|

시장보고서

상품코드

2072696

미국의 진료 관리 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Practice Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

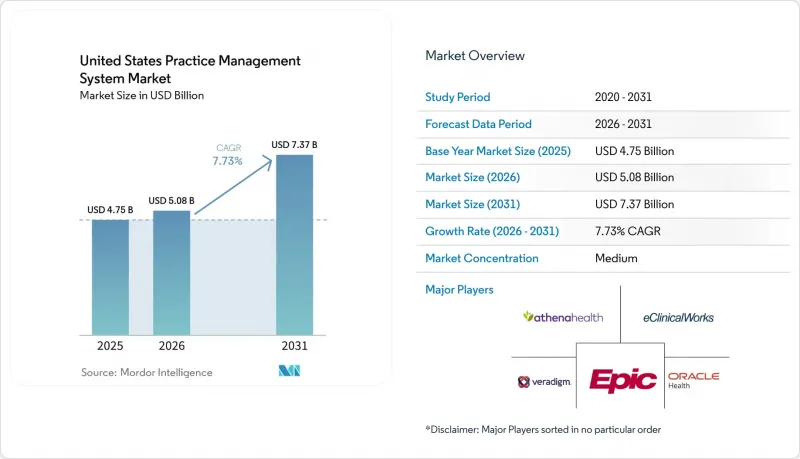

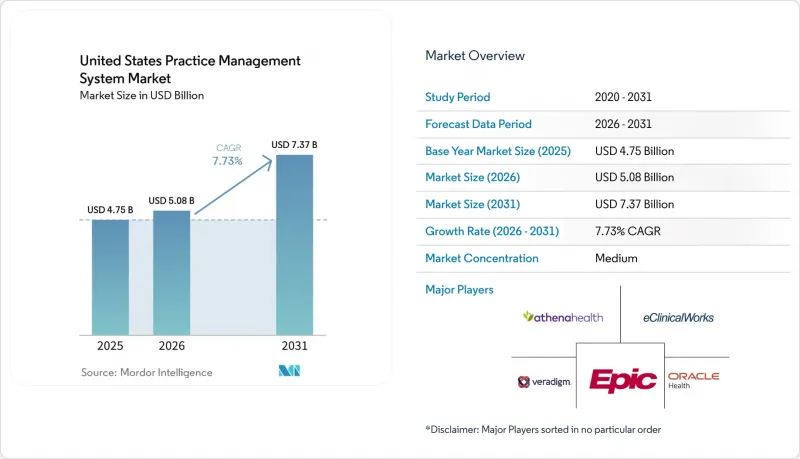

Mordor Intelligence에 의하면, 미국의 진료 관리 시스템 시장 규모는 2025년 47억 5,000만 달러로 평가되었고, 2026년 50억 8,000만 달러로 추정되고, 2031년까지 73억 7,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 7.73%를 나타낼 전망입니다.

본 보고서는 제품별(통합형, 독립형), 구성 요소별(소프트웨어, 서비스), 제공 방식별(웹 기반, 클라우드 기반/SaaS, On-Premise), 기능별(일정 관리, 청구, 사전 승인, 진료 기록, 분석, 환자 참여 유도, 원격 의료, 전자 처방), 최종 사용자별(진료소, 병원, 검사 기관, 약국, 외래 진료)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

미국의 진료 관리 시스템 시장 동향 및 인사이트

관리 비용과 보험 청구 거절로 인해 현 상태를 유지하기가 어려워지고 있습니다.

미국의 진료 관리 시스템 시장은 의료 제공업체가 파편화된 도구만으로는 관리하기가 현저히 어려워진 청구 환경에 의해 형성되고 있습니다. Kodiak Solutions의 보고서에 따르면, 2025년에는 미국 전역의 병원에서 최종 청구 거절 및 부실채권으로 인한 순수익 손실이 484억 달러에 달했고, 2024년의 386억 달러에서 증가했습니다. 한편, 최종 청구 기각률의 중앙값은 2.5%에서 2.7%로 상승했습니다. 또한 Premier의 보고서에 따르면, 청구 심사에 드는 비용은 의료기관 기준으로 257억 달러에 달하며, 그중 180억 달러는 잠재적으로 불필요한 지출이라고 합니다. 이는 지불 주기에서 여전히 얼마나 많은 피할 수 있는 재작업이 남아 있는지를 보여줍니다. 그 결과, 의료기관에서는 수급 자격 확인, 청구서 제출 전 데이터 검토, 코딩 지원, 그리고 지급 회수와 직접적으로 연결되는 미승인 방지 기능에 더 높은 우선순위를 두고 있습니다. 이것이 바로 청구, 코딩 및 청구 관리가 미국 진료 관리 시스템 시장에서 여전히 가장 중요한 기능 영역으로 남아 있는 이유이며, 공급업체들이 측정 가능한 수익 회수를 핵심 가치 제안으로 내세우는 경향이 강해지고 있는 이유이기도 합니다.

통합형 EHR-PM-RCM 제품군이 플랫폼의 구매 단위를 재정의합니다.

미국의 진료 관리 시스템 시장은 통합된 관리·임상 플랫폼으로 전환되고 있습니다. 이는 의료 제공업체가 예약, 진료 기록, 수익 사이클 업무 전반에 걸쳐 데이터 인계 및 대조 과정의 지연을 줄이고자 하기 때문입니다. 2025년에는 통합형 진료 관리 시스템이 매출의 61.9%를 차지했는데, 이는 구매자들이 이미 독립형 단일 기능 제품보다 광범위한 제품군을 선호하고 있음을 뒷받침합니다. Epic은 HIMSS 2026에서 청구 및 청구 기각 방지를 위한 'Penny'에 더해, 메인 플랫폼의 외부가 아닌 내부에 통합된 에이전트 기반 워크플로우 도구를 선보이며 그 방향성을 제시했습니다. athenahealth도 2026년 봄의 'athenaOne' 릴리스에서는 내장형 수익 주기 개선 기능을 확충하고, 연동된 워크플로우 및 정기적인 플랫폼 수준 업그레이드를 향한 이러한 전환을 강화했습니다. 실용적인 관점에서 볼 때, 이 통합 모델을 통해 데이터의 중복 입력이 줄어들고, 환자 데이터와 청구 데이터가 단일 운영 계층으로 통합될 뿐만 아니라, 조달 시 상호 운용성 준비 상태를 보다 쉽게 평가할 수 있게 됩니다.

이전 비용과 워크플로우의 혼란이 시스템 업데이트 주기에 큰 부담이 되고 있습니다.

시스템 업데이트 가속화를 저해하는 주요 요인은 가동 중인 관리 업무를 한 시스템에서 다른 시스템으로 이전할 때 발생하는 시간과 업무상의 혼란입니다. 현재, 도입 작업은 단순한 소프트웨어 설치에 그치지 않습니다. 의료 기관에서는 완전한 전환을 실시하기 전에 데이터 정제, 워크플로우 재설계, 직원 재교육, 보험사 규정 조정 및 병행 운영 기간이 필요한 경우가 많기 때문입니다. 이러한 부담은 사내 프로젝트 팀을 갖추지 않았거나, 운영 개시 기간 동안 청구 업무를 처리할 여력이 없는 독립 의료기관이나 지역 운영 사업자에게 특히 큰 과제가 되고 있습니다. 2031년까지 연평균 9.3%의 성장이 예상되는 서비스의 급속한 확대는 많은 구매자들이 사내 팀에만 의존하지 않고 외부 도입 지원, 교육 및 수익 주기 관리 지원에 비용을 투자하고 있음을 보여줍니다. 이는 단기적으로는 구매를 위축시키는 한편, 미국 진료 관리 시스템 시장공급업체들이 지속적인 수익을 올릴 수 있게 하는 요인이 되고 있습니다.

부문별 분석

통합형 진료 관리 시스템은 2025년에 매출의 61.87%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 8.25%로 확대될 것으로 전망되어, 제품 옵션 중 가장 큰 시장 규모와 가장 강력한 성장세를 모두 갖추고 있습니다. 제품 측면에서는 의료 제공업체들이 예약 관리, 진료 기록 연동, 청구 절차, 환자와의 소통을 하나의 시스템에서 처리하기를 원하고 있기 때문에 이 부문은 현재 미국 진료 관리 시스템 시장에서 가장 뚜렷한 중심축을 이루고 있습니다. 의료 시스템이나 대규모 의사 단체는 여전히 단일 공급업체의 운영 환경을 선호하기 때문에 EHR 및 EMR 통합 시스템은 이 그룹 내에서 가장 큰 점유율을 계속 차지하고 있습니다. 또한, 의료 제공업체들이 청구 정보의 수집, 편집 및 미승인 관리를 프런트엔드의 접수 업무나 백엔드의 수금 업무와 더욱 긴밀하게 연계하고자 함에 따라, 수익 주기 통합형 제품의 인기도 높아지고 있습니다. 디지털 방식의 환자 접수, 진료비 견적, 셀프 서비스 워크플로가 선택적 기능에서 일상적인 관리 업무로 전환됨에 따라, 환자 참여 통합 도구의 중요성이 커지고 있습니다. 또한, 의료 제공 현장 전반에서 상호 운용성에 대한 기대가 계속 높아지는 가운데, 전자 처방전의 통합도 표준 기능으로 자리 잡아가고 있습니다.

이러한 경향은 미국 진료 관리 시스템 업계가 상호 연동이 되지 않는 소프트웨어 스택에 대한 용인 수준을 점차 낮추고 있다는 관점을 뒷받침하고 있습니다. Epic, athenahealth, eClinicalWorks, Veradigm은 모두 워크플로우의 적용 범위를 확대하는 데 주력하고 있습니다. 이는 의료기관들이 플랫폼의 가치를 구매 가능한 개별 모듈의 수로 판단하기보다는 플랫폼이 업무 인계나 수익 기회 손실을 얼마나 줄일 수 있는지에 따라 판단하는 경향이 강해지고 있기 때문입니다. 독립형 시스템은 2025년에는 제품 매출의 38% 가까이 차지할 것으로 예상되는 등, 여전히 상당한 시장 점유율을 유지하고 있습니다. 이는 소규모 진료소나 전문 클리닉의 경우, 대규모 시스템이 갖춘 복잡한 기능을 모두 갖추지 않고도 보다 간단한 예약 관리 및 청구 관리 도구를 원하는 경우가 많기 때문입니다. 이러한 구매자들은 특히 이미 임상 시스템이 도입되어 있거나, 진료소가 플랫폼의 전면적인 전환을 피하고자 하는 경우, 전환 장벽이 낮고 설정이 용이하며 운영 부담이 적다는 점을 여전히 중요하게 여기고 있습니다. 시간이 지남에 따라 모듈형 SaaS 패키지 덕분에 그 격차가 점차 좁혀지고 있으며, 그 결과 소규모 진료 환경에서도 미국의 진료 관리 시스템 시장은 서서히 통합형 솔루션으로 전환되고 있습니다.

2025년에는 소프트웨어가 구성 요소 매출의 63.83%를 차지했으며, 이는 모든 규모의 의료 기관에서 라이선싱, 구독 및 핵심 용도에 대한 접근이 핵심적인 역할을 하고 있음을 반영합니다. 기록 관리 시스템과 워크플로우 제어 계층이 없다면 어떤 의료 기관도 예약, 접수, 청구 및 보고 프로세스를 운영할 수 없기 때문에 이 도입된 소프트웨어 기반은 미국 진료 관리 시스템 시장의 상업적 기반으로 계속 자리 잡고 있습니다. 또한, 구매자가 외부 도구가 아닌 플랫폼 내에서 AI를 활용한 코딩, 워크플로우 조정, 분석, 환자와의 소통 기능을 추가하고 있기 때문에 소프트웨어 매출은 계속해서 높은 수준을 유지하고 있습니다. 벤더가 통합 제품군에 더 많은 기능을 포함시키면서, 소프트웨어를 모듈별로 개별적으로 교체하기가 어려워지고, 이로 인해 고객 유지율 향상과 계정 가치 심화가 촉진됩니다. 이것이 바로 구매자들이 보다 단순한 기술 환경을 원한다고 밝혔음에도 불구하고, 주요 공급업체들이 제품 라인업을 계속 확대하고 있는 이유 중 하나입니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 9.34%를 기록하며 더욱 빠르게 성장하고 있으며, 이러한 성장은 소프트웨어 수요의 감소라기보다는 도입의 어려움을 반영한다고 볼 수 있습니다. 많은 의료 서비스 제공업체들이 단순한 기술적 이양이 아닌, 청구 워크플로우, 미승인 관리, 채권 회수, 업무 혁신에 관한 직접적인 지원을 요구하고 있기 때문에 관리형 수익 주기 서비스가 확대되고 있습니다. 또한, 교육 및 지원 역할도 확대되고 있습니다. 이는 새로운 AI 및 자동화 기능이 단순히 시스템에 화면을 추가하는 데 그치지 않고, 접수 담당자, 청구 담당자, 관리자의 업무 루틴 자체를 변화시키기 때문입니다. AdvancedMD, Veradigm, CareCloud 등 각사는 2026년에 워크플로우를 강화하는 새 버전을 출시할 것이라고 강조하고 있으며, 이는 도입의 성패가 기술적 가용성뿐만 아니라 운영 지원에도 크게 좌우된다는 점을 보여줍니다. 사실, 미국의 진료 관리 시스템 업계에서는 많은 의료 기관에서 플랫폼의 고도화가 내부 관리 능력의 향상 속도를 앞지르는 속도로 진행되고 있어, 서비스 수익이 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the united states practice management system market size is projected to expand from USD 4.75 billion in 2025 and USD 5.08 billion in 2026 to USD 7.37 billion by 2031, registering a CAGR of 7.73% between 2026 to 2031.

This report is Segmented by Product (Integrated, Standalone), Component (Software, Services), Delivery Mode (Web-Based, Cloud-Based/SaaS, On-Premise), Functionality (Scheduling, Billing, Prior Auth, Records, Analytics, Patient Engagement, Telehealth, E-Prescribing), and End User (Physician Offices, Hospitals, Labs, Pharmacies, Ambulatory). Market Forecasts are Provided in Value (USD).

United States Practice Management System Market Trends and Insights

Administrative Costs and Claim Denials Make Status Quo Unsustainable

The United States practice management system market is being shaped by a billing environment that has become materially harder for providers to manage with fragmented tools. Kodiak Solutions reported that net revenue leakage from final denials and bad debt reached USD 48.4 billion across U.S. hospitals in 2025, up from USD 38.6 billion in 2024, while the median final denial rate rose from 2.5% to 2.7%. Premier also reported that claims adjudication costs providers USD 25.7 billion and that USD 18 billion of that spend is potentially unnecessary expense, which shows how much avoidable rework remains in the payment cycle. As a result, practices are giving higher priority to eligibility checks, pre-submission claim scrubbing, coding support, and denial prevention functions that can be tied directly to cash collection. This is why billing, coding, and claims management remain the largest functionality block in the United States practice management system market and why vendors are increasingly positioning measurable revenue recovery as the central value proposition.

Integrated EHR-PM-RCM Suites Redefine the Platform Buying Unit

The United States practice management system market is moving toward unified administrative and clinical platforms because providers now want fewer data handoffs and fewer reconciliation delays across scheduling, documentation, and revenue cycle activity. Integrated practice management systems controlled 61.9% of revenue in 2025, which confirms that buyers are already favoring broader suites over isolated point products. Epic showed the direction of travel at HIMSS 2026 with Penny for billing and denial avoidance, alongside agent-driven workflow tools that sit inside the main platform rather than outside it. athenahealth also expanded embedded revenue cycle improvements in its Spring 2026 athenaOne release, reinforcing the same shift toward connected workflows and regular platform-level upgrades. In practical terms, the integrated model reduces duplicate entry, keeps patient and billing data in one operating layer, and makes interoperability readiness easier to evaluate during procurement.

Migration Costs and Workflow Disruption Weigh on Replacement Cycles

The main brake on faster replacement remains the time and disruption involved in moving live administrative operations from one system to another. Implementation now goes beyond software installation because practices often need data cleansing, workflow redesign, staff retraining, payer rule alignment, and a parallel operating period before a full switch can happen. That burden is especially difficult for independent practices and community operators that do not have internal project teams or spare billing capacity during go-live periods. The rapid expansion of services, which is projected to grow at 9.3% through 2031, shows that many buyers are paying for outside implementation, training, and managed revenue cycle support instead of relying only on internal teams. This slows purchasing in the short run, even as it supports recurring vendor revenue inside the United States practice management system market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration Extends Beyond Cost Savings Into Operational Resilience

- FHIR-Based Interoperability Moves From Optional to Contractually Mandated

- Cybersecurity Exposure Reshapes Cloud Vendor Selection Criteria

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated practice management systems held 61.87% of revenue in 2025 and are projected to expand at 8.25% CAGR through 2031, which gives them both the largest base and the strongest momentum among product options. In product terms, this segment now represents the clearest center of gravity in the United States practice management system market because providers want one system to handle scheduling, documentation links, billing flow, and patient communication. EHR and EMR integrated systems remain the largest volume layer inside this group because health systems and larger physician organizations still favor single-vendor operating environments. Revenue-cycle integrated products are also gaining ground because providers want charge capture, edits, and denial management connected more tightly to front-end registration and back-end collections. Patient engagement integrated tools are becoming more relevant as digital intake, payment estimation, and self-service workflows move from optional features to normal administrative practice. E-prescribing integration is also shifting toward baseline functionality as broader interoperability expectations continue to rise across provider settings.

This direction supports the view that the United States practice management system industry is becoming less tolerant of disconnected software stacks. Epic, athenahealth, eClinicalWorks, and Veradigm are all leaning into broader workflow coverage because providers increasingly judge value by whether a platform reduces handoffs and missed revenue opportunities, not by how many separate modules can be purchased. Standalone systems still retain a meaningful share of demand, at near 38% of product revenue in 2025, because smaller physician offices and specialty clinics often want simpler scheduling and billing tools without the full complexity of a larger suite. Those buyers still value lower switching friction, easier configuration, and lower perceived operating burden, especially when clinical systems are already in place or when the office wants to avoid a full platform conversion. Over time, modular SaaS packaging is narrowing that gap, and that is gradually shifting more of the United States practice management system market toward integrated offers even in smaller practice settings.

Software accounted for 63.83% of component revenue in 2025, which reflects the central role of licensing, subscriptions, and core application access across provider organizations of every size. That installed software base remains the commercial foundation of the United States practice management system market because no practice can operate its scheduling, registration, billing, and reporting processes without a system of record and workflow control layer. Software revenue also stays elevated because buyers are adding AI-assisted coding, workflow orchestration, analytics, and patient communication capabilities inside the platform rather than through outside tools. As vendors bundle more functions into unified suites, software becomes harder to replace module by module, which supports retention and deeper account value. This is one reason the leading vendors continue to widen their product scope even when buyers say they want simpler technology estates.

Services are growing faster, at 9.34% CAGR through 2031, and that growth says more about implementation difficulty than about a reduced need for software. Managed revenue cycle services are expanding because many providers want direct support with claims workflows, denial management, collections, and operational change rather than a technology-only handoff. Training and support are also taking on a larger role because new AI and automation features alter work routines for front-desk staff, billers, and managers instead of merely adding another screen to the system. AdvancedMD, Veradigm, and CareCloud have all emphasized workflow-enhancing releases in 2026, which shows that successful deployment now depends on operating support as much as on technical availability. In effect, the United States practice management system industry is generating more service revenue because platform sophistication is rising faster than internal administrative capacity in many provider organizations.

Complete Report Scope:

- By Product

- Integrated Practice Management Systems

- EHR / EMR-Integrated Systems

- Billing and Revenue-Cycle-Integrated Systems

- Patient Engagement-Integrated Systems

- E-Prescribing-Integrated Systems

- Standalone Practice Management Systems

- Integrated Practice Management Systems

- By Component

- Software

- Services

- Implementation and Configuration Services

- Training and Support Services

- Managed Revenue Cycle Services

- By Delivery Mode

- Web-Based

- Cloud-Based / SaaS

- On-Premise

- By Functionality

- Appointment Scheduling and Registration

- Billing, Coding and Claims Management

- Insurance Eligibility and Prior Authorization Workflow

- Patient Record Tracking and Document Management

- Reporting, Analytics and Dashboarding

- Patient Engagement and Communication

- Telehealth Coordination

- E-Prescribing and Referral Management

- By End User

- Physician Back Offices / Physician Offices

- Hospitals and Health Systems

- Diagnostic Laboratories

- Pharmacies

- Ambulatory and Other Outpatient Settings

List of Companies Covered in this Report:

- AdvancedMD

- athenahealth

- Azalea Health

- CareCloud

- CollaborateMD

- Curemd Healthcare

- DrChrono

- Elation Health

- eClinicalWorks

- Epic Systems

- Greenway Health

- Henry Schein One / MicroMD

- Meditab

- ModMed

- NextGen Healthcare

- Office Ally

- Oracle Health

- PracticeSuite

- RXNT

- Tebra

- Veradigm

- WRS Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Administrative Cost and Claim-Denial Reduction Imperative

- 4.2.2 Shift To Integrated EHR-PM-RCM Suites

- 4.2.3 Cloud Migration for Multi-Site and Hybrid Workflows

- 4.2.4 FHIR-Based Interoperability and E-Prior-Authorization Compliance

- 4.2.5 TEFCA / QHIN Connectivity Becoming a Buying Criterion

- 4.2.6 AI-Native Denial Prevention and Staff-Capacity Extension

- 4.3 Market Restraints

- 4.3.1 Costly Migration, Onboarding, and Workflow Disruption

- 4.3.2 Cybersecurity and HIPAA Exposure in Cloud-Connected Environments

- 4.3.3 Payer Data Quality and API-Readiness Gaps

- 4.3.4 Vendor Consolidation and Legacy-Platform Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Integrated Practice Management Systems

- 5.1.1.1 EHR / EMR-Integrated Systems

- 5.1.1.2 Billing and Revenue-Cycle-Integrated Systems

- 5.1.1.3 Patient Engagement-Integrated Systems

- 5.1.1.4 E-Prescribing-Integrated Systems

- 5.1.2 Standalone Practice Management Systems

- 5.1.1 Integrated Practice Management Systems

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.2.2.1 Implementation and Configuration Services

- 5.2.2.2 Training and Support Services

- 5.2.2.3 Managed Revenue Cycle Services

- 5.3 By Delivery Mode

- 5.3.1 Web-Based

- 5.3.2 Cloud-Based / SaaS

- 5.3.3 On-Premise

- 5.4 By Functionality

- 5.4.1 Appointment Scheduling and Registration

- 5.4.2 Billing, Coding and Claims Management

- 5.4.3 Insurance Eligibility and Prior Authorization Workflow

- 5.4.4 Patient Record Tracking and Document Management

- 5.4.5 Reporting, Analytics and Dashboarding

- 5.4.6 Patient Engagement and Communication

- 5.4.7 Telehealth Coordination

- 5.4.8 E-Prescribing and Referral Management

- 5.5 By End User

- 5.5.1 Physician Back Offices / Physician Offices

- 5.5.2 Hospitals and Health Systems

- 5.5.3 Diagnostic Laboratories

- 5.5.4 Pharmacies

- 5.5.5 Ambulatory and Other Outpatient Settings

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AdvancedMD

- 6.3.2 athenahealth

- 6.3.3 Azalea Health

- 6.3.4 CareCloud

- 6.3.5 CollaborateMD

- 6.3.6 CureMD

- 6.3.7 DrChrono

- 6.3.8 Elation Health

- 6.3.9 eClinicalWorks

- 6.3.10 Epic Systems Corporation

- 6.3.11 Greenway Health

- 6.3.12 Henry Schein One / MicroMD

- 6.3.13 Meditab

- 6.3.14 ModMed

- 6.3.15 NextGen Healthcare

- 6.3.16 Office Ally

- 6.3.17 Oracle Health

- 6.3.18 PracticeSuite

- 6.3.19 RXNT

- 6.3.20 Tebra

- 6.3.21 Veradigm

- 6.3.22 WRS Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment