|

시장보고서

상품코드

2072641

치과 충전 재료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Tooth Filling Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

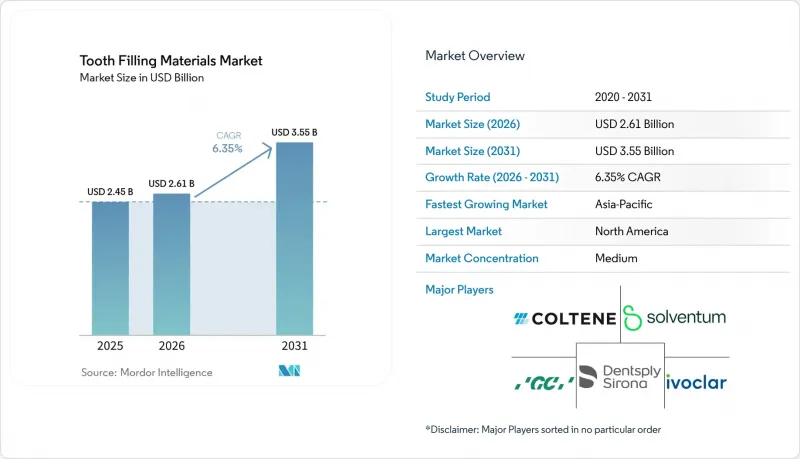

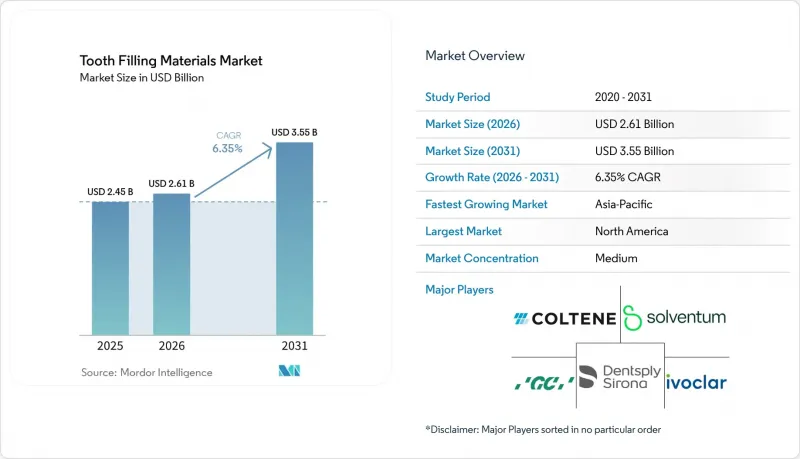

Mordor Intelligence에 의하면, 치과 충전 재료 시장 규모는 2025년 24억 5,000만 달러로 평가되었고, 2026년 26억 1,000만 달러로 추정되고, 2031년까지 35억 5,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 6.35%를 나타낼 것으로 예측됩니다.

본 보고서는 재료 유형별(복합 레진, 은 아말감, 유리 이온 마, 금 충전재, 세라믹, 기타), 충전 유형별(직접 충전, 간접 충전), 최종 사용자별(치과, 병원, 치과 기공소), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 치과 충전재 시장 동향 및 인사이트

전 세계적으로 치아 우식증으로 인한 부담이 크다는 점이 수복 치료 수요를 뒷받침하고 있습니다.

영구치의 치료되지 않은 충치는 여전히 전 세계적으로 가장 널리 퍼진 건강 문제이며, WHO 보고서에 따르면 전 세계 질병 부담(GBD) 평가를 바탕으로 약 37억 명이 그 영향을 받고 있으며, 70세가 될 때까지 24억 명의 성인이 치료되지 않은 충치를 앓고 있는 것으로 추정됩니다. 이러한 뿌리 깊은 부담으로 인해, 불소 농도가 높은 지역에서의 예방 프로그램 확대나 학교를 거점으로 한 활동 강화가 진행되는 가운데서도, 기본적인 치료 건수는 안정적인 수준을 유지하고 있습니다. 도시화와 당분이 많은 식단에 대한 접근성 확대로 인해 신흥 시장에서는 위험이 높아지고 있는 반면, 보험 적용 범위 확대와 소득 증가로 인해 더 많은 수복 치료가 가능해지고 있습니다. 대규모 국민건강보험 제도의 보험 적용 범위 미비점은 의료 서비스가 충분히 제공되지 않는 계층에서 치료 지연을 지속적으로 초래하고 있으며, 이는 의료 접근성이 개선되었을 때 글라스 아이오노머 및 직접 컴포지트의 안정적인 사용을 뒷받침하고 있습니다. 노인에 관한 연구 결과에 따르면, 미국에서는 치아 결손 및 충치 비율이 높으며, 노인의 재치료 필요성과 충치 위험을 높이는 구강 건조증을 자주 겪는 의학적으로 복잡한 환자들의 재치료 필요성이 부각되고 있습니다.

심미성이 뛰어나며, 치아 색상에 맞춘 수복물에 대한 선호도가 높아지고 있습니다.

소비자의 기대와 소셜 미디어를 통한 노출로 인해, 주변 치열과 자연스럽게 어우러지는 앞니 및 어금니 부위의 수복물에 대한 수요가 형성되고 있습니다. 간소화된 쉐이드 복합 시스템과 투과성 조절 기능의 향상으로, 바쁜 진료 현장에서 효율성과 심미성 사이의 상충 관계가 완화되고 있습니다. 예를 들어, 2025년에 도입된 Ivoclar사의 유니버설 복합레진 시스템은 설계된 투과도 변화를 활용하여 벌크 충전(bulk filling)을 가능하게 하며, 동시에 경화 후 상아질과 같은 불투명도를 구현하여 처리량이 많은 임상 일정에 적합합니다. 에나멜질과 상아질에 확실한 접착력을 갖춘 범용 접착제는 심미적인 치료 과정을 더욱 효율적으로 만들어 주며, 임상의가 다양한 임상 상황에서 예측 가능한 결과를 유지할 수 있도록 지원합니다. 치과의사들이 더 적은 SKU 수와 짧은 충전 시간으로 색조를 커버할 수 있는 시스템을 선호하게 됨에 따라, 치과 충전재 시장에서는 일반 치과 및 심미 치과 양 분야에서 심미성이 뛰어난 레진 계열 제품이 계속해서 지지를 받고 있습니다.

첨단 소재의 높은 비용과 선택적 수리에 대한 보험 급여 제한

프리미엄 복합레진, 벌크 필 시스템, CAD/CAM 가공 블록은 기본적인 대체품보다 구입 비용이 높기 때문에 공공 의료기관이나 충분한 보험에 가입하지 않은 자비 진료 환자의 경우 예산에 부담을 줄 수 있습니다. 많은 지역에서 성인 치과 보험 적용 범위에 미비한 점이 있어 가격에 대한 민감도가 높아지고 있으며, 이로 인해 임상의들은 수복 재료를 선택할 때 심미성, 속도, 단가의 균형을 고려할 수밖에 없게 되었습니다. 병원이나 지역 진료소에서는 디지털 워크플로우를 위한 설비 투자에 대해, 환자층과 각 주·지역에서 적용되는 보험 환급 제도를 고려하여 검토할 필요가 있습니다. 치과 치료가 의학적 치료와 임상적으로 관련되어 있는 경우 보험 적용을 허용하는 정책 변경은 의료 접근성 향상에 기여하지만, 이러한 적용 범위는 여전히 제한적이며, 서류 작성 요건이 행정적 부담을 가중시킬 가능성이 있습니다. 그 결과, 조달위원회는 교육을 표준화하고 낭비를 줄일 수 있는 범용 접착제나 색상 관리가 간소화된 복합재를 우선적으로 선정하는 경우가 많습니다. 그러나 비용 제약이 있는 환경에서는 첨단 간접 수복 재료의 보급이 더딘 경향이 있으며, 이것이 치과 충전재 시장의 성장을 저해하는 요인이 되고 있습니다.

부문별 분석

2025년에는 복합 레진이 42.37%의 점유율로 1위를 유지했습니다. 이는 필러 기술, 중합 화학 및 색상 체계의 단순화 분야에서 지속적인 발전이 미적 측면과 효율성을 모두 갖춘 워크플로우에 대한 임상의들의 선호를 뒷받침했기 때문입니다. 이 부문은 더 깊은 경화를 가능하게 하는 벌크 필 복합레진과, 폭넓은 적응증에서 접착 공정을 단축하는 범용 접착제의 혜택을 지속적으로 누리고 있습니다. Solventum사의 복합 레진 제품군은 응력 완화형 모노머 시스템과 최대 4.5 mm까지의 원스텝 충전 기능을 특징으로 하며, 후방 치열의 수복 시 마모 성능을 저하시키지 않으면서 진료소의 처리 능력 향상에 기여하고 있습니다. 이보클라르의 '2025' 유니버설 복합 시스템은 중합 시 투과도의 변화를 설계함으로써 색조의 조화와 중합 깊이를 향상시키고, 고출력 광중합과 결합하여 벌크 충전 과정을 신속하게 진행합니다. 이러한 설계는 SKU 수를 줄이면서도 예측 가능한 색상 매칭을 실현함으로써 일반 치과 진료의 요구를 충족시킬 뿐만 아니라, 바쁜 진료 일정 속에서도 클래스 I 및 클래스 II 시술에 대응할 수 있도록 합니다. 치과 체인(DSO)이나 그룹 진료소에서는 재고 관리와 연수를 표준화하기 위해 간소화된 색상 분류 시스템의 도입이 확대되고 있습니다.

유리 이오노머 시멘트의 경우, 나노 입자나 생체 활성 첨가제를 사용함으로써 압축 강도와 불소 방출량이 크게 개선된다는 것이 연구를 통해 밝혀졌으며, 그 역할이 확대되고 있습니다. 한 동료 심사를 거친 연구에 따르면, 이온겔 및 수산화 티타늄 첨가제를 사용했을 때, 후치부 사용에 관한 ISO 기준을 충족할 뿐만 아니라 이를 상회하는 압축 강도가 보고되었습니다. 이와 동시에, 또 다른 연구에서는 나노 실버가 도핑된 생체활성 유리 이오노머가 기존의 배합보다 더 높은 누적 불소 방출량을 보인다는 사실이 밝혀졌습니다. 이러한 특성 덕분에, 화학적 접착이나 불소 재공급의 이점을 필요로 하는 고령자나 충치 위험이 높은 환자에게 유리 이오노머는 매력적인 선택지가 되고 있습니다. 고급 간접 수복 분야에서는 리튬 디실리케이트나 하이브리드 세라믹을 이용한 인레이·온레이를 진료석에서 제작할 수 있지만, 설비 투자 비용이 높기 때문에 진료 건수가 적은 클리닉에서의 도입은 제한적입니다. 은 아말감은 전환 계획 및 재고 상황에 따라 특정 시장에서 일시적인 수요 회복이 나타나고 있지만, 규제 일정을 고려할 때 2031년까지 수은을 포함하지 않는 대안으로의 장기적인 전환이 진행될 것으로 예측됩니다.

지역별 분석

2025년, 북미는 치과 충전재 시장 점유율의 39.41%를 차지했습니다. 이는 1인당 치과 진료비 수준이 높고, 민간 보험이 널리 보급되었으며, 프리미엄 복합레진과 스캐너가 조기에 도입된 것이 수요를 뒷받침했기 때문입니다. 해당 지역에서는 수은이 포함되지 않은 재료로의 전환이 진행되고 있으며, 인디언 보건 서비스(IHS)는 연방 및 부족 의료 현장에서 2027년까지 아말감 사용을 중단하겠다는 방침을 발표함에 따라, 이에 따라 조달 및 교육이 복합 레진 및 유리 이오노머로 전환되고 있습니다. 치과 서비스 조직(DSO)은 표준 처방집과 일괄 구매를 장려하고 있으며, 이를 통해 색조가 단순화된 복합 레진 및 범용 접착제의 보급이 촉진되고 있습니다. 디지털화가 진전된 치과에서는 스캐너를 클라우드 플랫폼에 연결하여 치과 기공소와 연계를 도모하고 있지만, 진료보수제를 채택하고 있는 시설이나 지방의 진료소에서는 설비 투자 예산이 제한적이기 때문에 복합레진 치료에 직접적으로 주력하는 추세가 지속되고 있습니다.

유럽에서는 2025년까지 일상 진료에서 아말감을 퇴출시키려는 규제 움직임이 두드러졌으며, 이에 따라 공공 및 민간 의료 시스템 전반에서 복합 레진 및 글라스 아이오노머로의 전환이 가속화되고 있습니다. 서유럽에서는 예측 가능한 심미성과 시술 시간 단축을 중시하는 치과가 많아, 유니버설 접착제나 색조가 단순화된 복합 레진의 사용이 활발합니다. 의료기기의 문서화 및 시판 후 조사 요건의 이행은 여전히 공급업체 시장 진입을 좌우하고 있으며, 전문 단체들은 치과 기공소 및 맞춤형 의료기기에 대한 적절한 기대치에 대해 규제 당국과 협의하고 있습니다. 또한, 이 지역에서는 대도시권에서 체어사이드 밀링이나 CAD/CAM 워크플로가 활용되고 있지만, 소규모 치과에서는 증례의 복잡성에 따라 프레스 성형이나 밀링 가공된 세라믹에 대해 치과 기공소에 의뢰하는 경우도 있습니다.

아시아태평양은 중산층의 확대, 도시 지역의 보험 시범 사업, 그리고 임상 인프라에 대한 투자가 재활 치료 건수를 증가시킴에 따라 연평균 성장률(CAGR) 12.84%를 나타낼 것으로 전망되며, 향후 성장을 주도하고 있습니다. '미나마타 협약'에 따른 지역별 규제 시행으로 수은이 포함되지 않은 소재로의 전환이 가속화되고 있으며, 이는 폭넓은 복합재 및 접착제 제품 라인업을 보유한 공급업체들에게 유리하게 작용하고 있습니다. 일본, 호주, 한국에서는 대규모 치과에서 디지털 워크플로우 도입이 활발히 진행되고 있습니다. 한편, 동남아시아의 일부 지역에서는 공중보건 프로그램의 일환으로 지역 사회에서 글라스 아이오노머를 이용한 비침습적 수복 기술이 적용되고 있습니다. 스캐너가 널리 보급되고 있는 지역에서는 프린팅된 레진 블록 및 리튬 디실리케이트에 관한 연구를 통해 간접 오버레이에 대한 신뢰도가 높아지고 있지만, 자본 비용이 시장 계층에 따라 도입 속도를 계속해서 좌우하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the tooth filling materials market size is projected to expand from USD 2.45 billion in 2025 and USD 2.61 billion in 2026 to USD 3.55 billion by 2031, registering a CAGR of 6.35% between 2026 to 2031.

This report is Segmented by Material Type (Composite Resin, Silver Amalgam, Glass Ionomer, Gold Fillings, Ceramics, and Others), Filling Type (Direct Fillings, and Indirect Fillings), End User (Dental Clinics, Hospitals, and Dental Laboratories), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Tooth Filling Materials Market Trends and Insights

High Global Caries Burden Sustaining Restorative Demand

Untreated dental caries in permanent teeth remains the most prevalent health condition worldwide, with the WHO reporting nearly 3.7 billion people affected and 2.4 billion adults carrying untreated decay by age 70 based on Global Burden of Disease assessments. This persistent burden keeps baseline procedures steady even as preventive programs scale in high fluoridation regions and school-based initiatives expand. Urbanization and increased access to sugar-dense diets are increasing risk in emerging markets at the same time that insurance coverage and income growth enable more restorative care. Insurance gaps in large national schemes continue to delay treatment in underserved populations, which drives steady use of glass ionomer and direct composites once access improves. Evidence on older adults shows high rates of missing and decayed teeth in the United States, underscoring retreatment needs in seniors and medically complex patients who often face xerostomia, which compounds caries risk.

Rising Preference for Aesthetic, Tooth Colored Restorations

Consumer expectations and social media visibility are shaping demand for natural-looking anterior and posterior restorations that blend with surrounding dentition. Simplified shade composite systems and improved translucency control are reducing the trade-off between efficiency and esthetics in busy practices. For example, Ivoclar's universal composite system introduced in 2025 uses engineered translucency shift to support bulk placement while achieving dentin-like opacity after cure, which fits high-throughput clinical schedules. Universal adhesives with reliable bonding to enamel and dentin further streamline esthetic workflows and help clinicians maintain predictable results across variable clinical conditions. As practitioners gravitate toward systems that achieve shade coverage with fewer SKUs and shorter placement time, the tooth filling materials market continues to favor esthetic resin-based options in both general dentistry and cosmetic practices.

High Cost of Advanced Materials and Limited Reimbursement for Elective Restorations

Premium composites, bulk fill systems, and CAD/CAM milled blocks carry higher acquisition costs than basic alternatives, which can strain budgets in public clinics and among fee-for-service patients without robust insurance. Gaps in adult dental coverage in many geographies push price sensitivity, which drives clinicians to balance esthetics, speed, and unit cost when selecting restorative materials. Hospitals and community clinics must weigh capital purchases for digital workflows against the patient mix and reimbursement structures available in their states and regions. Policy changes that allow coverage where dental care is clinically linked to medical treatment can improve access, but these pathways remain narrow, and documentation requirements may add administrative burden. As a result, procurement committees often prioritize universal adhesives and simplified shade composites that standardize training and reduce wastage. However, broader adoption of advanced indirect materials can lag in cost-constrained settings, which moderates growth in the tooth-filling materials market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Innovation in Composites, Glass Ionomers, and Universal Adhesives

- Amalgam Phase Down/Ban Accelerating Shift to Mercury Free Materials

- Safety/Regulatory Scrutiny of Monomers and MDR/FDA Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Composite resin held the leading position in 2025 with 42.37% share as continuous gains in filler technology, polymerization chemistry, and shade simplification reinforced clinician preference for esthetic and efficient workflows. The segment continues to benefit from bulk fill composites that enable deeper cures and from universal adhesives that shorten bonding steps across a wide set of indications. Solventum's composite families feature stress-relieving monomer systems and single-step placement up to 4.5 mm, which helps clinics manage throughput without compromising wear performance in posterior restorations. Ivoclar's 2025 universal composite system uses a designed translucency transition during cure to improve blending and depth of cure, paired with high-output light activation to accelerate placement in bulk. These designs fit general practice needs for predictable shade matching with fewer SKUs, while also supporting Class I and Class II applications in busy appointment schedules. The tooth filling materials market sees higher adoption of simplified shade systems in DSOs and group practices that standardize inventory and training.

Glass ionomer cements are broadening their role as studies show significant improvements in compressive strength and fluoride release when nanoparticle and bioactive additives are used. One peer-reviewed study reported compressive strength that met and exceeded ISO thresholds for posterior use with ionogel and titanium hydroxide additives. At the same time, another showed nanosilver-doped bioactive glass ionomer with higher cumulative fluoride release than conventional formulations. These features make glass ionomers attractive in older adults and high caries risk patients who benefit from chemical adhesion and fluoride recharge. In premium indirect care, lithium disilicate and hybrid ceramics support inlays and onlays that can be fabricated chairside, although capital costs limit adoption in lower volume clinics. Silver amalgam shows a temporary lift in certain markets due to transition planning and inventory behavior, but regulatory timelines point to a secular shift to mercury-free options through 2031.

Complete Report Scope:

- By Material Type

- Composite Resin

- Silver Amalgam

- Glass Ionomer

- Gold Fillings

- Ceramics

- Others

- By Filling Type

- Direct Fillings

- Indirect Fillings

- By End User

- Dental Clinics

- Hospitals

- Dental Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 39.41% of the tooth filling materials market share in 2025, as high per capita dental spending, private insurance, and early adoption of premium composites and scanners sustained demand. The region continues shifting to mercury-free materials, with the Indian Health Service moving to end amalgam use by 2027 in federal and tribal care, which guides procurement and training toward composites and glass ionomers. DSOs drive standard formularies and bulk buying, which support simplified shade composites and universal adhesives. Digitally enabled practices connect scanners to cloud platforms to coordinate with labs, while fee-for-service and rural sites maintain a direct composite focus where capital budgets are limited.

Europe is defined by regulatory momentum that removed amalgam from routine care by 2025, which accelerates a transition to composites and glass ionomers across public and private systems. Adoption of universal adhesives and simplified shade composites is strong in Western Europe, where clinics favor predictable esthetics and reduced procedure time. Implementation of device documentation and post-market follow-up requirements continues to shape supplier participation, with professional organizations engaging regulators on proportionate expectations for dental labs and custom-made devices. The region also uses chairside milling and CAD/CAM workflows in metropolitan areas, though smaller clinics may pursue labs for pressed or milled ceramics depending on case complexity.

Asia-Pacific leads future expansion with a projected 12.84% CAGR as middle-class growth, urban insurance pilots, and clinical infrastructure investments lift restorative volumes. Regional enforcement aligned to the Minamata Convention reinforces a shift to mercury-free materials, which benefits suppliers with broad composite and adhesive portfolios. Japan, Australia, and South Korea maintain advanced adoption of digital workflows in larger practices. At the same time, public health programs across parts of Southeast Asia apply atraumatic restorative techniques with glass ionomers in community settings. Studies on printed resin blocks and lithium disilicate support confidence in indirect overlays where scanner penetration is rising, although capital costs continue to modulate adoption by market tier.

- BISCO, Inc.

- Coltene Holding

- DenMat Holdings, LLC

- Dentsply Sirona

- DMG Chemisch-Pharmazeutische Fabrik

- DMP Dental Industry S.A.

- Envista Holdings Corporation (Kerr Dental)

- FGM Dental Group

- GC Corporation

- Ivoclar Vivadent

- Kulzer

- Kuraray Noritake Dental Inc.

- Prime Dental Products Pvt. Ltd.

- SDI

- Shofu Inc.

- Solventum

- Tokuyama Dental

- Ultradent Products

- VITA Zahnfabrik

- VOCO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Global Caries Burden Sustaining Restorative Demand

- 4.2.2 Rising Preference for Aesthetic, Tooth-Colored Restorations

- 4.2.3 Aging Population and Greater Oral-Health Awareness Increasing Procedure Volumes

- 4.2.4 Rapid Innovation in Composites, Glass Ionomers, And Universal Adhesives

- 4.2.5 Amalgam Phase-Down/Ban Accelerating Shift to Mercury-Free Materials

- 4.2.6 Digitization Expanding Indirect Inlays/Onlays and Resin/Ceramic Blocks

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Materials and Limited Reimbursement for Elective Restorations

- 4.3.2 Safety/Regulatory Scrutiny of Monomers and MDR/FDA Compliance Burden

- 4.3.3 Polymerization Shrinkage and Technique Sensitivity Driving Secondary Caries/Retreatments

- 4.3.4 Time and Skill Intensity for Multi-Layer Esthetic Composites in Public/DSO Settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Composite Resin

- 5.1.2 Silver Amalgam

- 5.1.3 Glass Ionomer

- 5.1.4 Gold Fillings

- 5.1.5 Ceramics

- 5.1.6 Others

- 5.2 By Filling Type

- 5.2.1 Direct Fillings

- 5.2.2 Indirect Fillings

- 5.3 By End User

- 5.3.1 Dental Clinics

- 5.3.2 Hospitals

- 5.3.3 Dental Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 BISCO, Inc.

- 6.3.2 Coltene Holding AG

- 6.3.3 DenMat Holdings, LLC

- 6.3.4 Dentsply Sirona Inc.

- 6.3.5 DMG Chemisch-Pharmazeutische Fabrik GmbH

- 6.3.6 DMP Dental Industry S.A.

- 6.3.7 Envista Holdings Corporation (Kerr Dental)

- 6.3.8 FGM Dental Group

- 6.3.9 GC Corporation

- 6.3.10 Ivoclar Vivadent AG

- 6.3.11 Kulzer GmbH

- 6.3.12 Kuraray Noritake Dental Inc.

- 6.3.13 Prime Dental Products Pvt. Ltd.

- 6.3.14 SDI Limited

- 6.3.15 Shofu Inc.

- 6.3.16 Solventum

- 6.3.17 Tokuyama Dental Corporation

- 6.3.18 Ultradent Products Inc.

- 6.3.19 VITA Zahnfabrik

- 6.3.20 VOCO GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment