 탄중 에님에 시간당 3,000톤의 처리 능력을 갖춘 열차 적재 스테이션 2곳을 설치했습니다. 여기에는 13킬로미터와 17킬로미터 길이의 컨베이어가 연계되어 있어, 연간 2,000만 톤의 처리 능력을 갖추고 있습니다. 이러한 추세는 시간당 5,000톤 이상을 처리하는 시스템으로 정의되는 대용량 컨베이어가 신규 노천 채굴 광산에서 표준으로 자리 잡고 있음을 보여줍니다. 이러한 변화로 인해 기어리스 구동 장치, 첨단 벨트 소재, 실시간 장력 모니터링 시스템에 대한 수요가 증가하는 한편, 기존의 트럭과 굴삭기를 이용한 물류 방식은 점차 대체되고 있습니다.

유럽 및 북미의 석탄 단계적 폐지 정책 가속화

유럽과 북미에서는 2025-2026년 15-20기가와트의 발전 용량이 폐지될 전망이며, 영국은 석탄 화력 발전에서 완전히 철수할 예정이고, 독일도 여러 발전 단위를 폐쇄할 계획입니다. 이로 인해 신규 프로젝트 수요와 장기적인 부품 매출을 모두 잃게 될 것입니다. 각 OEM 기업들은 미결제 수주를 확보하기 위해 판매 전략을 아시아로 전환하고, 바이오매스 처리 분야로의 사업 확장을 추진하고 있습니다.

부문별 분석

2025년, 컨베이어는 석탄 처리 장비 시장의 48.2%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 4.5%로 성장할 것으로 전망됩니다. 이 부문은 광산 및 항만에서의 컨베이어 통합 프로젝트 시장 규모가 2025년에 140억 달러를 넘어섬에 따라 성장을 이룩했습니다. 티센크루프가 제공하는 마찰을 최대 80%까지 줄여주는 레일 주행식 컨베이어 등, 초장거리 육상 컨베이어 설계 분야의 혁신을 통해 운송 비용이 절감되면서 아시아의 광산 기업들 사이에서 주목을 받고 있습니다.

또한, 설비 교체 노력도 컨베이어 수요를 견인하고 있습니다. 인도의 '퍼스트 마일 연결성' 계획의 업그레이드에는 트럭 덤프를 대용량 컨베이어 벨트로 교체하는 102건의 프로젝트가 포함되어 있습니다. 또한, BEUMER사의 새로운 타이창 공장은 장거리 시스템의 지역 생산을 지원함으로써 아시아태평양 고객에 대한 납기 기간을 단축하고 있습니다. 분쇄기, 스태커, 피더가 합쳐서 나머지 시장 점유율을 차지하고 있습니다. 분쇄기의 경우, 6mm 미만의 원료를 필요로 하는 석탄 화학 플랜트에서 수요가 증가하고 있습니다. 스태커와 리클레이머는 맥더피 등의 수출 터미널에서 투자를 유치하고 있으며, 해당 지역에서는 2억 달러 규모의 현대화 프로젝트를 통해 야금용 석탄의 적재 효율이 향상되고 있습니다.

2025년 기준으로, 자재관리 부문은 석탄 취급 설비 시장 점유율의 48.2%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 4.5%를 나타낼 것으로 예측됩니다. 탄광, 선탄장, 저장장, 항만을 연결하는 연속 벨트 컨베이어는 장기적인 서비스 수익에 기여하고 있으며, 이 부문 가치의 거의 절반을 차지하고 있습니다.

수취 및 파쇄 공정은 여전히 중요하지만, 점점 더 일반화되고 있습니다. 인도네시아의 철도 연계 허브에서는 화물차 티플러와 전동 에이프런 피더가 도입되어 있는 반면, 인도의 중앙 집중형 수취 시설에서는 차하 배출 시스템과 대용량 댐퍼가 중시되고 있습니다. 리처즈베이에서 러시아 극동의 터미널에 이르기까지, 항만 내 저장 및 회수 설비의 현대화에는 새로운 스태커·리클레이머가 필요하지만, 예산 제약으로 인해 완전 자동화의 범위가 제한되는 경우가 종종 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 45.0%를 차지했으며, 중국, 인도, 인도네시아의 발전용 및 산업용 석탄 수요 증가에 힘입어 2031년까지 연평균 성장률(CAGR) 4.8%를 나타낼 것으로 예측됩니다. '퍼스트 마일 연결성'이 구상과 관련된 석탄 처리 장비 시장 규모는 2030년까지 37억 달러를 넘어설 것으로 예측됩니다. 또한, 중국석유화학(Sinopec)의 내몽골 올레핀 프로젝트로 인해 중국 내 미세 분탄 선별 라인에 대한 수요가 증가하고 있습니다. 타이창, 푸네 또는 자카르타에 시설을 갖춘 OEM(주문자 상표 제조업체)은 운송비와 관세 절감이라는 이점을 누리고 있으며, 국영 기업의 입찰에서 경쟁 우위를 점하고 있습니다.

북미에서는 2025년에 석탄 생산량이 4% 증가하여 5억 2,750만 쇼트톤에 달했습니다. 이는 주로 이상 기후로 인한 겨울철 수요 증가가 원인입니다. 그러나 투자는 여전히 확장에 비해 유지 관리에 중점을 두고 있습니다. 주목할 만한 프로젝트로는 앨라배마주의 맥더피 석탄 터미널 현대화 사업과, 노퍽 서던사가 2억 달러를 투자하는 '3B 복도' 등이 있습니다. 이는 수출 수익성이 좋은 분야에 자본 지출을 중점적으로 배분하는 것입니다.

유럽에서는 석탄 화력 발전소의 급속한 폐쇄로 인해 석탄 수요가 계속 감소하고 있습니다. 그러나 폴란드에서 펠릿 혼합 연료로 전환하는 등 바이오매스 대응을 위한 개조에는 변화하는 에너지 수요에 부응할 기회가 존재합니다.

남아프리카, 러시아, 그리고 일부 남미 항구도 더 많은 기회가 있는 지역입니다. 남아프리카공화국의 리처즈베이 항구는 2025년에 5,766만 톤을 수출했으며, 처리 능력을 강화하기 위해 스태커·리클레이머에 투자하고 있습니다. 러시아에서는 바니노 항과 보스토치니 항의 확장으로 인해 연간 처리량이 합계 2,000만 톤 이상 증가할 것으로 예상에 따라, 새로운 선박 적재기 및 야드 설비가 필요하게 되었습니다. 중동은 발전이 천연가스에 의존하고 있기 때문에 석탄 취급 설비 시장으로는 여전히 극히 소규모에 그치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the coal handling equipment market is projected to reach USD 29.18 billion in 2025, USD 30.40 billion in 2026, and USD 36.67 billion by 2031, growing at a CAGR of 3.82% from 2026 to 2031.

This report is Segmented by Equipment Type (Conveyors, Crushers, Feeders, Stackers, and More), Operation Type (Material Receiving, and More), Automation Level (Manual, Semi-Automated, Fully Automated), End-User (Power Generation, Steel and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Coal Handling Equipment Market Trends and Insights

Aging infrastructure upgrade cycle across existing plants

Many conveyors, crushers, and stackers installed in the 1990s have exceeded their design life. India's 102 First Mile Connectivity initiatives focus on replacing low-capacity belts with digitally monitored systems capable of handling over 10,000 tons per hour. Martin Engineering reported a surge in belt-cleaner retrofits in 2025 as operators aimed to reduce spillage and implement real-time belt tracking. South Africa's Richards Bay Coal Terminal is refurbishing stacker-reclaimers to address rail bottlenecks and restore throughput. These upgrade projects provide consistent parts and service revenue, helping OEMs mitigate the impact of regional demand fluctuations.

Surge in surface-mined coal output requiring high-capacity conveyors

Surface mining is gaining market share from underground operations due to lower extraction costs and the use of ultra-high-capacity conveyors that eliminate the need for truck haulage. Warrior Met Coal's Blue Creek No.1 mine, commissioned in 2025 with a USD 1 billion investment, features a Sempertrans ST7500 belt and a BEUMER 9-mile overland conveyor system capable of handling 6 million short tons annually over a 40-year mine life. Peabody Energy's Centurion Mine allocated USD 12 million to a 2.5-kilometer underground conveyor, replacing diesel truck haulage to reduce fuel costs and emissions. Indonesia's PT Bukit Asam installed two 3,000-tonne-per-hour train loading stations at Tanjung Enim, supported by 13-kilometer and 17-kilometer conveyors, enabling a throughput of 20 million tonnes per year. These developments indicate that high-capacity conveyors, defined as systems handling over 5,000 tonnes per hour, are becoming the standard for new surface mines. This shift is driving demand for gearless drives, advanced belt materials, and real-time tension monitoring systems, while displacing traditional truck-and-shovel logistics.

Accelerated coal phase-out policies in Europe & North America

Europe and North America are expected to shut down 15-20 GW of capacity during 2025-2026, with the U.K. finalizing its exit and Germany closing several blocks. This will eliminate both greenfield demand and long-tail parts revenue. OEMs are redirecting their sales efforts toward Asia and expanding into biomass handling to safeguard their backlogs.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of automation & digital twins for OPEX reduction

- Hybrid renewable-coal micro-grids needing modular handling systems

- Coal-price volatility delaying equipment CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conveyors accounted for 48.2% of the coal handling equipment market in 2025 and are projected to grow at a 4.5% CAGR through 2031. This segment experienced growth as the market size for conveyor-integrated projects at mines and ports surpassed USD 14 billion in 2025. Innovations in ultra-long overland conveyor designs, such as Thyssenkrupp's rail-running conveyor offering up to 80% friction savings, are reducing haulage costs and gaining traction among Asian mining companies.

Replacement initiatives are also driving demand for conveyors. India's First Mile Connectivity upgrades include 102 projects replacing truck dumps with high-capacity conveyor belts. Additionally, BEUMER's new Taicang plant supports regional production of long-distance systems, reducing delivery lead times for Asia-Pacific customers. Crushers, stackers, and feeders collectively hold the remaining market share. Crushers are witnessing increased demand from coal-to-chemicals plants requiring sub-6 mm feed. Stackers and reclaimers are attracting investments at export terminals, such as McDuffie, where a USD 200 million modernization project is enhancing metallurgical coal loading efficiency.

Material conveying accounted for 48.2% of the coal handling equipment market share in 2025 and is expected to grow at a CAGR of 4.5% through 2031. Continuous belts connecting pits, preparation plants, stockyards, and ports contribute to long-term service revenues, representing nearly half of the segment's value.

Receiving and crushing remain critical but are increasingly commoditized. Indonesian rail-linked hubs are incorporating wagon tipplers and electric apron feeders, while India's centralized receiving facilities focus on under-car discharge systems and high-capacity dumpers. Storage and reclaim upgrades at ports, ranging from Richards Bay to terminals in the Russian Far East, require new stacker-reclaimers, although budget limitations often restrict the scope of full automation.

Complete Report Scope:

- By Equipment Type

- Conveyors

- Crushers

- Feeders

- Stackers

- Reclaimers

- Wagon Tipplers

- Magnetic Separators

- Hoppers

- Other Auxiliary Equipment

- By Operation Type

- Material Receiving

- Material Crushing

- Material Conveying

- Material Storage & Reclaim

- By Automation Level

- Manual

- Semi-automated

- Fully Automated

- By End-user

- Power Generation (Thermal Power Plants)

- Steel and Cement Industries

- Mining Operations

- Ports and Terminals

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific accounted for 45.0% of the revenue in 2025 and is expected to grow at a 4.8% CAGR through 2031, driven by increasing power and industrial coal demand in China, India, and Indonesia. The coal handling equipment market size associated with First Mile Connectivity schemes is projected to exceed USD 3.7 billion by 2030. Additionally, Sinopec's Inner Mongolian olefins project is intensifying China's demand for fine-coal preparation lines. Original Equipment Manufacturers (OEMs) with facilities in Taicang, Pune, or Jakarta benefit from reduced freight and duty costs, providing a competitive advantage in state-run tenders.

North America recorded a 4% increase in coal output in 2025, reaching 527.5 million short tons, primarily due to heightened winter demand caused by extreme weather. However, investments remain focused on maintenance rather than expansion. Notable projects include the modernization of Alabama's McDuffie coal terminal and Norfolk Southern's USD 200 million 3B Corridor, which emphasizes selective capital expenditure where export economics are favorable.

Europe continues to experience a decline in coal demand due to the rapid retirements of coal-fired plants. However, opportunities exist in biomass-ready retrofits, such as Poland's pellet blend upgrades, which cater to evolving energy needs.

South Africa, Russia, and select South American ports represent additional opportunity areas. South Africa's Richards Bay exported 57.66 million tons in 2025 and is investing in stacker-reclaimers to enhance capacity. In Russia, expansions at Vanino and Vostochny ports, which collectively add over 20 million tons of annual throughput, necessitate new shiploaders and yard equipment. The Middle East remains a negligible market for coal handling equipment due to its reliance on natural gas for power generation.

- AUMUND Fordertechnik GmbH

- Beumer Group GmbH & Co. KG

- Bevcon Wayors Pvt. Ltd.

- Caterpillar Inc.

- ContITech AG

- Doosan Heavy Industries & Construction Co., Ltd.

- Elecon Engineering Company Limited

- Epiroc AB

- Fenner Dunlop Conveyor Belting

- FLSmidth & Co. A/S

- Hitachi Construction Machinery Co., Ltd.

- Kawasaki Heavy Industries, Ltd.

- Komatsu Ltd.

- Martin Engineering

- McNally Bharat Engineering Company Limited

- Metso Oyj

- RPM Solutions

- Sandvik AB

- SCHADE Lagertechnik GmbH

- Siemens AG

- Tenova S.p.A.

- Babcock & Wilcox Enterprises, Inc.

- thyssenkrupp AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of coal-fired capacity in emerging Asia

- 4.2.2 Ageing infrastructure upgrade cycle across existing plants

- 4.2.3 Surge in surface-mined coal output requiring high-capacity conveyors

- 4.2.4 Adoption of automation & digital twins for OPEX reduction

- 4.2.5 Hybrid renewable-coal micro-grids needing modular handling systems

- 4.2.6 Coal-to-chemicals build-out in China & India spurring preparation demand

- 4.3 Market Restraints

- 4.3.1 Accelerated coal phase-out policies in Europe & North America

- 4.3.2 Coal price volatility delaying equipment CAPEX

- 4.3.3 Rising insurance & credit restrictions for coal assets

- 4.3.4 Shift to biomass-coal co-firing reducing coal-specific equipment

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Equipment Type

- 5.1.1 Conveyors

- 5.1.2 Crushers

- 5.1.3 Feeders

- 5.1.4 Stackers

- 5.1.5 Reclaimers

- 5.1.6 Wagon Tipplers

- 5.1.7 Magnetic Separators

- 5.1.8 Hoppers

- 5.1.9 Other Auxiliary Equipment

- 5.2 By Operation Type

- 5.2.1 Material Receiving

- 5.2.2 Material Crushing

- 5.2.3 Material Conveying

- 5.2.4 Material Storage & Reclaim

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-automated

- 5.3.3 Fully Automated

- 5.4 By End-user

- 5.4.1 Power Generation (Thermal Power Plants)

- 5.4.2 Steel and Cement Industries

- 5.4.3 Mining Operations

- 5.4.4 Ports and Terminals

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AUMUND Fordertechnik GmbH

- 6.4.2 Beumer Group GmbH & Co. KG

- 6.4.3 Bevcon Wayors Pvt. Ltd.

- 6.4.4 Caterpillar Inc.

- 6.4.5 ContiTech AG

- 6.4.6 Doosan Heavy Industries & Construction Co., Ltd.

- 6.4.7 Elecon Engineering Company Limited

- 6.4.8 Epiroc AB

- 6.4.9 Fenner Dunlop Conveyor Belting

- 6.4.10 FLSmidth & Co. A/S

- 6.4.11 Hitachi Construction Machinery Co., Ltd.

- 6.4.12 Kawasaki Heavy Industries, Ltd.

- 6.4.13 Komatsu Ltd.

- 6.4.14 Martin Engineering

- 6.4.15 McNally Bharat Engineering Company Limited

- 6.4.16 Metso Oyj

- 6.4.17 RPM Solutions

- 6.4.18 Sandvik AB

- 6.4.19 SCHADE Lagertechnik GmbH

- 6.4.20 Siemens AG

- 6.4.21 Tenova S.p.A.

- 6.4.22 Babcock & Wilcox Enterprises, Inc.

- 6.4.23 thyssenkrupp AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment