|

시장보고서

상품코드

2072645

미국의 벤자틴 페니실린 G 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Benzathine Penicillin G - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

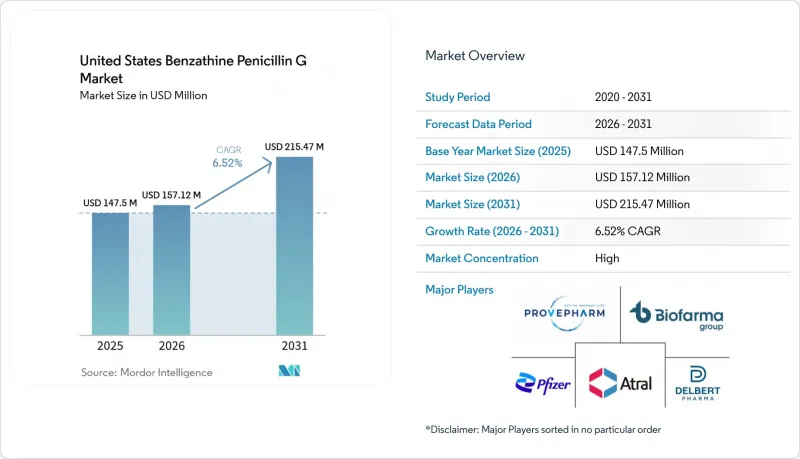

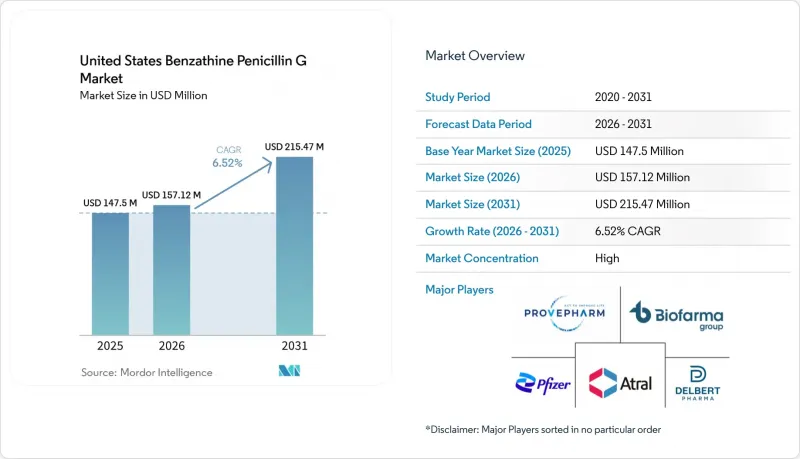

Mordor Intelligence에 의하면, 미국의 벤자틴 페니실린 G 시장 규모는 2025년에 1억 4,750만 달러로 평가되었고, 2026년에 1억 5,712만 달러로 추정되고, 2031년까지 2억 1,547만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.52%로 성장할 전망입니다.

본 보고서는 적응증별(매독 치료, 류마티스열 및 류마티스성 심장병(RHD) 예방 등), 제품 형태별(사전 충전 주사기, 분말 및 희석액), 최종 사용자별(병원, 진료소, 전문 의료 센터), 조달 채널별(도매업체, 공공 보건 입찰, 긴급 수입, 의료 기관에 대한 직접 판매)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 벤자틴 페니실린 G 시장 동향 및 분석

선천성 매독 치료의 시급성이 커지고 있습니다.

선천성 매독은 미국 내 벤자틴 페니실린 G 시장에서 여전히 가장 뚜렷한 당면 수요 요인으로 작용하고 있습니다. 이는 CDC가 2024년에 신생아 사례 약 4,000건을 보고했으며, 그 총 수가 12년 연속 증가세를 보이며 2015년 수준보다 700%나 높다고 설명했기 때문입니다. 총 사례 수는 의약품 수요를 과소평가했습니다. 왜냐하면, 확인된 영아 사례 1건마다 산모의 치료, 배우자의 치료, 그리고 추가 투여가 필요한 광범위한 산전 추적 관찰로 이어질 가능성이 있기 때문입니다. 이는 보고된 1건의 사례가 단일하고 고립된 처방이 아니라, 관련 의료 현장 전체에서 여러 차례의 치료 과정으로 이어진다는 것을 의미합니다. 가장 큰 부담을 안고 있는 곳은 남부 및 남서부 각 주이며, 이 지역들은 이미 확진자 밀도가 높은 상태여서 공중보건 프로그램에서는 대개 임산부에 대한 공급을 최우선으로 하고 있습니다. 그 결과, 제조 및 유통 과정에서 발생하는 어떠한 혼란이라도 가장 긴급한 환자에게 조기에 영향을 미치게 되며, 미국의 벤자틴 페니실린 G 시장은 산모 및 신생아 의료 수용 능력과 밀접하게 연계된 상태를 유지하고 있습니다.

성인 매독의 지속적인 환자 수와 반복 투여를 통한 잠복기 치료

2024년에는 1기 및 2기 매독 환자 수가 전년보다 감소했음에도 불구하고, 성인 매독이 여전히 미국 벤자틴 페니실린 G 시장의 광범위한 기본 수요를 뒷받침하고 있습니다. 표면상의 사례 수보다 치료의 집중도가 중요한 이유는 잠복기 및 후기 잠복기 질환의 경우 주 3회, 240만 단위의 투여가 필요하며, 이로 인해 초기 감염에 비해 환자 1인당 투여량이 훨씬 많아지기 때문입니다. 이러한 투여 패턴으로 인해 잠복 매독 사례는 수요를 견인하는 강력한 요인이 되지만, 기획 담당자가 보고된 신규 감염 사례에만 주목할 경우 이러한 경향이 간과되기 쉽습니다. 또한, 수요는 급성기 증상 치료에 비해 시스템 내 유통 속도가 느리기 때문에 재고 계획이 실제 보충 수요와 어긋날 가능성이 있습니다. 이러한 시차로 인해 품귀 현상이 장기화되면서, 가장 눈에 띄는 성매개감염증(STI) 지표가 개선되는 것처럼 보일지라도, 미국의 벤자틴 페니실린 G 시장은 계속해서 공급 부족 위험에 반복적으로 노출될 것입니다.

국내 공급원의 단일화와 장기화되는 공급 부족의 위험

미국 벤자틴 페니실린 G 시장의 가장 큰 제약 요인은 FDA 승인을 받은 국내 제조업체 1곳에 대한 의존이 계속되고 있다는 점입니다. 화이자(Pfizer)의 자회사인 킹 파마슈티컬스(King Pharmaceuticals)가 유일한 승인된 국내 공급처로 남아 있었기 때문에 2023년 4월 이후에도 공급 부족 현상이 지속되었고, 2025년 7월 리콜로 인해 중요한 프리필드 주사기 로트가 시장에서 철수되었을 때 시장 전체가 그 영향을 받기 쉬운 상황이 되었습니다. 화이자사가 2026년 1월에 발표한 최신 정보에 따르면, 도매업체 차원의 배분 제한과 주요 제형의 회복 지연이 여전히 나타나고 있으며, 이후 업데이트된 정보에서는 회복 전망이 2027년까지 더욱 연기되었습니다. 무균 주사제의 광범위한 공급 부족 현상 또한 중요한 문제입니다. 품질 문제와 낮은 이익률로 인해, 헬스케어 시스템 전반에 걸쳐 저비용 주사제공급에 반복적으로 차질이 발생해 왔기 때문입니다. 그 결과, 미국의 벤자틴 페니실린 G 시장은 의료적 수요가 존재함에도 불구하고, 치료에 필요한 투여량은 여전히 단일 공급망이 중단 없이 기능할 수 있는지 여부에 달려 있는 상황에 놓여 있습니다.

부문별 분석

2025년에는 매독 치료제가 68.31%의 점유율을 차지했으며, 미국 내 벤자틴 페니실린 G 시장의 중심적인 위치를 확고히 다졌습니다. 이러한 상황은 선천성 및 성인 매독에 대한 치료 수요가 여전히 막대함을 반영하는 것으로, CDC 보고서에 따르면 2024년에는 선천성 매독 사례가 4,000건에 육박할 것으로 예상되며, 전국적으로 성매개감염병(STI)의 부담이 계속해서 증가하고 있습니다. 또한, 매독은 임신 중에는 치료를 쉽게 미룰 수 없으며, 잠복 감염의 경우 다회 투여 요법이 필요한 경우가 많기 때문에 임상적 긴급성도 높습니다. 그 밖의 적응증 범주는 규모가 작은 것으로, 의학적으로 필수적이며 임의적인 수요와 같은 성질을 지니지 않습니다.

류마티스열 및 류마티스성 심장병의 예방 시장은 2026-2031년 연평균 성장률(CAGR) 7.38%를 나타낼 것으로 예측되며, 이는 미국 벤자틴 페니실린 G 시장에서 가장 빠르게 확대되고 있는 적응증이 될 것입니다. WHO의 2024년 지침에서는 근육 내 주사를 통한 예방 요법이 장기적인 접근법으로 권장되며, 경구 요법에 비해 재발 방지에 있어 큰 이점이 있다는 점이 재확인되었습니다. 이 부위의 증상은 매독과는 다릅니다. 환자는 수년에 걸쳐 치료를 계속해야 하며, 정기적인 간격으로 반복적으로 주사를 맞아야 하기 때문입니다. 이러한 장기적인 치료 양상으로 인해, 설령 시간이 지남에 따라 매독 환자 수 증가세가 둔화되더라도 신규 환자의 유입으로 인해 수요는 계속해서 확대될 것입니다.

2025년에는 프리필드 주사기가 73.24%의 점유율을 차지했으며, 미국 벤자틴 페니실린 G 시장에서 여전히 주류 제형으로 자리매김했습니다. 이러한 우위는 의료진의 익숙함, 투여의 신속성, 그리고 바쁜 임상 현장에서의 조제 부담 경감에서 비롯되었습니다. 그러나 2025년 리콜로 인해 중요한 프리필드 주사기 로트가 시장에서 철수되면서, 단일 제형 및 단일 국내 공급원에 대한 과도한 의존이 초래하는 위험이 드러남에 따라 그 우위는 약화되었습니다. 또한, 이번 리콜 기간을 계기로 신뢰할 수 있는 공급을 확보할 수 있다면, 재구성이 필요한 제형의 사용에 대해 더 많은 의료 제공업체들이 그 타당성을 재검토하게 되었습니다.

현탁액용 분말 및 희석액은 2026-2031년 연평균 성장률(CAGR) 8.52%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 제품 부문이 될 것입니다. FDA의 집행 재량에 따라, 이 제형의 '엑스텐실린' 그리고 '렌토실린'이 국내에 도입됨에 따라, 2024년 이전에는 존재하지 않았던 실용적인 공급 경로가 확립되었습니다. 대량 사용을 하는 공중보건 시설이 재편에 점차 적응해 감에 따라, 업무상의 부담도 관리하기 쉬워지고 있습니다. 이를 통해 일부 국내산 주사기공급이 회복된 후에도 미국 벤자틴 페니실린 G 시장의 제형 다양화가 지속적으로 뒷받침될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states benzathine penicillin g market size is projected to be USD 147.5 million in 2025, USD 157.12 million in 2026, and reach USD 215.47 million by 2031, growing at a CAGR of 6.52% from 2026 to 2031.

This report is Segmented by Indication (Syphilis Treatment, Rheumatic Fever & RHD Prophylaxis, and More), Product Presentation (Prefilled Syringe, Powder and Diluent), End User (Hospitals, Clinics, Specialty Care Centers), and Procurement Channel (Wholesaler, Public Health Tenders, Emergency Import, Direct Institutional). Market Forecasts are Provided in Terms of Value (USD).

United States Benzathine Penicillin G Market Trends and Insights

Rising Congenital Syphilis Treatment Urgency

Congenital syphilis remains the clearest immediate demand trigger in the United States benzathine penicillin G market because the CDC reported nearly 4,000 newborn cases in 2024 and described that total as the twelfth straight annual increase and 700% above 2015 levels. The case total understates drug demand because every confirmed infant case can also lead to maternal treatment, partner treatment, and broader prenatal follow-up that consumes additional doses. This means that one reported event can translate into several treatment courses across connected care settings rather than a single isolated prescription. The heaviest pressure falls on Southern and Southwestern states, where case intensity is already high and public health programs often direct supply toward pregnant patients first. As a result, any disruption in manufacturing or allocation reaches the most urgent patients early and keeps the United States benzathine penicillin G market tightly linked to maternal and neonatal care capacity.

Persistent Adult Syphilis Caseload And Repeat-Dose Latent Therapy

The adult syphilis burden still supports broad baseline demand in the United States benzathine penicillin G market even though primary and secondary syphilis declined in 2024 from the prior year. Treatment intensity matters more than headline case counts because latent and late-latent disease require three weekly doses of 2.4 million units, which creates much higher volume per patient than early-stage infection. This dosing pattern turns latent cases into a strong volume driver that can remain hidden when planners focus only on reported incident infections. Demand also moves through the system more slowly than it does for acute symptomatic care, which can leave inventory planning out of step with actual refill needs. That lag helps sustain shortage conditions and keeps the United States benzathine penicillin G market exposed to repeat stress even when the most visible STI indicators appear to improve.

Single-Source Domestic Supply And Prolonged Shortage Risk

The largest restraint on the United States benzathine penicillin G market is the continued reliance on one FDA-approved domestic manufacturer. Pfizer's King Pharmaceuticals subsidiary remained the sole approved domestic source, which left the entire market exposed when shortage cycles persisted after April 2023 and when the July 2025 recall removed critical prefilled syringe lots from circulation. Pfizer's January 2026 update still showed allocation at the wholesaler level and delayed recovery for key presentations, and later updates extended recovery expectations further into 2027. The wider sterile injectable shortage pattern also matters because quality failures and limited margins have repeatedly disrupted low-cost injectable drugs across the healthcare system. That leaves the United States benzathine penicillin G market in a position where medical need exists, but treatable volume still depends on whether one supply chain can perform without interruption.

Other drivers and restraints analyzed in the detailed report include:

- Need For Long-Acting Rheumatic Fever Prophylaxis

- Temporary Import Pathways Expand Powder-Format Demand

- Sterile Injectable Manufacturing And Cold-Chain Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Syphilis treatment accounted for 68.31% share in 2025, which kept it firmly at the center of the United States benzathine penicillin G market. That position reflects the continued scale of congenital and adult syphilis treatment need, with the CDC reporting nearly 4,000 congenital syphilis cases in 2024 and continued national STI pressure. Syphilis also has high clinical urgency because treatment cannot be delayed easily in pregnancy and latent infection often requires multi-dose therapy. Other indication categories remain smaller, but they are still medically necessary and do not behave like discretionary demand.

Rheumatic fever and rheumatic heart disease prophylaxis is projected to grow at 7.38% CAGR through 2026-2031, making it the fastest-expanding indication in the United States benzathine penicillin G market. WHO's 2024 guidance reinforced intramuscular prophylaxis as the preferred long-term approach and a strong recurrence advantage over oral therapy. This segment grows differently from syphilis because patients can remain on therapy for years and require repeated injections at regular intervals. That long-duration pattern means new patient starts continue to build demand even if syphilis case growth becomes less severe over time.

Prefilled syringes captured 73.24% share in 2025 and remained the dominant presentation within the United States benzathine penicillin G market. Their lead came from provider familiarity, faster administration, and lower preparation burden in busy clinical settings. That advantage was weakened by the 2025 recall, which removed important prefilled lots and exposed the risk of relying too heavily on one format and one domestic source. The recall period also pushed more providers to reassess their willingness to use formats that require reconstitution if that meant securing reliable supply.

Powder and diluent for suspension is projected to grow at 8.52% CAGR through 2026-2031, which makes it the fastest-growing product segment. FDA enforcement discretion brought Extencilline and Lentocilin into the country in this format, creating a practical supply path that had not existed before 2024. As high-volume public health sites gain more comfort with reconstitution, the workflow penalty becomes easier to manage. That supports lasting format diversification in the United States benzathine penicillin G market even after some domestic syringe supply returns.

Complete Report Scope:

- By Indication

- Syphilis treatment

- Rheumatic fever and rheumatic heart disease prophylaxis

- Group A streptococcal infections

- Other Indications

- By Product Presentation

- Prefilled syringe

- Powder and diluent for suspension

- By End User

- Hospitals

- Clinics

- Specialty Care Centers

- By Procurement Channel

- Wholesaler procurement

- State and local public-health tenders

- Emergency import channels

- Direct institutional contracting

List of Companies Covered in this Report:

- AdvaCare

- Biopharma S.r.l.

- Centurion Healthcare

- CSPC Holdings Company Limited

- GNH India Pharmaceuticals Limited

- Laboratoires Delbert

- Laboratorios Atral

- Lavina Pharmaceuticals Pvt. Ltd.

- Lifechem Healthcare

- Orofino Pharmaceuticals Group

- Pfizer

- Provepharm

- Reyoung Pharmaceutical Co., Ltd.

- Shanghai Trifecta Pharma Co. Ltd.

- SiNi Pharma Pvt. Ltd.

- Wellona Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising congenital syphilis treatment urgency

- 4.2.2 Persistent adult syphilis caseload and repeat-dose latent therapy

- 4.2.3 Need for long-acting rheumatic fever prophylaxis

- 4.2.4 Temporary import pathways expand powder-format demand

- 4.2.5 Public-health buffer stocking and direct clinic procurement

- 4.3 Market Restraints

- 4.3.1 Single-source domestic supply and prolonged shortage risk

- 4.3.2 Sterile injectable manufacturing and cold-chain complexity

- 4.3.3 Powder reconstitution workflow slows imported-product uptake

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Industry rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Indication

- 5.1.1 Syphilis treatment

- 5.1.2 Rheumatic fever and rheumatic heart disease prophylaxis

- 5.1.3 Group A streptococcal infections

- 5.1.4 Other Indications

- 5.2 By Product Presentation

- 5.2.1 Prefilled syringe

- 5.2.2 Powder and diluent for suspension

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Specialty Care Centers

- 5.4 By Procurement Channel

- 5.4.1 Wholesaler procurement

- 5.4.2 State and local public-health tenders

- 5.4.3 Emergency import channels

- 5.4.4 Direct institutional contracting

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AdvaCare Pharma

- 6.3.2 Biopharma S.r.l.

- 6.3.3 Centurion Healthcare

- 6.3.4 CSPC Holdings Company Limited

- 6.3.5 GNH India Pharmaceuticals Limited

- 6.3.6 Laboratoires Delbert

- 6.3.7 Laboratorios Atral

- 6.3.8 Lavina Pharmaceuticals Pvt. Ltd.

- 6.3.9 Lifechem Healthcare

- 6.3.10 Orofino Pharmaceuticals Group

- 6.3.11 Pfizer Inc.

- 6.3.12 Provepharm

- 6.3.13 Reyoung Pharmaceutical Co., Ltd.

- 6.3.14 Shanghai Trifecta Pharma Co. Ltd.

- 6.3.15 SiNi Pharma Pvt. Ltd.

- 6.3.16 Wellona Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment