|

시장보고서

상품코드

2072717

미국의 방위 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Defense Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

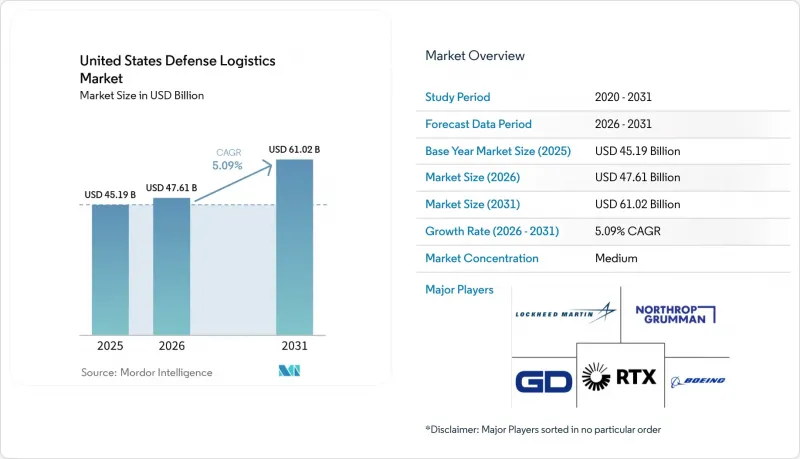

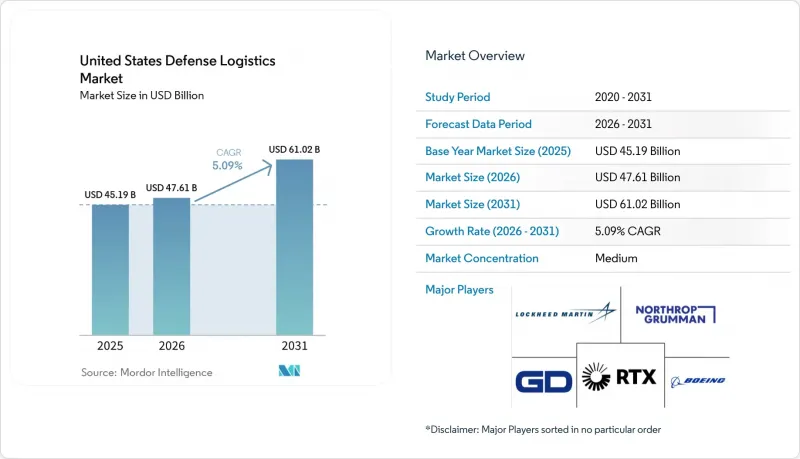

Mordor Intelligence에 의하면, 미국의 방위 물류 시장 규모는 2025년에 451억 9,000만 달러로 평가되었고, 2026년 476억 1,000만 달러로 추정되고, 2031년까지 610억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 5.09%를 나타낼 전망입니다.

미국의 국방 물류 시장이 확대되고 있는 것은 국방부가 2026년에 접어들면서 조달 건수가 대폭 증가하고, 탄약 보충 수요가 높아지며, 조선 및 미사일 관련 지출이 지속되고 있기 때문입니다. 이로 인해 운송, 창고 보관 및 유지 관리에 대한 수요가 수년 동안 높은 수준을 유지하고 있습니다. 본 보고서는 서비스 유형별(무기, 부대 이동, 기술 지원, 의료 지원 및 보건 서비스 등), 물류 기능별(수송, 창고 및 유통, 부가가치 서비스), 최종 사용자별(육군, 해군, 공군 등), 지역별(북동부, 남동부, 중서부, 남서부, 서부)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 방위 물류 시장 동향 및 인사이트

유지 및 현대화를 위한 미국 국방부(DoD)의 조달 확대

미국 국방부(펜타곤)의 2026 회계연도 조달 예산은 2,050억 달러에 육박하며, 2025 회계연도의 확정 조달액인 1,740억 달러보다 증가한 수치입니다. 이러한 증가로 인해 신규 장비 및 예비 부품의 입고, 보관, 운송 및 유지보수와 관련된 물류 업무량이 직접적으로 확대됩니다. 조정 지출에는 250억 달러 규모의 군수품 예산 한도도 포함되어 있으며, 이는 미국 국방 물류 시장 전반에 걸쳐 무기 취급, 정비소의 처리 능력 및 안전한 수송을 지원하는 데 사용됩니다. 이러한 수요는 초기 조달 연도에만 국한되는 것이 아닙니다. 각 플랫폼의 수명 주기 전반에 걸쳐 물류 비용이 지속적으로 발생하기 때문에 확고한 유지 관리 역량을 갖춘 기업에게는 계약 전망이 장기화되기 때문입니다. 또한, 역물류 역시 여전히 중요합니다. 국방물류국(DLA)은 2025 회계연도에 당초 2,320억 달러 상당의 자산을 처리하였고, 20억 달러 상당의 물품 240만 점을 재사용했습니다. 이는 폐기, 회수, 재분배, 재사용이 전방으로의 배송을 넘어 계속해서 업무량을 발생시키고 있음을 보여줍니다. 2026년도 예산이 집행되고 그 이후의 계획이 수립됨에 따라, 정비 지원, 유해 물질 취급, 재고 관리 분야에서 실적이 있는 도급업체는 미국 국방 물류 시장에서 지속적인 수주를 확보할 수 있는 입장에 있습니다. 이를 통해 조달 주기가 최종적으로 안정화되더라도 수익의 지속성이 유지됩니다.

인도-태평양으로의 전략적 중심 이동이 사전 배치 재고를 뒷받침

미국 국방 물류 시장에서 가장 두드러진 구조적 변화는 여전히 인도-태평양 지역으로의 전략적 중점 이동에 있습니다. 해당 지역에서는 전구 규모의 광대함, 곳곳에 흩어져 있는 섬들, 그리고 장거리 해상·항공 노선으로 인해 더 많은 재고 거점과 더욱 탄탄한 지속 지원 계획이 요구되고 있습니다. 해병대도 수빅 만에 새로운 사전 배치 프로그램을 마련했습니다. 이 부대는 팔라우와 호주에 추가 거점을 마련하기 위한 평가를 진행하는 한편, 해군은 10년 임대 계약에 따라 필리핀에 대규모 공조 관리형 보관 시설을 구축하는 작업을 추진했습니다. 또한, 합동 훈련을 통해 제1도서선 부근에서의 전방 무장 및 급유 개념이 입증되었으며, 가혹한 환경 하에서의 연료 취급, 탄약 중계 보관, 그리고 신속한 재보급 서비스에 대한 수요가 높아지고 있음이 드러났습니다. 일본의 2026년 인도-태평양 전개 계획은 다국적 후방 지원 조정에 새로운 차원을 더함으로써, 미국 방위 물류 시장 전반에서 운송, 창고 보관 및 전방 지원 관련 계약 활동이 더욱 활성화될 것입니다. 그 결과, 단일 허브에 대한 의존도를 낮추고, 유연한 민간 및 군용 유통 네트워크를 더욱 중시하는 보다 광범위한 물류 기반이 형성될 것입니다.

공급업체 기반의 축소와 공급망의 취약성

공급업체의 취약성은 여전히 미국 국방 물류 시장의 제약 요인으로 작용하고 있습니다. 이는 물류 성과가 부품, 특수 자재 및 인증된 정비 자재의 안정적인 공급에 달려 있기 때문입니다. 2026년 해군학원(Naval Postgraduate School)의 조사에 따르면, 주요 계약업체의 84% 이상이 1차 공급업체 이후 단계에 대한 가시성을 확보하지 못하고 있으며, 이는 주조품, 폭발물, 베어링, 이와 유사한 자재공급 차질이 나중에 드러나 프로그램 실행을 지연시킬 가능성이 있음을 의미합니다. 인증 및 사이버 규정 준수에 드는 비용은 애초에 제한된 자본과 좁은 인력 풀로 운영되던 중소기업에 추가적인 부담을 주고 있습니다. 또한, '국가 안보를 위한 비즈니스 임원단(Business Executives for National Security)'는 2025년에 중소기업의 경영권 이양이 잇따를 전망이라며, 대체하기 어려운 전문 공급업체들의 사업 철수나 통합 위험이 높아지고 있다고 경고했습니다. 실제로, 공급업체 기반의 축소는 미국 국방 물류 시장 전체에 걸쳐 재고 보충 주기의 지연, 가격 책정 유연성의 저하, 운전 자본 완충 장치 확보의 필요성 증가를 초래할 가능성이 있습니다. 이는 대체 조달처가 제한적인 탄약, 항공기 부품 및 기타 품목에서 특히 두드러집니다.

부문별 분석

2025년, 무기 부문은 미국 국방 물류 시장 규모의 43.11%를 차지했으며, 가장 큰 서비스 유형이 되었습니다. 이러한 주도적인 위상은 지속적인 탄약 감축, 보충 수요, 그리고 2026년의 자금 조달 환경 속에서 무기 재고 조달 및 공급망 지원이 계속해서 우선순위로 다뤄지고 있음을 반영합니다. 이러한 운영 방식은 단순한 단기적인 조달 붐에 그치지 않고, 실전 지역에서의 지원과 전시 비축 물자의 재구축이 병행되어 진행되기 때문에 무기고와 유통 거점에서는 지속적인 처리량이 발생하고 있습니다. 위험물 운송 자격, 안전한 보관 능력 및 인증된 취급 절차를 갖춘 계약업체는 이러한 수요 구조 하에서 계속해서 유리한 입지를 차지하고 있습니다. 또한, 탄약 수송의 규모와 기밀성이 높기 때문에 전체 업무 흐름에서 경쟁할 수 있는 공급업체의 수가 제한되어, 기존 사업자들의 재계약이 유지되고 있습니다.

의료 지원 및 보건 서비스는 가장 빠르게 성장하고 있는 서비스 분야입니다. 이러한 요인들은 변화하는 부상자 치료 요건과 분산된 전장에서의 대피 준비 태세 강화에 힘입어, 2031년까지 연평균 성장률(CAGR) 7.93%로 확대될 것으로 전망됩니다. 이에 따라 의료 물자 배치, 콜드체인 지원 및 현장 대응 물류는 향후 전망에서도 계속해서 중요한 위치를 차지할 것입니다. 군 부대의 이동, 소방·방재 및 기타 서비스는 안정적이고 지속적인 활동의 기반을 형성하고 있으며, 이 모든 요소가 결합되어 미국의 국방 물류 산업은 전투 시의 보급뿐만 아니라 시설의 지속적인 운영, 즉각 대응 태세 지원, 그리고 비상 대응 계획과도 밀접하게 연결되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states defense logistics market size was valued at USD 45.19 billion in 2025 and is estimated to grow from USD 47.61 billion in 2026 to reach USD 61.02 billion by 2031, at a CAGR of 5.09% during the forecast period 2026 to 2031.

The United States defense logistics market is expanding because the Department of Defense entered 2026 with a materially higher procurement pipeline, stronger munitions replenishment needs, and continued shipbuilding and missile spending that have kept transportation, warehousing, and sustainment demand elevated for multiple years. This report is Segmented by Service Type (Armament, Troop Movement, Technical Support, Medical Aid and Health Services, and More), by Logistics Functions (Transportation, Warehousing and Distribution, and Value-Added Services), by End User (Army, Navy, Air Force, and More), and by Region (Northeast, Southeast, Midwest, Southwest, and West). The Market Forecasts are Provided in Terms of Value (USD).

United States Defense Logistics Market Trends and Insights

Rising DoD Procurement for Sustainment and Modernization

The Pentagon's FY2026 procurement budget stands near USD 205 billion, up from the FY2025 enacted procurement of USD 174 billion, and that increase directly expands the logistics workload associated with receiving, storing, transporting, and maintaining new equipment and spare parts. Reconciliation spending also includes a USD 25 billion munitions envelope, which supports armament handling, depot throughput, and secure transportation across the United States defense logistics market. The demand is not limited to the initial procurement year, because logistics costs continue throughout the life of each platform, thereby extending contract visibility for firms with established sustainment capacity. Reverse logistics also remains important because the Defense Logistics Agency processed property originally valued at USD 232 billion in FY2025 and reutilized 2.4 million items valued at USD 2 billion, demonstrating that disposal, recovery, redistribution, and reuse continue to generate workload beyond forward delivery. As the 2026 budget is executed and follow-on plans are shaped, contractors with proven depot support, hazardous material handling, and inventory management records are positioned to capture recurring work across the United States defense logistics market. This maintains revenue durability even as acquisition cycles eventually moderate.

Indo-Pacific Pivot Boosting Pre-Positioned Stocks

The strongest structural shift in the United States defense logistics market remains the Indo-Pacific posture, where theater scale, distributed islands, and long sea and air routes require more inventory nodes and more resilient sustainment planning. The Marine Corps also established a new prepositioning program at Subic Bay. They evaluated additional sites in Palau and Australia, while the Navy pursued a large, climate-controlled storage facility in the Philippines under a 10-year lease. Joint exercises also validated forward arming and refueling concepts near the first island chain, indicating rising demand for fuel handling, ammunition staging, and rapid resupply services in austere settings. Japan's 2026 Indo-Pacific deployment schedule adds another layer of multinational sustainment coordination, and that supports more contracting activity for transportation, warehousing, and forward support across the United States defense logistics market. The result is a wider logistics footprint that depends less on single hubs and more on flexible commercial and military distribution links.

Vendor Base Contraction and Supply-Chain Fragility

Supplier fragility remains a restraint on the United States defense logistics market because logistics performance depends on stable access to components, specialized materials, and qualified maintenance inputs. Naval Postgraduate School research in 2026 found that more than 84% of prime contractors lacked visibility beyond Tier-1 suppliers, which means disruptions in castings, energetics, bearings, and similar inputs can surface late and delay program execution. Certification and cyber compliance costs add more pressure on smaller firms that were already operating with limited capital and narrow labor pools. Business Executives for National Security also warned in 2025 that a large wave of small-business ownership transitions is approaching, increasing the risk of exits or consolidation among specialized suppliers that are difficult to replace. In practical terms, a thinner supplier base can slow replenishment cycles, reduce pricing flexibility, and increase the need for working capital buffers across the United States defense logistics market. That is especially relevant in ammunition, aviation parts, and other categories where alternate sourcing is limited.

Other drivers and restraints analyzed in the detailed report include:

- Digital Transformation and AI-Enabled Predictive Logistics

- DLA WMS Roll-Out Unlocking Outsourced 3PL Demand

- Federal Budget Uncertainty/CRs Delaying Contract Awards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Armament held 43.11% of the United States defense logistics market size in 2025, making it the largest service type. Its leading position reflects ongoing munitions drawdowns, replenishment demand, and a 2026 funding environment that continues to prioritize procurement and supply-chain support for weapons inventories. The operating pattern is broader than a short procurement wave because live theater support and war reserve rebuilding occur in parallel, creating sustained throughput at depots and distribution sites. Contractors with hazardous-material transport qualifications, secure storage capacity, and certified handling processes remain well-positioned under this demand structure. The scale and sensitivity of munitions movement also limit the number of providers that can compete across the full workflow, which supports repeat business for established performers.

Medical aid and health services are the fastest-growing service type. They are projected to expand at a 7.93% CAGR through 2031, supported by evolving casualty care requirements and heightened evacuation readiness in dispersed theaters. That keeps medical supply positioning, cold-chain support, and field response logistics relevant to future contracting scopes. Military troop movement, firefighting protection, and other services add a stable base of recurring activity, and together they keep the United States defense logistics industry tied not only to combat resupply but also to installation continuity, readiness support, and contingency planning.

Complete Report Scope:

- By Service Type

- Armament

- Military Troops Movement Support

- Technical Support & Maintenance

- Medical Aid & Health Services

- Fire-fighting Protection

- Other Services

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing & Distribution

- Value-added Services (Labelling, Kitting, Consulting)

- Transportation

- By End User

- Army

- Navy

- Air Force

- Others

- By Region

- Northeast

- Southeast

- Midwest

- Southwest

- West

List of Companies Covered in this Report:

- Lockheed Martin

- Northrop Grumman

- RTX Corporation (Raytheon business units)

- General Dynamics

- Boeing Defense, Space & Security

- Leidos

- L3Harris Technologies

- Huntington Ingalls Industries

- Booz Allen Hamilton

- Amentum

- KBR

- Science Applications International Corporation (SAIC)

- ASRC Federal

- FedEx Government Services

- UPS Government & Defense

- J.B. Hunt Transport Services

- Werner Enterprises

- Schneider National

- Crowley

- Maersk Line, Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Modern Warfare

- 4.2 Defense Spending Trends

- 4.3 Market Drivers

- 4.3.1 Rising DoD Procurement for Sustainment and Modernization

- 4.3.2 Indo-Pacific Pivot Boosting Pre-Positioned Stocks

- 4.3.3 Digital Transformation and AI-Enabled Predictive Logistics

- 4.3.4 DLA WMS Roll-Out Unlocking Outsourced 3PL Demand

- 4.3.5 Net-Zero Mandates Spurring Electric/Autonomous Base Fleets

- 4.3.6 Warstopper and Industrial-Base Funds for Niche Suppliers

- 4.4 Market Restraints

- 4.4.1 Vendor Base Contraction and Supply-Chain Fragility

- 4.4.2 Federal Budget Uncertainty/CRs Delaying Contract Awards

- 4.4.3 PFAS Remediation Inflating Infrastructure Costs

- 4.4.4 Zero-Trust Cyber Compliance Slowing System Roll-Outs

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Defense Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Armament

- 5.1.2 Military Troops Movement Support

- 5.1.3 Technical Support & Maintenance

- 5.1.4 Medical Aid & Health Services

- 5.1.5 Fire-fighting Protection

- 5.1.6 Other Services

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing & Distribution

- 5.2.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.2.1 Transportation

- 5.3 By End User

- 5.3.1 Army

- 5.3.2 Navy

- 5.3.3 Air Force

- 5.3.4 Others

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Southeast

- 5.4.3 Midwest

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Lockheed Martin

- 6.4.2 Northrop Grumman

- 6.4.3 RTX Corporation (Raytheon business units)

- 6.4.4 General Dynamics

- 6.4.5 Boeing Defense, Space & Security

- 6.4.6 Leidos

- 6.4.7 L3Harris Technologies

- 6.4.8 Huntington Ingalls Industries

- 6.4.9 Booz Allen Hamilton

- 6.4.10 Amentum

- 6.4.11 KBR

- 6.4.12 Science Applications International Corporation (SAIC)

- 6.4.13 ASRC Federal

- 6.4.14 FedEx Government Services

- 6.4.15 UPS Government & Defense

- 6.4.16 J.B. Hunt Transport Services

- 6.4.17 Werner Enterprises

- 6.4.18 Schneider National

- 6.4.19 Crowley

- 6.4.20 Maersk Line, Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment