|

시장보고서

상품코드

2072653

인도의 미들 마일 배송 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Middle Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

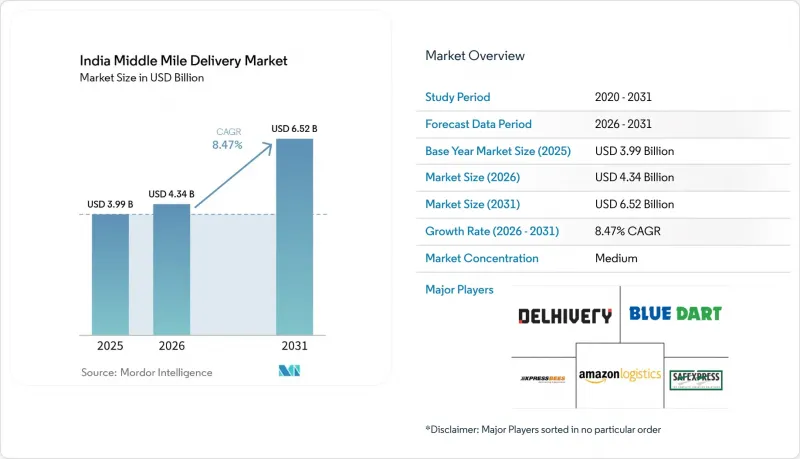

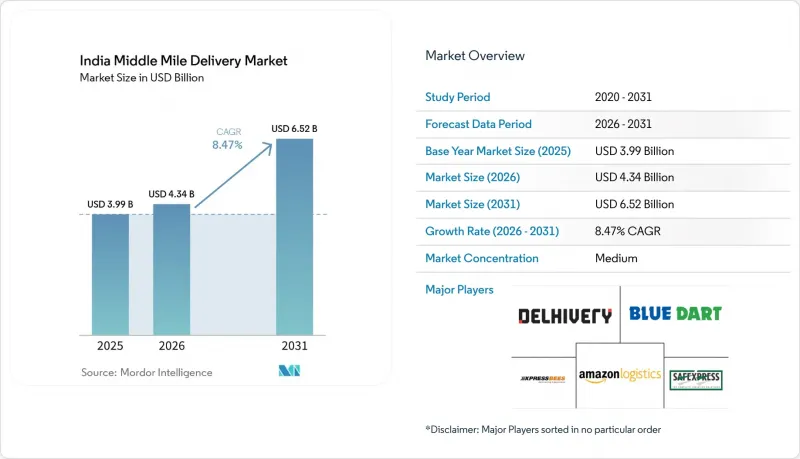

Mordor Intelligence에 의하면, 인도의 미들 마일 배송 시장 규모는 2025년에 39억 9,000만 달러로 평가되었고, 2026년 43억 4,000만 달러로 추정되고, 2031년까지 65억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.47%를 나타낼 전망입니다.

본 보고서는 운송 수단별(도로, 철도, 항공 등), 비즈니스 모델별(B2B, B2C, C2C), 온도 관리별(온도 관리 유무), 배송지별(국내 및 국제), 최종 사용자 산업별(전자상거래, 패션 등) 및 지역별(북부, 중부 등)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

인도의 미들 마일 배송 시장 동향 및 인사이트

국가 물류 정책과 '가티 샤크티'인프라 추진

인도의 미들 마일 배송 시장은 운송 회랑, 산업 클러스터, 물류 거점을 통합한 조율된 공공 프레임워크로 연결하는 계획 시스템의 혜택을 받고 있습니다. 'PM 가티 샤크티' 57개 부처와 1,700개 이상의 데이터 레이어를 통합하여, 기존의 경로 결정 방식보다 더욱 견고한 공간적 기반을 바탕으로 한 화물 계획을 가능하게 하고 있습니다. '통합 물류 인터페이스 플랫폼'은 44개의 정부 시스템을 연계하고 1,700개 이상의 등록 기업에 서비스를 제공함으로써, 다양한 운송 수단을 아우르는 화물의 실시간 가시성을 높이고 있습니다. 인프라와 데이터 시스템이 같은 방향으로 나아감으로써 경로 계획, 업무 인계, 회랑 선정이 용이해지므로, 이는 미들마일 운영에 있어 중요합니다. 이러한 지정 회랑을 따라 허브나 장거리 운송 자산을 배치하는 사업자는 멀티모달 파크나 회랑과 연결된 시설이 본격적으로 가동됨에 따라 비용 면에서 우위를 유지할 가능성이 높을 것입니다.

전자상거래 및 퀵커머스 배송 붐

인도의 미들 마일 배송 시장은 소포 운송이 몇년전보다 더 대규모로, 더 빈번하게 이루어지게 되었습니다는 사실로부터도 혜택을 보고 있습니다. 전자상거래와 퀵커머스의 부상으로 인해, 기존의 소포 운송보다 더 엄격한 서비스 시간 범위 내에서 허브로의 빈번한 보충, 짧은 주기로 이루어지는 분류, 도시 간 운송에 대한 수요가 증가하고 있습니다. 이로 인해 자동화의 경제성이 변화하고 있습니다. 왜냐하면 지방 도시의 허브에서는 더 빠른 분류 작업과 더 규칙적인 간선 운송 일정을 정당화할 수 있을 만큼의 소포 처리량이 확보되게 되었기 때문입니다. 또한, 수요가 최대 규모를 자랑하는 대도시권을 넘어 확대됨에 따라 사업자들은 Tier 2 및 Tier 3 회랑의 더 깊은 곳까지 운송 역량을 배치할 수밖에 없게 되었으며, 이에 따라 네트워크 설계에도 변화가 생기고 있습니다. 그 결과, 시장은 더 이상 출하량 증가뿐만 아니라, 더 고밀도화된 네트워크를 통해 규모가 더 작고 시간적 제약이 엄격한 화물을 운송해야 할 필요성에 의해서도 견인되고 있습니다.

분산된 트럭 운송 인프라와 운전기사 부족

인도의 미들 마일 배송 시장은 여전히, 피크 시간대에 운송 능력을 얼마나 신속하게 확대할 수 있는지를 제한하는 인력 및 차량 조직과 관련된 구조적인 문제에 직면해 있습니다. 핵심적인 문제는 자격을 갖춘 운전자의 부족뿐만 아니라, 차량의 상당 부분이 자금 조달, 교육, 디지털 시스템 이용 기회가 고르지 않은 소규모 사업자들 사이에 분산되어 있다는 사실에도 있습니다. 따라서 출하 수요가 급증할 경우, 사업자는 신중한 대응을 할 수밖에 없거나, 유휴 자산 및 인건비 증가를 감수해야 하게 되어 처리 능력 확대가 어려워집니다. 또한 배기가스 규제, 안전 시스템, 노선 관리 기술 등의 규정 준수 수준 향상도 뒤처지고 있어, 체계적으로 운영되는 화주들은 서비스 계약의 일환으로 이러한 개선을 점점 더 기대하고 있습니다. 이러한 상황으로 인해 서비스 품질에 편차가 발생하고 있으며, 인도 미들 마일 배송 시장의 일부에서는 운송 경로의 개선이 완전히 신뢰할 수 있는 운영 성과로 이어지지 못하고 있는 것이 현실입니다.

부문별 분석

2025년, 인도의 미들 마일 배송 시장에서 도로 운송은 69.73%의 점유율을 차지했으며, 다른 운송 수단을 크게 앞질렀습니다. 이러한 주도적 지위는 총 연장 146,572km에 달하며, 산업 회랑과 소비 회랑을 가로지르는 유연한 허브 간 이동을 지속적으로 뒷받침하고 있는 인도의 국도망 규모에서 비롯된 것입니다. 인도의 미들 마일 배송 시장에서 광범위한 지리적 커버리지, 불규칙한 화물 크기, 혹은 철도나 항공으로는 같은 수준의 편의성으로 대응할 수 없는 '도어 투 허브'의 유연성이 요구되는 운송의 경우, 여전히 도로 운송이 기본적인 운송 수단으로 자리 잡고 있습니다. 이는 순수한 운송 경로의 속도보다 운송 빈도가 더 중요한 단거리 운송이나 지역 내 운송에서 특히 해당됩니다.

항공 운송은 2031년까지 인도의 미들 마일 배송 시장 규모에서 10.10%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 시간적 확실성을 중시하는 의약품, 신선식품 및 국경을 넘는 화물에 대한 수요가 증가하고 있음을 반영합니다. 철도는 운행 일정의 신뢰성과 장거리 수송의 경제성 덕분에, 회랑 기반의 화물 수송에 유리한 분야에서 입지를 넓혀가고 있습니다. 2026년 서부 전용 화물 회랑이 완공됨에 따라, 단일 구간의 배송 유연성보다는 간선 수송의 효율성과 혼잡 완화가 중시되는 노선에서 철도의 역할은 더욱 강화될 것입니다. 해운 활동은 여전히 항만 주도형 및 연안 산업 클러스터에 의존하고 있기 때문에 그 역할이 광범위하게 미치기보다는 특정 지역에 집중되어 있습니다.

2025년 인도의 미들 마일 배송 시장 규모 중 B2C가 72.03%를 차지했으며, 이는 전자상거래 플랫폼과 퀵커머스 사업자들이 체계적인 소포 운송에 미치는 영향의 규모를 반영하고 있습니다. 이 모델은 표준화된 포장, 고정 노선, 허브 간 빈번한 운행, 그리고 매우 대규모의 전체 출하량에 걸쳐 자동화 비용을 분산할 수 있다는 장점이 있습니다. 이러한 운영상의 특징 덕분에 B2C 부문은 고밀도 분류 네트워크와 정기적인 간선 운송 일정을 가장 효과적으로 활용할 수 있는 분야가 되었습니다. B2B는 제조업, FMCG(일용소비재) 및 정식 유통 계약을 통해 안정적인 화물 수요의 기반을 마련해 주기 때문에 여전히 중요하며, 사업자들이 전자상거래의 계절적 변동을 상쇄하는 데 도움이 되고 있습니다.

C2C는 가장 빠르게 성장하고 있는 비즈니스 모델로, 2031년까지 연평균 성장률(CAGR) 10.22%로 확대될 것으로 전망됩니다. 이러한 변화는 리커머스, 소셜 셀링, 그리고 P2P 소포 배송과 밀접한 관련이 있으며, 이러한 분야는 점점 더 체계화되고 디지털 네트워크를 통해 경로 설정이 용이해지고 있습니다. 인도의 미들 마일 배송 업계에서 이는 리버스 플로우, 소량 소포 운송, 그리고 다방향 운송이 이전보다 더욱 중요해지고 있음을 의미합니다. B2C 순방향 운송만을 염두에 두고 네트워크를 구축해 온 사업자는 반품, 분류, 경로 변경에 대한 처리 능력을 강화하기 위해 허브를 재설계해야 할 가능성이 있습니다. 인도 미들 마일 배송 업계에서 이 분야는 여전히 B2C보다 규모는 작지만, 전국적인 소포 네트워크의 활용 사례를 확대한다는 점에서 구조적으로 중요한 위치를 차지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the india middle-mile delivery market size was valued at USD 3.99 billion in 2025 and is estimated to grow from USD 4.34 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 8.47% during the forecast period (2026-2031).

This report is Segmented by Transportation Mode (Road, Rail, Air, and More), by Business Model (B2B, B2C, and C2C), by Temperature Control (Temperature-Controlled and Non-Temperature-Controlled), by Destination (Domestic and International), by End-User Industry (E-Commerce, Fashion, and More), and by Region (North, Central, and More). The Market Size and Forecasts are Provided in Terms of Value (USD).

India Middle Mile Delivery Market Trends and Insights

National Logistics Policy and Gati Shakti Infrastructure Push

The India middle-mile delivery market is benefiting from a planning system that now links transport corridors, industrial clusters, and logistics nodes into a coordinated public framework. PM Gati Shakti integrates 57 ministries and more than 1,700 data layers, enabling freight planning with a stronger spatial basis than earlier corridor decisions. The Unified Logistics Interface Platform connects 44 government systems and serves more than 1,700 registered companies, improving real-time cargo visibility across transport modes. This matters for middle-mile operations because route planning, handoffs, and corridor selection become easier when infrastructure and data systems move in the same direction. Operators that place hubs and linehaul assets along these designated corridors are likely to maintain a cost advantage as more multimodal parks and corridor-linked facilities enter full use.

E-Commerce and Quick-Commerce Shipment Boom

The India middle-mile delivery market is also benefiting from the fact that parcel movement now occurs in larger, more frequent waves than it did a few years ago. E-commerce and quick commerce are increasing the need for repeat-hub replenishment, short-cycle sortation, and intercity transfers operating within tighter service windows than conventional parcel movement. This is changing the economics of automation because secondary-city hubs now have enough parcel density to justify faster sortation and more regular linehaul schedules. It is also shifting network design, since demand is moving beyond the largest metros and forcing operators to place capacity deeper into Tier-2 and Tier-3 corridors. As a result, the market is no longer driven only by shipment growth, but also by the need to move smaller, more time-sensitive consignments through a denser network.

Fragmented Trucking Base and Driver Shortage

The India middle-mile delivery market still faces a structural labor and fleet-organizational problem that limits how quickly capacity can scale during peak periods. The core issue is not only the shortage of qualified drivers, but also the fact that a large share of the fleet remains dispersed across small operators with uneven access to finance, training, and digital systems. That makes throughput harder to scale when shipment demand rises quickly, because operators either commit cautiously or carry higher idle-asset and labor costs. It also slows compliance upgrades in emissions, safety systems, and route technology, which organized shippers increasingly expect as part of service contracts. This keeps service quality uneven and prevents some parts of the India middle-mile delivery market from converting corridor upgrades into fully reliable operational performance.

Other drivers and restraints analyzed in the detailed report include:

- Dedicated Freight Corridors Cut Rail Transit Cost/Time

- AI-/IoT-Enabled Visibility and Optimization Platforms

- Fuel-Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Roadways held 69.73% of the India middle-mile delivery market share in 2025, leaving them far ahead of other transport modes. That leadership came from the scale of India's national highway system, which reached 146,572 km and continues to support flexible hub-to-hub movement across industrial and consumption corridors. In the Indian middle-mile delivery market, road remains the default mode for shipments that require broad geographic reach, irregular consignment sizes, or door-to-hub flexibility that rail and air cannot match with the same ease. This is especially relevant for short-haul and intra-regional transfers, where shipment frequency matters more than pure corridor speed.

Airways is set to record the fastest India middle-mile delivery market size CAGR at 10.10% through 2031, reflecting stronger demand from pharmaceutical, perishable, and cross-border freight that places a premium on time certainty. Railways are gaining ground where schedule reliability and long-haul economics now favor corridor-based freight movement. The completion of the Western dedicated freight corridor in 2026 gives rail a stronger role on routes where linehaul efficiency and less congestion matter more than one-leg delivery flexibility. Maritime activity remains tied to port-led and coastal industrial clusters, so its role is concentrated rather than broad.

B2C accounted for 72.03% of the India middle-mile delivery market size in 2025, reflecting the scale that e-commerce platforms and quick-commerce players now bring to organized parcel movement. This model benefits from standardized packaging, repeat routes, frequent inter-hub runs, and the ability to spread automation cost across very large shipment pools. Those operating features make B2C the segment that most clearly rewards dense sortation networks and repeat linehaul schedules. B2B remains important because it anchors steady freight demand from manufacturing, FMCG, and formal distribution contracts, helping operators balance e-commerce seasonality.

C2C is the fastest-growing business model and is projected to expand at a 10.22% CAGR through 2031. The change is tied to recommerce, social selling, and peer-to-peer parcel movement, which are becoming more formal and easier to route through digital networks. In the India middle-mile delivery industry, that means reverse flows, small-batch parcel transfers, and mixed-direction movement are becoming more relevant than before. Operators that built networks only around forward B2C movement may need to redesign hubs to handle more returns, grading, and rerouting capacity. This part of the India middle-mile delivery industry is still smaller than B2C, but it is structurally important because it widens the use cases for national parcel networks.

Complete Report Scope:

- By Transportation Mode

- Roadways

- Railways

- Airways

- Maritime

- By Business Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Customer-to-Consumer (C2C)

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Destination

- Domestics

- International

- By End User Industry

- E-commerce Retail

- Fashion and Lifestyle

- Beauty, Wellness and Personal Care

- Home and Furniture

- Consumer Electronics and Appliances

- Healthcare and Medical Supplies

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- Delhivery

- Blue Dart Express

- Amazon Transportation Services

- XpressBees

- Safexpress

- Ekart Logistics

- TCI Express

- Gati (Allcargo Group)

- Mahindra Logistics

- DHL Supply Chain India

- VRL Logistics

- DTDC Express

- FedEx India

- TVS Supply Chain Solutions

- CJ Darcl Logistics

- Om Logistics Ltd.

- Navata Road Transport

- Nitco Logistics

- BlackBuck

- Rivigo

- LetsTransport

- ElasticRun

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Logistics Policy and Gati Shakti Infrastructure Push

- 4.2.2 E-Commerce and Quick-Commerce Shipment Boom

- 4.2.3 Dedicated Freight Corridors Cut Rail Transit Cost/Time

- 4.2.4 AI-/IoT-Enabled Visibility and Optimization Platforms

- 4.2.5 MSME LTL Cluster Aggregators Unlocking New Volumes

- 4.2.6 Renewable-Powered Cold-Chain Hubs Lowering OPEX

- 4.3 Market Restraints

- 4.3.1 Fragmented Trucking Base and Driver Shortage

- 4.3.2 Fuel-Price Volatility Squeezing Margins

- 4.3.3 Ramp-Up Bottlenecks at Multimodal Logistics Parks

- 4.3.4 Cold-Chain Compliance Gaps Causing Spoilage Penalties

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Insights on Warehousing & Distribution Centers

- 4.9 Insights on Refrigerated Middle-Mile Delivery

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Transportation Mode

- 5.1.1 Roadways

- 5.1.2 Railways

- 5.1.3 Airways

- 5.1.4 Maritime

- 5.2 By Business Model

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.2.3 Customer-to-Consumer (C2C)

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Destination

- 5.4.1 Domestics

- 5.4.2 International

- 5.5 By End User Industry

- 5.5.1 E-commerce Retail

- 5.5.2 Fashion and Lifestyle

- 5.5.3 Beauty, Wellness and Personal Care

- 5.5.4 Home and Furniture

- 5.5.5 Consumer Electronics and Appliances

- 5.5.6 Healthcare and Medical Supplies

- 5.5.7 Others

- 5.6 By Region

- 5.6.1 North

- 5.6.2 Central

- 5.6.3 West

- 5.6.4 East

- 5.6.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Delhivery

- 6.4.2 Blue Dart Express

- 6.4.3 Amazon Transportation Services

- 6.4.4 XpressBees

- 6.4.5 Safexpress

- 6.4.6 Ekart Logistics

- 6.4.7 TCI Express

- 6.4.8 Gati (Allcargo Group)

- 6.4.9 Mahindra Logistics

- 6.4.10 DHL Supply Chain India

- 6.4.11 VRL Logistics

- 6.4.12 DTDC Express

- 6.4.13 FedEx India

- 6.4.14 TVS Supply Chain Solutions

- 6.4.15 CJ Darcl Logistics

- 6.4.16 Om Logistics Ltd.

- 6.4.17 Navata Road Transport

- 6.4.18 Nitco Logistics

- 6.4.19 BlackBuck

- 6.4.20 Rivigo

- 6.4.21 LetsTransport

- 6.4.22 ElasticRun

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment