|

시장보고서

상품코드

2072798

AI 기반 의료 챗봇 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-Based Healthcare Chatbots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

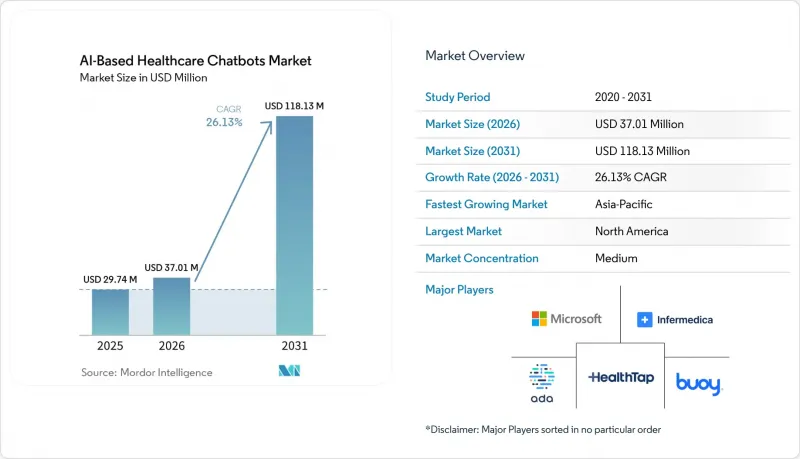

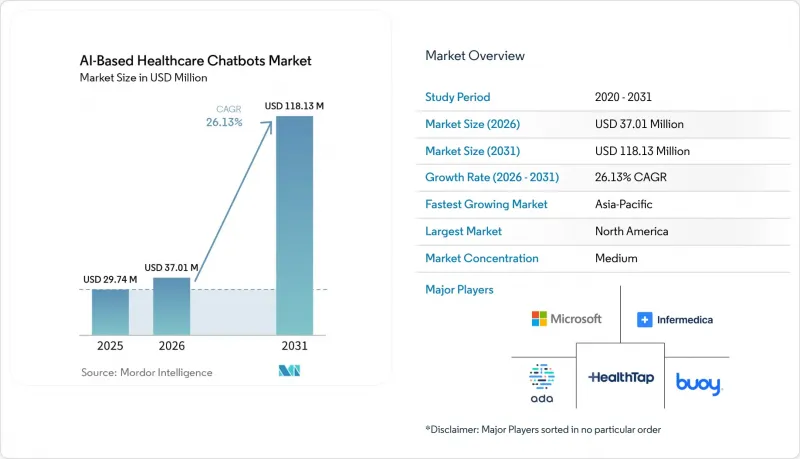

Mordor Intelligence에 의하면, AI 기반 의료 챗봇 시장은 2025년 2,974만 달러로 평가되었고, 2026년에는 3,701만 달러로 추정되고, 2026-2031년 CAGR 26.13%로 성장을 지속할 전망이며, 2031년에는 1억 1,813만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어, 서비스), 배포 방식별(클라우드 기반, 온프레미스형, 하이브리드형), 용도별(증상 확인, 예약 처리, 기타), 최종 사용자별(의료 제공업체, 환자 및 간병인, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 기반 의료 챗봇 시장 동향 및 인사이트

연중무휴 24시간 환자 참여 및 안내에 대한 수요 증가

환자 수가 증가함에 따라 진료 시간 외 전화 응대 및 접수 팀에 끊임없는 부담이 가해지고 있으며, 많은 의료 현장에서 상시 이용 가능한 디지털 소통 수단이 접근성 측면에서 핵심적인 요건으로 대두되고 있습니다. Druid AI의 2025-2026년 벤치마크 조사에 따르면, 이 회사의 의료 분야 전체 고객 기반에서 환자 신원 확인, 예약 관리 및 환자용 FAQ가 합쳐서 챗봇 워크플로우의 57%를 차지하고 있으며, 이는 '정문(초기 대응)'에 대한 접근이 AI 기반 의료 챗봇 시장의 주요 수요 축으로 계속 자리 잡고 있음을 뒷받침하고 있습니다. 이러한 경향이 중요한 이유는 병원, 진료소, 디지털 헬스 프로그램 전반에 걸쳐 매우 빈번하게 발생하는 일상적인 내비게이션 업무가 수요를 주도하고 있음을 보여주기 때문입니다. 또한, Wolters Kluwer사가 2026년에 실시한 조사에 따르면, 임상의와 환자 모두의 70%가 AI를 통해 건강 문해력과 참여도가 향상될 것이라고 생각하는 것으로 나타났으며, 이에 따라 환자용 도구에 대한 자금 지원에 대한 조직의 의지가 높아지고 있습니다. 이러한 의료 제공업체 측의 압력과 환자 측의 수용이 맞물리면서, AI 기반 의료 챗봇 시장은 기존의 디지털 참여 주기보다 더 폭넓은 기반을 구축하고 있습니다. 또한, 이는 구매자가 연중무휴 24시간 대화형 접근을 단순한 서비스의 부가 기능이 아닌, 케어 내비게이션의 일부로 인식하게 되었음을 의미합니다.

트리아지, 예약, 치료 배정 워크플로우의 신속화

AI 기반 의료 챗봇 시장은 환자가 처음 증상을 보고한 후 임상 진료 경로가 결정되기까지 걸리는 시간을 단축해 주는 분류 도구를 통해 지지를 넓혀가고 있습니다. Ada Health는 2026년 4월, CUF Hospitais와의 공동 임상 AI 연구에서 진료 시작 전 임상적으로 적절한 치료를 받는 환자의 비율이 29.8%에서 64.4%로 증가했다고 보고했습니다. 이 조사에서는 응급실을 방문할 예정이었던 환자의 40%가, 독립적인 의사 패널이 적절하다고 판단한 응급도가 낮은 의료시설로 진료처를 변경한 사실도 밝혀졌습니다. Infermedica가 2026년에 출시한 'Conversational Triage'은 대규모 언어 모델과 베이즈 모델을 결합한 것으로, 이 분야가 정적인 증상 트리에서 보다 구조화된 임상 내비게이션으로 전환되고 있음을 보여줍니다. 이러한 변화는 AI 기반 의료 챗봇 시장에 있어 중요합니다. 왜냐하면 실제 환자와의 대화에서는 의학적으로 모호한 사례가 빈번하게 발생하며, 이러한 사례들은 획일적인 대본만으로는 적절히 처리할 수 없기 때문입니다. 남은 과제는 운영상의 통합입니다. 트리아지의 결과는 임상 의사와의 상담이 시작되기 전에 전자건강기록(EHR) 내에서 이용 가능해질 때 비로소 최대의 가치를 창출하기 때문입니다.

환각이나 잘못된 지침으로 인한 임상적 위험

임상상의 잘못된 정보는 AI 기반 의료 챗봇 시장에서 여전히 가장 큰 도입 장벽으로 남아 있습니다. 이는 환자용 도구가 일반 소비자용 AI보다 훨씬 더 엄격한 안전성 기준에 따라 평가되기 때문입니다. 마운트 시나이 의과대학의 아이칸 의과대학(Icahn School of Medicine at Mount Sinai) 연구진은 또한 챗봇이 잘못된 의료 정보를 유포하는 경우가 많다는 사실을 발견했으나, 간단한 안전 조치 프롬프트를 적용함으로써 환각 발생률이 크게 감소했습니다. 이 연구에서는 구조화된 프롬프트, 함수 호출 및 검색 강화 생성(RAG)을 통해 대조 실험에서 중대한 '환각'이 최대 75% 감소한 것으로 나타났습니다. 이로 인해 AI 기반 의료 챗봇 시장에는 위험을 완화할 수 있는 명확한 방향성이 보이지만, 한편으로는 대기업이 본격적인 실운용을 승인하기 전에 공급업체가 보안 아키텍처에 투자해야 함을 의미하기도 합니다.

부문별 분석

2025년 기준으로 AI 기반 의료 챗봇 시장 점유율의 64.27%를 소프트웨어가 차지했으며, 2031년까지 연평균 성장률(CAGR) 26.92%를 나타낼 것으로 예측됩니다. 이러한 규모와 성장률의 조합은 대부분의 의료 시스템이 제공업체 네트워크 전체에 본격적으로 도입하기 전에 여전히 플랫폼 라이선스를 구매하고 있음을 보여줍니다. 소프트웨어 분야에 지출이 집중되는 이유는 구독형 플랫폼이 서비스 주도형 프로젝트보다 신속하게 구축될 수 있고, 일반적으로 더 안정적인 지속 수익을 기대할 수 있기 때문입니다. 또한, 증상 분류, 접수, 환자 대상 메시지 전송, 사후 관리에 이르는 전체 워크플로우의 표준화 과정을 구매자에게 더욱 명확하게 제시해 줍니다. AI 기반 의료 챗봇 시장의 현 단계에서 그 잠재력을 충분히 발휘하기 전이라 하더라도 소프트웨어가 지출의 주요 축을 차지하고 있는 것은 바로 그 때문입니다.

의료 시스템이 공급업체 선정 단계에서 실제 전자건강기록(EHR)과의 통합, 워크플로우 재설계, 모델 거버넌스 업무로 전환됨에 따라 서비스 시장의 중요성은 더욱 커질 것입니다. 이러한 요구 사항은 도입 시 현지 개인정보 보호 규정, 임상 심사 절차, 조달 요건을 준수해야 하는 경우에 특히 두드러집니다. Infermedica사가 2026년 'Conversational Triage'의 EU MDR 인증 획득을 위해 노력하고 있다는 점은 규정 준수 지원이 별도로 구매해야 하는 것이 아니라 소프트웨어 제안의 부가가치를 더하는 확장 기능으로 자리 잡고 있음을 보여줍니다. 순수 소프트웨어 공급업체에게 있어 장기적인 위험 요소는 하이퍼스케일러들이 챗봇 기능을 더욱 광범위한 헬스케어 클라우드 서비스에 지속적으로 통합해 나갈 가능성이 있으며, AI 기반 의료 챗봇 시장이 성숙해짐에 따라 가격 측면의 압박이 커질 것이라는 점입니다.

2025년에는 클라우드 도입이 매출의 68.22%를 차지했습니다. 이는 초기 비용 부담이 적고, 중규모 의료 제공업체나 디지털 헬스 기업이 도입하기 쉽다는 점을 반영한 것입니다. 도입 속도가 온프레미스 환경 관리보다 더 중요하게 여겨지는 경우, 클라우드는 여전히 기본 모델로 자리 잡고 있습니다. 또한, 대규모 아키텍처 결정을 내리기 전에 환자 참여 및 라우팅 도구를 테스트하고자 하는 조직에게도 유용한 선택지입니다. 그렇다고는 해도, 클라우드가 주류를 이루고 있다고 해서 AI 기반 의료 챗봇 시장에서 거버넌스 관련 우려가 해소된 것은 아닙니다. 대규모 의료 시스템에서는 보호 대상인 의료 정보, 감사 기록 및 데이터의 보관 장소에 대해 여전히 강력한 관리가 요구되고 있습니다.

하이브리드 시장 규모는 2031년까지 연평균 성장률(CAGR) 27.17%를 나타낼 것으로 예측되며, 이는 AI 기반 의료 챗봇 시장 전체의 성장 속도를 웃도는 수준입니다. 이는 대규모 의료 서비스 제공업체들이 실용적인 관점에서 클라우드 기반 모델의 성능과 기밀 데이터 및 통합 계층에 대한 보다 엄격한 온프레미스 관리를 결합한 방식을 선호하고 있음을 반영합니다. 온프레미스형 도입은 인도나 중국 일부 지역 등, 현지화 규제나 내부 보안 정책이 엄격한 환경에서 여전히 틈새 역할을 담당하고 있습니다. 따라서 기업들이 벤더 리스크 평가를 체계화해 나가고, AI 기반 의료 챗봇 시장이 유연한 도입 모델을 더욱 중시하게 됨에 따라 하이브리드형 도입은 계속해서 증가할 것으로 보입니다.

지역별 분석

2025년, 북미는 AI 기반 의료 챗봇 시장 점유율의 41.22%를 차지했습니다. 이는 해당 지역의 성숙한 전자건강기록(EHR) 기반, 원격의료의 활발한 활용, 그리고 선진적인 AI 조달 활동을 반영한 것입니다. 또한, 해당 지역에는 기업 전체를 아우르는 디지털 계약을 체결하고, 장기적인 도입 주기에 자금을 지원할 수 있는 대규모 의료 시스템이 밀집해 있다는 점도 강점으로 꼽힙니다. 또한, 아마존과 마이크로소프트가 기존 기업들과의 관계를 활용해 의료 특화형 AI 기능을 실제 운영 환경에 도입하고 있기 때문에 북미에서는 경쟁 압박도 가장 심합니다. 상위 계층에서는 플랫폼 보급률이 높은 편이지만, 소규모 의사 그룹이나 연방 공인 의료 센터(FQHC)의 경우, 저렴한 비용으로 EHR과 연동되는 도구에 대한 수요가 여전히 견조하게 유지되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 28.22%를 기록하며 성장할 것으로 예상되며, AI 기반 의료 챗봇 시장에서 가장 두드러진 성장세를 보일 지역 부문이 될 것입니다. 이러한 성장은 충분한 의료 서비스를 받지 못하고 있는 대규모 인구층, 스마트폰 보급률의 상승, 그리고 서비스의 도달 범위를 확대하기 위한 공공 디지털 헬스 프로그램의 활용에 힘입어 이루어지고 있습니다. 2026년 2월에 발표된 인도의 '의료 분야의 인공지능 전략'에서는 AI 거버넌스를 '아유슈만 바라트 디지털 미션'이라고 밝히며, AIIMS 델리, PGIMER 찬디가르, AIIMS 리시케시를 AI 우수 센터로 지정했습니다. 또한, 인도의 'eSanjeevani' 플랫폼은 정책 지원과 디지털 채널이 연계됨으로써, AI와 연계된 공중보건 인프라가 국민 전체를 대상으로 어떻게 기능할 수 있는지를 보여주고 있습니다. 한국, 일본, 호주에서는 도입당 지출액이 높은 반면, 인도와 중국은 앞으로도 수요의 주요 거점으로 남을 전망입니다.

유럽은 디지털 헬스 정책의 추진력과 규제 대상인 AI 도구에 대한 의료 제공업체들의 높은 관심에 힘입어, AI 기반 의료 챗봇 시장에서 지역별 점유율 2위를 차지하고 있습니다. 가장 큰 변화는 규제 측면에서 나타납니다. EU AI법에서 의료용 AI에 대한 '고위험' 요건이 2026년 8월 2일에 전면 시행됨에 따라, 적합성 평가, 투명성, 시판 후 감시에 대한 부담이 증가했기 때문입니다. 이러한 기준의 상향 조정은 단기적으로는 복잡성을 초래하겠지만, 인증 가능한 컴플라이언스 아키텍처에 조기에 투자하는 벤더의 입지를 강화하는 결과도 가져올 것입니다. 중동 및 아프리카은 GCC(걸프협력회의)의 의료 디지털화 프로그램에 힘입어 여전히 초기 단계에 머물러 있습니다. 한편, 남미에서는 브라질이 주도하고 있지만, 의료 시스템의 자금 조달 및 조달 주기의 장기화로 인해 여전히 제약받기 쉬운 상황에 놓여 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the AI-based healthcare chatbots market is expected to grow from USD 29.74 million in 2025 to USD 37.01 million in 2026 and is forecasted to reach USD 118.13 million by 2031 at 26.13% CAGR over 2026-2031.

This report is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premises, Hybrid), Application (Symptom Checking, Appointment Scheduling, and Others), End-User (Healthcare Providers, Patients and Caregivers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Based Healthcare Chatbots Market Trends and Insights

Rising Demand for 24/7 Patient Engagement and Navigation

Patient volumes are putting steady pressure on after-hours phone lines and front-desk teams, which is making always-on digital engagement a core access requirement in many care settings. Druid AI's 2025-2026 benchmark showed that patient identity and verification, appointment management, and patient FAQs together represented 57% of chatbot workflow volume across its healthcare customer base, which confirms that front-door access remains the main demand anchor for the AI-based healthcare chatbots market. This pattern matters because it shows that demand is being led by routine navigation tasks that appear in very high volumes across hospitals, clinics, and digital health programs. Wolters Kluwer's 2026 survey also found that 70% of both clinicians and patients believe AI can improve health literacy and engagement, which increases organizational willingness to fund patient-facing tools.That combination of provider-side pressure and patient-side acceptance gives the AI-based healthcare chatbots market a broader base than earlier digital engagement cycles. It also means buyers are now treating 24/7 conversational access as part of care navigation, not as a simple service add-on.

Faster Triage, Appointment, and Care Routing Workflows

The AI-based healthcare chatbots market is gaining support from triage tools that reduce the time between a patient's first report of symptoms and the point of clinical routing. Ada Health reported in April 2026 that its clinical AI study with CUF Hospitais increased the share of patients receiving clinically appropriate care from 29.8% to 64.4% before the visit began. The same study found that 40% of patients who had planned to visit the emergency department shifted to a lower-acuity care setting that an independent physician panel judged appropriate. Infermedica's 2026 launch of Conversational Triage, which combines large language models with Bayesian models, shows how this category is moving beyond static symptom trees toward more structured clinical navigation. That shift is important for the AI-based healthcare chatbots market because medically ambiguous cases are common in real patient conversations and cannot be managed well by rigid scripts alone. The remaining bottleneck is operational integration, because triage outputs create the most value when they are available inside the EHR before the clinician visit starts.

Clinical Risk from Hallucinated or Incorrect Guidance

Clinical misinformation remains the largest adoption brake on the AI-based healthcare chatbots market because patient-facing tools are judged against safety expectations that are much stricter than those in general consumer AI. Researchers at the Icahn School of Medicine at Mount Sinai also found that chatbots often expanded false medical information, although a simple safeguard prompt sharply reduced hallucination incidence. The same study showed that structured prompting, function calling, and retrieval-augmented generation reduced major hallucinations by as much as 75% in controlled tests. That leaves the AI-based healthcare chatbots market with a clear path to mitigation, but it also means vendors must invest in safety architectures before large enterprises will approve full live deployment.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Telehealth, Virtual Care, and Remote Monitoring

- Increasing Need for Clinician Workflow Offload and Call Deflection

- Integration Complexity with EHR, CRM, and Payer Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 64.27% of the AI-based healthcare chatbots market share in 2025 and is also projected to grow at 26.92% CAGR through 2031. This combination of scale and growth shows that most health systems are still buying platform licenses before they reach full deployment across their provider networks. The software layer attracts spending because subscription platforms can be rolled out faster than service-led projects and usually carry stronger recurring revenue economics. It also gives buyers a clearer path to standardization across symptom triage, intake, patient messaging, and follow-up workflows. In the current phase of the AI-based healthcare chatbots market, that makes software the main spending anchor even before utilization reaches its full potential.

The services market should expand in importance as health systems move from vendor selection into actual EHR integration, workflow redesign, and model governance work. Those needs are especially visible where deployments must fit local privacy rules, clinical review processes, and procurement requirements. Infermedica's work toward EU MDR certification for Conversational Triage in 2026 illustrates how compliance support is becoming a value-added extension of the software proposition rather than a separate purchase. The long-term risk for pure software vendors is that hyperscalers may continue bundling chatbot functions into broader health cloud offerings, which can pressure pricing as the AI-based healthcare chatbots market matures.

Cloud deployment held 68.22% of revenue in 2025, which reflects its lower upfront burden and its ease of adoption for mid-sized providers and digital health companies. Cloud remains the default model where speed of implementation matters more than local infrastructure control. It also works well for organizations that want to test patient engagement and routing tools before making larger architectural decisions. Even so, cloud leadership does not mean governance concerns have disappeared inside the AI-based healthcare chatbots market. Large health systems still need strong control over protected health information, audit trails, and data residency.

Hybrid deployment is forecasted to grow at 27.17% CAGR through 2031, which places it ahead of the broader AI-based healthcare chatbots market. This reflects the practical preference of large providers for cloud-based model performance combined with tighter local control over sensitive data and integration layers. On-premises deployment still holds a niche role in settings where localization rules or internal security policy are strict, including parts of India and China. Hybrid adoption is therefore likely to keep rising as enterprises formalize vendor risk reviews and as the AI-based healthcare chatbots market places more value on flexible deployment models.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Symptom Checking and Triage

- Appointment Scheduling and Reminders

- Medication and Drug Information Assistance

- Patient Education and Care Navigation

- Mental Health and Behavioral Support

- Administrative and Billing Support

- By End-User

- Healthcare Providers

- Patients and Caregivers

- Payers and Insurance Companies

- Life Sciences and CROs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.22% of the AI-based healthcare chatbots market share in 2025, which reflects the region's mature EHR base, strong telehealth use, and advanced AI procurement activity. The region also benefits from a dense concentration of large health systems that can sign enterprise-wide digital agreements and fund long implementation cycles. Competitive pressure is also highest in North America because Amazon and Microsoft are already using existing enterprise relationships to push healthcare-specific AI capabilities into live environments. Even with strong platform coverage at the top end, smaller physician groups and federally qualified health centers still represent a durable opening for lower-cost, EHR-linked tools.

Asia-Pacific is forecasted to grow at 28.22% CAGR through 2031, which makes it the fastest-growing regional segment in the AI-based healthcare chatbots market. Growth is supported by large underserved populations, rising smartphone access, and the use of public digital health programs to extend service reach. India's Strategy for Artificial Intelligence in Healthcare, published in February 2026, linked AI governance to the Ayushman Bharat Digital Mission and named AIIMS Delhi, PGIMER Chandigarh, and AIIMS Rishikesh as AI Centres of Excellence. India's eSanjeevani platform also shows how AI-linked public health infrastructure can operate at population scale when policy support and digital channels move together. South Korea, Japan, and Australia offer higher spending per deployment, while India and China remain the main volume centers for future demand.

Europe accounts for the second-largest regional share in the AI-based healthcare chatbots market, supported by digital health policy momentum and strong provider interest in regulated AI tools. The biggest shift is regulatory, because the EU AI Act's full high-risk obligations for healthcare AI came into effect on August 2, 2026, which raised the burden for conformity assessment, transparency, and post-market monitoring. That higher bar creates short-term complexity, but it also strengthens the position of vendors that invest early in certifiable compliance architecture. The Middle East and Africa remains an earlier-stage region led by GCC healthcare digitalization programs, while South America is led by Brazil and remains more constrained by health system financing and longer procurement cycles.

- 98point6 Technologies, Inc.

- Ada Health GmbH

- Amazon Web Services, Inc.

- Babylon Health

- Buoy Health, Inc.

- Conversa Health, Inc.

- Google LLC

- Healthily LTD.

- HealthTap, Inc.

- IBM

- Infermedica

- K Health, Inc.

- Microsoft

- Nuance Communications, Inc.

- Orbita, Inc.

- PACT Care BV

- Sensely, Inc.

- Woebot Health

- Wysa Ltd.

- Your.MD Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for 24/7 Patient Engagement and Navigation

- 4.2.2 Faster Triage, Appointment, and Care Routing Workflows

- 4.2.3 Expansion of Telehealth, Virtual Care, and Remote Monitoring

- 4.2.4 Increasing Need for Clinician Workflow Offload and Call Deflection

- 4.2.5 Multilingual Patient Access Across Fragmented Care Networks

- 4.2.6 Use of Chatbots for Medication Adherence and Follow-Up Nudges

- 4.3 Market Restraints

- 4.3.1 Clinical Risk from Hallucinated or Incorrect Guidance

- 4.3.2 Integration Complexity with EHR, CRM, and Payer Systems

- 4.3.3 Patient Trust Gaps for Sensitive Health Interactions

- 4.3.4 Data Privacy, Consent, and Model Governance Burden

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Symptom Checking and Triage

- 5.3.2 Appointment Scheduling and Reminders

- 5.3.3 Medication and Drug Information Assistance

- 5.3.4 Patient Education and Care Navigation

- 5.3.5 Mental Health and Behavioral Support

- 5.3.6 Administrative and Billing Support

- 5.4 By End-User

- 5.4.1 Healthcare Providers

- 5.4.2 Patients and Caregivers

- 5.4.3 Payers and Insurance Companies

- 5.4.4 Life Sciences and CROs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 98point6 Technologies, Inc.

- 6.3.2 Ada Health GmbH

- 6.3.3 Amazon Web Services, Inc.

- 6.3.4 Babylon Health

- 6.3.5 Buoy Health, Inc.

- 6.3.6 Conversa Health, Inc.

- 6.3.7 Google LLC

- 6.3.8 Healthily LTD.

- 6.3.9 HealthTap, Inc.

- 6.3.10 IBM Corporation

- 6.3.11 Infermedica

- 6.3.12 K Health, Inc.

- 6.3.13 Microsoft Corporation

- 6.3.14 Nuance Communications, Inc.

- 6.3.15 Orbita, Inc.

- 6.3.16 PACT Care BV

- 6.3.17 Sensely, Inc.

- 6.3.18 Woebot Health

- 6.3.19 Wysa Ltd.

- 6.3.20 Your.MD Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment