|

시장보고서

상품코드

2072635

두개내 동맥류 치료 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Intracranial Aneurysm Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

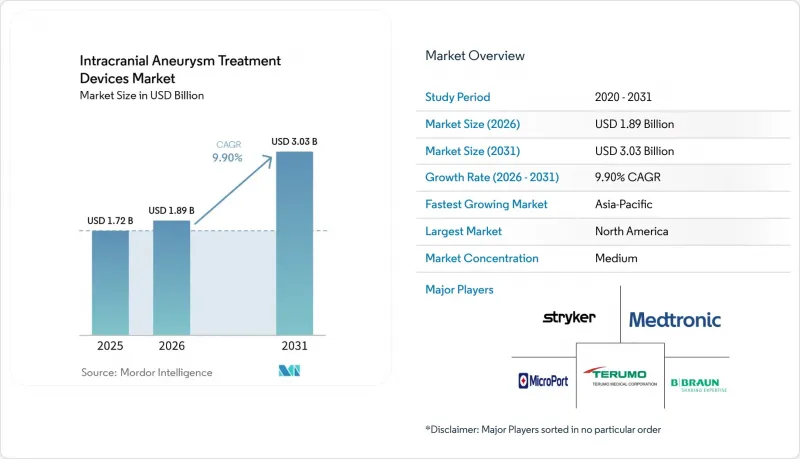

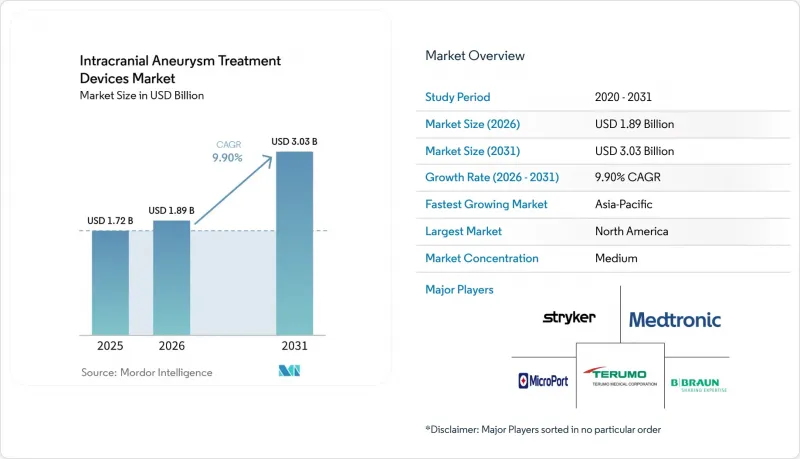

Mordor Intelligence에 의하면, 두개내 동맥류 치료 기기 시장 규모는 2025년에 17억 2,000만 달러로 평가되었고, 2026년 18억 9,000만 달러로 추정되고, 2031년까지 30억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.90%를 나타낼 전망입니다.

본 보고서는 기기 유형별(색전 코일, 플로우 다이버터, 낭내 플로우 디스래프터, 두개내 스텐트 및 풍선 등), 최종 사용자별(병원, 외래수술센터(ASC), 전문 뇌신경외과 센터), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 두개내 동맥류 치료 기기 시장 동향 및 인사이트

저침습 혈관내 치료에 대한 수요 증가

외래 진료에 적합한 플로우 다이버터와 AI 유도형 로봇 시스템의 등장으로, 외래 환경에서도 복잡한 신경혈관 수술이 가능해졌습니다. 2024년에는 미국의 외래수술센터(ASC)에서 330만 명의 메디케어 수급자가 치료를 받았으며, 이는 입원을 수반하는 뇌신경외과 수술에서 결정적인 전환이 이루어졌음을 보여주었습니다. CorPath GRX 플랫폼 등의 로봇 시스템 도입을 통해 100%의 기술적 성공률과 방사선 피폭량 감소를 실현함으로써, 의료기관들이 외래 전용 신경 중재 시술실을 개설하는 추세가 가속화되고 있습니다.

뇌 영상 검사의 부수적 소견에 따른 미파열 동맥류 검출률 증가

고해상도 MRI 및 CT 혈관조영술을 통해 현재는 수많은 무증상 병변이 발견되고 있으며, 치료 대상이 되는 환자층이 확대되고 있습니다. 2024년에 FDA 승인을 받은 'Viz ANEURYSM'와 같은 AI 알고리즘은 영상 판독 프로토콜을 표준화하고, 판독자 간 편차를 줄여줍니다. 이러한 급증은 위험 계층화 워크플로우에 부담을 주고 있으며, 차세대 기기와 결합된 의사결정 지원 도구에 대한 수요를 촉진하고 있습니다.

의료기기 및 시술의 높은 비용과 제한된 보험 급여

미국 CMS(의료보험서비스센터)의 패스스루 코드는 최첨단 임플란트에 대해 여전히 제한적인 반면, 한국에서는 플로우 다이버터의 보험 적용이 대형 동맥류로 한정되어 있어 보급률에 상한선이 설정되어 있습니다. 현재 각 제약사는 제품 출시 시 의료 경제성에 관한 자료와 위험 분담 계약을 함께 제시하며, 지불 주체에게 제품의 수명 주기 가치를 입증하기 위해 노력하고 있습니다.

부문별 분석

플로우 다이버터는 가장 빠른 성장 궤도에 올라 있으며, 2031년까지 연평균 성장률(CAGR) 14.0%로 확대될 전망이며, 코일의 우위를 꾸준히 잠식하고 있습니다. 'Pipeline Vantage'는 주요 임상시험에서 6개월간 81.7%의 폐색률을 기록한 반면, 친수성 코팅이 적용된 변형 제품은 혈전성 사건을 4.7%로 감소시켰으며, 92.3%의 장기 폐색률을 달성했습니다. 백금은 방사선 불투과성과 생체 적합성 덕분에 재료 구성의 30-40%를 차지하며, 여전히 핵심적인 역할을 수행하고 있습니다.

이 부문의 전망은 파열된 동맥류에서 1년 후 86.5%의 완전 폐쇄율을 달성하는 'WEB 17' 등의 낭내 파괴 장치에 힘입어 발전하고 있습니다. 그 결과, 전 세계의 구매자들은 재치료 횟수가 적고 학습 곡선이 짧은 것으로 기대되는 기기로 자본 예산을 재분배하고 있으며, 이는 두개내 동맥류 치료 기기 시장의 활성화로 이어지고 있습니다.

지역별 분석

북미는 2025년, FDA의 ‘브레이크스루 패스웨이(Breakthrough Pathway)’와 보험사들의 프리미엄 임플란트에 대한 수용성 증가에 힘입어 매출 점유율 41.3%를 유지했습니다. 기업 간 M&A는 여전히 활발하게 이루어지고 있으며, 그 한 예로 정맥 및 신경혈관 분야로의 진출을 확대하고 있는 스트라이커(Stryker)사가 49억 달러에 이나리(Inari)사를 인수한 사례를 들 수 있습니다. 그러나 FDA의 의료기기 심사 담당자 감원으로 인해 승인 대기 기간이 길어질 위험이 있어, 단기적인 성장 가속화가 둔화될 가능성이 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 11.2%로, 가장 빠르게 성장하고 있는 지역입니다. 중국에서는 국가의약품감독관리국(NMPA)의 개혁과 '건강 중국 2030' 지침에 따라 뇌혈관 의료에 대한 자금 지원이 늘어나고 있는 반면, 일본의 의약품 및 의료기기종합기구(PMDA)는 예측 가능하고 과학에 기반한 승인을 진행하고 있습니다. 중산층 수요 증가와 정책 지원이 맞물리면서 두개내 동맥류 치료용 기기 시장은 성장하고 있지만, 보험 급여 제도의 차이로 인해 가격대의 폭은 여전히 넓습니다.

유럽의 MDR(의료기기 규정) 환경은 여전히 엄격하며, 장기적인 안전성 데이터가 중시되고 있습니다. 페남브라사가 2024년에 흡입 시스템 및 코일 시스템에 대해 취득한 CE 마크는 확고한 임상적 근거가 뒷받침된다면 신규 의료기기라도 승인 절차를 순조롭게 통과할 수 있음을 보여줍니다. 브렉시트로 인한 규제 차이로 인해 기업들은 영국 규정을 준수하기 위해 별도의 예산을 편성해야 하며, 이로 인해 일부 중소 진출기업들은 EU 27개국을 우선시할 수밖에 없는 상황에 처해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the intracranial aneurysm treatment devices market size was valued at USD 1.72 billion in 2025 and is estimated to grow from USD 1.89 billion in 2026 to reach USD 3.03 billion by 2031, at a CAGR of 9.90% during the forecast period (2026-2031).

This report is Segmented by Device Type (Embolization Coils, Flow Diverters, Intrasaccular Flow Disruptors, Intracranial Stents & Balloons, and More), End User (Hospitals, Ambulatory Surgical Centers, Specialty Neurosurgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Intracranial Aneurysm Treatment Devices Market Trends and Insights

Rising Demand for Minimally Invasive Endovascular Procedures

Outpatient-ready flow diverters and AI-guided robotic systems have made complex neurovascular work feasible in ambulatory environments. In 2024, US ambulatory surgical centers treated 3.3 million Medicare beneficiaries, signaling a decisive swing away from inpatient neurosurgery. Robotic deployments such as the CorPath GRX platform secured 100% technical success and lower radiation exposure, encouraging health systems to open dedicated outpatient neuro-intervention suites.

Growing Prevalence of Unruptured Aneurysm Detection Through Incidental Brain Imaging

High-resolution MRI and CT angiography now uncover countless asymptomatic lesions, expanding the treatable population. AI algorithms like Viz ANEURYSM, cleared by the FDA in 2024, standardize reading protocols and reduce inter-observer variability. The surge strains risk-stratification workflows and stimulates demand for decision-support tools bundled with next-generation devices.

High Device & Procedural Costs With Limited Reimbursement

US CMS pass-through codes remain restrictive for cutting-edge implants, while Korea reimburses flow diverters only for large aneurysms, capping penetration. Manufacturers now pair launches with health-economic dossiers and risk-sharing contracts to prove lifetime value to payers.

Other drivers and restraints analyzed in the detailed report include:

- Age-Linked Hypertension & Smoking Prevalence in Developing Economies

- FDA Breakthrough-Device Designations Accelerating Device Approvals

- Shortage Of Dual-Trained Endovascular Neurosurgeons in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flow diverters occupy the fastest lane, expanding at a 14.0% CAGR through 2031 and steadily eroding coil dominance. The Pipeline Vantage recorded 81.7% six-month occlusion in pivotal studies, while hydrophilic-coated variants cut thrombotic events to 4.7% and achieved 92.3% long-term closure. Platinum remains central, forming 30-40% of material content for its radiopacity and biocompatibility.

The segment's outlook is strengthened by intrasaccular disruptors such as WEB 17 that produce 86.5% complete occlusion in ruptured aneurysms after one year. As a result, global purchasers are reallocating capital budgets toward devices promising fewer retreatments and shorter learning curves, uplifting the intracranial aneurysm treatment devices market.

Complete Report Scope:

- By Device Type

- Embolization Coils

- Flow Diverters

- Intrasaccular Flow Disruptors

- Intracranial Stents & Balloons

- Aneurysm Clips

- Others

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty Neurosurgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America sustained a 41.3% revenue share in 2025, aided by FDA breakthrough pathways and payer openness to premium implants. Corporate M&A remains brisk, exemplified by Stryker's USD 4.9 billion Inari acquisition that broadens access to venous and neurovascular segments. Nonetheless, device review staffing cuts at the FDA risk stretching approval queues, tempering near-term acceleration.

Asia-Pacific is the fastest-growing region with an 11.2% CAGR through 2031. China's NMPA reforms and the "Healthy China 2030" mandate increase funding for cerebrovascular care, whereas Japan's PMDA provides predictable, science-based approvals. Growing middle-class demand, combined with policy support, expands the intracranial aneurysm treatment devices market, though heterogeneous reimbursement keeps price tiers wide.

Europe's MDR environment remains rigorous, emphasizing long-term safety data. Penumbra's 2024 CE marks for aspiration and coil systems show that novel devices can still navigate the pathway when supported by robust clinical evidence. Brexit-related divergence obliges firms to budget separately for UK conformity, nudging some smaller entrants to prioritize EU27 first.

- Stryker

- Medtronic

- Johnson & Johnson (CERENOVUS)

- Terumo Neuro

- MicroPort

- Penumbra

- Balt Extrusion S.A.

- Phenox

- B. Braun

- Integra LifeSciences

- Adeor Medical

- Sequent Medical

- Wallaby Medical

- Rapid Medical

- Evasc Neurovascular

- Kaneka Medix

- Cerus Endovascular

- Ceremedix (Boston Scientific spin-out)

- Route 92 Medical

- MicroVasx

- Codman Neuro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally-Invasive Endovascular Procedures

- 4.2.2 Growing Prevalence of Unruptured Aneurysm Detection Through Incidental Brain Imaging

- 4.2.3 Age-Linked Hypertension & Smoking Prevalence in Developing Economies

- 4.2.4 FDA Breakthrough-Device Designations Accelerating Device Approvals

- 4.2.5 Emergence of AI-Guided Robotic Neuro-Intervention Platforms

- 4.2.6 Venture Funding Surge into Nano-Coil Surface Engineering Start-Ups

- 4.3 Market Restraints

- 4.3.1 High Device & Procedural Costs with Limited Reimbursement

- 4.3.2 Shortage of Dual-Trained Endovascular Neurosurgeons in Emerging Markets

- 4.3.3 Device-Related Thrombo-Embolic Complications Requiring Lifelong DAPT

- 4.3.4 Supply-Chain Dependence on Platinum & Cobalt Price Volatility Exposure

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Device Type

- 5.1.1 Embolization Coils

- 5.1.2 Flow Diverters

- 5.1.3 Intrasaccular Flow Disruptors

- 5.1.4 Intracranial Stents & Balloons

- 5.1.5 Aneurysm Clips

- 5.1.6 Others

- 5.2 By End-user

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Specialty Neurosurgical Centers

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Stryker

- 6.3.2 Medtronic

- 6.3.3 Johnson & Johnson (CERENOVUS)

- 6.3.4 Terumo Neuro

- 6.3.5 MicroPort Scientific

- 6.3.6 Penumbra Inc.

- 6.3.7 Balt Extrusion S.A.

- 6.3.8 Phenox GmbH

- 6.3.9 B. Braun Melsungen

- 6.3.10 Integra LifeSciences

- 6.3.11 Adeor Medical

- 6.3.12 Sequent Medical

- 6.3.13 Wallaby Medical

- 6.3.14 Rapid Medical

- 6.3.15 Evasc Neurovascular

- 6.3.16 Kaneka Medix

- 6.3.17 Cerus Endovascular

- 6.3.18 Ceremedix (Boston Scientific spin-out)

- 6.3.19 Route 92 Medical

- 6.3.20 MicroVasx

- 6.3.21 Codman Neuro

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment