|

시장보고서

상품코드

2072636

주사용 생리식염수 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Normal Saline For Parenteral Use - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

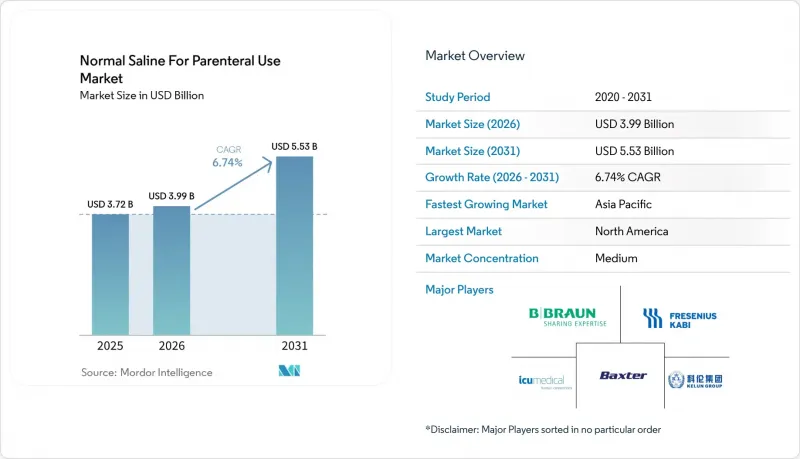

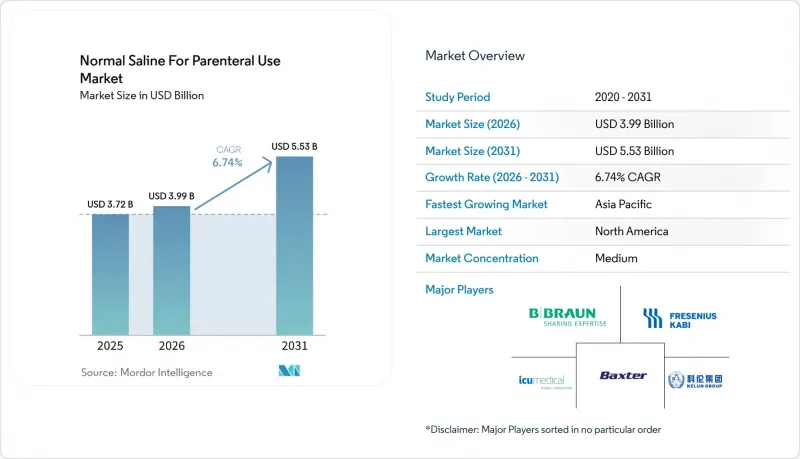

Mordor Intelligence에 의하면, 주사용 생리식염수 시장 규모는 2025년에 37억 2,000만 달러로 평가되었고, 2026년 39억 9,000만 달러로 추정되고, 2031년까지 55억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.74%를 나타낼 전망입니다.

본 보고서는 포장 유형별(연질 파우치, 기타), 용량별(100mL 이하, 101-250mL, 251-500mL, 501-1,000mL), 용도별(정맥 주사, 기타), 최종 사용자별(병원, 기타), 유통 채널별(직접 입찰 및 그룹 구매, 기타), 지역별(북미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 주사용 생리식염수 시장 동향 및 인사이트

전 세계 외과 수술 건수 증가

모든 수술에서 마취, 수액 투여, 약물 투여를 위해 정맥로를 확보해야 하므로, 수술 건수와 생리식염수 수요는 직접적인 관련이 있습니다. 영국에서는 2024년 12월에 235만 건의 응급실 내원 건수가 기록되어, 전년 대비 7.6% 증가했습니다. 이는 의료 체계 확충에 따라 누적된 수요가 수술 건수로 이어지고 있음을 시사합니다. 벨기에에서는 최근 보고 연도에 주민 10만 명당 2만 712건의 수술이 시행된 반면, 사하라 이남 아프리카에서는 평균 500건 미만에 그치고 있어, 신흥 경제국에서 수술실이 증설됨에 따라 수요 증가 여지가 있음을 여실히 보여주고 있습니다. 미국에서는 현재 6,100곳 이상의 메디케어 인증 외래수술센터(ASC)가 정형외과 및 안과 분야의 대량의 환자를 진료하고 있으며, 폐기량 감축과 시술의 유연성 사이에서 균형을 이룬 101-250mL 및 251-500mL 용량의 백에 대한 수요가 정착되어 있습니다. 이러한 동향은 '주사용 생리식염수' 시장에서 가장 빠르게 성장하고 있는 부문의 지표와 일치합니다. 따라서 병원과 외래수술센터(ASC)는 기준 사용량과 중용량 제품 구성으로의 전환을 모두 주도하고 있습니다.

만성 질환과 입원 부담 증가

만성 질환은 잦은 입원을 초래하며, 수분 보충과 약물 투여를 위해 대량의 정맥 주사액이 소모됩니다. 미국 성인의 10명 중 6명은 적어도 한 가지 만성 질환을 앓고 있으며, 이로 인해 연간 약 3,600만 건의 입원이 발생하고, 각 입원 건당 수 리터의 생리식염수가 사용되고 있습니다. 유럽의 65세 이상 인구 비율은 2023년에 21%에 달했으며, 1,000명당 퇴원자 수는 155명으로 증가하여 유지 수액에 대한 안정적인 수요가 지속되고 있습니다. 중국에서는 2025년까지 60세 이상 인구가 3억 명을 넘어설 것으로 예상되며, 이러한 인구 급증으로 인해 주요 연안 도시 이외 지역의 입원 환자 수가 더욱 증가할 전망입니다. 이러한 수요량은 '주사용 생리식염수' 시장을 주도하고 있지만, 중국 및 EU 일부 국가의 집중 조달 제도로 인해 단가가 압박받고 있어, 대규모의 저비용 생산 공장을 보유하지 않은 제조업체의 경우 이익률 확대가 어려운 상황입니다. 그 결과, 매출 성장세는 유지되고 있지만 수익성에는 압박이 가해지고 있으며, 산업 통합이 계속해서 진행되고 있습니다.

엄격한 규제와 품질 준수 요건

무균 주사제 제조 공장은 FDA 21 CFR Part 211 및 2022년판 EMA GMP 부록 1을 준수해야 합니다. 이러한 무균 제조 공정에 대한 더욱 엄격한 규제로 인해, 신규 건설(그린필드)의 자본 비용은 최대 1억 달러까지 치솟고 있습니다. FDA는 2024년에 무균 의약품 관련 위반 사항으로 12건의 경고장을 발부했으며, 이는 사소한 위반이라도 생산이 중단될 수 있음을 시사합니다. 박스터사의 홍수로 인한 가동 중단은 아무리 엄격한 규정 준수를 실천하더라도 자연재해를 완전히 막을 수는 없습니다는 사실을 여실히 보여주었습니다. 또한, 가동 재개에는 클린룸의 재인증을 받는 데 상당한 시간이 소요되어 시장 재진입이 지연되었습니다. 높은 진입 장벽은 신규 시장 진출기업의 의욕을 꺾고 생산을 기존 기업에 집중시키는 한편, 단일 공장이 기능 부전에 빠질 경우 시스템적 위험을 초래하고 있습니다. 그 결과, 규제가 엄격한 지역의 '주사용 생리식염수' 시장의 잠재적 연평균 성장률(CAGR)은 1.2% 하락했습니다.

부문별 분석

2025년에는 플라스틱 병 시장 점유율이 전 세계 매출의 48.54%에 달했으나, 연질 파우치는 높은 보관 효율과 운송 하중 경감 덕분에 2031년까지 연평균 성장률(CAGR) 8.54%로 성장할 전망입니다. 이러한 접이식 구조는 창고 점유 면적을 약 60% 줄일 수 있어, 공간 임대료가 비싼 도심 지역의 병원에게는 결정적인 이점이 됩니다. B. Braun의 'Ecoflac'나 Baxter의 'Viaflex'와 같은 비 PVC 가방은 이미 지속가능성을 중시하는 유럽의 입찰에서 채택되고 있지만, 비용을 중시하는 아시아의 시설에서는 PVC 가방이 채택되고 있습니다. 다만, 재활용 규제가 강화될 경우 방침을 변경할 가능성이 있습니다. 재택 간호에서 수동 중력식 점적 요법의 경우, 환자들이 용기의 내구성과 점적 속도의 가시성을 중요시하기 때문에 플라스틱 병이 여전히 선호되고 있으며, 성장률은 둔화되고 있지만 상당한 시장 기반을 유지하고 있습니다. 유리병은 현재, 재사용형 유리 용기가 여전히 멸균 처리를 거치는 아프리카 및 라틴아메리카 일부 지역에서 틈새 시장으로 활용되고 있지만, 세계 시장 점유율은 계속해서 감소하고 있습니다.

각 제조업체는 오염을 방지하기 위해 봉투를 밀폐식 이송 장치와 일체화했으며, 이 기능은 팬데믹 이후의 감염 예방 대책에도 부합합니다. 물류 비용 절감도 중요한 요소입니다. 유연한 백을 실은 팔레트는 같은 양의 액체를 채운 경질 용기에 비해 최대 20% 더 가벼워, 운송 시 배출량과 비용을 절감할 수 있습니다. 미국 북동부 지역의 한 병원에 따르면, 폐기물 처리 비용과 면적 절감분을 산입한 결과, 봉투 형태로 전환한 지 9개월 만에 투자 회수를 달성했다고 보고되었습니다. 한편, 다층 폴리머 필름은 폐기물 분리 수거를 복잡하게 만들기 때문에 재활용 가능성에 대한 우려가 남아 있습니다. 탄소 보고 규제가 강화되는 가운데, 단일 소재 또는 화학적으로 재활용 가능한 필름을 모색하고 있는 제조업체는 경쟁 우위를 확보할 가능성이 있습니다.

2025년에는 101-250mL 용량이 항생제 희석 및 일상적인 수액 투여 프로토콜에 적합하다는 점 때문에 주사용 생리식염수 시장에서 55.43%의 점유율을 차지하며 시장을 주도했습니다. 중용량인 251-500mL 용기는 명백히 성장의 견인차 역할을 하고 있으며, 연평균 성장률(CAGR) 8.43%로 확대되고 있습니다. 이는 외래수술센터(ASC)가 60-180분 동안의 시술 중 폐기물을 최소화할 수 있는 크기를 표준화하고 있기 때문입니다. 501-1,000mL 대용량 용기는 중환자실(ICU) 수요에 따라 널리 보급되고 있지만, 이 부문 특유의 호재는 없습니다.

보험사가 중증도가 낮은 환자를 비용이 많이 드는 입원 병상에서 멀리하도록 유도하고 있기 때문에 외래 수술로의 전환이 중용량 제품의 보급에 영향을 미치고 있습니다. 이러한 변화는 휴대용 펌프가 다루기 쉬운 250mL 용량의 저장탱크를 선호하는 가정 내 수액 요법의 추세와 맞물려 진행되고 있습니다. 일반적으로 3-10mL 용량의 프리필드 플러시 주사기는 CLABSI(중심정맥카테터 관련 혈류 감염) 감소 프로그램 덕분에 급성장하고 있는 마이크로 부문을 개척하고 있습니다. 미국의 병원에서는 CLABSI 1건당 약 4만 8,000달러의 비용이 소요되고 있으며, 감염률이 낮아진다면 이러한 주사기의 높은 가격도 쉽게 정당화될 수 있습니다. 그러나 원자재 가격의 급등은 고도로 자동화된 조립 라인을 통해 상쇄되지 않는 한, 주사기의 수익성을 위협하는 과제가 되고 있습니다.

지역별 분석

북미는 시장의 성숙과 균형 잡힌 크리스탈로이드로의 점진적인 대체가 진행된 결과, 2025년에는 전 세계 매출의 42.67%를 차지했습니다. 2024년 허리케인으로 인한 피해로 박스터사의 노스 코브 공장이 가동을 중단하게 된 것은 생산 집중화에 따른 위험성을 여실히 드러냈습니다. 그 후 FDA가 제시한 비용 절감 지침과 GPO(그룹 구매 조직)공급업체 다각화는 조달 전략에 장기적인 영향을 미치고 있습니다. 캐나다의 단일 지불자 제도와 니스쇼어링 거점으로서의 멕시코의 역할은 모두 지역 동향에 영향을 미치고 있으며, 멕시코의 낮은 인건비는 미국 시장을 겨냥한 새로운 생산 능력을 유치하고 있습니다.

아시아태평양은 중국, 인도, 베트남, 인도네시아의 인프라 확충을 원동력으로 삼아 2031년까지 연평균 성장률(CAGR) 7.54%라는 가장 빠른 성장세를 보이고 있습니다. 중국의 쾰른 그룹은 비용 경쟁력을 바탕으로 80개국으로 제품을 수출하고 있습니다. 한편, 인도의 '메이크 인 인디아' 정책은 국내 제조 능력과 수출 능력을 강화하고 있습니다. 동남아시아 국가들은 무균 주사제 생산 라인을 확충하기 위한 외국인 직접 투자(FDI)를 유치하고 있으며, 이를 통해 지역 내 공급망이 강화되고 유럽산 수입품에 대한 의존도가 낮아지고 있습니다. 일본 등 성숙 시장도 여전히 성장을 이어가고 있으며, 이는 고령화에 따른 시술 건수 증가가 비용 절감 노력에 의해 상쇄되고 있음을 반영하고 있습니다.

2025년에는 유럽이 전 세계 지출에서 상당한 비중을 차지했습니다. 개정된 부속서 1의 규정에 따라 규정 준수 비용이 증가함에 따라, 프레제니우스 카비나 B. 브라운과 같은 대기업들의 생산 통합이 진행되고 있습니다. 인구 고령화는 여전히 기초 수요를 끌어올리고 있지만, 남유럽의 긴축 재정 조치와 영국의 당일 수술로의 전환으로 인해 전반적인 수요량은 억제되고 있습니다. 유럽연합(EU)의 지속가능성 관련 지침은 포장재 선택에 더욱 큰 영향을 미치고 있으며, 소폭의 가격 프리미엄이 적용되는 비PVC 제품이 선호되고 있습니다.

중동 및 아프리카와 남미를 합친 2025년 매출액에서 차지하는 비중은 미미했습니다. 걸프협력회의(GCC) 회원국들은 고품질의 즉시 사용 가능한 솔루션을 선호하는 3차 의료기관에 대한 투자를 추진하고 있지만, 아프리카의 입찰에서는 최저가를 제시한 업체가 선정되는 경우가 많아 중국이나 인도공급업체들에게 유리하게 작용하고 있습니다. 브라질의 국민보편의료보험 제도 확대는 안정적인 수요를 창출하는 한편, 공급업체들은 이익률을 제한하는 기준 가격 상한선에 얽매여 있습니다. 전반적으로 신흥 시장의 성장률이 선진 지역을 상회하고 있어, 다국적 제조업체들의 지역별 포트폴리오 균형이 재조정되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the normal saline for parenteral use market size was valued at USD 3.72 billion in 2025 and is estimated to grow from USD 3.99 billion in 2026 to reach USD 5.53 billion by 2031, at a CAGR of 6.74% during the forecast period (2026-2031).

This report is Segmented by Packaging Type (Flexible Bags, and More), Volume Size (<=100 ML, 101-250 ML, 251-500 ML, and 501-1, 000 ML), Application (Intravenous Injection, and More), End User (Hospitals, and More), Distribution Channel (Direct Tenders & Group Purchasing, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Normal Saline For Parenteral Use Market Trends and Insights

Growing Global Surgical Procedure Volumes

Every surgical case requires intravenous access for anesthesia, fluid resuscitation, and drug delivery, thereby directly linking procedure counts to saline demand. The United Kingdom logged 2.35 million accident-and-emergency visits in December 2024, a 7.6% year-over-year increase, signaling pent-up demand that converts into surgeries as capacity expands. Belgium performed 20,712 procedures per 100,000 residents in the latest reporting year, while sub-Saharan Africa averages below 500, underlining upside potential as emerging economies add operating theaters. In the United States, more than 6,100 Medicare-certified ambulatory surgery centers now handle high-volume orthopedic and ophthalmologic cases, cementing demand for 101-250 mL and 251-500 mL bags that balance waste with procedural flexibility. These trends align with the fastest-growing segment metrics noted in the Normal Saline for Parenteral Use market. Hospitals and ambulatory centers thus shape both baseline volume and the product-mix evolution toward intermediate sizes.

Rising Burden of Chronic Diseases and Hospital Admissions

Chronic illnesses drive frequent hospitalizations that consume large-volume parenteral fluids for hydration and drug administration. Six in 10 U.S. adults live with at least one chronic disease, leading to roughly 36 million admissions per year, each involving multiple liters of saline. Europe's population over 65 reached 21% in 2023, elevating discharge rates to 155 per 1,000 inhabitants and sustaining steady demand for maintenance fluids. China expects more than 300 million citizens over 60 by 2025, a demographic surge that magnifies inpatient throughput outside major coastal cities. Although these volumes drive the Normal Saline for Parenteral Use market, centralized procurement schemes in China and several EU states compress unit pricing, challenging margin expansion for manufacturers without large-scale, low-cost plants. The net effect supports topline growth but pressures profitability, fostering continued consolidation.

Stringent Regulatory and Quality Compliance Requirements

Sterile-injectable plants must comply with FDA 21 CFR Part 211 and the 2022 EMA GMP Annex 1, whose tighter aseptic-process rules push greenfield capital costs up to USD 100 million. The FDA issued 12 warning letters for sterile-drug violations in 2024, illustrating how even minor deviations can halt production. Baxter's flood-induced closure revealed that stringent compliance does not fully shield against natural disasters, while the restart required extensive cleanroom requalification, delaying market re-entry. High barriers dampen new-entrant interest, keeping production concentrated among incumbents but also creating systemic risk when a single plant fails. The resulting impact trims 1.2 percentage points from the Normal Saline for Parenteral Use market's potential CAGR in highly regulated regions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Healthcare Infrastructure in Emerging Economies

- Increasing Adoption of Ready-to-Use Sterile IV Solutions

- Environmental Concerns Over Single-Use Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The market share for plastic bottles reached 48.54% of global revenue in 2025, yet flexible bags are on track for 8.54% CAGR through 2031 due to storage efficiency and lighter freight loads. These collapsible formats lower warehouse footprint by roughly 60%, a decisive advantage for urban hospitals where space commands premium rents. B. Braun's Ecoflac and Baxter's Viaflex non-PVC bags already win sustainability-weighted European tenders, while cost-focused Asian facilities adopt PVC bags but may pivot if recycling mandates tighten. Plastic bottles remain preferred for manual gravity infusions in home care, where patients value rigidity and drop-rate visibility, sustaining a sizable base despite slower growth. Glass bottles now serve niche markets in parts of Africa and Latin America where reusable glassware is still sterilized, but their global share continues to erode.

Manufacturers integrate bags with closed-system transfer devices to curtail contamination, a feature that aligns with post-pandemic infection controls. Logistics savings also matter: a pallet of flexible bags weighs up to 20% less than equivalently filled rigid containers, reducing transport emissions and cost. Hospitals in the U.S. Northeast reported a nine-month payback after switching to bag formats once waste-handling fees and floor-space savings were tallied. Conversely, recyclability questions linger because multilayer polymer films complicate waste-stream sorting. Producers exploring monomaterial or chemically recyclable films may gain an edge as carbon-reporting rules tighten.

The 101-250 mL category led the Normal Saline for Parenteral Use market with a 55.43% share in 2025, driven by its fit with antibiotic dilution and routine hydration protocols. Intermediate 251-500 mL bags are the clear growth leader, advancing at an 8.43% CAGR as ambulatory surgery centers standardize on sizes that minimize waste during 60- to 180-minute procedures. Large 501-1,000 mL containers expand broadly with ICU demand but without a segment-specific tailwind.

Ambulatory migration influences mid-range uptake, as payers direct low-acuity cases away from costlier inpatient beds. This shift dovetails with home-infusion trends where portable pumps favor manageable 250 mL reservoirs. Prefilled flush syringes, typically 3-10 mL, carve a fast-growing micro-segment thanks to CLABSI mitigation programs. U.S. hospitals spend roughly USD 48,000 per CLABSI, making the syringes' premium easily justified when infection rates drop. Yet, raw-material inflation challenges syringe profitability unless offset through highly automated assembly lines.

Complete Report Scope:

- By Packaging Type

- Flexible Bags

- Plastic Bottles

- Glass Bottles

- By Volume Size

- <=100 mL

- 101 - 250 mL

- 251 - 500 mL

- 501 - 1 000 mL

- By Application

- Intravenous Injection

- Intramuscular Injection

- Flush / Catheter Lock

- By End User

- Hospitals

- Clinics & Ambulatory Surgery Centers

- Home Healthcare Settings

- By Distribution Channel

- Direct Tenders & Group Purchasing

- Distributors / Wholesalers

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America generated 42.67% of global revenue in 2025 because of market maturity and incremental substitution by balanced crystalloids. The 2024 hurricane damage that idled Baxter's North Cove plant revealed the risks of concentrated production; subsequent FDA conservation guidance and GPO supplier diversification have lasting effects on sourcing strategy. Canada's single-payer system and Mexico's role as a nearshoring location both influence regional dynamics, with Mexico's lower labor costs attracting fresh capacity aimed at U.S. demand.

Asia-Pacific shows the fastest expansion at 7.54% CAGR through 2031, powered by infrastructure build-outs across China, India, Vietnam, and Indonesia. China's Kelun Group exports to 80 countries, capitalizing on cost advantages, while India's "Make in India" push strengthens domestic manufacturing and export capacity. Southeast Asian nations receive FDI that adds sterile-injectable lines, tightening regional supply chains, and reducing reliance on European imports. Mature markets such as Japan still grow, reflecting increased procedure volumes among aging populations balanced by cost-containment efforts.

Europe accounted for significant percentage of global spending in 2025. Revised Annex 1 rules increase compliance expenses, consolidating production among large players like Fresenius Kabi and B. Braun. Aging demographics continue to propel baseline demand, yet austerity measures in Southern Europe and the United Kingdom's shift toward day-case surgery moderate overall volume. The European Union's sustainability directives further influence packaging decisions, favoring non-PVC lines that command minor price premiums.

The Middle East & Africa and South America combined for minor share of 2025 revenue. Gulf Cooperation Council countries invest in tertiary hospitals that favor premium ready-to-use solutions, while African tenders often reward the lowest bidder, benefiting Chinese and Indian suppliers. Brazil's universal healthcare expansion channels consistent demand but subjects suppliers to reference-pricing caps that limit margin. Overall, emerging-market growth outpaces developed regions, re-balancing the geographic portfolio of multinational producers.

- B. Braun

- Baxter

- Cardinal Health

- Cisen Pharmaceutical Co., Ltd.

- CR Double-Crane Pharmaceutical Co., Ltd.

- Fresenius

- Grifols

- Hospira (Pfizer)

- Huaren Pharmaceuticals

- ICU Medical

- Kelun Group

- Nipro

- Otsuka

- Qidu Pharmaceutical

- Shijiazhuang No. 4 Pharmaceutical Co., Ltd.

- SSY Group Limited

- Terumo

- Zhejiang Chimin Health Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Surgical Procedure Volumes

- 4.2.2 Rising Burden of Chronic Diseases and Hospital Admissions

- 4.2.3 Expansion of Healthcare Infrastructure in Emerging Economies

- 4.2.4 Increasing Adoption of Ready-to-Use Sterile IV Solutions

- 4.2.5 Supply Chain Localization and Capacity Investments Post-Pandemic

- 4.2.6 Growth of Home and Ambulatory Infusion Therapies

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory and Quality Compliance Requirements

- 4.3.2 Commodity Pricing Pressure and Thin Margins

- 4.3.3 Clinical Shift Toward Balanced Crystalloid Alternatives

- 4.3.4 Environmental Concerns Over Single-Use Plastic Packaging

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Packaging Type

- 5.1.1 Flexible Bags

- 5.1.2 Plastic Bottles

- 5.1.3 Glass Bottles

- 5.2 By Volume Size

- 5.2.1 <=100 mL

- 5.2.2 101 - 250 mL

- 5.2.3 251 - 500 mL

- 5.2.4 501 - 1 000 mL

- 5.3 By Application

- 5.3.1 Intravenous Injection

- 5.3.2 Intramuscular Injection

- 5.3.3 Flush / Catheter Lock

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics & Ambulatory Surgery Centers

- 5.4.3 Home Healthcare Settings

- 5.5 By Distribution Channel

- 5.5.1 Direct Tenders & Group Purchasing

- 5.5.2 Distributors / Wholesalers

- 5.5.3 Online Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 B. Braun Melsungen AG

- 6.3.2 Baxter International Inc.

- 6.3.3 Cardinal Health

- 6.3.4 Cisen Pharmaceutical Co., Ltd.

- 6.3.5 CR Double-Crane Pharmaceutical Co., Ltd.

- 6.3.6 Fresenius Kabi AG

- 6.3.7 Grifols S.A.

- 6.3.8 Hospira (Pfizer)

- 6.3.9 Huaren Pharmaceuticals

- 6.3.10 ICU Medical, Inc.

- 6.3.11 Kelun Group

- 6.3.12 Nipro Corporation

- 6.3.13 Otsuka Pharmaceutical Co., Ltd.

- 6.3.14 Qidu Pharmaceutical

- 6.3.15 Shijiazhuang No. 4 Pharmaceutical Co., Ltd.

- 6.3.16 SSY Group Limited

- 6.3.17 Terumo Corporation

- 6.3.18 Zhejiang Chimin Health Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment