|

시장보고서

상품코드

2072750

면화 수확 기계 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cotton Harvesting Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

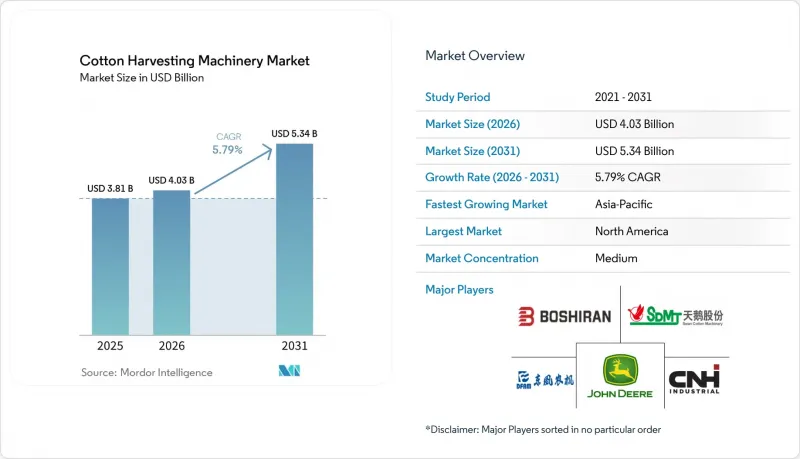

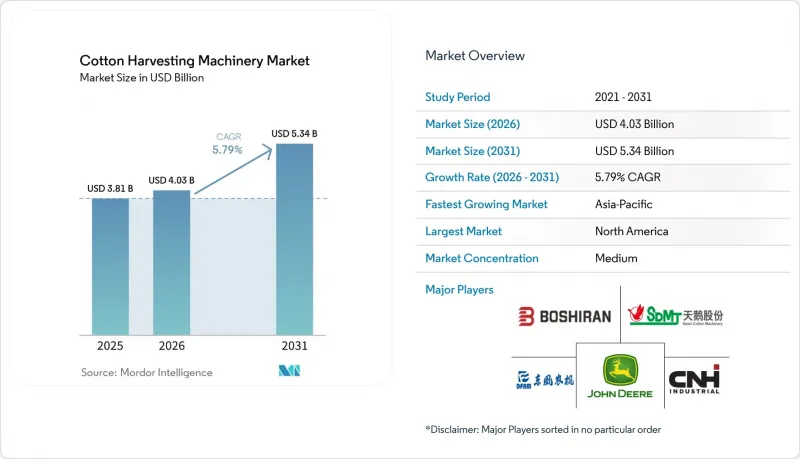

Mordor Intelligence에 의하면, 면화 수확 기계 시장 규모는 2025년 38억 1,000만 달러로 평가되었고, 2026년 40억 3,000만 달러로 추정되고, 2031년까지 53억 4,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 5.79%를 나타낼 전망입니다.

본 보고서는 유형별(스핀들식 수확기 및 스트리퍼식 수확기), 구동 방식별(자주식 및 트랙터 탑재식), 동력원별(디젤 동력, 전기 동력, 기타), 그리고 지역별(북미, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 면화 수확 기계 시장 동향 및 분석

심화되는 농업 인력 부족과 임금 상승

2021-2025년 주요 생산 지역 전반에서 면화 수확 인력이 대폭 감소함에 따라, 생산자들은 기계화 솔루션으로 전환할 수밖에 없었습니다. 미국의 H-2A 프로그램에서는 2025 회계연도에 39만 8,258건 이상의 취업 할당량이 승인되었으나, 주요 농업 주에서는 여전히 계절적인 노동력 부족 현상이 지속되고 있습니다. 캘리포니아주에서의 인건비 인상을 포함한 부정적인 영향은 대규모 기계화를 통한 면화 수확의 경제적 타당성을 더욱 강화하고 있습니다. 중국 신장 위구르 자치구에서는 농촌에서 도시로의 인구 이동이 진행되면서 면화 수확 인력을 확보하기 어려워지자, 해당 지역 전체에서 기계화 도입이 가속화되었습니다. 인도에서는 수작업에 따른 수확 비용이 여전히 높은 인력 부족 주를 대상으로, 정부의 지원 프로그램을 통해 농업 기계에 대한 보조금이 확대되었습니다. 호주에서도 계절적인 농업 인력 부족에 직면하면서, 주요 면화 생산 지역의 생산자들은 수작업으로 수확할 인력을 늘리는 대신 수확기를 추가로 임대하기 시작했습니다. 이러한 노동력과 임금에 대한 압박이 맞물리면서 기계화 수확의 투자 회수 기간이 단축되고, 면화 수확 장비에 대한 수요가 유지되고 있습니다.

자동화, 인공지능, GPS 안내를 통한 정밀 수확의 급속한 보급

면화 수확 기계는 추적성, 업무 효율성 및 섬유 품질 관리를 강화하도록 설계된 네트워크 연결형 정밀 농업 플랫폼으로 진화하고 있습니다. 2024년 소비자 가전 전시회(CES)에서 존 디어(John Deere)는 CP770 면화 수확 기계에 통합된 자동 면화 수확 기술을 선보였습니다. 이를 통해 모듈의 생산량, 수분 함량, 중량, GPS 위치 정보 및 수확 데이터를 실시간으로 모니터링할 수 있게 됩니다. 이 시스템은 면화 수확부터 면화 정제(진) 관리에 이르는 전체 워크플로우에 걸쳐 디지털 데이터 공유를 지원합니다. 이러한 첨단 수확 기능을 통해 생산자는 수확과 관련된 의사결정을 최적화하고, 수작업을 최소화하며, 밭에서 최종 용도에 이르기까지 면화의 추적성을 향상시킬 수 있습니다. 한편, 각 제조업체들은 첨단 위성 유도식 자동 조향 기술을 면화 수확 기계에 탑재하여, 수입 내비게이션 시스템에 비해 도입 비용을 절감하면서도 밭에서의 정확도와 작업 효율을 높이고 있습니다. 이러한 기술 발전은 즉시 업무상의 이점을 가져다주고 있으며, 미국, 중국, 호주 등 주요 면화 생산국의 생산자들은 면화 가격 변동에도 불구하고 장비 업그레이드를 가속화하고 있습니다.

높은 초기 구입 비용과 수명 주기 전반에 걸친 유지 관리 비용

6열 스핀들식 피커는 그 높은 자동화 수준, 대규모 수확 효율 및 뛰어난 가동 능력을 반영하여 일반적으로 가격이 높게 책정되어 있습니다. 그 가격은 구자라트 주나 카두나 주의 10헥타르 규모 농장에서 15-20년 동안 올릴 수 있는 순이익에 해당합니다. 연간 유지비에는 스핀들 교체, 유압 시스템 정비, 텔레매틱스 이용료 등이 포함됩니다. 보조금이 있다고는 하지만, 생산자들은 여전히 일반적인 농촌 지역의 대출 한도를 초과하는 막대한 자금 조달 필요에 직면해 있습니다. 아프리카에서는 합리적인 자금 조달 기회가 제한적이고 금리도 높기 때문에 인건비 상승에도 불구하고 도입이 제약을 받고 있습니다. 브라질의 중규모 농장에서는 설비 비용이 높아 연간 수익의 상당 부분을 차지하고 있습니다. 전문 금융업체는 잔존 가치에 따른 위험을 부담하기 때문에 경작 면적이 해마다 크게 변동하는 지역에서는 리스 계약 제공이 제한됩니다. 자본 비용이 낮아지거나 유연한 자금 조달 모델이 확대되기 전까지는 높은 도입 비용이 소규모 농가 지역에서의 보급을 계속해서 저해할 것입니다.

부문별 분석

2025년, 스핀들식 수확기는 면화 수확 기계 시장 점유율의 54.2%를 차지했으며, 고품질 업랜드 면과 장섬유 면 생산에서 그 우위를 보여주고 있습니다. 스트리퍼식 수확기는 두 번째로 큰 시장 점유율을 차지하고 있으며, 텍사스주, 오클라호마주, 호주에서 '원 오버' 건조 지대에서 재배하는 데 적합합니다. 이러한 광범위한 도입은 낮은 혼입률, 높은 섬유 유지 효율, 그리고 대규모 기계화 수확 작업과의 호환성 덕분에 촉진되고 있습니다.

미국과 브라질의 건조 지역 경작 면적이 확대됨에 따라, 2026-2031년 스트리퍼식 수확기의 연평균 성장률(CAGR)은 6.4%로 가장 높은 수준을 기록할 것으로 예상되는 반면, 스핀들식 수확기는 같은 기간 동안 비교적 완만한 성장에 그칠 것으로 전망됩니다. 1회 통과 시 연료 소비량이 18% 감소하고, 디어(Deere)사의 CS770 모델에서는 작업 속도가 20% 향상되며, 적극적인 스트리핑 기법에 대한 작물 품종의 내성이 높아지고 있는 점 등이 이러한 높은 성장률을 뒷받침하고 있습니다. 중국과 튀르키예에서는 섬유 품질과 관련된 엄격한 제재가 여전히 존재하기 때문에 교체 수요가 스핀들형 수확기의 판매를 계속해서 뒷받침할 것으로 보입니다. 이러한 요인들이 복합적으로 작용함에 따라, 2031년까지 면화 수확 기계 시장 규모는 보다 균형 잡힌 상태를 보일 전망이지만, 스핀들형이 주도적인 지위를 잃지는 않을 것입니다. 기계화에 대한 투자 증가와 수확 기술의 지속적인 발전으로 인해, 선진국과 신흥국 모두의 면화 시장에서 수요가 더욱 확대될 것으로 예측됩니다.

지역별 분석

북미는 2025년 매출의 36.8%를 차지했으며, 농업 인건비 상승과 기계화 및 정밀 농업의 확산에 힘입어 이 지역은 꾸준한 성장을 이어갈 것으로 전망됩니다. 주요 장비 제조업체들은 첨단 기술의 통합과 자동화 기능을 통해 입지를 지속적으로 강화하고 있으며, 면화 가격이 약세를 보이는 시기에도 지속적인 교체 및 업그레이드 수요를 뒷받침하고 있습니다.

아시아태평양은 정부의 보조금과 기계화 수확 장비의 투자 회수 기간을 단축하는 생산성 향상 프로그램의 지원에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.3%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 중국에서는 높은 기계화 수준이 꾸준한 교체 수요를 창출하고 있는 반면, 호주에서는 첨단 수확 시스템의 도입이 계속해서 견조한 추세를 보이고 있습니다. 인도에서는 소형이며 가격도 합리적인 수확기 개발로 인해, 현재 수작업에 의존하고 있는 소규모 농가에서의 도입이 촉진될 것으로 보이며, 세분화된 토지 소유 구조 전반에 걸쳐 목표 시장이 대폭 확대될 것으로 예측됩니다.

남미에서는 브라질을 필두로 꾸준한 성장이 예상됩니다. 브라질에서는 면화 재배 면적이 확대되고 기계화가 진행되면서 장비 수요를 뒷받침하고 있을 뿐만 아니라, 융자 프로그램을 통해 보다 저렴한 가격의 기계 도입이 촉진되고 있습니다. 아르헨티나에서는 수입 관련 제약과 환율 변동이 계속해서 구매 행태에 영향을 미치고 있습니다. 유럽 매출에서 차지하는 비중은 적으며, 일부 지역에서는 재배 면적이 확대되고 있음에도 불구하고, 규제 준수 요건과 높은 운영 비용으로 인해 신규 장비 도입이 제한되고 있습니다. 중동 및 아프리카를 합치면 시장 점유율은 다소 낮은 편이지만, 일부 시장에서는 정책 지원에 힘입어 기계화가 진행되고 있습니다. 그러나 자금 조달 기회가 제한적이고 서비스 인프라가 취약하기 때문에 사하라 이남의 일부 지역에서는 여전히 대규모 도입이 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the cotton harvester market size is projected to grow from USD 3.81 billion in 2025 and USD 4.03 billion in 2026 to USD 5.34 billion by 2031, registering a CAGR of 5.79% between 2026 and 2031.

This report is Segmented by Type (Spindle Pickers and Stripper Harvesters), by Mechanism (Self-Propelled and Tractor-Mounted), by Power Source (Diesel-Powered, Electric-Powered, and Others), and by Geography (North America, Asia-Pacific, and Others). The Market Forecasts are Provided in Terms of Value (USD).

Global Cotton Harvesting Machinery Market Trends and Insights

Escalating Farm-Labor Shortages and Wage Inflation

Cotton-picking labor pools shrank significantly across leading producing regions between 2021 and 2025, pushing growers toward mechanized solutions. The United States H-2A program certified more than 398,258 positions in fiscal 2025, yet seasonal labor shortages persisted in major agricultural states. Rising Adverse Effect Wage Rates, including increases in California, are strengthening the economic case for large-scale mechanized cotton harvesting. China's Xinjiang region experienced rural-to-urban migration, reducing the availability of cotton pickers and accelerating the adoption of mechanization across the region. In India, government support programs have increased subsidies for agricultural machinery in labor-deficit states where manual harvesting costs remain high. Australia also faced shortages of seasonal agricultural labor, prompting growers in key cotton-producing valleys to lease additional harvesters rather than expand manual crews. Together, these labor and wage pressures are shortening the payback period for mechanized harvesting and sustaining demand for cotton-harvesting equipment.

Rapid Adoption of Automation, Artificial Intelligence, and GPS-Guided Precision Harvesting

Cotton harvesters are evolving into connected, precision-agriculture platforms designed to enhance traceability, operational efficiency, and fiber-quality management. At the Consumer Electronics Show 2024, John Deere showcased automated cotton harvesting technologies integrated with the CP770 cotton picker, enabling real-time monitoring of module production, moisture, weight, GPS location, and harvest data. The system supports digital data sharing across cotton harvesting and gin-management workflows. These advanced harvesting capabilities enable growers to optimize harvesting decisions, minimize manual processes, and improve cotton traceability from the field to end use. Meanwhile, manufacturers are integrating advanced satellite-guided auto-steering technologies into cotton harvesters to enhance field precision and operational efficiency at lower implementation costs compared to imported navigation systems. These technological advancements are delivering immediate operational benefits, encouraging growers in major cotton-producing countries such as the United States, China, and Australia to accelerate equipment upgrades despite fluctuations in cotton prices.

High Upfront Purchase and Life-Cycle Maintenance Costs

A six-row spindle picker is typically priced at premium levels, reflecting its advanced automation, large-scale harvesting efficiency, and high operational capacity, equal to 15-20 years of net income for a 10-hectare farm in Gujarat or Kaduna. Annual upkeep includes spindle replacement, hydraulic rebuilds, and telematics fees. Even with subsidies, growers still face significant financing requirements that exceed typical rural credit ceilings. In Africa, limited access to affordable financing and high interest rates constrain adoption despite rising labor costs. Brazilian mid-sized farms face high equipment costs that absorb a large share of annual revenue. Specialty financiers carry residual-value risk, limiting lease offerings where acreage fluctuates significantly year to year. Until capital costs fall or flexible financing models expand, high entry prices will continue to restrict penetration in smallholder regions.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy Programs Accelerating Mechanization in China, India, and the United States

- Rising Global Cotton Consumption and Acreage Expansion

- Cotton-Price Volatility Delaying Capital-Equipment Spending

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spindle pickers accounted for 54.2% of the cotton harvester market share in 2025, reflecting their dominance in premium-grade upland and long-staple production. Stripper harvesters ranked second-largest, favored in once-over dryland operations across Texas, Oklahoma, and Australia. Their widespread adoption is driven by lower contamination rates, higher fiber retention efficiency, and compatibility with large-scale mechanized harvesting operations.

Stripper harvesters are projected to register the quickest 6.4% CAGR between 2026 and 2031 as dryland acreage expands in the United States and Brazil, while spindle units are set to advance more modestly over the same span. Fuel savings of 18% on once-over passes, a 20% speed gain on Deere's CS770, and rising cultivar tolerance for aggressive stripping methods all support the lead growth rate. Replacement demand in China and Turkey will still sustain spindle sales, as stringent fiber-quality penalties remain. The combined effect leaves the cotton harvester market size more balanced by 2031, without dislodging spindle leadership. Rising investments in mechanization and continuous advancements in harvesting technology are anticipated to further drive demand in both developed and emerging cotton markets.

Complete Report Scope:

- By Type

- Spindle Pickers

- Stripper Harvesters

- By Mechanism

- Self-propelled

- Tractor-mounted

- By Power Source

- Diesel-powered

- Electric-powered

- Hybrid-powered

- By Geography

- North America

- United States

- Canada

- Rest of the North America

- South America

- Brazil

- Argentina

- Rest of the South America

- Europe

- Germany

- Spain

- Greece

- Rest of Europe

- Asia-Pacific

- China

- India

- Australia

- Rest of Asia-Pacific

- Middle East

- Turkey

- Israel

- Rest of the Middle East

- Africa

- Egypt

- South Africa

- Rest of the Africa

- North America

Geography Analysis

North America generated 36.8% of 2025 revenue, and the region is projected to grow at a steady pace driven by rising farm-labor costs and increasing adoption of mechanized and precision agriculture practices. Leading equipment manufacturers continue to strengthen their presence through advanced technology integration and automation capabilities, supporting ongoing replacement and upgrade demand even during periods of cotton price softness.

Asia-Pacific is forecast to record the fastest 8.3% CAGR through 2031, supported by government subsidies and productivity improvement programs that reduce payback periods for mechanized harvesting equipment. High mechanization levels in China are generating steady replacement demand, while Australia continues to demonstrate strong adoption of advanced harvesting systems. In India, compact and affordable picker development is estimated to unlock adoption in smallholder farms that currently rely on manual harvesting, significantly expanding the addressable market across fragmented landholding structures.

South America is projected to advance steadily, led by Brazil where expanding cotton acreage and mechanization are supporting equipment demand, while credit programs are steering adoption toward more affordable machinery options. Argentina's import-related constraints and currency volatility continue to influence purchasing behavior. Europe holds a smaller share of revenue, with regulatory compliance requirements and higher operational costs limiting new equipment adoption despite underlying acreage expansion in select regions. The Middle East and Africa together account for a modest share, where policy support is improving mechanization in some markets, but limited financing access and weak service infrastructure continue to restrict large-scale adoption in several sub-Saharan regions.

- Deere & Company.

- CNH Industrial N.V.

- Mahindra and Mahindra Ltd.

- OJSC "Gomselmash"

- Shandong Swan Cotton Industrial Machinery Stock Co., Ltd.

- Changzhou Dongfeng Agricultural Machinery Group Co., Ltd.

- Xinjiang Boshiran Intelligent Agricultural Machinery Co., Ltd.

- Hubei Fotma Machinery Co., Ltd.

- Jiangsu World Agricultural Machinery Co., Ltd.

- ColhiCana Agricultural Machinery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating farm-labor shortages and wage inflation

- 4.2.2 Rapid adoption of automation, artificial intelligence, and GPS-guided precision harvesting

- 4.2.3 Government subsidy programs accelerating mechanization in China, India, and the United States

- 4.2.4 Rising global cotton consumption and acreage expansion

- 4.2.5 Proliferation of on-board round-bale module builders that cut logistics costs

- 4.2.6 Emergence of pay-per-use harvesting-as-a-service platforms in developing markets

- 4.3 Market Restraints

- 4.3.1 High upfront purchase and life-cycle maintenance costs

- 4.3.2 Cotton-price volatility delaying capital-equipment spending

- 4.3.3 Sparse dealer telematics infrastructure hindering predictive-maintenance adoption in emerging regions

- 4.3.4 Stricter soil-compaction and emission regulations raising redesign and compliance expenses

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Spindle Pickers

- 5.1.2 Stripper Harvesters

- 5.2 By Mechanism

- 5.2.1 Self-propelled

- 5.2.2 Tractor-mounted

- 5.3 By Power Source

- 5.3.1 Diesel-powered

- 5.3.2 Electric-powered

- 5.3.3 Hybrid-powered

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of the North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of the South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 Spain

- 5.4.3.3 Greece

- 5.4.3.4 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Australia

- 5.4.4.4 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Turkey

- 5.4.5.2 Israel

- 5.4.5.3 Rest of the Middle East

- 5.4.6 Africa

- 5.4.6.1 Egypt

- 5.4.6.2 South Africa

- 5.4.6.3 Rest of the Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company.

- 6.4.2 CNH Industrial N.V.

- 6.4.3 Mahindra and Mahindra Ltd.

- 6.4.4 OJSC "Gomselmash"

- 6.4.5 Shandong Swan Cotton Industrial Machinery Stock Co., Ltd.

- 6.4.6 Changzhou Dongfeng Agricultural Machinery Group Co., Ltd.

- 6.4.7 Xinjiang Boshiran Intelligent Agricultural Machinery Co., Ltd.

- 6.4.8 Hubei Fotma Machinery Co., Ltd.

- 6.4.9 Jiangsu World Agricultural Machinery Co., Ltd.

- 6.4.10 ColhiCana Agricultural Machinery