|

시장보고서

상품코드

2072644

미국의 생명과학 툴 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Life Science Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

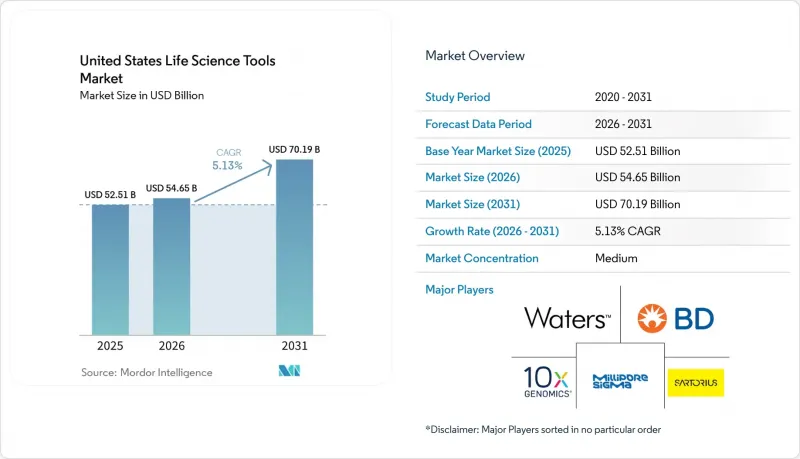

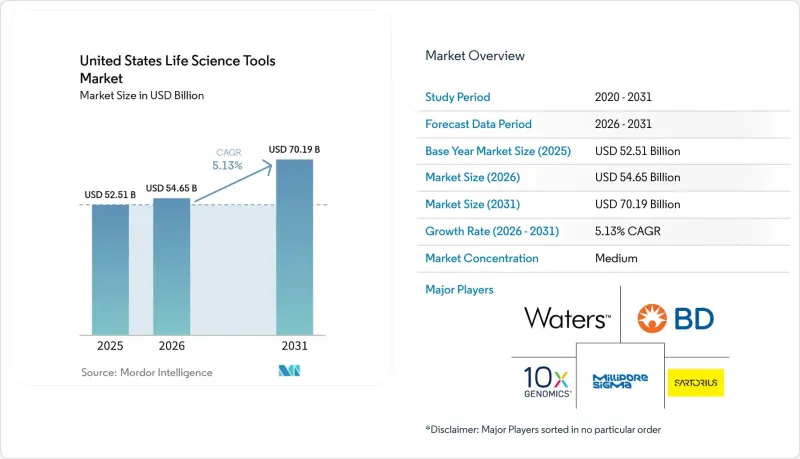

Mordor Intelligence에 의하면, 미국의 생명과학 툴 시장 규모는 2025년 525억 1,000만 달러로 평가되었고, 2026년 546억 5,000만 달러로 추정되고, 2031년까지 701억 9,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 5.13%를 나타낼 전망입니다.

본 보고서는 제품별(기기, 소모품 및 시약, 소프트웨어 및 서비스), 기술별(유전체학, 단백체학, 세포생물학, 멀티오믹스 및 공간생물학, 분석 및 분리), 용도별(신약 개발 및 의약품 개발 등), 최종 사용자별(제약 및 바이오기술 기업 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 생명과학 툴 시장 동향 및 인사이트

미국 바이오의약품 연구 개발의 활발한 정도와 파이프라인의 복잡성

미국의 생명과학 툴 시장에서는 2024년 당시와 비교해, 특히 종양학, 희귀질환 및 첨단 치료법 개발 분야에서 분석적으로 더 높은 수준의 요구 사항을 수반하는 바이오의약품 프로그램이 증가하고 있습니다. 동반 진단제의 공동 개발, 멀티오믹스를 통한 환자 군별 분류, 그리고 보다 상세한 CMC 특성 평가는 현재 많은 프로그램에서 일반적인 요건이 되고 있으며, 이로 인해 자산 1건당 사용되는 도구의 수가 증가하고 있습니다. 희귀질환 연구의 경우, 환자 코호트의 규모가 작기 때문에 단순한 처리 능력보다 샘플별 데이터 품질이 더욱 중요시되는 고감도 단백질체학 및 유전체학 워크플로가 필요하며, 이에 따른 부담이 더욱 커지고 있습니다. 신약 개발 분야의 비용 압박 또한 개발 기간을 단축하고 워크플로우의 반복을 줄일 수 있는 처리량이 더 높고 자동화가 가능한 플랫폼에 대한 수요를 촉진하고 있습니다. 이중 특이성 항체, 항체-약물 복합체(ADC), 기타 복잡한 치료법의 등장으로 인해, 미국의 생명과학 분석 장비 시장 전반에서 네이티브 질량 분석, 질량 광도법, 마이크로플루이딕스 모세관 전기영동 등 상호 보완적인 분석 기법의 활용이 확대되고 있습니다.

암 및 희귀질환 분야에서의 정밀의학 확대

정밀 의학의 상업적 확장에 따라, 미국의 생명과학 툴 시장에서 신약 개발 연구실을 넘어선 임상 유전체학 및 단백질체학 워크플로우에 대한 지속적인 수요가 발생하고 있습니다. 동반 진단의 보급은 진단약 개발 기업과 바이오의약품 기업이 규제 대응과 개발 프로세스를 보다 효율적으로 조화시키는 데 도움이 되고 있습니다. FDA의 종양학 분야 승인 관련 동료 심사를 거친 연구에 따르면, 동반 진단의 사용은 임상 개발 기간을 평균 379.5일 단축하는 것과 관련이 있는 것으로 밝혀졌으며, 이는 프로그램의 신속한 진행을 촉진하고 통합형 진단 툴셋의 가치를 높여주고 있습니다. 또한, 고감도 분자 검사에 대한 메디케어의 적용 범위도 확대되고 있으며, 2026년 5월에는 2기-3기 삼중음성 및 HER2 양성 유방암의 치료 경과 관찰에 있어 'Personalis NeXT Personal'의 적용 확대가 예정되어 있습니다. 검사 기관들이 기존 시퀀싱 플랫폼에 액체 생검 워크플로우를 통합함에 따라, 미국의 생명과학 툴 시장에서는 동일한 임상 현장에서 시약 수요의 새로운 흐름이 생겨나고 있습니다.

첨단 장비에 대한 설비 투자(CAPEX)와 소모품에 대한 지속적인 부담

미국의 생명과학 툴 시장에서 학술 기관의 핵심 시설, 병원 검사실 및 중규모 생명공학 기업을 고객으로 하는 구매자들 사이에서는 설비 투자 예산의 압박으로 인해 장비 교체 주기가 둔화되고 있습니다. 2025년 가을에 실시된 검사실 대상 구매 조사에 따르면, 81.1%의 검사실이 2026년에 들어서면서 비용 절감을 주요 운영 과제로 삼고 있으며, 81.9%는 총소유비용(TCO)을 최소화하기 위해서라면 브랜드 충성도를 포기해도 괜찮다고 응답했습니다. 이러한 추세로 인해 하드웨어 가격에 대한 압박이 커지고 있으며, 일부 이용 사례에서는 설비 투자(CAPEX)를 줄인 워크플로우나 장비가 필요 없는 워크플로우의 매력이 높아지고 있습니다. 또한, 완전히 통합된 자동화 시스템은 도입 및 검증에 오랜 시간이 소요되기 때문에 조달 주기의 장기화나 일시적인 워크플로우의 혼란을 감당할 수 없는 시설의 경우 도입이 어렵습니다. '기기로서의 서비스(IaaS)' 시약 대여와 같은 자금 조달 모델은 하이엔드 시장에서 어느 정도 효과를 거두고 있지만, 이러한 모델은 여전히 대형 공급업체와의 거래 관계에 집중되어 있어 미국 생명과학 툴 시장 전체에서 널리 활용되고 있는 것은 아닙니다.

부문별 분석

2025년, 장비는 미국 생명과학 툴 시장 점유율의 48.87%를 차지했으며, 매출 기준 최대 제품 카테고리로서의 위상을 유지했습니다. 이 위상은 바이오의약품 연구 개발(R&D) 및 제약 제조 거점에서의 크로마토그래피 시스템, 질량 분석 플랫폼, 시퀀싱 시스템, 유세포 분석기의 고부가가치 도입에 힘입어 달성되었습니다. 이 제품 카테고리 내에서 임상 실험실의 플랫폼 업그레이드와 세포 및 유전자 치료(CGT) 제조 분야의 분석 체계 확충에 따라, 질량 분석 시스템 및 시퀀싱 시스템이 가장 강력한 단위 매출 성장세를 보이고 있습니다. 또한, 액체 핸들링 시스템과 실험실 자동화 시스템 역시 고처리량의 신약 개발 환경에서 정확성과 재현성에 대한 요구가 높아짐에 따라, 중소 바이오기술 기업들이 자동화로 전환하는 추세에 발맞추어 시장 점유율을 확대되고 있습니다.

소모품 및 시약 시장은 2031년까지 연평균 성장률(CAGR) 6.98%를 나타낼 것으로 예측되며, 미국 생명과학 툴 시장에서 가장 빠르게 성장하는 제품 유형이 될 전망입니다. 이러한 추세는 장비가 이미 도입되어 종양학 검사, 세포 치료 및 멀티오믹스 워크플로우에서 더욱 빈번하게 활용됨에 따라 발생하는 지속적인 수요의 시너지 효과를 반영하고 있습니다. 시퀀싱 시약, 라이브러리 조제 키트, 항체 및 면역 시약, 세포 배양 배지는 도입 주기가 아닌 실행량과 직접 연동되기 때문에 여전히 가장 견고한 하위 카테고리로 자리 잡고 있습니다. 또한, 데이터 양이 많은 프로그램에서 바이오인포매틱스, LIMS, 워크플로우 인포매틱스의 중요성이 커짐에 따라 소프트웨어 및 서비스도 꾸준히 확대되고 있으며, 일루미나(Illumina)는 2026년 1분기 실적 설명회에서 BioInsight를 통해 이러한 방향성을 강조했습니다.

2025년 미국 생명과학 툴 시장 규모 중 단백질체학 기술이 33.83%를 차지했습니다. 이는 바이오의약품의 개발 및 품질 관리에서 질량 분석, 크로마토그래피, 그리고 면역 분석 플랫폼이 핵심적인 역할을 하고 있음을 반영합니다. 바이오의약품, 이중 특이성 항체 및 세포 치료제는 모두 개발 및 제조 단계 전반에 걸쳐 고해상도 특성 평가가 필요하며, 이는 설비 투자와 소모품에 대한 지속적인 수요를 모두 뒷받침하고 있습니다. 또한, 단백질 마이크로어레이와 면역측정법 역시 제약 기업의 연구개발 및 임상 실험실에서 계속해서 널리 활용되고 있으며, 이 부문은 안정적인 도입 기반과 지속적인 구매 패턴을 보이고 있습니다. 따라서 새로운 유전체 분석 워크플로가 급속히 확대되고 있는 상황에서도, 이 부문은 미국 생명과학 툴 시장에서 여전히 핵심적인 위치를 차지하고 있습니다.

유전체 기술은 2031년까지 연평균 성장률(CAGR) 7.46%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 기술 부문으로 꼽히고 있습니다. 시퀀싱 비용의 하락과 종양학 및 유전성 질환 검사 분야에서 임상용 NGS의 보급에 힘입어, 고객 기반은 연구 현장에서 보다 일상적인 임상 활용으로 확대되고 있습니다. 세포 생물학 기술 역시 세포 및 유전자 치료제 개발의 혜택을 받고 있으며, 특히 CDMO나 전문 제약 그룹이 활용하는 유세포 분석, 이미징, 하이컨텐츠 스크리닝 플랫폼 분야에서 그 효과가 두드러집니다. 멀티오믹스와 공간생물학은 매출 규모 면에서는 여전히 소규모이지만, 단일 세포 전사체학 및 공간 전사체학이 학술 연구에서 보다 체계화된 제약 연구개발 워크플로로 전환됨에 따라 급속히 발전하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states life science tools market size is projected to expand from USD 52.51 billion in 2025 and USD 54.65 billion in 2026 to USD 70.19 billion by 2031, registering a CAGR of 5.13% between 2026 to 2031.

This report is Segmented by Product (Instruments, Consumables and Reagents, Software and Services), Technology (Genomic, Proteomic, Cell Biology, Multi-Omics and Spatial Biology, Analytical and Separation), Application (Drug Discovery and Development, and More), and End User (Pharma and Biotech Companies, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Life Science Tools Market Trends and Insights

United States Biopharma R&D Intensity and Pipeline Complexity

The United States life science tools market is seeing more analytically demanding biopharma programs than it did in 2024, especially in oncology, rare disease, and advanced modality development. Companion diagnostic co-development, multi-omics patient stratification, and deeper CMC characterization are now common requirements for many programs, which raises the number of tools used per asset. Rare disease work adds further pressure because smaller patient cohorts require high-sensitivity proteomic and genomic workflows where data quality per sample carries greater weight than simple throughput. Cost pressure in drug development is also reinforcing demand for higher-throughput and more automatable platforms that can compress timelines and reduce workflow repetition. The rise of bispecific antibodies, antibody-drug conjugates, and other complex modalities is widening the use of orthogonal analytical methods such as native mass spectrometry, mass photometry, and microfluidic capillary electrophoresis across the United States life science tools market.

Precision Medicine Scaling Across Oncology and Rare Disease

The commercial expansion of precision medicine is creating durable demand for clinical genomic and proteomic workflows beyond discovery laboratories in the United States life science tools market. Broader use of companion diagnostics is helping diagnostic developers and biopharma companies align regulatory and development pathways more efficiently. A peer-reviewed study on FDA oncology approvals found that companion diagnostic use was associated with a mean reduction of 379.5 days in clinical development time, which supports faster program execution and raises the value of integrated diagnostic toolsets. Medicare coverage is also widening for highly sensitive molecular testing, including the May 2026 coverage expansion for Personalis NeXT Personal in Stage II-III triple-negative and HER2-positive breast cancer treatment monitoring. As laboratories layer liquid biopsy workflows onto existing sequencing platforms, the United States life science tools market is gaining a second stream of reagent demand from the same clinical site.

Advanced Instrument CAPEX and Recurring Consumables Burden

Capital budget pressure is slowing instrument refresh cycles across academic core facilities, hospital laboratories, and mid-sized biotech buyers in the United States life science tools market. A fall 2025 laboratory purchasing survey showed that 81.1% of labs entered 2026 with cost reduction as a primary operating mandate, while 81.9% said they were willing to abandon brand loyalty for the lowest total cost of ownership. This behavior is increasing hardware price pressure and making lower-CAPEX or instrument-free workflows more attractive in some use cases. Fully integrated automation systems also carry long installation and validation periods, which makes adoption harder for sites that cannot justify extended procurement cycles or temporary workflow disruption. Financing structures such as instrument-as-a-service and reagent rental are helping at the high end, but they remain concentrated among larger vendor relationships rather than broadly available across the United States life science tools market.

Other drivers and restraints analyzed in the detailed report include:

- NGS Cost Compression and Multi-Omics Throughput Gains

- Spatial Biology and Single-Cell Workflow Adoption

- Specialist Talent Shortages in Bioinformatics and Field Service

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments held 48.87% of the United States life science tools market share in 2025, which kept them as the largest product category by revenue. This position was supported by high-value placements of chromatography systems, mass spectrometry platforms, sequencing systems, and flow cytometers across biopharma R&D and pharmaceutical manufacturing sites. Within this product tier, mass spectrometry and sequencing systems are seeing the strongest unit revenue momentum as clinical laboratories upgrade platforms and CGT manufacturing expands analytical buildout. Liquid handling and lab automation systems are also gaining ground in high-throughput discovery settings where precision and reproducibility requirements are pushing smaller biotech firms toward automation.

Consumables and reagents are projected to grow at a 6.98% CAGR through 2031, making them the fastest-growing product type in the United States life science tools market. This pattern reflects the compounding effect of recurring demand once instruments are already installed and running more frequently across oncology testing, cell therapy, and multi-omics workflows. Sequencing reagents and library preparation kits, antibodies and immunoreagents, and cell culture media remain the strongest sub-categories because they are tied directly to run volume rather than placement cycles. Software and services are also expanding steadily as bioinformatics, LIMS, and workflow informatics become more important to data-heavy programs, and Illumina highlighted this direction with BioInsight in its first-quarter 2026 results commentary.

Proteomic technology accounted for 33.83% of the United States life science tools market size in 2025, reflecting the central role of mass spectrometry, chromatography, and immunoassay platforms in biologics development and quality control. Biologics, bispecific antibodies, and cell therapy products all require high-resolution characterization across development and manufacturing stages, which sustains both capital placements and recurring consumable pull-through. Protein microarrays and immunoassays also remain widely used across pharma R&D and clinical laboratories, giving this segment a stable installed base and repeat purchasing pattern. The segment, therefore, remains foundational to the United States life science tools market even as newer genomic workflows expand faster.

Genomic technology is projected to expand at a 7.46% CAGR through 2031, which makes it the fastest-growing technology segment. Falling sequencing costs and wider use of clinical NGS in oncology and genetic disease testing are broadening the customer base from research settings into more routine clinical use. Cell biology technology is also benefiting from cell and gene therapy development, especially in flow cytometry, imaging, and high-content screening platforms used by CDMOs and specialty pharma groups. Multi-omics and spatial biology remain smaller in revenue terms, but they are evolving quickly as single-cell and spatial transcriptomics move from academic research into more structured pharma R&D workflows.

Complete Report Scope:

- By Product

- Instruments

- Chromatography Systems

- Mass Spectrometry Systems

- Flow Cytometers and Cell Sorters

- Sequencing Systems

- Microscopy and Imaging Systems

- PCR and qPCR Systems

- Liquid Handling and Lab Automation Systems

- Electrophoresis and Separation Systems

- Centrifuges and Sample Preparation Systems

- Consumables and Reagents

- Assay Kits

- Antibodies and Immunoreagents

- Cell Culture Media and Sera

- Sequencing Reagents and Library Preparation Kits

- PCR Reagents and Enzymes

- Chromatography Columns and Solvents

- Sample Preparation and Purification Kits

- Microplates, Tubes, Tips and Lab Plastics

- Software and Services

- Bioinformatics and Data Analysis Software

- LIMS and Workflow Informatics

- Instrument Service and Maintenance

- Contract Assay and Research Services

- Instruments

- By Technology

- Genomic Technology

- Next-Generation Sequencing

- Sanger Sequencing

- PCR and qPCR

- Microarrays

- Digital PCR

- Proteomic Technology

- Mass Spectrometry

- Protein Microarrays

- Chromatography

- Immunoassays

- Cell Biology Technology

- Cell Culture

- Flow Cytometry

- High-Content Screening

- Imaging and Microscopy

- Cell Line Development Tools

- Multi-omics and Spatial Biology

- Single-Cell Omics

- Spatial Transcriptomics

- Spatial Proteomics

- Integrated Multi-omics Informatics

- Analytical and Separation Technology

- Spectroscopy

- Electrophoresis

- Centrifugation

- Liquid Handling and Automation

- Genomic Technology

- By Application

- Drug Discovery and Development

- Target Identification and Validation

- Hit Discovery and Screening

- Preclinical Translational Research

- CMC and Process Development Analytics

- Clinical Diagnostics and Precision Medicine

- Oncology Testing

- Rare Disease and Inherited Disease Testing

- Infectious Disease Testing

- Companion Diagnostics Development

- Academic and Government Research

- Basic Research

- Translational Research

- Core Facilities

- Bioprocessing and Advanced Therapies

- Cell Therapy Development

- Gene Therapy Development

- Biologics and Biosimilars Analytics

- Vaccine Research and Manufacturing Support

- Drug Discovery and Development

- By End User

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutes

- Hospitals and Diagnostic Laboratories

- Contract Research Organizations and CDMOs

List of Companies Covered in this Report:

- Agilent Technologies

- Beckton Dickinson

- Bio-Rad Laboratories

- Bio-Techne

- Bruker

- Danaher

- Eppendorf

- Illumina

- Merck KGaA (MilliporeSigma)

- Oxford Nanopore Technologies

- Pacific Biosciences

- QIAGEN

- Revvity

- Roche

- Sartorius

- Standard BioTools

- Thermo Fisher Scientific

- Waters Corporation

- ZEISS

- 10x Genomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 United States Biopharma R&D Intensity and Pipeline Complexity

- 4.2.2 NIH Extramural Funding and Translational Program Spend

- 4.2.3 Precision Medicine Scaling Across Oncology and Rare Disease

- 4.2.4 NGS Cost Compression and Multi-Omics Throughput Gains

- 4.2.5 Spatial Biology and Single-Cell Workflow Adoption

- 4.2.6 Trusted-Source Procurement Shifts After Biosecurity Scrutiny

- 4.3 Market Restraints

- 4.3.1 Advanced Instrument CAPEX and Recurring Consumables Burden

- 4.3.2 LDT Regulatory Phaseout Raises Validation and Compliance Costs

- 4.3.3 NIH Grant Timing Volatility for Academia-Led Purchases

- 4.3.4 Specialist Talent Shortages in Bioinformatics and Field Service

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.1.1 Chromatography Systems

- 5.1.1.2 Mass Spectrometry Systems

- 5.1.1.3 Flow Cytometers and Cell Sorters

- 5.1.1.4 Sequencing Systems

- 5.1.1.5 Microscopy and Imaging Systems

- 5.1.1.6 PCR and qPCR Systems

- 5.1.1.7 Liquid Handling and Lab Automation Systems

- 5.1.1.8 Electrophoresis and Separation Systems

- 5.1.1.9 Centrifuges and Sample Preparation Systems

- 5.1.2 Consumables and Reagents

- 5.1.2.1 Assay Kits

- 5.1.2.2 Antibodies and Immunoreagents

- 5.1.2.3 Cell Culture Media and Sera

- 5.1.2.4 Sequencing Reagents and Library Preparation Kits

- 5.1.2.5 PCR Reagents and Enzymes

- 5.1.2.6 Chromatography Columns and Solvents

- 5.1.2.7 Sample Preparation and Purification Kits

- 5.1.2.8 Microplates, Tubes, Tips and Lab Plastics

- 5.1.3 Software and Services

- 5.1.3.1 Bioinformatics and Data Analysis Software

- 5.1.3.2 LIMS and Workflow Informatics

- 5.1.3.3 Instrument Service and Maintenance

- 5.1.3.4 Contract Assay and Research Services

- 5.1.1 Instruments

- 5.2 By Technology

- 5.2.1 Genomic Technology

- 5.2.1.1 Next-Generation Sequencing

- 5.2.1.2 Sanger Sequencing

- 5.2.1.3 PCR and qPCR

- 5.2.1.4 Microarrays

- 5.2.1.5 Digital PCR

- 5.2.2 Proteomic Technology

- 5.2.2.1 Mass Spectrometry

- 5.2.2.2 Protein Microarrays

- 5.2.2.3 Chromatography

- 5.2.2.4 Immunoassays

- 5.2.3 Cell Biology Technology

- 5.2.3.1 Cell Culture

- 5.2.3.2 Flow Cytometry

- 5.2.3.3 High-Content Screening

- 5.2.3.4 Imaging and Microscopy

- 5.2.3.5 Cell Line Development Tools

- 5.2.4 Multi-omics and Spatial Biology

- 5.2.4.1 Single-Cell Omics

- 5.2.4.2 Spatial Transcriptomics

- 5.2.4.3 Spatial Proteomics

- 5.2.4.4 Integrated Multi-omics Informatics

- 5.2.5 Analytical and Separation Technology

- 5.2.5.1 Spectroscopy

- 5.2.5.2 Electrophoresis

- 5.2.5.3 Centrifugation

- 5.2.5.4 Liquid Handling and Automation

- 5.2.1 Genomic Technology

- 5.3 By Application

- 5.3.1 Drug Discovery and Development

- 5.3.1.1 Target Identification and Validation

- 5.3.1.2 Hit Discovery and Screening

- 5.3.1.3 Preclinical Translational Research

- 5.3.1.4 CMC and Process Development Analytics

- 5.3.2 Clinical Diagnostics and Precision Medicine

- 5.3.2.1 Oncology Testing

- 5.3.2.2 Rare Disease and Inherited Disease Testing

- 5.3.2.3 Infectious Disease Testing

- 5.3.2.4 Companion Diagnostics Development

- 5.3.3 Academic and Government Research

- 5.3.3.1 Basic Research

- 5.3.3.2 Translational Research

- 5.3.3.3 Core Facilities

- 5.3.4 Bioprocessing and Advanced Therapies

- 5.3.4.1 Cell Therapy Development

- 5.3.4.2 Gene Therapy Development

- 5.3.4.3 Biologics and Biosimilars Analytics

- 5.3.4.4 Vaccine Research and Manufacturing Support

- 5.3.1 Drug Discovery and Development

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Academic and Research Institutes

- 5.4.3 Hospitals and Diagnostic Laboratories

- 5.4.4 Contract Research Organizations and CDMOs

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Bio-Rad Laboratories

- 6.3.4 Bio-Techne

- 6.3.5 Bruker Corporation

- 6.3.6 Danaher Corporation

- 6.3.7 Eppendorf

- 6.3.8 Illumina

- 6.3.9 Merck KGaA (MilliporeSigma)

- 6.3.10 Oxford Nanopore Technologies

- 6.3.11 Pacific Biosciences

- 6.3.12 QIAGEN N.V.

- 6.3.13 Revvity

- 6.3.14 Roche

- 6.3.15 Sartorius AG

- 6.3.16 Standard BioTools

- 6.3.17 Thermo Fisher Scientific Inc.

- 6.3.18 Waters Corporation

- 6.3.19 ZEISS

- 6.3.20 10x Genomics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment