|

시장보고서

상품코드

2072735

영국의 디지털 헬스케어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Digital Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

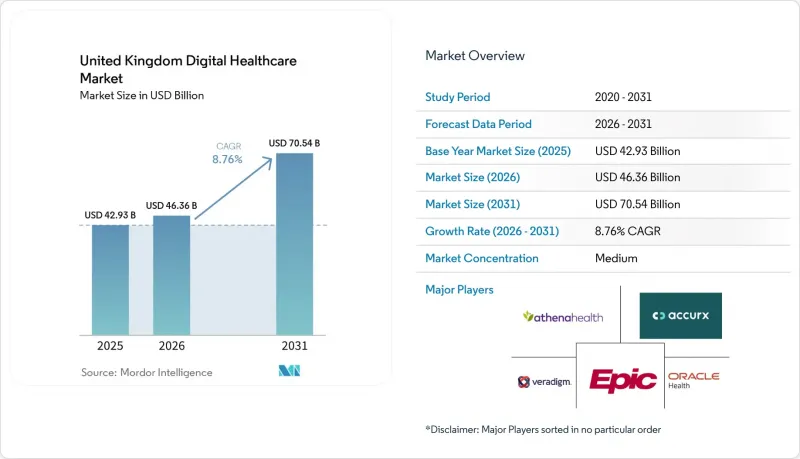

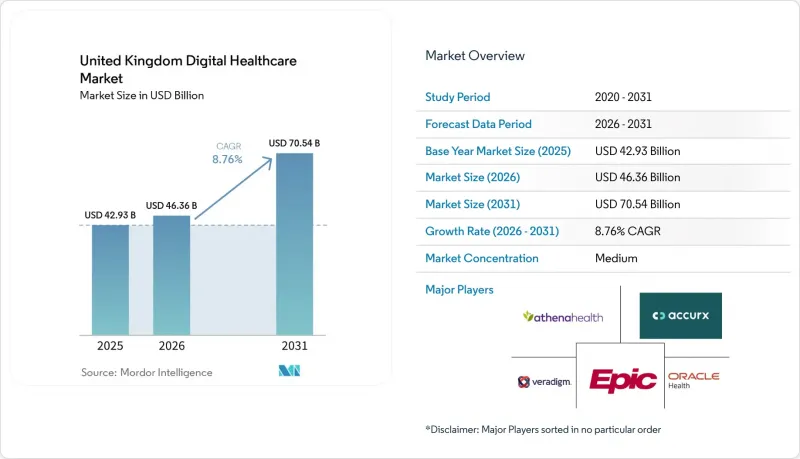

Mordor Intelligence에 의하면, 영국의 디지털 헬스케어 시장 규모는 2025년 429억 3,000만 달러로 평가되었고, 2026년 463억 6,000만 달러로 추정되고, 2031년까지 705억 4,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 8.76%를 나타낼 전망입니다.

본 보고서는 제공 형태별(소프트웨어, 서비스, 하드웨어), 기술별(원격의료, 원격 환자 모니터링, m헬스, 헬스케어 분석 및 AI 등), 도입 형태별(클라우드 기반, 하이브리드형, 온프레미스형), 용도별(만성 질환 관리 등), 최종 사용자별(병원 등), 지역별(영국)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

영국의 디지털 헬스케어 시장 동향 및 인사이트

NHS의 전자 환자 기록(EPR) 도입이 전환점에 도달합니다.

2025년 디지털 성숙도 평가에 따르면, NHS 제공업체의 93%가 전자 환자 기록(EPR) 시스템을 운영 중이었으나, 양방향 데이터 흐름을 통합한 곳은 고작 30%에 불과했습니다. 이는 현재의 움직임이 초기 도입이 아니라 최적화에 중점을 두고 있음을 의미합니다. NHS 잉글랜드는 2026년 말까지 급성기 의료 트러스트의 97%가 EPR을 도입할 것으로 전망하고 있으며, 이러한 도입 작업이 계속해서 영국 디지털 헬스케어 시장 전체 수요를 뒷받침하고 있습니다. NHS의 지역 차원 IT 지출은 2025/26 회계연도의 49억 파운드(62억 달러)에서 2028/29 회계연도에는 68억 파운드(86억 달러)로 증가할 것으로 예상되며, 이로 인해 플랫폼 공급업체와 서비스 파트너는 도입 및 지원 업무를 수행할 수 있는 더 긴 기간을 확보할 수 있게 될 것입니다. 중요한 비즈니스 변화 중 하나로, NHS 최전선 생산성 프로그램을 통해 수익 자금이 전자 환자 기록(EPR) 최적화, 교육, 업무 흐름 재설계에 투입되게 된 점을 들 수 있습니다. 이로 인해 지출 범위가 초기 라이선스 비용을 넘어 확대되고 있습니다. 이러한 변화로 인해, 이미 대규모 도입을 완료한 트러스트에서도 매니지드 서비스, 통합 지원, 사용자 교육, 가동 후 컨설팅이 지속적으로 제공되며, 일회성 계약이 아닌 지속적인 계약 가치가 뒷받침되고 있습니다.

급성기 의료 현장을 넘어선 가상 병동의 확대

NHS 잉글랜드는 2025년 3월 기준으로 12,825병상의 가상 병동을 운영했으며, 남동부 지역만 해도 2024년에 8만 5,000건이 넘는 가상 병동 입원 사례가 기록되었는데, 이는 2023년 수준보다 18% 증가한 수치입니다. 'NHS 10개년 보건 계획'에 따라 예방적이고 계획적인 의료 플랫폼을 위한 전국적인 조달 경로가 마련될 것이 약속되었으며, 인센티브가 지역 밀착형 응급 의료 활동과 보다 직접적으로 연계되었습니다. NHS가 의뢰한 한 연구에 따르면, '재택 병원(Hospital at Home)' 외래 치료가 입원 치료보다 비용이 저렴하며, 환자 1인당 치료 건당 평균 2,265파운드(2,860달러)를 절감할 수 있는 것으로 밝혀졌으며, 이 수치는 현재 각지의 사업 계획 수립에 영향을 미치고 있습니다. COPD, 심부전, 허약 상태에 대한 케어 패스는 현재 단순한 추가적인 시범 사업이 아니라, '가상 우선' 서비스로 설계되어, 이로 인해 원격 모니터링 업체가 의료 서비스 제공에서 차지하는 위상이 변화하고 있습니다. 이러한 변화로 인해 영국의 디지털 헬스케어 시장에서 NHS의 일상 업무에 활용되는 연결 기기, 워크플로우 플랫폼, 그리고 재택 환경에서의 데이터 통합에 대한 수요가 증가하고 있습니다.

NHS 시설 전반에 걸쳐 존재하는 기존 상호운용성 문제

'2025년 디지털 성숙도 평가'에 따르면, 전자 환자 기록(EPR)을 도입한 NHS 제공 기관 중 양방향 데이터 흐름을 통합하고 있는 곳은 고작 30%에 불과하며, 이는 커넥티드 케어의 성장을 저해하는 가장 명백한 제약 요소 중 하나로 남아 있습니다. NHS 잉글랜드의 '최전선 생산성 프로그램' 및 'NHS 표준 데이터 모델'은 이 격차를 줄이는 것을 목적으로 하고 있지만, 이사회는 '단일 환자 기록(SPR)'이 프로그램의 완전한 이점이 실현되는 것은 2030년까지는 기대하기 어렵다는 견해를 밝혔습니다. 여전히 호환되지 않는 시스템에 의존하고 있는 지역에서는 특히 급성기 의료, 지역 의료, 정신보건 서비스 간의 연계가 필요한 경우, 치료 경로의 재설계가 지연되고, 데이터 교환 속도가 저하되며, 통합 작업 비용이 급증하는 상황에 직면하고 있습니다. 원격 모니터링, 공동 진료, 의사결정 지원과 관련된 수익은 각 의료 현장 간의 신뢰할 수 있는 데이터 교환에 의존하고 있기 때문에 이러한 지연은 영국의 디지털 헬스케어 시장에 있어 중대한 문제가 됩니다. 따라서 FHIR UK Core R4 및 NHS GP Connect 표준 준수를 입증할 수 있는 공급업체는 여전히 자체 개발한 연동 방식에 의존하는 공급업체보다 뚜렷한 상업적 우위를 점하고 있습니다.

부문별 분석

2025년, 소프트웨어는 영국 디지털 헬스케어 시장 점유율의 59.27%를 차지했습니다. 이는 EPR(전자건강기록) 라이선싱, SaaS 기반 임상 플랫폼, 그리고 앰비언트 음성 및 분석 도구의 급속한 상업적 확장에 힘입은 결과입니다. 이러한 주도적 지위는 단기적인 모멘텀이라기보다는 구조적인 수요를 반영하고 있습니다. 왜냐하면, 제한된 수의 EPR 공급업체와 앱 생태계를 중심으로 한 NHS의 표준화로 인해 대규모 업데이트 기반이 형성되어 있기 때문입니다. 또한 소프트웨어 분야는 클라우드 네이티브 임상 플랫폼이 더 이상 단독 프로젝트가 아니라 장기적인 운영 인프라로 취급되게 된 점에서도 혜택을 보고 있습니다. 이에 따라 조달은 일회성에서 벗어나, 트러스트 및 통합 케어 시스템 전반에 걸친 다년간의 변혁 계획과 더욱 밀접하게 연계된 형태로 변화하고 있습니다. 또한, 트러스트가 임상 및 관리 측면에서 더 광범위한 기능을 갖춘 소수의 시스템을 요구하게 됨에 따라, 이 소프트웨어는 영국 디지털 헬스케어 산업 전반에 깊이 뿌리내리게 될 것입니다.

서비스 부문은 가장 빠르게 성장하고 있는 분야이며, 영국 디지털 헬스케어 시장의 서비스 규모는 2026-2031년 연평균 성장률(CAGR) 9.08%로 확대될 것으로 예측됩니다. NHS의 각 기관은 대규모 시스템 가동 시작 이후, 매니지드 서비스, 도입 지원, 최적화 작업 및 AI-as-a-Service(AaaS)로 더 많은 예산을 전환하고 있습니다. EPR(전자 환자 기록)의 사용성 조사에 따르면, NHS 직원 중 단 34%만이 EPR 덕분에 업무 효율이 향상되었다고 느끼고 있는 것으로 나타났습니다. 이는 트러스트가 교육, 워크플로우 재설계, 도입 후 지원에 더 많은 비용을 투자하고 있는 이유를 설명하는 한 가지 요인입니다. 하드웨어 시장 규모는 여전히 작지만, 가상 병동 키트, 연결형 웨어러블 기기, 원격 모니터링 기기가 재택 간호 모델에서 핵심적인 역할을 수행하고 있기 때문에 여전히 중요한 위치를 차지하고 있습니다. 계획 중인 20억 파운드(25억 달러) 규모의 '임상 디지털 헬스 시스템 2.0'이 프레임워크 역시 NHS 계약이 단일 제품 구매가 아닌, 소프트웨어 및 서비스를 결합한 제공 형태로 전환되고 있음을 보여줍니다.

2025년에는 텔레헬스 및 원격의료가 매출의 35.79%를 차지했으며, 영국 디지털 헬스케어 시장에서 가장 큰 기술 부문으로서의 위상을 유지했습니다. 이러한 우위는 팬데믹 기간 동안 도입된 조치의 장기적인 여파, 특히 응급 진료, 경과 관찰 및 만성 질환 관리의 진료 경로 재설계 측면에서 여전히 반영되고 있습니다. 또한, 가상 병동 모델이 여전히 연결 기기, 경보 시스템, 임상의용 대시보드에 의존하고 있기 때문에 이러한 기술 기반 하에서 원격 환자 모니터링도 확대되고 있습니다. m헬스 용도는 양식, 메시징, 예약 관리, 만성 질환 관리 관련 소통을 점점 더 많이 지원하게 된 NHS 앱의 기능 확충 덕분에 혜택을 보고 있습니다. 디지털 헬스 시스템은 소수의 플랫폼 제공업체를 중심으로 통합이 진행되고 있으며, 이에 따라 영국 디지털 헬스케어 업계 전반에서 기술 스택의 통합이 진행되고 있습니다.

헬스케어 분석과 AI는 예측 기반 운영, 의사결정 지원, 그리고 앰비언트 음성 기록에 힘입어 2031년까지 연평균 성장률(CAGR) 8.98%를 기록하며 가장 빠르게 성장이 전망되는 기술 분야입니다. NHS 연합 데이터 플랫폼 및 관련 AI 안전 프로그램은 데이터 인프라를 임상 및 운영 용도의 직접적인 원동력으로 전환하는 데 기여하고 있습니다. OECD의 분석에 따르면, 영국은 의료 분야에서 확장 가능한 클라우드 도입의 대표적인 사례로 꼽혔으며, AI 진단 도구의 조달은 공공 부문 도입의 벤치마크로 지목되었습니다. 디지털 치료제도 성장하고 있지만, NICE의 증거 기반 지침에 따르면 광범위한 도입 지원 체계가 확립되기까지는 여전히 긴 검증 주기가 필요하기 때문에 그 보급에는 여전히 제약이 남아 있습니다. 따라서 AI와 분석 기술은 완전히 새로운 치료 경로가 확립될 때까지 기다릴 필요 없이 기록 작성, 처리 능력, 분류 및 수용 능력 관리를 개선할 수 있기 때문에 주요 추가 지출 분야로 자리 잡고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united kingdom digital healthcare market size is projected to expand from USD 42.93 billion in 2025 and USD 46.36 billion in 2026 to USD 70.54 billion by 2031, registering a CAGR of 8.76% between 2026 to 2031.

This report is Segmented by Offering (Software, Services, Hardware), Technology (Telehealth, Remote Patient Monitoring, Mhealth, Healthcare Analytics and AI, and More), Deployment Mode (Cloud-Based, Hybrid, On-Premise), Application (Chronic Disease Management, and More), End User (Hospitals, and More), and Geography (United Kingdom). Market Forecasts are in Value (USD).

United Kingdom Digital Healthcare Market Trends and Insights

NHS Electronic Patient Record Rollouts Reach Critical Mass

As of the 2025 Digital Maturity Assessment, 93% of NHS providers had a live EPR, yet only 30% had integrated bi-directional data flows, which means the current wave centers on optimization rather than first-time installation. NHS England expects 97% of acute trusts to have EPR coverage by the end of 2026, so rollout work is still feeding demand across the UK digital healthcare market. Local NHS IT spending is projected to rise from GBP 4.9 billion, or USD 6.2 billion, in 2025/26 to GBP 6.8 billion, or USD 8.6 billion, by 2028/29, which gives platform vendors and service partners a longer runway for implementation and support work. The important commercial change is that revenue funding is now being used for EPR optimization, training, and workflow redesign through the NHS Frontline Productivity Programme, which widens spend beyond initial software licensing. This change keeps managed services, integration support, user training, and post-go-live consulting active even in trusts that have already completed major deployments, and it supports recurring rather than one-off contract value.

Virtual Ward Expansion Beyond Acute Settings

NHS England operated 12,825 virtual ward beds in March 2025, and the South East alone recorded more than 85,000 virtual ward admissions in 2024, which was 18% above the 2023 level. The NHS 10 Year Health Plan committed to a national procurement route for a proactive planned care platform, and it linked incentives more directly to community-based urgent care activity. One NHS-commissioned trial found Hospital at Home care to be less expensive than inpatient treatment, with average savings of GBP 2,265, or USD 2,860, per patient episode, and that figure is now shaping local business cases. Pathways for COPD, heart failure, and frailty are now being designed as virtual-first services rather than as add-on pilots, which changes where remote monitoring vendors sit in care delivery. That shift strengthens demand in the UK digital healthcare market for connected devices, workflow platforms, and home-setting data integration that can work within routine NHS operations.

Legacy Interoperability Debt Across NHS Estates

The 2025 Digital Maturity Assessment showed that only 30% of EPR-equipped NHS providers had integrated bi-directional data flows, and this remains one of the clearest limits on connected care growth. NHS England's Frontline Productivity Programme and the NHS Canonical Data Model are intended to narrow this gap, yet the board has stated that full benefits from the Single Patient Record program are not expected to be realized until 2030. Regions that still rely on incompatible systems face slower care pathway redesign, slower data exchange, and more expensive integration work, particularly where acute, community, and mental health services need to coordinate. This delay matters for the UK digital healthcare market because revenue tied to remote monitoring, shared care, and decision support depends on reliable data exchange between settings. Vendors that can demonstrate compliance with FHIR UK Core R4 and NHS GP Connect standards, therefore, have a clearer commercial advantage than those that still depend on bespoke links.

Other drivers and restraints analyzed in the detailed report include:

- NHS App as a National Digital Front Door

- AI-Enabled Clinical Workflow Automation

- Cybersecurity and Clinical Safety Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 59.27% of the UK digital healthcare market share in 2025, supported by EPR licensing, SaaS-based clinical platforms, and the fast commercial expansion of ambient voice and analytics tools. This leadership reflects structural demand rather than short-term momentum because NHS standardization around a limited set of EPR vendors and app ecosystems creates a large renewal base. The software layer also benefits from the fact that cloud-native clinical platforms are now being treated as long-term operating infrastructure rather than stand-alone projects. That makes procurement less episodic and more tied to multiyear transformation plans across trusts and integrated care systems. It also keeps software deeply embedded in the broader UK digital healthcare industry as trusts seek fewer systems with stronger clinical and administrative coverage.

Services is the fastest-growing segment, with the UK digital healthcare market size for services expected to expand at a 9.08% CAGR from 2026 to 2031. NHS organizations are shifting more budget toward managed services, implementation support, optimization work, and AI-as-a-service after major go-lives. EPR usability surveys showed only 34% of NHS staff felt their EPR made them more efficient, which helps explain why trusts are spending more on training, workflow redesign, and post-implementation support. Hardware remains smaller, but it still matters because virtual ward kits, connected wearables, and remote monitoring devices are central to home-based care models. The planned GBP 2 billion, or USD 2.5 billion, Clinical Digital Health Systems 2.0 framework also shows that NHS contracting is moving toward bundled software and service delivery rather than stand-alone product purchasing.

Telehealth and telemedicine held 35.79% of revenue in 2025, which kept them as the largest technology category in the UK digital healthcare market. Their lead still reflects the long aftereffects of pandemic-era adoption, especially in urgent access, follow-up visits, and pathway redesign for chronic care. Remote patient monitoring is also expanding under this technology base because virtual ward models continue to rely on connected devices, alert systems, and clinician dashboards. mHealth applications are benefiting from the wider function set of the NHS App, which increasingly supports forms, messaging, appointment management, and chronic care interactions. Digital health systems are consolidating around fewer platform providers, which keeps the technology stack more integrated across the UK digital healthcare industry.

Healthcare analytics and AI are the fastest-growing technology segments at an 8.98% CAGR through 2031, driven by predictive operations, decision support, and ambient voice documentation. The NHS Federated Data Platform and related AI safety programs are helping turn data infrastructure into a direct enabler of clinical and operational applications. OECD analysis identified the UK as a leading example of scalable cloud adoption in health and pointed to AI diagnostics procurement as a benchmark for public sector deployment. Digital therapeutics are also growing, but they remain more constrained because NICE evidence pathways still require long validation cycles before broad commissioning support builds. This leaves AI and analytics as the main incremental spending category because they can improve documentation, throughput, triage, and capacity management without always waiting for entirely new care pathways.

Complete Report Scope:

- By Offering

- Software

- Services

- Hardware

- By Technology

- Telehealth and Telemedicine

- Remote Patient Monitoring

- mHealth Applications

- Healthcare Analytics and AI

- Digital Health Systems

- Digital Therapeutics

- By Deployment Mode

- Cloud-Based

- Hybrid

- On-Premise

- By Application

- Chronic Disease Management

- Diagnostics and Decision Support

- Mental Health

- Preventive and Wellness Care

- Administration and Workflow Automation

- By End User

- Hospitals and NHS Trusts

- Primary Care and GP Practices

- Patients and Home-Care Settings

- Payers and Commissioners

- Pharmaceutical and Life Sciences Companies

List of Companies Covered in this Report:

- Accurx

- athenahealth

- Babylon Health

- Cera

- Current Health

- Dedalus S.p.A.

- Doccla

- DrDoctor

- EMIS Health

- Epic Systems

- Fielmann

- Graphnet Health

- Huma

- Intersystems

- KIND GmbH & Co. KG

- Livi

- Oracle Health

- Patients Know Best

- Koninklijke Philips

- System C Healthcare

- TPP

- Visionable

- Veradigm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NHS Electronic Patient Record Rollouts

- 4.2.2 Virtual Ward Expansion Beyond Acute Settings

- 4.2.3 NHS App as a National Digital Front Door

- 4.2.4 AI-Enabled Clinical Workflow Automation

- 4.2.5 Community Care Digitization and Home Monitoring

- 4.2.6 FHIR-Based Interoperability Standardization

- 4.3 Market Restraints

- 4.3.1 Legacy Interoperability Debt Across NHS Estates

- 4.3.2 Cybersecurity and Clinical Safety Compliance Burden

- 4.3.3 Long Validation Cycles for Regulated Software and AI Tools

- 4.3.4 Shortage of Clinical Informatics and Health Data Talent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Technology

- 5.2.1 Telehealth and Telemedicine

- 5.2.2 Remote Patient Monitoring

- 5.2.3 mHealth Applications

- 5.2.4 Healthcare Analytics and AI

- 5.2.5 Digital Health Systems

- 5.2.6 Digital Therapeutics

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 Hybrid

- 5.3.3 On-Premise

- 5.4 By Application

- 5.4.1 Chronic Disease Management

- 5.4.2 Diagnostics and Decision Support

- 5.4.3 Mental Health

- 5.4.4 Preventive and Wellness Care

- 5.4.5 Administration and Workflow Automation

- 5.5 By End User

- 5.5.1 Hospitals and NHS Trusts

- 5.5.2 Primary Care and GP Practices

- 5.5.3 Patients and Home-Care Settings

- 5.5.4 Payers and Commissioners

- 5.5.5 Pharmaceutical and Life Sciences Companies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accurx

- 6.3.2 athenahealth

- 6.3.3 Babylon Health

- 6.3.4 Cera

- 6.3.5 Current Health

- 6.3.6 Dedalus S.p.A.

- 6.3.7 Doccla

- 6.3.8 DrDoctor

- 6.3.9 EMIS Health

- 6.3.10 Epic Systems Corporation

- 6.3.11 Fielmann

- 6.3.12 Graphnet Health

- 6.3.13 Huma

- 6.3.14 InterSystems Corporation

- 6.3.15 KIND GmbH & Co. KG

- 6.3.16 Livi

- 6.3.17 Oracle Health

- 6.3.18 Patients Know Best

- 6.3.19 Philips

- 6.3.20 System C Healthcare

- 6.3.21 TPP

- 6.3.22 Visionable

- 6.3.23 Veradigm

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment