|

시장보고서

상품코드

2072651

미국의 단백질 표지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Protein Labeling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

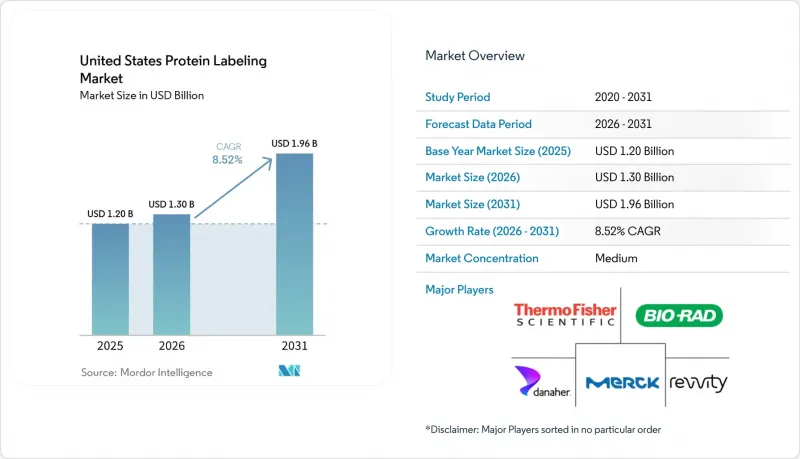

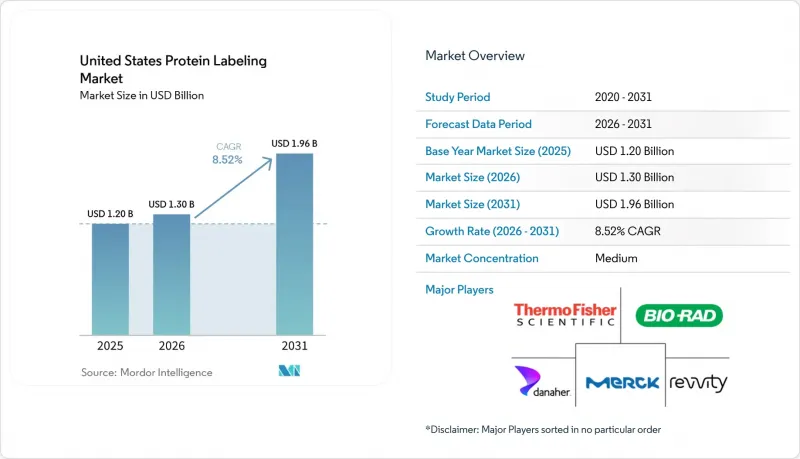

Mordor Intelligence에 의하면, 미국의 단백질 표지 시장 규모는 2025년에 12억 달러로 평가되었고, 2026년 13억 달러로 추정되고, 2031년까지 19억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.52%를 나타낼 전망입니다.

본 보고서는 제품별(시약 및 키트, 서비스, 소모품), 용도별(면역학적 기술, 세포 기반 분석법, 형광 현미경법, 단백질 마이크로어레이, 질량 분석법), 표지법별(in vitro, in vivo), 최종 사용자별(제약 및 바이오기술, CDMO, 학술 기관, 임상 진단실험실)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 단백질 표지 시장 동향 및 인사이트

단백질체학 및 멀티오믹스 파이프라인의 확대

단백질체학는 전이 연구 프로그램 전반에 걸쳐 집단 규모의 단백질 프로파일링이 운영상 실현 가능해짐에 따라, 단순한 구상 단계를 벗어나고 있습니다. 2026년에 발표된 UltraPlex-TMT는 직교 프로테아제 분해를 통한 58-plex 의사 멀티플렉스 분석을 가능하게 하며, 추가 장비 없이 단 한 번의 LC-MS 분석으로 처리할 수 있는 시료 수를 늘려줍니다. 이러한 처리량 향상으로 인해 동일한 시간 내에 더 많은 샘플에 태그를 지정하고 처리할 수 있게 되므로, 각 캠페인에서 사용되는 표지 시약 세트의 수가 증가합니다. 또한, 질량 분석에 의한 측정 전에 농도가 낮은 표적 물질을 분리하는 데 도움이 되는 비오틴화 프로브나 가교제 등의 친화성 농축 물질에 대한 수요도 증가할 것입니다. 멀티오믹스 프로그램에서는 단백질체학 분석 결과가 유전체학 및 대사체학 분석 전반에 걸쳐 호환성을 가져야 할 뿐만 아니라, 서로 직교하는 화학적 처리가 필요하기 때문에 시약 사용량이 더욱 증가합니다. 써모피셔 사이언티피크가 2026년에 출시할 예정인 'Orbitrap Tribrid Apex'에는 생 스펙트럼 데이터를 대규모로 실용적인 단백질체학 분석 결과로 변환하는 AI 탑재 소프트웨어가 추가되었으며, 이에 따라 미국 단백질 표지 시장에서 고순도 시약의 역할이 더욱 중요해지고 있습니다.

ADC 및 표적 단백질 분해 워크플로우에서의 활용 확대

ADC의 개발로 인해 단백질 표지화는 단순한 일상적인 분석 공정에서 벗어나, 많은 의약품 개발 프로그램에서 정밀한 제조 요건으로 변화했습니다. 론자는 2026년 2월, GlycoConnect, HydraSpace, toxSYN을 하나의 'Advanced Synthesis' 플랫폼에 통합하고, 해당 스택을 듀얼 페이로드 ADC 형식으로 확장했습니다. 이는 차세대 구조체에서 결합이 얼마나 엄격하게 정의되게 되었는지를 보여줍니다. 이러한 변화가 중요한 이유는 현재 약물-항체 비율 조절과 결합 부위의 정의가 후기 개발의 핵심 요소로 자리 잡고 있으며, 규제 환경 하에서 무작위 표지 화학 기술의 상업적 중요성이 감소하고 있기 때문입니다. 표적 단백질 분해의 경우, 생세포 분석에서 세포 내 결합을 확인하기 위해 각 분해 효소의 설계에 따라 E3 리가아제 모집 모듈과 표적 결합 모듈에 각각 별도의 표지 처리가 필요하기 때문에 새로운 수요가 발생하고 있습니다. 따라서 단일 프로그램 내에서 부위 특이적 결합 키트, 형광 프로브 및 질량 태그 정량 시약을 순차적으로가 아니라 병행하여 사용할 수 있게 됩니다. 이러한 방식을 통해 조달 주기가 단축되고, 미국 단백질 표지 시장 전반에 걸쳐 공급업체와의 관계가 더욱 지속 가능한 형태로 발전하게 됩니다.

고분해능 질량 분석 워크플로우의 높은 비용

고분해능 정량 단백질체학에는 여전히 많은 학술 기관과 임상 실험실에서 감당하기 어려운 비용 부담이 존재합니다. Orbitrap이나 비행시간형(TOF) 장비는 대당 50만-150만 달러가 들며, 완전한 도입을 위해서는 고가의 표지 키트, 크로마토그래피 시스템 및 전용 소프트웨어도 필요합니다. 이러한 비용 구조 때문에 많은 기관들은 얻을 수 있는 정보는 적지만 초기 투자 비용이 적게 드는 웨스턴 블롯이나 ELISA와 같은 분석 방식에 머물러 있습니다. 이러한 제약은 장비 구입 후에도 계속되고 있으며, 차세대 멀티플렉스 태그 키트의 경우 여전히 실험당 비용이 상당하기 때문에 실험 실시 빈도가 줄어들 가능성이 있습니다. 또한, 생물정보학 담당자의 부족도 걸림돌이 되고 있습니다. 복잡한 DIA(직접 면역 분석법)의 결과 데이터를 신속하게 해석하지 못하면, 시약에 대한 투자의 가치가 떨어지기 때문입니다. 이러한 제약으로 인해 저예산 부문의 지출이 억제되면서, 미국의 단백질 표지 시장에서 학계의 폭넓은 관심이 전체 워크플로우 도입으로 이어지는 속도가 둔화되고 있습니다.

부문별 분석

2025년, 시약 및 키트는 미국 단백질 표지 시장의 70.31%를 차지했으며, 해당 시장에서 주도적인 위치를 확립했습니다. 이러한 규모는 면역측정법, 단백질체학 플랫폼 및 바이오의약품 품질관리 연구소에서 표준화된 키트 프로토콜이 실험의 변동성을 줄여줌으로써, 해당 기술들이 널리 정착되어 활용되고 있음을 반영하고 있습니다. 또한, 실험 실패가 막대한 비용으로 이어지는 경우, 연구소에서는 신뢰성이 높은 형광증백제, 비오틴 포획 시스템, 매스 태그 키트를 선호하여 사용하기 때문에 브랜드의 신뢰성도 가격 책정을 뒷받침하고 있습니다. 소모품은 표지 처리 후의 과정을 뒷받침하는 정제 컬럼, 젤, 플레이트 포맷을 통해 유사한 워크플로우에 기여하고 있습니다. 소모품의 가격 결정력은 비교적 낮은 편이지만, 재주문 패턴은 시료 처리량에 연동되어 있어 미국 단백질 표지 업계에서 계속해서 중요한 위치를 차지하고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 10.38%로 확대될 것으로 예상되며, 미국 단백질 표지 시장에서 가장 빠르게 성장하는 제품 부문이 될 전망입니다. GenScript사는 2026년 5월에 'TurboCHO 단백질 발현 키트'를 출시했습니다. 이 키트는 3-5일 만에 결과를 확인할 수 있으며, 경쟁 제품에 비해 수확량이 최대 5배 더 높습니다. 이는 서비스 구매자가 외부 위탁 파트너에게 단순한 개별 공정의 수행뿐만 아니라 신약 개발 일정을 단축해 줄 것을 기대하고 있는 현 상황을 반영하고 있습니다. 바이오오르토고날법이나 부위 특이적법 등의 기법을 사내에서 수행하기가 어려워짐에 따라, 맞춤형 접합 의뢰는 지속적인 프로그램 계약으로 전환되고 있습니다. 이러한 변화로 인해 서비스 수익은 단기적인 수요 변동의 영향을 덜 받게 되었으며, 전문 서비스 제공업체들은 높은 이익률을 유지할 여지가 생겼습니다.

2025년, 면역학 기법은 미국 단백질 표지 시장의 34.24%를 차지했으며, 해당 시장에서 가장 큰 응용 분야로서의 위상을 유지했습니다. ELISA, 웨스턴 블롯 및 면역조직화학은 확립된 실험실 표준 작업 절차(SOP), 병리 검사 루틴 및 로트 승인 시험 시스템에 통합되어 있어 여전히 견고한 입지를 유지하고 있습니다. 이러한 기존 도입 기반의 효과로 인해, 새로운 측정법이 주목을 받더라도 대체는 제한적인 수준에 그치고 있습니다. 질량 분석법도 중요한 위치를 차지하고 있지만, 그 확산은 도입에 걸림돌이 되는 장비 및 정보 처리 비용에 의해 제한받고 있습니다. 형광 현미경법이나 단백질 마이크로어레이는 국소화 연구나 다중 프로파일링 분야의 특정 틈새 시장에서 계속해서 활용되고 있으며, 시스템 업그레이드나 플랫폼 업데이트 주기에 연동된 안정적인 수요가 예상됩니다.

세포 기반 분석법은 2031년까지 연평균 성장률(CAGR) 10.52%를 나타낼 것으로 예측되며, 이는 각 용도 분야 중 가장 빠른 성장 속도로서, 미국의 단백질 표지 시장을 더 많은 생물학적 시스템 워크플로로 확대하게 될 것입니다. 머크(Merck)와 프로메가(Promega)는 Duolink 근접 리게이션 분석 기술과 HiBIT 스플릿 루시페라제 리포터를 결합하여, 3D 세포 모델에서 단백질 간 상호작용을 검출함과 동시에 표적 단백질의 수준을 정량할 수 있는 시스템을 개발했습니다. 또한, 조직 모델의 경우 단순한 표면 염색이 아닌 체적 표지 기법이 필요하기 때문에 오가노이드 기반 시험에 대한 수요도 증가하고 있습니다. 이러한 요건으로 인해, 표준 키트로는 충분히 충족되지 않는 고품질 세포 투과성 프로브 및 효소 태그 시장이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 맟 향후 전망

AJYAccording to Mordor Intelligence, the united states protein labeling market size was valued at USD 1.20 billion in 2025 and is estimated to grow from USD 1.30 billion in 2026 to reach USD 1.96 billion by 2031, at a CAGR of 8.52% during the forecast period (2026-2031).

This report is Segmented by Product (Reagents and Kits, Services, Consumables), Application (Immunological Techniques, Cell-Based Assays, Fluorescence Microscopy, Protein Microarrays, Mass Spectrometry), Labeling Method (In-Vitro, In-Vivo), and End User (Pharma and Biotech, Crdmos, Academic Institutes, Clinical Diagnostics Labs). The Market Forecasts are Provided in Terms of Value (USD).

United States Protein Labeling Market Trends and Insights

Expansion of Proteomics and Multi-Omics Pipelines

Proteomics is moving past an aspirational phase because population-scale protein profiling is becoming operationally feasible across translational research programs. UltraPlex-TMT, published in 2026, enables 58-plex pseudo-multiplexed analysis through orthogonal protease digestion, which lifts the number of samples handled in one LC-MS run without extra instrumentation. That throughput shift increases the number of labeling reagent sets used in each campaign because more samples can be tagged and processed in the same time window. It also raises demand for affinity enrichment materials such as biotinylated probes and crosslinkers that help isolate low-abundance targets before mass spectrometry readout. Multi-omics programs further increase reagent intensity because proteomic outputs need compatible and orthogonal chemistries across genomic and metabolomic assays. Thermo Fisher Scientific's 2026 Orbitrap Tribrid Apex launch adds AI-enabled software that converts raw spectra into usable proteomic readouts at scale, which deepens the role of high-purity reagents in the US protein labeling market.

Growing Use in ADC and Targeted Protein Degradation Workflows

ADC development has changed protein labeling from a routine analytical step into a precision manufacturing requirement across many drug programs. Lonza integrated GlycoConnect, HydraSpace, and toxSYN into one Advanced Synthesis platform in February 2026 and expanded the stack to dual-payload ADC formats, which shows how tightly defined conjugation has become for next-generation constructs. This shift matters because drug-to-antibody ratio control and conjugation site definition are now central to late-stage development, which reduces the commercial relevance of random-labeling chemistries in regulated settings. Targeted protein degradation adds a second demand stream because each degrader design requires separate labeling of the E3 ligase recruiting and target-binding modules to confirm cellular engagement in live-cell assays. A single program can therefore consume site-specific conjugation kits, fluorescent probes, and mass-tag quantification reagents in parallel rather than one after another. That pattern shortens procurement cycles and makes supplier relationships more durable across the US protein labeling market.

High Cost of High-Resolution Mass Spectrometry Workflows

High-resolution quantitative proteomics still carries a cost base that many academic and clinical labs cannot absorb. Orbitrap and time-of-flight instruments cost USD 500,000 to USD 1.5 million per unit, and full deployment also requires premium labeling kits, chromatography systems, and specialized software. That cost profile keeps many institutions on western blot and ELISA workflows that generate less information but require lower up-front spending. The limitation continues after instrument purchase because next-generation multiplex tag kits still carry meaningful per-experiment costs that can reduce run frequency. A shortage of bioinformatic staff adds another barrier because reagent investments are less valuable when complex DIA outputs cannot be interpreted quickly. This restraint caps spending in lower-budget segments and slows the pace at which the US protein labeling market can convert broad academic interest into full-workflow adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Outsourcing of Complex Conjugation to CROs and CDMOs

- Shift Toward Site-Specific and Bioorthogonal Labeling

- Regulatory Complexity for Radio-Isotope Conjugates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and Kits captured 70.31% of US protein labeling market share in 2025, which gave them the leading position in the US protein labeling market. Their scale reflects entrenched use across immunoassays, proteomics platforms, and biopharmaceutical quality control laboratories where standardized kit protocols reduce experimental variability. Brand validation also supports pricing because laboratories often prefer trusted fluorescent dyes, biotin capture systems, and mass-tag kits when failed runs are costly. Consumables serve the same workflows through purification columns, gels, and plate formats that support processing after labeling. Even though consumables carry less pricing power, their reorder pattern stays tied to sample throughput and keeps them important inside the US protein labeling industry.

Services are projected to expand at a 10.38% CAGR through 2031, making them the fastest-growing product segment in the US protein labeling market. GenScript launched the TurboCHO Protein Expression Kit in May 2026 with output in 3 to 5 days and yields up to 5 times higher than competing formats, reflecting how service buyers now expect outsourced partners to reduce discovery timelines rather than only execute isolated steps. As bioorthogonal and site-specific methods become harder to run internally, custom conjugation orders are increasingly turning into recurring program agreements. That shift makes service revenue less exposed to short-term demand swings and gives specialist providers room to sustain premium margins.

Immunological Techniques accounted for 34.24% of the US protein labeling market size in 2025, which kept them as the largest application area in the US protein labeling market. ELISA, western blot, and immunohistochemistry remain durable because they sit inside established laboratory SOPs, pathology routines, and lot-release testing systems. That installed-base effect limits substitution even as newer readouts gain visibility. Mass spectrometry also holds a meaningful place, but its expansion is moderated by instrument and informatics costs already weighing on adoption. Fluorescence microscopy and protein microarrays continue to serve specific niches in localization studies and multiplex profiling with steady demand tied to system upgrades and platform refresh cycles.

Cell-based Assays are projected to grow at a 10.52% CAGR through 2031, which gives them the fastest pace within applications and expands the US protein labeling market into more live-system workflows. Merck and Promega combined Duolink proximity ligation assay technology with HiBIT split-luciferase reporters, creating a system that can detect protein-protein interactions and quantify target protein levels in 3D cell models. Organoid-based testing is also adding demand because tissue-like models need volumetric labeling approaches rather than simple surface staining. That requirement opens space for premium cell-permeant probes and enzymatic tags that standard kits do not address well.

Complete Report Scope:

- By Product

- Reagents and Kits

- Services

- Consumables

- By Application

- Immunological Techniques

- Cell-based Assays

- Fluorescence Microscopy

- Protein Microarrays

- Mass Spectrometry

- By Labeling Method

- In-vitro Labeling

- In-vivo Labeling

- By End User

- Pharmaceutical and Biotechnology Companies

- Contract Research and Development / Manufacturing Organizations

- Academic and Research Institutes

- Clinical Diagnostics Laboratories

List of Companies Covered in this Report:

- Abcam

- Agilent Technologies

- Bio-Rad Laboratories

- Bio-Techne

- Biotium Inc.

- Cell Signaling Technology

- Creative Diagnostics

- Danaher

- Roche

- Genscript

- LI-COR Biosciences

- Lonza Group

- Lumiprobe Corporation

- Merck

- New England Biolabs

- Promega

- Proteintech Group

- Revvity Inc.

- Sartorius

- Takara Bio

- Thermo Fisher Scientific

- Vector Laboratories

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of proteomics and multi-omics pipelines

- 4.2.2 Growing use in ADC and targeted protein degradation workflows

- 4.2.3 Rising outsourcing of complex conjugation to CROs and CDMOs

- 4.2.4 Shift toward site-specific and bioorthogonal labeling

- 4.2.5 AI-assisted probe design for multiplex imaging

- 4.2.6 Single-day organ-scale in-tissue labeling platforms

- 4.3 Market Restraints

- 4.3.1 High cost of high-resolution mass spectrometry workflows

- 4.3.2 Regulatory complexity for radio-isotope conjugates

- 4.3.3 Dye stability and cold-chain burden

- 4.3.4 Large-tag steric hindrance and localization artifacts

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Reagents and Kits

- 5.1.2 Services

- 5.1.3 Consumables

- 5.2 By Application

- 5.2.1 Immunological Techniques

- 5.2.2 Cell-based Assays

- 5.2.3 Fluorescence Microscopy

- 5.2.4 Protein Microarrays

- 5.2.5 Mass Spectrometry

- 5.3 By Labeling Method

- 5.3.1 In-vitro Labeling

- 5.3.2 In-vivo Labeling

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Contract Research and Development / Manufacturing Organizations

- 5.4.3 Academic and Research Institutes

- 5.4.4 Clinical Diagnostics Laboratories

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abcam plc

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Bio-Rad Laboratories Inc.

- 6.3.4 Bio-Techne Corporation

- 6.3.5 Biotium Inc.

- 6.3.6 Cell Signaling Technology

- 6.3.7 Creative Diagnostics

- 6.3.8 Danaher Corporation

- 6.3.9 F. Hoffmann-La Roche Ltd.

- 6.3.10 GenScript Biotech Corporation

- 6.3.11 LI-COR Biosciences

- 6.3.12 Lonza Group AG

- 6.3.13 Lumiprobe Corporation

- 6.3.14 Merck KGaA

- 6.3.15 New England Biolabs Inc.

- 6.3.16 Promega Corporation

- 6.3.17 Proteintech Group

- 6.3.18 Revvity Inc.

- 6.3.19 Sartorius AG

- 6.3.20 Takara Bio Inc.

- 6.3.21 Thermo Fisher Scientific Inc.

- 6.3.22 Vector Laboratories Inc.

- 6.3.23 WuXi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-Need Assessment