|

시장보고서

상품코드

2072640

인쇄회로기판 조립 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Printed Circuit Board Assembly - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

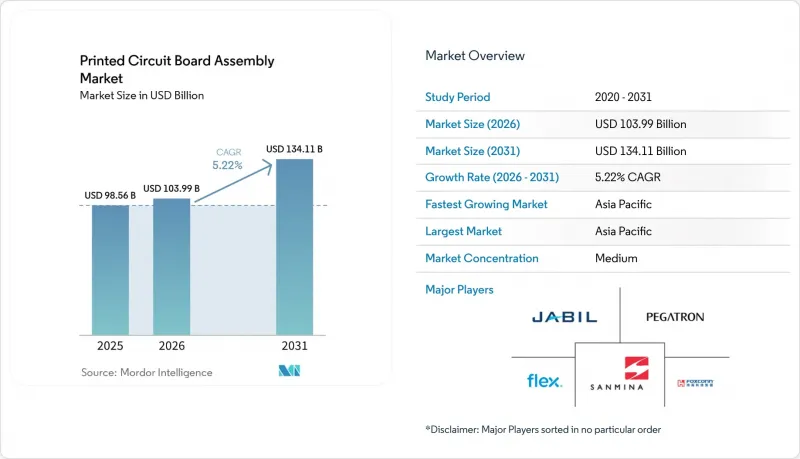

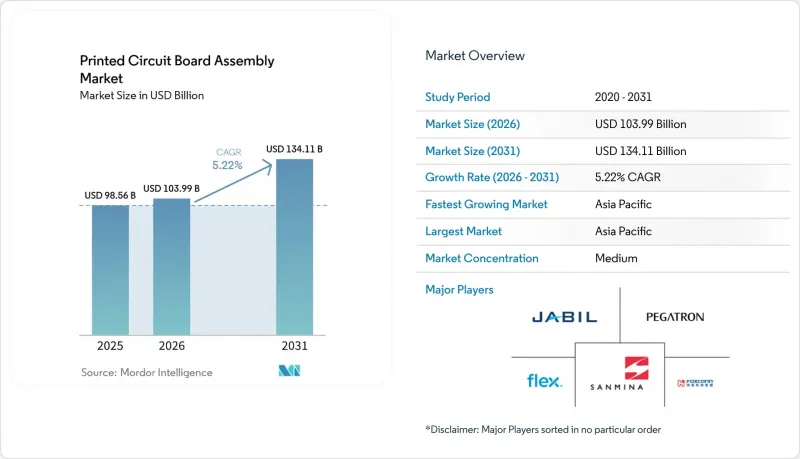

Mordor Intelligence에 의하면, 인쇄회로기판 조립 시장은 2026년에 1,039억 9,000만 달러 시장 규모로 추정되고, 2031년까지 1,341억 1,000만 달러에 이를 것으로 예측되며, 예측 기간을 통해서 CAGR 5.22%로 성장할 전망입니다.

본 보고서는 조립 유형별(표면 실장, 스루홀, 혼합 기술), 고객 참여 모델별(빌드 투 프린트, 부분 턴키, 설계 지원), 최종 사용자별(모바일 기기, 가전, 컴퓨터, 산업용, 자동차, 통신, 조명, 기타), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 인쇄회로기판 조립 시장 동향 및 인사이트

가전제품 교체 주기의 급증

구독형 업그레이드가 보급됨에 따라, 교체 주기는 2020년의 36개월에서 2025년에는 24개월로 단축되었으며, 이는 성장률을 0.8포인트 끌어올리는 효과를 가져왔습니다. 각 제조업체들은 향후 시행될 유럽연합(EU) 지침에 대응하기 위해 탈착식 배터리 설계를 채택하고 있으며, 이러한 변화로 인해 단말기 1대당 표면 실장 부품의 사용량이 15-20% 증가했습니다. 2025년에는 태블릿 출하 대수가 8% 감소했지만, 모뎀, 햅틱, 디지타이저를 더 얇은 스택으로 통합하기 위해 인쇄회로기판의 층 수는 8층에서 12층으로 증가했습니다. 폴더블 디스플레이의 보급에 따라, 20만 회 접힘을 견딜 수 있다는 인증을 받은 연질 어셈블리에 대한 수요가 증가하고 있습니다. 이러한 능력을 갖춘 전 세계의 어셈블러는 10개사 미만입니다. 이러한 동향들이 맞물리면서, 집적 밀도는 1제곱인치당 150개를 넘어섰고, 스텐실 공급업체에게는 20미크론 이하의 페이스트 공급이 요구되며, 자동 광학 검사(AOI)에 대한 수요도 증가하고 있습니다.

자동차의 급속한 전기화가 자동차용 PCB 수요를 끌어올리고 있습니다.

경차 1대당 전자 부품 탑재액은 2025년에 720달러에 달할 것으로 보이며, 배터리식 전기차의 보급이 가속화됨에 따라 2030년까지 1,100달러에 이를 것으로 예측됩니다. 최대 120개의 개별 제어 장치를 대체하는 집중형 구역 제어기를 사용하면, 어셈블리의 층 수가 16층을 초과하게 되어 순차적 적층 및 레이저 드릴링이 필요하게 됩니다. 예를 들어, BMW의 'Neue Klasse' 플랫폼에서는 통합을 통해 2027년까지 하네스의 무게를 30% 줄이는 것을 목표로 하고 있는 반면, 48볼트 아키텍처에서는 6온스의 구리박과 150 W/in²의 열을 방출하는 열 비아가 필요합니다. 따라서 각 조립 제조업체들은 -40°C에서 +125°C 범위에서 AEC-Q100 등급 1의 사이클 요건을 충족하기 위해, 질소 환경 리플로우 및 플라잉 프로브를 이용한 임피던스 검사에 대한 투자를 확대되고 있습니다. 그 결과, 인쇄회로기판 조립 시장의 연평균 성장률(CAGR)이 1.2포인트 상승했습니다.

구리 가격 변동이 제조 마진을 압박하고 있습니다.

2025년, 구리 거래 가격은 톤당 8,200달러에서 1만 400달러 사이에서 등락했으며, 이 21%의 가격 변동 폭으로 인해 제조업체의 이익률은 최대 3포인트나 압박을 받았습니다. 조립 업체들은 현재 헤지 목적으로 60일 분량의 호일 재고를 보유하고 있으며, 이는 2020년의 30일 분량에서 증가한 수치입니다. 한편, HDI 제조에 사용되는 두께 12 마이크로미터의 얇은 포일은 원자재 비용을 15% 절감하지만, 라미네이션 공정에서 포일이 찢어지기 때문에 불량률을 350ppm으로 끌어올리고 있습니다. TTM Technologies와 같은 수직 통합형 기업은 2025년에 14%의 매출총이익률을 유지한 반면, 현물 구매업체는 9%에 그쳤습니다. 구리 공급 탄력성이 개선될 때까지, 인쇄회로기판 조립 시장은 연평균 성장률(CAGR) 측면에서 0.6포인트의 하락 요인에 직면하게 될 것입니다.

부문별 분석

혼합 기술 라인은 2031년까지 연평균 성장률(CAGR) 5.63%로 확대될 것으로 예측되며, 이는 인쇄회로기판 조립 시장 전체의 평균 성장률을 상회할 것으로 전망됩니다. 스마트폰 및 태블릿 제조 과정에서 1제곱인치당 150개 이상의 부품이 실장되고 있는 만큼, 2025년 매출에서 표면 실장 공정이 차지하는 비중은 여전히 66.47%로 성장을 지속하고, 있습니다. 스루홀 기술은 진동이 20 g를 초과하고 온도 사이클이 -55°C에서 +125°C에 이르는 전력 변환 모듈 및 방위용 모듈 분야에서 여전히 널리 사용되고 있습니다. 전기차 충전 설비용 연질 PCB 어셈블리 시장 규모도 확대되고 있습니다. 이는 400 A 버스바의 경우, 납땜보다는 기계적 고정이 필요하기 때문입니다. 3D 솔더 프로파일링을 활용한 자동 검사가 점차 표준화되고 있지만, 동남아시아의 조립업체 중 이러한 시스템을 보유하고 있는 곳은 불과 30%에 그치고 있어 수율 향상에 한계가 있습니다.

압입 커넥터의 보급으로 인해 납땜된 스루홀 부품의 사용량은 연간 12% 감소하고 있지만, 80 N의 삽입력으로 인한 배럴 균열을 방지하기 위해서는 도금 두께를 40 마이크로미터 이상으로 유지해야 합니다. 동시에, 0201 메트릭보다 작은 표면 실장 부품이 스마트폰 조립의 22%를 차지하게 되면서, 스텐실의 종횡비를 1.2 이하로 낮추고, 에스케이프율을 2배로 증가시키고 있습니다. 그 결과, 혼합 기술의 도입은 신뢰성과 고밀도화의 균형을 맞추며, 인쇄회로기판 조립 시장에서 평균을 상회하는 성장 추세를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 71.82%를 차지한 것으로 평가되었으며, 2031년까지 연평균 6.72%의 성장률을 기록하며 성장세를 가속화하고 있어, 인쇄회로기판 조립 시장에서 지역별 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 중국에서는 2025년에 14억 대의 스마트폰이 조립되었으나, 광둥성의 인건비가 연평균 6% 상승하고 있어 보급형 제품 생산은 베트남이나 인도로 점차 이전되고 있습니다. 대만은 첨단 포장 공장과 인접한 지리적 이점을 활용해 하이퍼스케일러에 48시간 이내에 제품을 출하함으로써, 서버용 마더보드의 42%를 공급했습니다. 인도는 2025년에 1,180억 달러 규모의 전자기기 생산액을 기록하며, 25%의 자본 보조금을 통해 새로운 투자를 유치하고 있지만, 여전히 표면 실장 부품의 65%를 수입에 의존하고 있습니다.

일본에서는 자동차 OEM 조립이 해외로 이전됨에 따라 2025년 매출이 3% 감소했으나, 결함률을 10ppm 이하로 억제해야 하는 로봇 공학 및 이미징 조립 부문에서는 여전히 주도적인 위치를 유지하고 있습니다. 한국에서는 폴더블 스마트폰 및 자동차용 디스플레이용 연성 인쇄회로기판의 생산을 확대하고 있으며, 이 부문에서 삼성과 LG디스플레이가 전 세계 매출의 58%를 차지하고 있습니다. 동남아시아에서는 지정학적 리스크를 줄이기 위한 리쇼어링 전략을 바탕으로, 2025년에 120억 달러 규모의 전자 부문 설비 투자를 유치했습니다.

북미는 2025년에 4.2%의 성장률을 기록하며, '바이 아메리카' 조항에 따라, 의료·항공·우주용 기판 지출의 62%를 차지했습니다. 유럽에서는 자동차 산업의 침체로 인해 매출이 위축되었으나, 산업용 및 자동차용 등급 기판에 주력한 결과, 매출총이익률은 16%를 유지하며 아시아태평양 평균보다 4포인트 높은 수치를 기록했습니다. 기타 지역(주로 멕시코)은 북미 고객을 위한 니어쇼어링 거점으로 부상하며, 2025년에는 해당 지역의 인쇄회로기판 조립 시장 점유율을 6%로 끌어올렸습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the printed circuit board assembly market achieved a market size of USD 103.99 billion in 2026 and is projected to reach USD 134.11 billion by 2031, advancing at a 5.22% CAGR across the forecast period.

This report is Segmented by Assembly Type (Surface Mount, Through-Hole, and Mixed Technology), Customer Engagement Model (Build-To-Print, Partial Turnkey, and Design-Assisted), End-User (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Global Printed Circuit Board Assembly Market Trends and Insights

Surge in Consumer Electronics Refresh Cycles

Refresh intervals shortened from 36 months in 2020 to 24 months in 2025 as subscription-based upgrades gained traction, adding 0.8 percentage points to growth. Manufacturers are now adopting removable-battery designs to satisfy forthcoming European Union directives, a shift that adds 15-20% more surface-mount components per handset. Tablet shipments slipped 8% in 2025, yet printed circuit board layer counts rose from 8 to 12 to consolidate modems, haptics, and digitizers on slimmer stacks. Foldable displays are deepening demand for flexible assemblies certified to endure 200,000 folds, capabilities held by fewer than ten global assemblers. Together, these trends push placement densities beyond 150 parts per square inch, forcing stencil suppliers to deliver sub-20-micron pastes and amplifying demand for automated optical inspection.

Rapid Electrification of Vehicles Boosting Automotive PCB Demand

Electronics content per light vehicle climbed to USD 720 in 2025 and is expected to reach USD 1,100 by 2030 as battery-electric penetration accelerates. Centralized zone controllers that replace up to 120 discrete control units raise assembly layer counts above 16 and call for sequential lamination and laser drilling. BMW's Neue Klasse platform, for example, aims to slash harness weight by 30% by 2027 through consolidation, while 48-volt architectures require 6-ounce copper and thermal vias that dissipate 150 W/in2. Assemblers are therefore investing in nitrogen-atmosphere reflow and flying-probe impedance testing to meet AEC-Q100 Grade 1 cycles from -40 °C to +125 °C. The result is a 1.2-percentage-point lift to the Printed Circuit Board Assembly market CAGR.

Volatile Copper Prices Squeezing Fabrication Margins

Copper traded between USD 8,200 and USD 10,400 per ton in 2025, a 21% band that cut fabricator margins by as much as 3 points. Assemblers now carry 60 days of foil inventory to hedge, up from 30 days in 2020. Meanwhile, thinner 12-µm foils used in HDI builds lower raw-material cost 15% but push defect rates to 350 ppm because foils tear during lamination. Vertically integrated players such as TTM Technologies held 14% gross margins in 2025 versus 9% for spot buyers. Until copper supply elasticity improves, the Printed Circuit Board Assembly market faces a 0.6-point drag on CAGR.

Other drivers and restraints analyzed in the detailed report include:

- 5G Infrastructure Rollouts Accelerating HDI and RF Board Orders

- Cloud and Hyperscale Data Centers Driving High-Layer Count Server Boards

- Stringent Environmental Regulations on PCB Manufacturing Chemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mixed-technology lines are projected to expand at a 5.63% CAGR through 2031, eclipsing the overall Printed Circuit Board Assembly market average. Surface-mount processes still accounted for 66.47% of 2025 revenue, thanks to smartphone and tablet builds that top 150 placements per square inch. Through-hole remains entrenched in power-conversion and defense modules where vibration can exceed 20 g and temperature cycling spans -55 °C to +125 °C. Flexible PCB Assembly market size for electric-vehicle charging equipment is also rising, as 400 A busbars require mechanical fastening over solder. Automated inspection with 3-D solder profiling is becoming standard, yet only 30% of assemblers in Southeast Asia own such systems, limiting yield gains.

Press-fit connectors are reducing soldered through-hole volumes by 12% annually, but plating thickness must exceed 40 µm to avert barrel cracking during 80 N insertions. Simultaneously, surface-mount components smaller than 0201 metric now form 22% of smartphone placements, pushing stencil aspect ratios below 1.2 and doubling escape rates. As a result, mixed-technology adoption balances reliability with densification, reinforcing its above-average growth profile in the Printed Circuit Board Assembly market.

Complete Report Scope:

- By Assembly Type

- Surface Mount Assembly

- Through-Hole Assembly

- Mixed Technology Assembly

- By Customer Engagement Model

- Build-to-Print PCBA

- Partial Turnkey PCBA

- Design-Assisted PCBA

- By End-User

- Mobile Devices (Smartphones and Tablets)

- Consumer Electronics

- Computer (PCs/Desktop/Laptops)

- Industrial

- Automotive

- Communication

- Lighting

- Medical

- Other End-Users

- By Region

- North America

- United States

- Rest of North America

- Europe

- Germany

- United Kingdom

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Taiwan

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Rest of World

- North America

Geography Analysis

Asia-Pacific generated 71.82% of global revenue in 2025 and is accelerating at 6.72% through 2031, the fastest regional CAGR in the Printed Circuit Board Assembly market. China assembled 1.4 billion smartphones in 2025, yet entry-level production is migrating to Vietnam and India as Guangdong labor costs climb 6% per year. Taiwan supplied 42% of server motherboards, leveraging its proximity to advanced packaging fabs to achieve 48-hour shipment windows to hyperscalers. India booked USD 118 billion in electronics output in 2025 and is attracting fresh investment through 25% capital subsidies, though it still imports 65% of surface-mount components.

Japan's 2025 revenue fell 3% as automotive OEM assembly shifted abroad, yet the nation retained leadership in robotics and imaging assemblies that require defect rates below 10 ppm. South Korea is scaling flexible printed circuits for foldable phones and automotive displays, a segment where Samsung and LG Display controlled 58% of global revenue. Southeast Asia attracted USD 12 billion in electronics capex in 2025, driven by reshoring strategies to reduce geopolitical risk.

North America grew 4.2% in 2025 and now captures 62% of medical and aerospace board spend owing to Buy America provisions. Europe's automotive slump curbed revenue, yet its focus on industrial and automotive-grade boards sustained 16% gross margins, four points higher than Asia-Pacific averages. Rest of World, mainly Mexico, rose as a near-shoring hub for North American customers, lifting the region's Printed Circuit Board Assembly market share to 6% in 2025.

- Hon Hai Precision Industry Co. Ltd. (Foxconn)

- Pegatron Corporation

- Jabil Inc.

- Flex Ltd.

- Sanmina Corporation

- Celestica Inc.

- Wistron Corporation

- Compal Electronics Inc.

- Benchmark Electronics Inc.

- Plexus Corp.

- Universal Scientific Industrial Co. Ltd.

- Shenzhen Kaifa Technology Co. Ltd.

- Venture Corporation Limited

- SIIX Corporation

- Zollner Elektronik AG

- Integrated Micro-Electronics Inc.

- Lite-On Technology Corporation

- TTM Technologies Inc.

- Asteelflash Group (a USI Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Consumer Electronics Refresh Cycles

- 4.2.2 Rapid Electrification of Vehicles Boosting Automotive PCB Demand

- 4.2.3 5G Infrastructure Rollouts Accelerating HDI and RF Board Orders

- 4.2.4 Cloud and Hyperscale Data Centers Driving High-Layer Count Server Boards

- 4.2.5 Chiplet-Based Heterogeneous Integration Spurring Package Substrate Volumes

- 4.2.6 LEO Satellite Constellation Build-Outs Requiring Radiation-Hardened Boards

- 4.3 Market Restraints

- 4.3.1 Volatile Copper Prices Squeezing Fabrication Margins

- 4.3.2 Stringent Environmental Regulations on PCB Manufacturing Chemicals

- 4.3.3 Capacity Bottlenecks in ABF Resin Supply for High-End Substrates

- 4.3.4 Skilled Labor Shortages in SMT Assembly in Southeast Asia

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Assembly Type

- 5.1.1 Surface Mount Assembly

- 5.1.2 Through-Hole Assembly

- 5.1.3 Mixed Technology Assembly

- 5.2 By Customer Engagement Model

- 5.2.1 Build-to-Print PCBA

- 5.2.2 Partial Turnkey PCBA

- 5.2.3 Design-Assisted PCBA

- 5.3 By End-User

- 5.3.1 Mobile Devices (Smartphones and Tablets)

- 5.3.2 Consumer Electronics

- 5.3.3 Computer (PCs/Desktop/Laptops)

- 5.3.4 Industrial

- 5.3.5 Automotive

- 5.3.6 Communication

- 5.3.7 Lighting

- 5.3.8 Medical

- 5.3.9 Other End-Users

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Netherlands

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Taiwan

- 5.4.3.3 Japan

- 5.4.3.4 India

- 5.4.3.5 South Korea

- 5.4.3.6 Southeast Asia

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Rest of World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank, Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Hon Hai Precision Industry Co. Ltd. (Foxconn)

- 6.4.2 Pegatron Corporation

- 6.4.3 Jabil Inc.

- 6.4.4 Flex Ltd.

- 6.4.5 Sanmina Corporation

- 6.4.6 Celestica Inc.

- 6.4.7 Wistron Corporation

- 6.4.8 Compal Electronics Inc.

- 6.4.9 Benchmark Electronics Inc.

- 6.4.10 Plexus Corp.

- 6.4.11 Universal Scientific Industrial Co. Ltd.

- 6.4.12 Shenzhen Kaifa Technology Co. Ltd.

- 6.4.13 Venture Corporation Limited

- 6.4.14 SIIX Corporation

- 6.4.15 Zollner Elektronik AG

- 6.4.16 Integrated Micro-Electronics Inc.

- 6.4.17 Lite-On Technology Corporation

- 6.4.18 TTM Technologies Inc.

- 6.4.19 Asteelflash Group (a USI Company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment