|

시장보고서

상품코드

2072796

줄기세포 은행 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Stem Cell Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

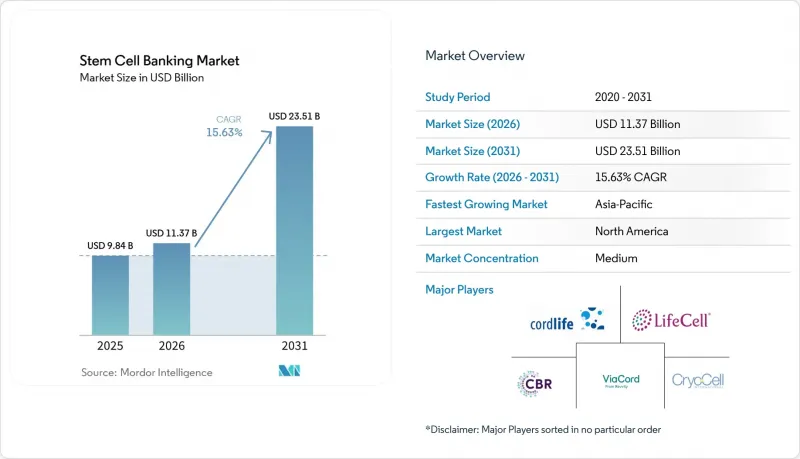

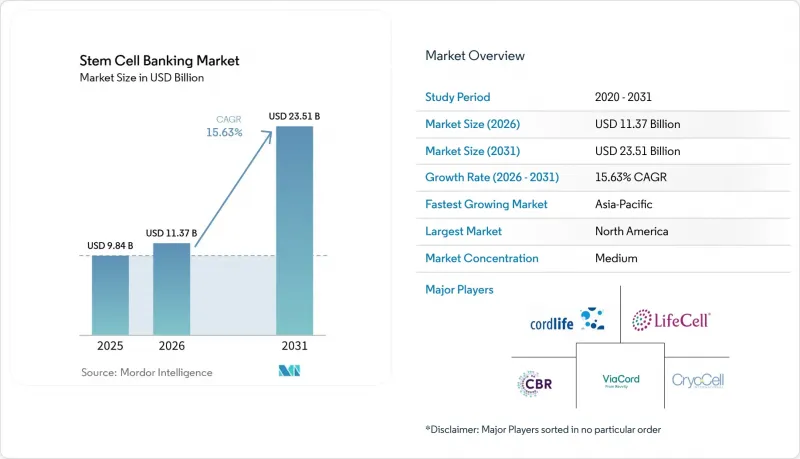

Mordor Intelligence에 의하면, 줄기세포 은행 시장 규모는 2025년에 98억 4,000만 달러로 평가되었고, 2026년 113억 7,000만 달러로 추정되고, 2031년까지 235억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 15.63%를 나타낼 전망입니다.

본 보고서는 뱅크 유형별(공공, 민간, 하이브리드), 줄기세포 공급원별(제대혈 등), 서비스 유형별(채취 및 운송 등), 용도별(맞춤형 뱅크 등), 최종 사용자별(병원 및 클리닉, 생명공학 및 제약 기업 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 줄기세포 은행 시장 동향 및 인사이트

제대혈 및 제대 조직 보존에 대한 수요 증가

제대혈의 용도가 기존의 혈액암 치료에 그치지 않고 확대되고 있는 만큼, 줄기세포 은행 시장은 성장을 거듭하고 있습니다. 2025년 12월, 중증 재생불량성 빈혈에 대한 '오미두비셀-ONLV'이 승인된 것은 화학적으로 강화된 제대혈 제제를 새로운 임상 현장에 도입하고 제조 기준을 한 단계 높였습니다는 점에서 큰 전환점이 되었습니다. 마찬가지로, 제대 조직 은행 사업도 발전하고 있습니다. 이는 제대 조직 유래 중간엽 줄기세포가 GMP 기준에 부합하는 제조 조건 하에서 강력한 증식 능력을 보이며, 오염 위험이 낮은 것으로 밝혀졌기 때문입니다. 이러한 과학적 진보 덕분에 민간 사업자들은 출산 시 제대혈과 제대 조직을 함께 제공하는 서비스를 제공할 수 있게 되었으며, 채취 방법을 변경하지 않고도 가족당 수익을 늘릴 수 있게 되었습니다. 현재 수요는 출산에 대한 인식 제고, 상담사 이용 편의성, 그리고 향후 활용 가치에 대한 명확한 설명에 힘입어 증가하고 있습니다.

재생의학 및 세포 치료 연구 확대

재생의학 및 세포 치료에 대한 관심이 높아짐에 따라, 신뢰성이 높은 생물학적 재료에 대한 수요가 확대되고 있으며, 줄기세포 은행은 적극적인 공급 플랫폼으로 변모하고 있습니다. 현재 임상 프로그램에서는 독립된 단위가 아닌 표준화된 재고가 요구되고 있습니다. 예를 들어, 제2상 임상시험에서는 통합된 제대혈 제제를 사용함으로써 1년 생존율이 96%에 달했고, 중증 이식편대숙주병도 나타나지 않았음이 입증되었으며, 이로 인해 특성이 충분히 규명된 대규모 재고의 중요성이 부각되고 있습니다. 또한, 수혈 의존성 지중해빈혈에 대한 동종 조혈모세포 이식의 발전으로 인해, 적합한 동종 이식 단위에 대한 수요가 확대되고 있습니다. 이러한 변화는 가족 대상 계약 외에도 의약품 공급 계약 및 조사용 조달 계약의 중요성이 점점 더 커지고 있음을 보여줍니다.

채취, 처리, 보존에 드는 평생 비용의 높음

줄기세포 은행 시장은 비용 측면에서 어려움을 겪고 있습니다. 민간 등록에는 채취비, 처리비, 장기 보존 비용이 모두 포함되기 때문에 가족 입장에서는 중대한 경제적 결정이 됩니다. 이 문제는 의료 수요가 높은 반면 가처분 소득이 제한적인 출산율이 높은 시장에서 더욱 두드러지게 나타나며, 인지도가 높아지고 있음에도 불구하고 시장 침투 속도를 둔화시키고 있습니다. 사업자에게도 규정 준수 체계, 검사, 초저온 보관 인프라, 물류에 드는 비용이 큰 부담이 되고 있습니다. 더 폭넓은 참여자들에게 비용을 분산시키고, 가족의 참여를 용이하게 하기 위해 하이브리드형이나 보험 연계형 비즈니스 모델이 등장하고 있습니다. 그러나 특히 가격에 민감한 시장에서 고품질의 서비스 기준과 합리적인 가격 사이의 균형을 맞추는 데 있어, 비용은 여전히 주요 제약 요인으로 작용하고 있습니다.

부문별 분석

2025년, 프라이빗 뱅킹은 은행형 수익의 60.15%를 차지했으며, 줄기세포 은행 시장이 가족의 자금 지원을 통한 가입 및 지속적인 보관 계약에 의존하고 있다는 사실이 부각되고 있습니다. 이 모델은 예측 가능한 현금 흐름을 확보하고, 다조직 패키지로의 업셀링을 지원하는 동시에, 보조금 및 공공 환급에 대한 의존도를 낮춥니다. 개인 등록을 통해 사업자는 고객과 직접 소통할 수 있으며, 고객 유지, 계약 갱신 및 추가 서비스 제공이 간소화됩니다. 공공형이나 하이브리드형이 주목을 받고 있는 반면, 상담, 가격 책정, 병원 접근성이 적절히 갖춰져 있는 경우, 가족들이 장기적인 이점을 기대하며 투자할 의향이 있기 때문에 프라이빗 뱅킹은 여전히 상업적 핵심을 이루고 있습니다.

공공 은행은 이식 기회를 확대하고, 기증자 풀을 다양화하며, 적합성이 높은 기증자 풀에 의존하는 동종 이식 치료 경로를 뒷받침합니다. 그 중요성은 비혈연자의 제대혈이 중요한 대안 수단이 되는 의료 서비스가 충분히 제공되지 않는 집단에서 더욱 커지고 있습니다. 2031년까지 연평균 성장률(CAGR) 17.10%를 나타낼 것으로 예측되는 하이브리드 뱅킹은 가족의 가치관과 보다 광범위한 임상적 유용성을 융합한 것입니다. 스위스의 하이브리드 모델과 대만의 StemCyte사가 추진하는 보험 연계형 이니셔티브는 하이브리드 구조가 임상적 품질을 유지하면서도 합리적인 가격과 참여율을 높일 수 있음을 보여주고 있습니다.

제대혈은 확립된 임상적 용도와 보존 방법에 대한 신뢰를 바탕으로, 2025년에는 줄기세포 은행 시장의 45.25%를 차지했습니다. 출산과의 연관성, 충분히 검증된 보관 방법, 그리고 입증된 역사적 이용 실적을 바탕으로, 가족 대상 은행 프로그램의 중심적인 위치를 계속해서 차지하고 있습니다. 제대 조직을 제대혈과 함께 사용하는 사례가 늘어나고 있어, 채취 기간을 변경하지 않고도 공급원의 다양화를 촉진하고 있습니다. 태반 및 치아 유래 줄기세포는 일부 프로그램에서 제공되고 있지만, 여전히 주요 동력이라기보다는 보조적인 역할에 그치고 있습니다.

2031년까지 연평균 성장률(CAGR) 17.20%를 나타낼 것으로 예측되는 지방 조직 유래 줄기세포는 비침습적인 채취 방법과 높은 중간엽 세포 수율 덕분에 주목을 받고 있습니다. 개발자들은 치료 용도로 사용하기 위해 정의가 명확하고 추적 가능한 원료를 선호하기 때문에 지방 조직 은행은 산업용 조달에서 중요한 역할을 하고 있습니다. 표준화된 밀폐형 처리 방식과 GMP 준수 워크플로우를 통해 일관성이 향상되어, 치료 및 연구 분야에서 대규모 활용을 뒷받침하고 있습니다. 현재 공급량의 주된 원천은 제대혈이지만, 시장의 성장세를 주도하고 있는 것은 지방 조직 유래 줄기세포입니다.

지역별 분석

2025년, 북미는 줄기세포 은행 시장에서 40.60%의 점유율을 차지했으며, 시장을 주도했습니다. 이는 민간 은행에 대한 높은 보급률, 확립된 병원 네트워크, 그리고 임상용 및 가정용 보관을 뒷받침하는 성숙한 품질 관리 체제에 힘입은 결과입니다. 미국은 높은 인증 기준과 제도적 인프라를 바탕으로, 계속해서 이 지역의 중심적인 위치를 차지하고 있습니다. 규제가 명확해짐에 따라 채취, 처리, 등록 관행이 표준화되면서 수요가 더욱 증가하고 있습니다. 북미 시장에서 규모, 신뢰도, 그리고 운영상의 규율이 결합된 점은 기존 주요 기업들에게 계속해서 유리하게 작용하고 있습니다.

유럽은 여전히 중요한 시장이지만, 업계 재편으로 인해 그 구조가 변화하고 있습니다. 2025년 5월, FamiCord AG는 체코와 슬로바키아의 줄기세포 은행 지분의 과반수를 인수하는 한편, 맞춤형 의료와 관련된 세포 보존 공정에 대한 특허도 취득했습니다. 이는 소규모 지역 은행이 난립하던 시장에서 보다 광범위한 기술 역량을 갖추고 충분한 자본력을 보유한 소수의 사업자로 전환되고 있음을 반영합니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 대규모 출생 코호트와 민간 및 하이브리드 모델의 도입 확대에 힘입어 2031년까지 연평균 성장률(CAGR)이 16.67%를 나타낼 것으로 전망됩니다. 중국과 인도는 긍정적인 인구 동향, 도시 지역의 소득 증가, 그리고 생명공학 지원 정책에 힘입어 수요를 주도하고 있습니다. 해당 지역에서는 사업자들이 저장 서비스를 재생의료 프로그램 및 제품 개발과 통합함으로써 시장이 발전하고 있습니다. 대만의 StemCyte가 도입한 보험 연계형 모델은 임상 경로를 유지하면서 접근성을 확대하는 유연한 가입 구조의 좋은 사례입니다.

중동 및 아프리카와 남미는 현재 시장 점유율은 작지만, 장기적인 성장 잠재력을 지니고 있습니다. 높은 출산율과 중산층의 의료비 지출 증가가 성장의 기회를 창출하고 있지만, 이를 실현하기 위해서는 비용 대비 효과 및 인지도 문제 해결이 필수적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the stem cell banking market size was valued at USD 9.84 billion in 2025 and is estimated to grow from USD 11.37 billion in 2026 to reach USD 23.51 billion by 2031, at a CAGR of 15.63% during the forecast period (2026-2031).

This report is Segmented by Bank Type (Public, Private, Hybrid), Stem Cell Source (Umbilical Cord Blood, and More), Service Type (Collection and Transportation, and More), Application (Personalized Banking, and More), End User (Hospitals and Clinics, Biotech and Pharma Companies, and More), and Geography (North America, Europe, Aand More). The Market Forecasts are Provided in Terms of Value (USD).

Global Stem Cell Banking Market Trends and Insights

Rising Demand for Cord Blood and Cord Tissue Preservation

The stem cell banking market is experiencing growth due to the expanded utility of cord blood, which is no longer limited to legacy blood cancer treatments. The approval of omidubicel-onlv for severe aplastic anemia in December 2025 marked a significant shift by introducing a chemically enhanced cord blood product to a new clinical setting and raising manufacturing standards. Similarly, cord tissue banking is advancing as mesenchymal stem cells from umbilical cord tissue demonstrate strong proliferative capacity and lower contamination risks under GMP-feasible production conditions. This scientific progress enables private operators to offer bundled cord blood and cord tissue services at birth, increasing revenue per family without altering collection methods. Demand is now driven by delivery-time awareness, counselor access, and clear communication of future-use value.

Expansion of Regenerative Medicine and Cell Therapy Research

The growing focus on regenerative medicine and cell therapy is driving demand for reliable biological materials, transforming stem cell banks into active supply platforms. Clinical programs now require standardized inventories rather than isolated units. For instance, a phase 2 trial demonstrated a 96% one-year survival rate and no severe graft-versus-host disease using pooled cord blood products, highlighting the importance of large, well-characterized inventories. Additionally, advancements in allogeneic hematopoietic stem cell transplantation for transfusion-dependent thalassemia are broadening demand for matched allogeneic units. This shift underscores the increasing relevance of pharmaceutical supply contracts and research procurement agreements alongside family subscriptions.

High Lifetime Cost of Collection, Processing, and Storage

The stem cell banking market faces affordability challenges as private enrollment combines collection fees, processing charges, and long-term storage costs, making it a significant financial decision for families. This issue is more pronounced in high-birth markets where medical needs are high, but disposable incomes are limited, slowing market penetration despite growing awareness. Operators also face high costs due to compliance systems, testing, cryogenic infrastructure, and logistics. Hybrid and insurance-linked models are emerging to distribute costs across broader participation, easing entry for families. However, cost remains a key restraint, especially in balancing premium service standards with affordability in price-sensitive markets.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use of Private Family Banking as a Long-Term Healthcare Option

- Increasing Acceptance of Allogeneic Stem Cell Transplantation

- Uncertain Clinical Utilization Rate of Stored Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, private banking accounted for 60.15% of bank-type revenue, highlighting the stem cell banking market's reliance on family-funded enrollments and recurring storage contracts. This model ensures predictable cash flow, supports upselling into multi-tissue packages, and reduces dependence on grants or public reimbursements. Personalized enrollment provides operators direct customer access, simplifying retention, renewals, and add-on services. While public and hybrid formats gain attention, private banking remains the commercial core due to families' willingness to invest in perceived long-term benefits when counseling, pricing, and hospital access align.

Public banking enhances transplant access, diversifies donor pools, and supports allogeneic treatment pathways reliant on well-matched inventories. Its importance grows in underrepresented populations where unrelated cord blood serves as a critical alternative. Hybrid banking, growing at a 17.10% CAGR through 2031, combines family value with broader clinical utility. Switzerland's hybrid model and StemCyte's insurance-linked initiative in Taiwan demonstrate how hybrid architecture can enhance affordability and participation while maintaining clinical quality.

Umbilical cord blood held 45.25% of the stem cell banking market in 2025, driven by its established clinical use and trust in preservation practices. It remains central to family banking programs due to its association with childbirth, well-understood storage methods, and validated historical use. Cord tissue is increasingly paired with cord blood, enhancing source diversification without altering the collection window. Placental and dental stem cells are offered in select programs but remain supplementary rather than primary drivers.

Adipose tissue-derived stem cells, growing at a 17.20% CAGR through 2031, are gaining traction due to minimally invasive collection and higher mesenchymal cell yield. Developers prefer defined, traceable starting materials for therapeutic applications, making adipose banking relevant for industrial procurement. Standardized closed-system processing and GMP-ready workflows enhance consistency, supporting large-scale use in therapy and research. While cord blood anchors current volumes, adipose tissue drives forward momentum in the market.

Complete Report Scope:

- By Bank Type

- Public Banking

- Private Banking

- Hybrid Banking

- By Stem Cell Source

- Umbilical Cord Blood

- Umbilical Cord Tissue

- Placental Stem Cells

- Dental Stem Cells

- Bone Marrow-Derived Stem Cells

- Adipose Tissue-Derived Stem Cells

- Others

- By Service Type

- Collection and Transportation

- Processing

- Testing and Analysis

- Storage

- By Application

- Personalized Banking

- Regenerative Medicine

- Cell Therapy

- Research and Drug Discovery

- Transplantation

- By End User

- Hospitals and Clinics

- Biotechnology and Pharmaceutical Companies

- Research Institutes

- Specialty Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America led the stem cell banking market with a 40.60% share, driven by strong private banking penetration, established hospital networks, and a mature quality framework supporting clinical and family-directed storage. The U.S. remains the region's anchor due to advanced accreditation standards and institutional infrastructure. Regulatory clarity further enhances demand by standardizing collection, processing, and registration practices. North America's combination of scale, trust, and operational discipline continues to benefit established players.

Europe remains a key market, though consolidation is reshaping its structure. In May 2025, FamiCord AG acquired majority stakes in Czech and Slovak stem cell banks, along with patents for cell preservation processes tied to personalized health therapies. This reflects a shift toward fewer, well-capitalized operators with broader technical capabilities, moving away from a fragmented market of smaller local banks.

Asia-Pacific is the fastest-growing region, with a 16.67% CAGR projected through 2031, supported by large birth cohorts and rising adoption of private and hybrid models. China and India drive demand due to favorable demographics, urban income growth, and supportive biotech policies. The region is advancing as operators integrate preservation services with regenerative medicine programs and product development. Taiwan's insurance-linked model from StemCyte exemplifies flexible enrollment structures expanding access while maintaining clinical pathways.

The Middle East, Africa, and South America currently hold smaller market shares but offer long-term growth potential. High birth rates and increasing middle-class healthcare spending create opportunities for expansion, provided affordability and awareness challenges are addressed.

- Americord Registry, LLC

- Biocell Private Limited

- CBR Systems, Inc.

- Cells4Life Group LLP

- China Cord Blood Corporation

- Cordlife Group

- Cryo-Cell International, Inc.

- CryoSave AG

- Cryoviva Biotech Pvt. Ltd.

- FamiCord AG

- FamilyCord, Inc.

- Future Health Biobank Limited

- Global Cord Blood

- LifeCell International Private Limited

- NeoStem, Inc.

- New England Cord Blood Bank, Inc.

- Smart Cells International Ltd

- StemCyte, Inc.

- Stemlife Berhad

- TransCell Biolife Pvt. Ltd.

- ViaCord, LLC

- Virgin Health Bank

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Cord Blood and Cord Tissue Preservation

- 4.2.2 Expansion of Regenerative Medicine and Cell Therapy Pipelines

- 4.2.3 Rising Use of Private Family Banking as a Long-Term Health Security Product

- 4.2.4 Increasing Acceptance of Allogeneic Stem Cell Transplants

- 4.2.5 Rising Banking of Perinatal Tissues Beyond Cord Blood

- 4.2.6 Automation and Closed-System Cryopreservation Improving Viability and Throughput

- 4.3 Market Restraints

- 4.3.1 High Lifetime Cost of Collection, Processing, and Storage

- 4.3.2 Uncertain Clinical Utilization Rate of Stored Units

- 4.3.3 Regulatory Complexity Across Public, Private, and Cross-Border Models

- 4.3.4 Limited Donor Awareness and Birth-Time Conversion Friction in Some Countries

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Bank Type

- 5.1.1 Public Banking

- 5.1.2 Private Banking

- 5.1.3 Hybrid Banking

- 5.2 By Stem Cell Source

- 5.2.1 Umbilical Cord Blood

- 5.2.2 Umbilical Cord Tissue

- 5.2.3 Placental Stem Cells

- 5.2.4 Dental Stem Cells

- 5.2.5 Bone Marrow-Derived Stem Cells

- 5.2.6 Adipose Tissue-Derived Stem Cells

- 5.2.7 Others

- 5.3 By Service Type

- 5.3.1 Collection and Transportation

- 5.3.2 Processing

- 5.3.3 Testing and Analysis

- 5.3.4 Storage

- 5.4 By Application

- 5.4.1 Personalized Banking

- 5.4.2 Regenerative Medicine

- 5.4.3 Cell Therapy

- 5.4.4 Research and Drug Discovery

- 5.4.5 Transplantation

- 5.5 By End User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Biotechnology and Pharmaceutical Companies

- 5.5.3 Research Institutes

- 5.5.4 Specialty Laboratories

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Americord Registry, LLC

- 6.3.2 Biocell Private Limited

- 6.3.3 CBR Systems, Inc.

- 6.3.4 Cells4Life Group LLP

- 6.3.5 China Cord Blood Corporation

- 6.3.6 Cordlife Group Limited

- 6.3.7 Cryo-Cell International, Inc.

- 6.3.8 CryoSave AG

- 6.3.9 Cryoviva Biotech Pvt. Ltd.

- 6.3.10 FamiCord AG

- 6.3.11 FamilyCord, Inc.

- 6.3.12 Future Health Biobank Limited

- 6.3.13 Global Cord Blood Corporation

- 6.3.14 LifeCell International Private Limited

- 6.3.15 NeoStem, Inc.

- 6.3.16 New England Cord Blood Bank, Inc.

- 6.3.17 Smart Cells International Ltd

- 6.3.18 StemCyte, Inc.

- 6.3.19 Stemlife Berhad

- 6.3.20 TransCell Biolife Pvt. Ltd.

- 6.3.21 ViaCord, LLC

- 6.3.22 Virgin Health Bank

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment