|

시장보고서

상품코드

2072709

HR 워크플로우용 에이전트 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI In HR Workflows - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

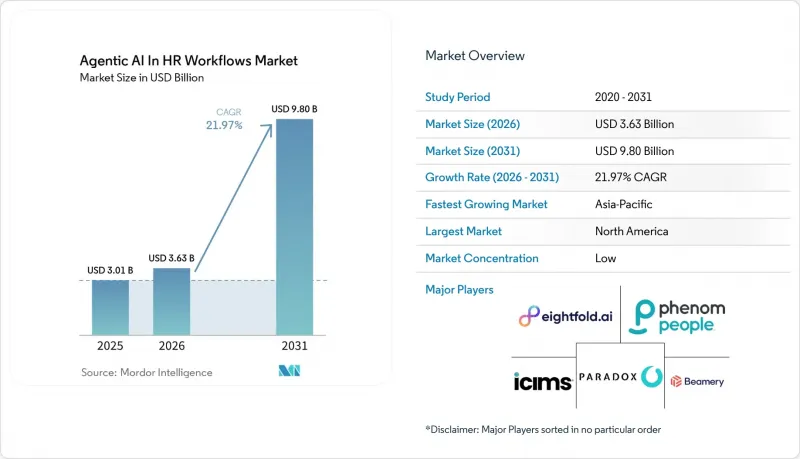

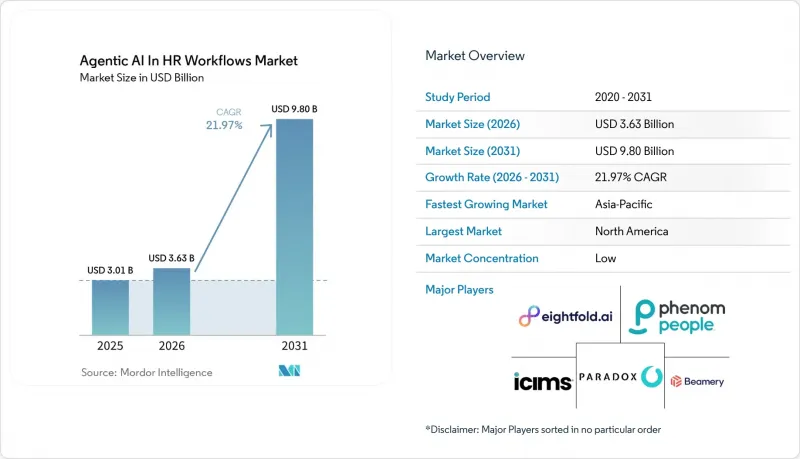

Mordor Intelligence에 의하면, HR 워크플로우용 에이전트 AI 시장 규모는 2025년 30억 1,000만 달러로 평가되었고, 2026년에는 36억 3,000만 달러로 추정되고, 2026-2031년 CAGR 21.97%로 성장을 지속할 전망이며, 2031년에는 98억 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(에이전트 AI 플랫폼 및 오케스트레이션 엔진 등), 기능별(인재 확보 및 채용 등), 배포 모델별(클라우드 기반, 하이브리드형, 온프레미스형), 기업 규모별(대기업 등), 최종 사용자 산업별(정보 기술 및 통신 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HR 워크플로우용 에이전트 AI 시장 동향 및 인사이트

자율적인 인사 서비스 제공에 대한 수요 증가

인사팀 내의 생산성 격차는 단순한 자동화만으로는 더 이상 해결할 수 없을 정도로 커졌습니다. 인사 부서의 인력이 제한적인 상황에서도 조직은 여전히 처리해야 할 업무량 증가, 직원들의 서비스에 대한 기대치 상승, 그리고 규정 준수 업무 증가에 직면해 있습니다. HR 워크플로우용 에이전트 AI 시장에서는 수동 개입을 최소화하면서도 Tier 1 요청을 접수부터 해결까지 처리할 수 있는 시스템에 대한 수요가 높아지고 있습니다. 자율적인 서비스 제공은 팀이 과부하 상태에 있을 때 기밀성이 높은 요청을 사내 스프레드시트나 이메일 스레드로 넘기는 경향도 줄여줍니다. 2026년에 실시된 경영진 대상 설문조사에 따르면, C-스위트 리더의 62%가 인재 데이터와 실적 간의 연관성에 대해 불만을 가지고 있으며, 이는 거버넌스가 강화된 인사 워크플로우에 대한 수요를 뒷받침하고 있습니다. 이러한 격차로 인해, HR 워크플로우용 에이전트 AI 시장에서는 서비스 자동화와 더욱 강력한 가시성, 관리 기능, 데이터 관리 체계를 결합한 벤더들이 지지를 받고 있습니다.

기술에 기반한 인재 선발에 대한 수요 증가

역량에 기반한 인재 선발은 단순한 방침 표명에서 일상적인 업무 흐름 설계로 점차 전환되고 있습니다. LinkedIn의 'Economic Graph'에 따르면, 기술 기반 접근 방식을 통해 AI 관련 직종의 AI 인재 파이프라인은 전 세계적으로 8.2배로 확대되었으며, 비 AI 직종에 비해 34%의 개선이 나타났습니다. HR 워크플로우용 에이전트 AI 시장에서 이로 인해 동적인 스킬 그래프와 매칭 로직은 정적인 자격 필터보다 더 높은 가치를 지니게 되었습니다. 평가 결과, 사내 이동 경로 및 인재 계획에 대한 신호가 동일한 환경에 통합됨에 따라, 새로운 조치가 취해질 때마다 향후 권장 사항이 개선됩니다. 또한, 단일 솔루션으로는 채용, 교육, 인사 이동 등 각 업무 간에 기술 데이터를 동기화할 수 없기 때문에 오케스트레이션 도구에 대한 수요도 증가하고 있습니다. 2026년 조사에 따르면, CHRO의 87%가 인사 프로세스에 AI가 더욱 확대 도입될 것으로 예상하고 있으며, 이는 2025년의 83%에서 증가한 수치입니다. 이는 기술에 기반한 의사결정을 대규모로 운영화할 수 있는 시스템에 대한 수요가 증가하고 있음을 보여줍니다.

채용 편향, 개인정보 보호, 감사 요건에 대한 높은 민감도

편향, 개인정보 보호 및 감사 요건은 HR 워크플로우에 에이전트 AI를 더 광범위하게 도입하는 데 있어 여전히 가장 큰 걸림돌로 남아 있습니다. EU AI법에서는 채용, 성과 평가 및 인사 관리에 사용되는 AI를 부속서 III에 따라 '고위험'으로 분류하고 있으며, 이에 따라 문서화, 테스트 및 감독에 대한 기준이 강화되었습니다. 즉, 공급업체와 구매자는 대규모 활용에 앞서 데이터 품질, 모델의 동작, 인적 감독 및 도입 후 모니터링에 관한 명확한 기록을 마련해야 합니다. 유럽연합 집행위원회의 2026년 시행 일정에 따라 규정 준수 대응을 위한 유예 기간이 마련되기는 했으나, 기한까지 이러한 관리 체제를 구축해야 할 필요성이 사라진 것은 아닙니다. 고용 AI 관련 법이 제정된 미국 주에서 인사 담당자의 57%가 이러한 규정을 인지하지 못하고 있었으며, 이를 인지하고 있는 조직 중에서도 규정 준수에 부합하는 정책을 수립한 곳은 고작 12%에 그쳤습니다. 이 때문에 HR 워크플로우용 에이전트 AI 시장에서는 처음부터 감사 추적 기록이나 사람이 직접 개입하여 변경한 경로를 보여줄 수 있는 벤더가 우위를 점하고 있습니다.

부문별 분석

2025년 기준으로, HR 워크플로우용 에이전트 AI 시장 규모 중 에이전트 AI 플랫폼 및 오케스트레이션 엔진이 41.71%의 점유율을 차지했으며, 인프라 계층이 가장 큰 시장 점유율을 차지하고 있습니다. 애플리케이션 에이전트가 기밀성이 높은 인사 프로세스에서 작동하려면 에이전트 등록, 권한 설정, 가시성 및 워크플로 제어가 제대로 갖춰져 있어야 하므로, 구매자들은 이 부분부터 착수하고 있습니다. 이러한 순서 설정 덕분에, 광범위한 자동화가 시작되기 전에 기업이 에이전트의 기록 접근 방식, 작업 실행 조건, 예외 처리 방식에 관한 정책을 수립할 수 있으므로 거버넌스 위험도 억제됩니다. 2026년 초에는 1,200개 이상의 고객사가 에이전트 등록 및 모니터링을 수행하고 있으며, 거버넌스를 최우선으로 한 도입이 실제 운영 환경으로 전환되고 있음이 드러났습니다. 이에 이어, 기존의 HR AI 에이전트 및 워크플로우 용도이 주목을 받고 있습니다. 이는 오케스트레이션 시스템을 전면적으로 구축하지 않고도 명확한 이용 사례를 필요로 하는 조직에 더 신속한 가치 실현(Time-to-Value)을 제공하기 때문입니다.

관리형 에이전트 AI 서비스는 2031년까지 연평균 성장률(CAGR) 24.36%를 나타낼 것으로 예측되며, 이는 구성 요소 중 가장 빠른 성장 속도입니다. HR 워크플로우 시장에서 에이전트 AI의 경우, 많은 구매자들이 설정, 모니터링, 재훈련 및 장기적인 정책 관리에 대해 외부 지원을 원하고 있기 때문에 이러한 서비스에 대한 수요가 증가하고 있습니다. 이는 특히 HR 팀에 AI 운영에 관한 심도 있는 전문 지식을 갖춘 인력이 부족하거나, 도입 후 복잡한 다중 에이전트 워크플로를 유지 관리할 충분한 기술 인력이 없는 경우에 해당합니다. 200종의 엔터프라이즈 에이전트를 종합적으로 출시하는 과정에서 HR에 특화된 15종의 신규 어시스턴트를 포함시킨 2026년 로드맵은 공급업체가 모든 도입 작업을 고객에게 맡기는 것이 아니라, 보다 관리 및 지도 중심의 기능을 패키지화하고 있음을 보여줍니다. HR 워크플로우용 에이전트 AI 시장에서 자율적인 실행을 시장 전체로 확대하기 위해서는 워크플로우 재설계, 변경 관리, 거버넌스 구축이 여전히 필요하기 때문에 전문 서비스는 여전히 중요한 역할을 수행하고 있습니다.

2025년 매출액 중 인재 확보·채용 대행 서비스가 26.82%를 차지했으며, 채용은 HR 워크플로우 내 에이전트 AI 시장에서 가장 큰 기능 부문이 되었습니다. 채용은 여전히 주요 진입 경로로 남아 있습니다. 이는 거래량이 많고, 선발 속도, 면접 일정 조율, 채용까지 소요되는 시간 등의 지표를 통해 성과를 측정하기 쉽기 때문입니다. 또한, 고용주는 채용 담당자에게 과도한 부담을 주지 않으면서 후보자 풀을 확대해야 한다는 지속적인 압박에 직면해 있으며, 이로 인해 체계적인 에이전트의 지원이 매력적인 선택지로 떠오르고 있습니다. 이 기능은 현재 선별 단계에 그치지 않고, 대규모 HCM 환경 내에서의 면접 및 워크플로우 실행으로 확대되고 있습니다. 2026년 5월, 주요 클라우드 채용 플랫폼과 AI 면접 도구가 통합된 것은 역량 기반의 자율적인 면접이 기업 채용 프로세스의 주류로 자리 잡고 있음을 보여줍니다.

HR 운영 자동화 에이전트 시장은 2031년까지 연평균 성장률(CAGR) 27.14%를 나타낼 것으로 예측되며, 이는 HR 워크플로우 내 에이전트형 AI 시장의 각 기능 중 가장 높은 성장률입니다. 이러한 성장은 반복적인 사건 처리, 복리후생 관리, 결근 처리, 서류 수집, 그리고 1단계 문의 대응과 같은 분야에서 비롯된 것으로, 이러한 업무는 처리량이 방대하며 의사결정이 대부분 규칙에 근거하고 있습니다. 이러한 워크플로는 직원 경험에도 직접적인 영향을 미치기 때문에 도입 직후부터 서비스 개선 효과를 체감할 수 있습니다. 과거 사례 검색 및 정책 지식 검색을 통해 일반적인 인사 관련 사안을 해결하도록 설계된 AI 전문가는 이 부문의 상업적 방향성과 부합합니다. 언어 모델이 비정형 요청에 대한 대응 능력을 향상시켜 감에 따라, HR 워크플로우 분야의 에이전트형 AI 시장은 완전한 자율적 의사결정이 기밀성이 더 높은 프로세스로 확대되기 전에 인사 운영 업무의 더 깊은 영역으로 침투해 나갈 것으로 보입니다.

지역별 분석

2025년, 북미는 HR 워크플로우용 에이전트 AI 시장 점유율의 39.66%를 차지했으며, 최대 지역 시장이 되었습니다. 미국은 기업 구매자, 플랫폼 공급업체, 통합 파트너가 집중되어 있어 계속해서 주요 수요 거점으로 자리 잡고 있습니다. 2026년 조사에 따르면, CHRO(최고인사책임자)의 87%가 인사 프로세스에 AI를 더욱 적극적으로 도입하기를 기대하고 있으며, 이는 2025년의 83%에서 증가한 수치로, 해당 지역에서 수요가 계속해서 증가하고 있음을 보여줍니다. 대기업은 거버넌스, 통합, 업무 흐름 재설계에 동시에 자금을 투입할 수 있기 때문에 지역 내 발전 속도를 주도하고 있습니다. 한편, 유럽에서는 EU AI법 및 현지 노사 협의 요건으로 인해 본 가동 전에 문서화, 심사, 승인 절차가 추가됨에 따라 도입 주기가 지연되고 있습니다.

아시아태평양은 HR 워크플로우용 에이전트 AI 시장에서 가장 빠른 성장세를 보일 것으로 예상되며, 2031년까지 연평균 성장률(CAGR)은 28.47%에 달할 전망입니다. 동남아시아, 인도, 한국, 중국, 일본, 호주에서는 고용주들이 더 소규모의 팀으로 채용, 신입 사원 온보딩, 인력 계획을 관리할 방법을 모색하고 있어 수요가 증가하고 있습니다. 일본은 기업 내 도입이 이미 광범위하게 이루어지고 있다는 점이 두드러지지만, 몇 가지 인사 활용 사례에 대해서는 더욱 심화할 여지가 남아 있습니다. 2026년 4월 기준으로, 조사 대상인 회원 기업의 약 90%가 어떤 형태로든 AI를 활용하고 있었으나, 성과 평가 분야에서의 AI 도입률은 여전히 5% 전후에 그치고 있어, 인사 업무 흐름에 대한 도입 확대 여지가 있습니다. 정부의 AI 정책 이니셔티브 및 인력 조사에 따르면, 정책 수립 및 거버넌스 계획이 도입과 병행하여 진행되고 있으며, 이것이 공급업체 선정 및 조달에 영향을 미치고 있습니다.

남미, 중동 및 아프리카는 2025년 HR 워크플로우용 에이전트 AI 시장에서 점유율은 낮았지만, 장기적인 성장 측면에서는 여전히 중요한 지역입니다. 남미에서는 브라질이 초기 수요를 주도하고 있으며, 중동에서는 아랍에미리트(UAE)와 사우디아라비아가 초기 도입 시장으로서의 역할을 수행하고 있습니다. 이는 인력 계획 및 채용의 자동화가 이들 국가의 노동 정책 우선순위와 부합하기 때문입니다. 아프리카에서는 남아프리카공화국이 가장 뚜렷한 수요 중심지이며, 나이지리아와 케냐에서는 중견 기업의 도입 기간을 단축할 수 있는 클라우드 네이티브 HR 플랫폼이 주목을 받고 있습니다. 이 지역들은 여전히 예산 및 프로세스 표준화와 관련된 제약에 직면해 있지만, HR 워크플로우용 에이전트 AI 시장에서 대규모 통합 작업 없이도 규정 준수 워크플로우를 제공할 수 있는 공급업체에게는 진입의 여지가 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the agentic AI in HR workflows market size is expected to grow from USD 3.01 billion in 2025 to USD 3.63 billion in 2026 and is forecast to reach USD 9.80 billion by 2031 at 21.97% CAGR over 2026-2031.

This report is Segmented by Component (Agentic AI Platforms and Orchestration Engines, and More), Function (Talent Acquisition and Recruiting, and More), Deployment Model (Cloud-Based, Hybrid, and On-Premises), Enterprise Size (Large Enterprises, and More), End-User Industry (Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In HR Workflows Market Trends and Insights

Rising Need For Autonomous HR Service Delivery

The productivity gap inside HR teams has become large enough that simple automation no longer solves it. Organizations still face rising case volumes, employee service expectations, and more compliance work, even when HR headcount stays tight. In the agentic AI in HR workflows market, which is pushing buyers toward systems that can take tier-1 requests from intake to resolution with less manual intervention. Autonomous service delivery also reduces the tendency to move sensitive requests into local spreadsheets or email threads when teams are overloaded. A 2026 executive survey found that 62% of C-suite leaders were dissatisfied with how people data connects to business performance, which supports demand for more governed HR workflows. That gap is helping the agentic AI in HR workflows market favor vendors that combine service automation with stronger visibility, controls, and data discipline.

Growing Demand For Skills-Based Talent Decisions

Skills-based talent decisions are moving from policy statements into day-to-day workflow design. LinkedIn's Economic Graph found that a skills-based approach expands the AI talent pipeline by 8.2 times globally for AI roles, a 34% improvement over non-AI roles. In the agentic AI in HR workflows market, this makes dynamic skills graphs and matching logic more valuable than static credential filters. When assessment results, internal mobility paths, and workforce planning signals feed the same environment, each new action improves future recommendations. This also increases demand for orchestration tools, as point solutions cannot keep skills data synchronized across recruiting, learning, and mobility tasks. A 2026 survey found that 87% of CHROs expected greater AI adoption in HR processes, up from 83% in 2025, underscoring stronger demand for systems that operationalize skills-based decisions at scale.

High Sensitivity To Hiring Bias, Privacy, And Audit Requirements

Bias, privacy, and audit requirements remain the most persistent barriers to wider adoption of agentic AI in HR workflows. The EU AI Act classifies AI used in recruitment, performance evaluation, and workforce management as high-risk under Annex III, which raises the bar for documentation, testing, and oversight. That means vendors and buyers need clear records of data quality, model behavior, human oversight, and post-deployment monitoring before scaled use. The European Commission's 2026 implementation timeline provided additional time for compliance, but it did not eliminate the need to build those controls before the deadline. Fifty-seven percent of HR professionals in U.S. states with employment AI laws were unaware of those rules, and only 12% of aware organizations had compliant policies in place. This keeps the agentic AI in HR workflows market tilted toward vendors that can show audit trails and human override paths from the start.

Other drivers and restraints analyzed in the detailed report include:

- Rising Pressure To Reduce HR Cycle Times Without Adding Headcount

- Fragmented HR Tech Stacks Creating Orchestration Demand

- Legacy HRIS And Payroll Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agentic AI Platforms and Orchestration Engines accounted for 41.71% share of the agentic AI in HR workflows market size in 2025, giving the infrastructure layer the largest commercial position. Buyers are starting here because agent registration, permissions, observability, and workflow control must be in place before application agents can run across sensitive HR processes. This sequencing also limits governance risk because enterprises can set policies for how agents access records, trigger actions, and hand off exceptions before wider automation begins. More than 1,200 customers were registering and monitoring agents in early 2026, indicating that governance-first deployment is moving into production environments. Pre-built HR AI Agents and Workflow Applications are closely followed because they offer faster time-to-value for organizations that want visible use cases without a full orchestration buildout.

Managed Agentic AI Services is projected to expand at 24.36% CAGR through 2031, the fastest pace within the component mix. The agentic AI in HR workflows market is seeing stronger demand for these services because many buyers want outside support for configuration, monitoring, retraining, and policy management over time. This is especially relevant when HR teams lack deep internal AI operations talent or sufficient technical staff to maintain complex multi-agent workflows after launch. A 2026 roadmap featuring 15 new HR focused assistants within a broader release of 200 enterprise agents shows how vendors are packaging more managed, guided capabilities instead of leaving all deployment work to clients. Professional Services still matter because workflow redesign, change management, and governance setup remain necessary before autonomous execution can scale across the agentic AI in HR workflows market.

Talent Acquisition and Recruiting Agents accounted for 26.82% of 2025 revenue, making hiring the largest functional segment in the agentic AI in HR workflows market. Recruiting remains the primary entry point because it generates high transaction volume and results are easier to measure through screening speed, interview coordination, and time-to-hire metrics. Employers also face ongoing pressure to widen candidate pools without overwhelming recruiters, which makes structured agent support attractive. The function is now moving beyond screening into interviewing and workflow execution inside large HCM environments. The integration of an AI Interviewer with a major cloud recruiting platform in May 2026 shows that autonomous skills-based interviewing is moving into mainstream enterprise recruiting stacks.

HR Operations Automation Agents is projected to grow at 27.14% CAGR through 2031, the fastest rate among functions in the agentic AI in HR workflows market. This growth comes from repetitive case handling, benefits administration, absence processing, document collection, and tier 1 query resolution, where process volumes are high, and decisions are often rules-based. These workflows also directly affect the employee experience, enabling buyers to see service improvements quickly after deployment. An AI specialist designed to resolve common HR cases through historical case retrieval and policy knowledge search aligns with this segment's commercial direction. As language models improve on unstructured requests, the agentic AI in HR workflows market is likely to push deeper into operational HR before fully autonomous decisions expand into more sensitive processes.

Complete Report Scope:

- By Component

- Agentic AI Platforms and Orchestration Engines

- Pre-built HR AI Agents and Workflow Applications

- Professional Services

- Managed Agentic AI Services

- By Function

- Talent Acquisition and Recruiting Agents

- Employee Lifecycle and HR Service Agents

- Talent Development and Internal Mobility Agents

- Workforce Planning and Intelligence Agents

- HR Operations Automation Agents

- By Deployment Model

- Cloud-Based

- Hybrid

- On-Premises

- By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- Information Technology and Telecom

- Healthcare and Life Sciences

- Banking, Financial Services and Insurance

- Retail and E-Commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America held 39.66% of the agentic AI market share in HR workflows in 2025, making it the largest regional market. The United States remained the main demand center because enterprise buyers, platform vendors, and integration partners are concentrated there. A 2026 survey found that 87% of CHROs expected greater AI adoption in HR processes, up from 83% in 2025, which supports continued demand momentum in the region. Large organizations set the regional pace because they can fund governance, integration, and workflow redesign simultaneously. Europe shows slower deployment cycles because the EU AI Act and local labor consultation requirements add documentation, review, and approval steps before going live.

Asia-Pacific is projected to record the fastest growth in the agentic AI in HR workflows market, with a 28.47% CAGR through 2031. Demand is rising across Southeast Asia, India, South Korea, China, Japan, and Australia as employers look for ways to manage recruiting, onboarding, and workforce planning with leaner teams. Japan stands out because corporate adoption is already broad, but several HR use cases still have room to deepen. Around 90% of surveyed member companies were using AI in some form in April 2026, while AI adoption for performance evaluation remained near 5%, leaving room for wider HR workflow deployment. National AI policy initiatives and workforce surveys show that policy development and governance planning are moving alongside adoption, which affects vendor qualification and procurement.

South America, the Middle East, and Africa held smaller shares of the agentic AI in HR workflows market in 2025, but they remain important for long-term expansion. Brazil is leading early demand in South America, while the United Arab Emirates and Saudi Arabia are serving as early rollout markets in the Middle East because workforce planning and hiring automation align with their labor policy priorities. South Africa is the clearest demand center in Africa, and Nigeria and Kenya are attracting cloud-native HR platforms that can shorten adoption timelines for mid-market employers. These regions still face budget and process standardization constraints, but they offer room for vendors that can package compliant workflows without heavy integration work in the agentic AI in HR workflows market.

- Phenom People, Inc.

- Eightfold AI, Inc.

- iCIMS, Inc.

- Paradox, Inc.

- Beamery, Inc.

- Gloat, Inc.

- HireVue, Inc.

- Findem, Inc.

- Harver B.V.

- Personio SE and Co. KG

- Lattice, Inc.

- Darwinbox Digital Solutions Private Limited

- Moveworks, Inc.

- Peoplebox, Inc.

- Peoplelogic, Inc.

- Humaans Ltd.

- Wisq, Inc.

- Visier, Inc.

- AvaHR, Inc.

- Rippling, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Need For Autonomous HR Service Delivery

- 4.3.2 Growing Demand For Skills-Based Talent Decisions

- 4.3.3 Rising Pressure To Reduce HR Cycle Times Without Adding Headcount

- 4.3.4 Fragmented HR Tech Stacks Creating Orchestration Demand

- 4.3.5 Expansion Of Employee Self-Service Expectations Across The Workforce

- 4.3.6 Early Compliance By Design Advantage For Governance-Ready Vendors

- 4.4 Market Restraints

- 4.4.1 High Sensitivity To Hiring Bias, Privacy, And Audit Requirements

- 4.4.2 Legacy HRIS And Payroll Integration Complexity

- 4.4.3 Human Oversight Requirements Limiting Full Autonomy In Critical Workflows

- 4.4.4 Low Process Standardization In Mid-Market Deployments

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat Of New Entrants

- 4.9.2 Bargaining Power Of Suppliers

- 4.9.3 Bargaining Power Of Buyers

- 4.9.4 Threat Of Substitutes

- 4.9.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Agentic AI Platforms and Orchestration Engines

- 5.1.2 Pre-built HR AI Agents and Workflow Applications

- 5.1.3 Professional Services

- 5.1.4 Managed Agentic AI Services

- 5.2 By Function

- 5.2.1 Talent Acquisition and Recruiting Agents

- 5.2.2 Employee Lifecycle and HR Service Agents

- 5.2.3 Talent Development and Internal Mobility Agents

- 5.2.4 Workforce Planning and Intelligence Agents

- 5.2.5 HR Operations Automation Agents

- 5.3 By Deployment Model

- 5.3.1 Cloud-Based

- 5.3.2 Hybrid

- 5.3.3 On-Premises

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecom

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Banking, Financial Services and Insurance

- 5.5.4 Retail and E-Commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Phenom People, Inc.

- 6.4.2 Eightfold AI, Inc.

- 6.4.3 iCIMS, Inc.

- 6.4.4 Paradox, Inc.

- 6.4.5 Beamery, Inc.

- 6.4.6 Gloat, Inc.

- 6.4.7 HireVue, Inc.

- 6.4.8 Findem, Inc.

- 6.4.9 Harver B.V.

- 6.4.10 Personio SE and Co. KG

- 6.4.11 Lattice, Inc.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Moveworks, Inc.

- 6.4.14 Peoplebox, Inc.

- 6.4.15 Peoplelogic, Inc.

- 6.4.16 Humaans Ltd.

- 6.4.17 Wisq, Inc.

- 6.4.18 Visier, Inc.

- 6.4.19 AvaHR, Inc.

- 6.4.20 Rippling, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment