|

시장보고서

상품코드

2072812

헬스케어 및 생명과학 분야 자연어처리(NLP) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)NLP In Healthcare and Life Science - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

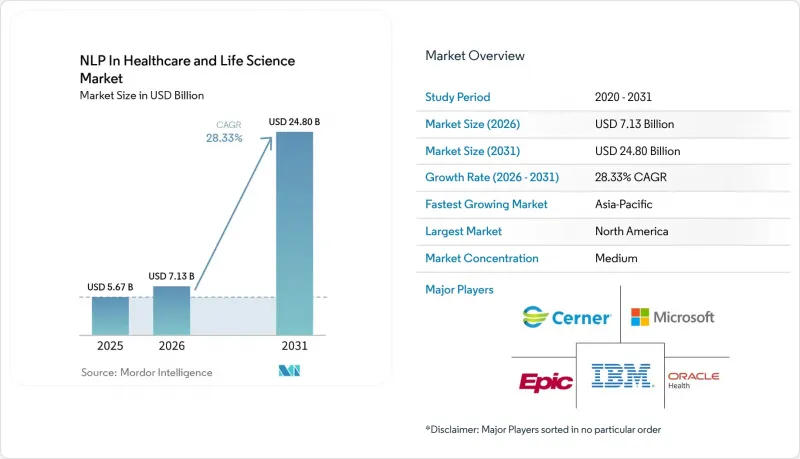

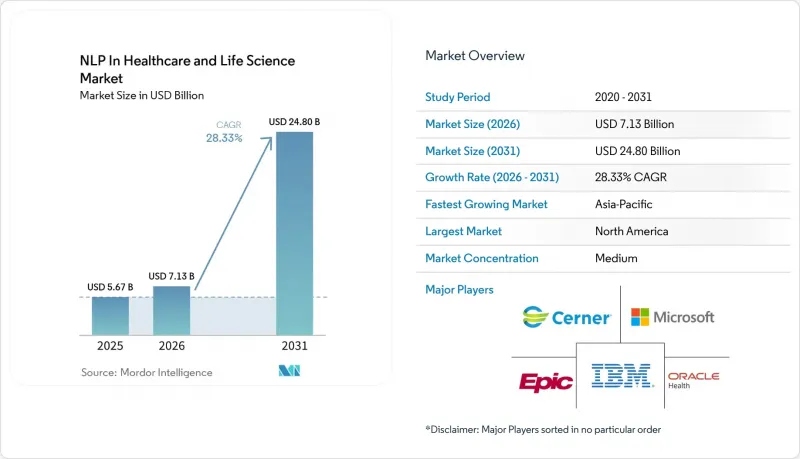

Mordor Intelligence에 의하면, 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장 규모는 2025년 56억 7,000만 달러로 평가되었고, 2026년에는 71억 3,000만 달러로 추정되고, 2031년까지 248억 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 28.33%로 성장할 전망입니다.

본 보고서는 제공 방식별(클라우드 기반, 온프레미스형, 하이브리드형), NLP 유형별(NLU, NLG), NLP 기술별(NER, OCR, 감정 분석, 텍스트 분류, 토픽 모델링 등), 용도별, 최종 사용자별, 조직 규모별(대기업, 중소기업), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

헬스케어 및 생명과학 분야 자연어처리(NLP) 시장 동향과 인사이트

비구조화된 임상 및 조사 자료의 양 증가

성장의 주된 원동력은 더 이상 기본적인 전자건강기록(EHR)의 디지털화가 아닙니다. 왜냐하면 그 전환은 2026년 이전에 이미 많은 선진 시장에서 성숙 단계에 접어들었기 때문입니다. 현재 수요를 주도하고 있는 요인은 앰비언트 문서화 도구, 원격의료 기록, 원격 모니터링 로그, 그리고 AI 지원형 임상 기록에서 발생하는 비정형 컨텐츠의 양이 증가하고 있다는 점입니다. Amazon Connect Health는 2026년에 시장에 진출하여 22개 이상의 전문 분야에 걸친 앰비언트 문서화를 지원했습니다. 이는 새로운 텍스트 스트림이 실제 의료 워크플로우에 얼마나 신속하게 도입되고 있는지를 보여줍니다. 또한 Netsmart사는 도입 후 1,300개가 넘는 고객 기관으로 구성된 네트워크 전체에서 앰비언트 문서화(Ambient Documentation)의 채택률이 275% 증가했다고 보고했는데, 이는 의료 제공업체의 시스템으로 유입되는 기계 생성 진료 기록의 기반이 훨씬 더 대규모로 확대되었음을 시사합니다. 이러한 요인들이 복합적으로 작용하여, 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장 수요 주기가 장기화되고 있습니다. 이는 구매자들이 현재 기존의 임상의 진료 기록과 새로 생성되는 문서 스트림 모두에서 진단, 처방, 소견을 추출하기 위한 파이프라인을 필요로 하고 있기 때문입니다.

자동화된 임상 문서 작성 및 스크라이빙에 대한 수요 증가

문서 작성에 따른 부담은 임상 NLP 분야에서 여전히 가장 뚜렷한 상업적 진입점 중 하나입니다. 2026년에 실시된 체계적 문헌고찰 및 메타분석에 따르면, NLP 및 대규모 언어 모델을 포함한 AI 도구는 실용적인 품질 관리에 뒷받침될 경우 문서 작성 부담을 줄일 수 있는 것으로 밝혀졌습니다. 마이크로소프트는 2026년에 Dragon Copilot이 9개국에서 매일 10만 명 이상의 임상의에게 이용되고 있으며, 58개 언어로 된 다국어 대화를 캡처하여 구조화된 기록으로 변환할 수 있다고 발표했습니다. 또한 Oracle사는 자사의 'Clinical AI Agent'는 미국 의사들의 문서 작성 시간을 20만 시간 이상 단축했다고 보고했으며, 아틀란티케어사에서는 도입 후 외래 진료 시 문서 작성 시간을 41% 단축하는 데 성공했습니다. 이러한 활용 사례가 확대됨에 따라, 의료 및 생명과학 분야의 자연어 처리 기술은 단순한 텍스트 변환의 가치를 넘어 코드 제안, 진단 지원, 리스크 관리 워크플로로 발전하고 있으며, 이를 통해 의료 제공업체와의 플랫폼 상의 관계가 더욱 깊어지고 있습니다.

모델의 '환각'이라고 하며 임상적 책임에 대한 우려

'환각'은 위험이 높은 환경에서 생성형 임상 NLP에 있어 여전히 가장 두드러진 장벽으로 남아 있습니다. 2026년 『npj Digital Medicine』지에 게재된 연구에 따르면, 대규모 언어 모델은 환자의 의료 관련 질문에 대해 안전하지 않은 답변을 제공할 확률이 높으며, 일상적인 업무 흐름에 통합하기 위해서는 여전히 엄격한 인적 감독이 필요한 것으로 밝혀졌습니다. 2026년 『Frontiers in Digital Health』지에 게재된 총설 역시 동일한 결론에 도달했으며, 의료용으로 조정된 모델이라 하더라도 특정 임상 상황에서는 안전하지 않은 동작을 보일 가능성이 있다고 지적하고 있습니다. 이는 약물 복용 조정, 진단 지원, 요약 생성이 모두 유창한 표현이 아니라 사실에 기반한 정확성에 의존하기 때문에 중요한 문제입니다. 따라서 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장에서는 감사 추적, 정보 출처의 근거 제시, 검토 관리 기능을 갖춘 플랫폼이 높이 평가되는 반면, 범용 모델을 단순히 얇게 포장한 것에 불과한 솔루션에 대해서는 구매자들이 여전히 신중한 태도를 보이고 있습니다.

부문별 분석

2025년, 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장의 65.12%를 솔루션이 차지했습니다. 이는 대규모 통합 의료 제공 시스템 전반에서 문서화, 코딩, 분석에 사용되는 소프트웨어의 도입 실적을 반영한 것입니다. 이러한 선도적 위상은 확립된 소프트웨어 계약과 의료 제공업체의 업무 흐름 내에서 패키지화된 NLP 도구가 수행하는 핵심적인 역할에 기인합니다. 임상 문서 작성, 코딩 지원 및 분석은 이 부문의 규모를 뒷받침하는 핵심적인 소프트웨어 활용 사례로 자리 잡고 있습니다. 텍스트 추출이 상환, 규정 준수 및 진료 워크플로우와 관련된 경우, 병원들은 검증된 시스템을 선호하는 경향이 있으므로 도입 실적은 여전히 중요한 요소로 남아 있습니다.

서비스 시장은 구매자들이 단순한 소프트웨어 라이선스뿐만 아니라 도입 지원, EHR(전자건강기록)과의 통합, 모델 튜닝, 지속적인 거버넌스를 요구하게 됨에 따라 2031년까지 연평균 성장률(CAGR) 29.67%로 성장할 것으로 전망됩니다. 의료 시스템은 벤더에게 독자적인 임상 코퍼스에 맞추어 모델을 조정하고, 가동 개시 후에도 이를 유지 관리할 것을 점점 더 요구하고 있습니다. John Snow Labs는 2026년, 자사의 헬스케어 NLP 플랫폼에 2,800개 이상의 사전 학습된 모델과, 변화하는 온톨로지 및 이용 사례에 맞추어 정기적으로 업데이트되는 파이프라인이 포함되어 있다고 발표했습니다. 이러한 서비스 중심의 관계는 시스템이 임상 및 생명과학 워크플로우에 통합된 후 지속적인 수익을 증대시키고, 전환 비용을 높입니다. 따라서 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장은 엔드투엔드 책임 체제로 전환되고 있으며, 장기적인 맞춤화, 재학습, 거버넌스에 대응할 수 없는 소프트웨어만을 제공하는 벤더들은 압박을 받고 있습니다.

2025년 시장에서 클라우드 기반 도입은 61.82%를 차지했습니다. 이는 대형 하이퍼스케일러의 투자뿐만 아니라, 공유 인프라를 통해 모델 훈련 및 추론을 손쉽게 확장할 수 있는 실질적인 편의성에 힘입은 것입니다. Microsoft Azure, AWS HealthLake, Google Cloud는 의료 분야에 특화된 AI 도구를 기업 환경 내에서 보다 쉽게 도입할 수 있도록 함으로써 이러한 우위 확보에 기여했습니다. 또한 클라우드는 보다 신속한 도입과 초기 인프라 비용 절감을 원하는 조직에도 적합합니다. 이는 통합된 모델 관리가 필요한 광범위한 의료 제공업체 네트워크나 여러 거점에 걸쳐 있는 생명과학 프로그램의 경우, 여전히 특히 중요한 요소로 남아 있습니다.

많은 의료 시스템이 식별 가능한 데이터를 승인된 환경 밖으로 반출하지 않으면서도 클라우드의 유연성을 추구함에 따라, 하이브리드 배포는 2031년까지 연평균 성장률(CAGR) 30.82%로 확대될 것으로 예측됩니다. 이러한 압박은 주권 및 현지화 관련 정책으로 인해 환자 데이터의 전송 및 저장 방식이 제한되고 있는 유럽, 일본 및 걸프 지역 시장에서 가장 크게 느껴지고 있습니다. 2026년 『Scientific Reports』지에 게재된 일본의 의료 PHI(개인 건강 정보) 추출에 관한 논문에서는 최적화된 로컬 모델이 클라우드 수준의 성능에 근접할 수 있음이 밝혀졌으며, 이를 통해 기밀성이 높은 워크로드를 온프레미스에서 유지함으로써 발생하는 단점을 완화할 수 있습니다. 온프레미스형 시스템은 군사 의료 네트워크나 구형 인프라를 갖춘 대규모 기관에서 여전히 중요한 역할을 하고 있지만, 하이브리드 모델이 보다 실용적인 중간 대안을 제공함에 따라 그 점유율은 감소할 것으로 보입니다. 따라서 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장은 기밀성이 높은 추론을 온프레미스에서 수행하고, 보다 광범위한 오케스트레이션 및 모델 관리는 클라우드에서 수행하는 혼합 아키텍처로 전환되고 있습니다.

2025년에는 자연어 이해(NLU)가 60.14%의 점유율을 차지하며 여전히 주도적인 위치를 유지했습니다. 이는 성숙한 의료 분야의 NLP 워크플로우 중 상당수가 여전히 기존 텍스트의 추출, 분류, 해석에 의존하고 있기 때문입니다. NLU는 EHR(전자건강기록) 연동 시스템 내에서 임상 개념 추출, 고유명사 인식 및 어설션 감지 분야에서 여전히 핵심적인 역할을 수행하고 있습니다. 이러한 기능들은 진단 내용 기록, 투약 정보 추출, 이상반응 검토 및 구조화된 문서 작성을 지원합니다. 이에 따라 NLU는 의료 제공 현장과 조사 현장 모두에서 폭넓은 역할을 수행하고 있습니다.

자연어 생성(NLG)은 퇴원 요약, 환자 연락, 임상 기록 작성 분야에서 생성 모델이 표준화됨에 따라 2031년까지 연평균 성장률(CAGR) 31.91%를 기록하며 성장할 것으로 전망됩니다. 마이크로소프트는 2026년에 Dragon Copilot이 환자와 의료진의 대화를 58개 언어로 된 구조화된 EHR 기록으로 변환할 수 있을 것이라고 보고했으며, 이는 생성형 도구의 배후에 있는 상업적 동력을 보여줍니다. 현재 구매자들은 생성된 컨텐츠를 기존의 정확도 지표뿐만 아니라, 유창성, 사실의 정확성, 기존 EHR 템플릿과의 일관성 등의 관점에서도 평가했습니다. 생성된 요약본은 케어 워크플로우에 직접 통합되어야 하며, 심사를 통과할 수 있는 수준이어야 하므로, 이에 따라 조달 기준도 변화하고 있습니다. 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장에서는 견고한 임상적 근거에 기반한 생성 기능을 제공할 수 있는 벤더가 높이 평가되는 반면, 의료 분야에 특화된 제어 기능을 갖추지 못한 범용 모델은 기업 내 의료 환경에 도입되는 과정에서 더 큰 어려움을 겪을 것으로 보입니다.

지역별 분석

북미는 2025년 시장 점유율의 43.23%를 차지했으며, 의료 NLP 도입 분야에서 지역별 1위를 유지했습니다. 미국은 EHR 보급률이 높고, 대규모 의료 제공업체 네트워크를 갖추고 있으며, 의료 제공업체, 보험사, 생명과학 분야의 다양한 활용 사례에 걸쳐 공급업체들이 활발히 활동하고 있어 조달 활동이 뒷받침되고 있기 때문에 여전히 수요의 중심지입니다. 마이크로소프트와 Oracle은 2026년에 의료 AI의 제공 범위를 확대했으며, 이를 통해 해당 지역이 기업용 임상 NLP의 주요 상용화 실증 거점으로서의 역할을 강화했습니다. 또한 AWS도 2026년에 HealthLake 내에서 CMS의 상호운용성 및 사전 승인에 관한 최종 규정에 대한 대응 기능을 추가했습니다. 이를 통해 미국의 보험사 및 관련 공급업체들은 규정 준수를 중시하는 NLP 기반 승인 워크플로우라는 직접적인 활용 사례를 확보하게 되었습니다. 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장은 북미에서 가장 성숙한 상태를 유지하고 있습니다. 이는 인프라 구축 현황, 상환 압박, 공급업체의 영향력 등 모든 요소가 다른 대부분의 지역보다 훨씬 더 명확하게 조화를 이루고 있기 때문입니다.

유럽에서는 도입 시기와 공급업체의 입지 모두에 영향을 미치는 더욱 엄격한 규정 준수 모델 하에서 발전이 계속되고 있습니다. GDPR(EU 개인정보보호규정) 제9조의 규정 및 EU AI법에서 규정하는 임상 AI에 대한 고위험 의무에 따라, 대규모 도입을 확대하기 위해서는 감독, 거버넌스 및 문서화에 관한 보다 확실한 증거가 요구됩니다. 독일과 영국은 여전히 주요 수요 거점이며, 한편 북유럽 국가들의 시스템은 높은 수준의 디지털화와 견고한 제도적 신뢰를 바탕으로 거버넌스 주도형 임상 AI 프로그램을 위한 탁월한 환경으로 두각을 나타내고 있습니다. 그 때문에 유럽의 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장은 보다 신중한 속도로 발전하고 있습니다. 상호 운용성의 격차와 규제 관련 실사 절차가 단기적인 진전을 늦추고 있는 반면, 승인된 솔루션에 대한 장기적인 품질 기준은 강화되고 있기 때문입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 32.53%를 기록하며 성장할 것으로 예상되며, 이 분야에서 가장 빠르게 성장하는 지역 클러스터가 될 전망입니다. 이러한 성장은 방대한 환자 수, 임상의 부족, 디지털 헬스 분야에 대한 투자 확대, 그리고 다국어 및 분산된 의료 현장에 걸친 의료 컨텐츠를 처리해야 할 필요성에 힘입어 이루어지고 있습니다. 일본이 중요한 사례로 떠오르고 있습니다. 그 이유는 현지 도입을 통해 기술적 신뢰성이 높아졌기 때문이며, 또한 리켄(RIKEN)이 2026년 5월, 병원 환경을 대상으로 한 전문의 면허 시험 벤치마크에서 90.8%의 정확도를 달성한 일본어 의료용 LLM을 공개했기 때문입니다. 이러한 현지 모델 개발은 주권을 중시하는 조달 방식에 부합하며, 온프레미스나 엄격하게 관리되는 환경을 선호하는 기관에서 도입을 보다 현실적으로 만들어 줍니다. 중동 및 아프리카는 걸프 국가들의 주도하에 여전히 초기 단계의 기회에 머물러 있는 반면, 남미에서는 브라질이나 아르헨티나 등지의 민간 공급자 네트워크에 집중되어 있습니다. 이 지역들의 헬스케어 및 생명과학 분야 자연어처리(NLP) 시장은 북미나 유럽에 비해 여전히 규모가 작지만, 현지 언어 지원 요구 사항과 공공 시스템의 현대화로 인해 도입을 위한 장기적인 성장 여지가 계속해서 나타나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the NLP in healthcare and life science market size is expected to increase from USD 5.67 billion in 2025 to USD 7.13 billion in 2026 and reach USD 24.80 billion by 2031, growing at a CAGR of 28.33% over 2026-2031.

This report is Segmented by Offering, Deployment Mode (Cloud-Based, On-Premises, Hybrid), NLP Type (NLU, NLG), NLP Technique (NER, OCR, Sentiment Analysis, Text Classification, Topic Modeling, and More), Application, End User, Organization Size (Large, SMEs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global NLP In Healthcare and Life Science Market Trends and Insights

Rising Unstructured Clinical and Research Text Volumes

The core growth engine is no longer basic EHR digitization because that transition had already matured in many developed markets before 2026. What is driving demand now is the rising volume of unstructured content coming from ambient documentation tools, telehealth transcripts, remote monitoring logs, and AI-assisted clinical notes. Amazon Connect Health entered the market in 2026 with ambient documentation support across more than 22 specialties, which shows how quickly new text streams are moving into production care workflows. Netsmart also reported a 275% increase in ambient documentation adoption across its network of more than 1,300 client organizations after deployment, which points to a much larger base of machine-generated notes entering provider systems. That combination keeps the NLP in healthcare and life science market on a long demand cycle because buyers now need extraction pipelines for diagnoses, medications, and findings from both traditional clinician notes and newly generated documentation streams.

Accelerating Demand for Automated Clinical Documentation and Scribing

Documentation burden remains one of the clearest commercial entry points for clinical NLP. A 2026 systematic review and meta-analysis found that AI tools, including NLP and large language models, reduce documentation burden when supported by practical quality control. Microsoft stated in 2026 that Dragon Copilot was being used by more than 100,000 clinicians each day across 9 countries and that it could capture multilingual conversations in 58 languages and convert them into structured notes. Oracle also reported that its Clinical AI Agent had saved U.S. doctors more than 200,000 documentation hours, and AtlantiCare achieved a 41% reduction in documentation time in ambulatory care after deployment. As this use case scales, the NLP in healthcare and life science market is shifting from simple transcription value toward code suggestion, diagnostic support, and risk workflows that create a deeper platform relationship with providers.

Model Hallucination and Clinical Liability Concerns

Hallucination remains the most visible barrier for generative clinical NLP in high-stakes settings. A 2026 study in npj Digital Medicine found that large language models gave unsafe responses to patient medical questions at rates that still require strong human oversight before they can sit inside routine workflows. A 2026 review in Frontiers in Digital Health reached a similar conclusion and noted that even medically tuned models can behave unsafely in specific clinical contexts. This matters because medication reconciliation, diagnostic support, and summary generation all depend on factual precision rather than fluent output. For that reason, the NLP in healthcare and life science market is rewarding platforms with audit trails, source grounding, and review controls, while buyers remain cautious toward thin wrappers around general-purpose models.

Other drivers and restraints analyzed in the detailed report include:

- Clinical Trial Matching and Real-World Evidence Extraction at Scale

- GenAI-Enabled Medical Coding and Summary Generation

- Data Privacy and Sovereignty Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 65.12% of the NLP in healthcare and life science market share in 2025, which reflected the installed base of software used for documentation, coding, and analytics across large integrated delivery systems. That lead came from established software contracts and the central role of packaged NLP tools inside provider workflows. Clinical documentation, coding support, and analytics remain the core software use cases that support this segment's scale. The installed base still matters because hospitals tend to prefer proven systems when text extraction touches reimbursement, compliance, and care workflows.

Services are projected to grow at 29.67% CAGR through 2031 as buyers ask for deployment support, EHR integration, model tuning, and ongoing governance rather than only a software license. Health systems increasingly want vendors to adapt models to proprietary clinical corpora and maintain them after go-live. John Snow Labs said in 2026 that its Healthcare NLP platform includes more than 2,800 pre-trained models and regularly updated pipelines tied to changing ontologies and use cases. That type of service-heavy relationship increases recurring revenue and raises switching costs once a system is embedded into clinical and life sciences workflows. The NLP in healthcare and life science market is therefore shifting toward end-to-end accountability, which puts pressure on software-only vendors that cannot support customization, retraining, and governance over time.

Cloud-based deployment accounted for 61.82% of the 2025 market, supported by large hyperscaler investments and the practical ease of scaling model training and inference through shared infrastructure. Microsoft Azure, AWS HealthLake, and Google Cloud helped shape this lead by making healthcare-focused AI tooling easier to deploy inside enterprise environments. Cloud also suits organizations that want faster implementation and lower upfront infrastructure costs. That remains especially relevant for broad provider networks and multisite life sciences programs that need centralized model management.

Hybrid deployment is forecast to advance at 30.82% CAGR through 2031 because many health systems want cloud flexibility without moving identifiable data outside approved environments. The pressure is strongest in Europe, Japan, and Gulf markets where sovereignty and localization policies limit how patient data can be transmitted or stored. The 2026 Scientific Reports paper on Japanese medical PHI extraction showed that optimized local models can approach cloud-level performance, which lowers the penalty of keeping sensitive workloads on site. On-premises systems still retain a role in military health networks and large institutions with older infrastructure, but their share is likely to decline as hybrid models offer a more practical middle path. The NLP in healthcare and life science market is therefore moving toward mixed architectures where sensitive inference stays local and broader orchestration or model management sits in the cloud.

Natural Language Understanding held 60.14% share in 2025, which kept it in the leading position because most mature healthcare NLP workflows still depend on the extraction, classification, and interpretation of existing text. NLU remains central to clinical concept extraction, named entity recognition, and assertion detection inside EHR-linked systems. Those functions support diagnosis capture, medication extraction, adverse event review, and structured documentation. This gives NLU a broad installed role across both provider and research settings.

Natural Language Generation is projected to grow at 31.91% CAGR through 2031 as generative models become standard for drafting discharge summaries, patient communications, and clinical notes. Microsoft reported in 2026 that Dragon Copilot could turn patient-clinician conversations into structured EHR notes in 58 languages, which illustrates the commercial pull behind generation-led tools. Buyers now evaluate generated content on fluency, factual accuracy, and alignment with existing EHR templates, not only on traditional precision metrics. That changes procurement criteria because a generated summary must fit directly into the care workflow and stand up to review. The NLP in healthcare and life science market is rewarding vendors that can deliver generation with strong clinical grounding, while general-purpose models without healthcare-specific controls face a harder path into enterprise care environments.

Complete Report Scope:

- By Offering

- Solutions

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By NLP Type

- Natural Language Understanding

- Natural Language Generation

- By NLP Technique

- Named Entity Recognition

- Optical Character Recognition

- Sentiment Analysis

- Text Classification

- Topic Modeling

- Text Summarization

- Predictive Risk Analytics

- By Application

- Clinical Operations and Decision Support

- Patient Care and Engagement

- Biomedical Research and Drug Development

- Administrative and Operations Management

- Genomics and Precision Medicine

- Clinical Trial Matching

- Medical Education and Knowledge Dissemination

- Risk and Compliance Management

- By End User

- Healthcare Providers

- Healthcare Payers

- Pharmaceutical and Biotechnology Companies

- Healthcare Researchers

- Public Health and Government Agencies

- Medical Device Companies

- By Organization Size

- Large Enterprises

- Small and Midsize Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 43.23% of the 2025 market, which kept it in the leading regional position for healthcare NLP adoption. The United States remains the center of demand because procurement is supported by deep EHR penetration, large provider networks, and broad vendor activity across provider, payer, and life sciences use cases. Microsoft and Oracle both expanded their healthcare AI offerings in 2026, which reinforced the region's role as the main commercial proving ground for enterprise clinical NLP. AWS also added support in 2026 for the CMS Interoperability and Prior Authorization Final Rule inside HealthLake, which gives U.S. payers and connected vendors a direct compliance-driven use case for NLP-enabled authorization workflows. The NLP in healthcare and life science market remains most mature in North America because infrastructure readiness, reimbursement pressure, and vendor presence all align more clearly there than in most other regions.

Europe continues to advance under a stricter compliance model that shapes both deployment timing and vendor positioning. GDPR Article 9 rules and the EU AI Act's high-risk obligations for clinical AI require stronger evidence around oversight, governance, and documentation before large deployments can scale. Germany and the United Kingdom remain the main national demand centers, while Nordic systems stand out as strong environments for governance-led clinical AI programs because of high digitization and stronger institutional trust. The NLP in healthcare and life science market in Europe is therefore moving forward with a more measured pace, as interoperability gaps and regulatory diligence slow near-term rollout even while they strengthen the long-run quality bar for approved solutions.

Asia-Pacific is projected to grow at 32.53% CAGR through 2031, making it the fastest-expanding regional cluster in this space. Growth is being supported by large patient populations, clinician shortages, stronger digital health investment, and the need to process healthcare content across multiple languages and fragmented care settings. Japan is emerging as an important case because local deployment is gaining technical credibility and because RIKEN published a Japanese medical LLM in May 2026 that achieved 90.8% accuracy on specialist licensing benchmarks in hospital-oriented environments. That kind of local model development fits sovereignty-driven procurement patterns and makes deployment more realistic where institutions prefer on-premises or tightly controlled environments. Middle East and Africa remains an earlier-stage opportunity led by Gulf initiatives, while South America is still concentrated in private provider networks in countries such as Brazil and Argentina. The NLP in healthcare and life science market in these regions is still smaller than in North America or Europe, but local-language requirements and public system modernization continue to create a longer runway for adoption.

- 3M

- Amazon Web Services, Inc.

- Averbis GmbH

- Cerner

- Clinithink Ltd.

- CORTI AI ApS

- Deep 6 AI, Inc.

- Dolbey Systems, Inc.

- Edifecs, Inc.

- Epic Systems

- Google LLC

- IBM Corporation (International Business Machines Corporation)

- Inovalon Holdings, Inc.

- IQVIA

- John Snow Labs Inc.

- Lexalytics, Inc.

- Microsoft

- Notable Health, Inc.

- Nuance Communications, Inc.

- Optum

- Oracle

- SAS Institute

- Suki AI, Inc.

- Syapse, Inc.

- Tempus AI, Inc.

- Xerox Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Unstructured Clinical and Research Text Volumes

- 4.2.2 Accelerating Demand for Automated Clinical Documentation and Scribing

- 4.2.3 Clinical Trial Matching and Real-World Evidence Extraction at Scale

- 4.2.4 GenAI-Enabled Medical Coding and Summary Generation

- 4.2.5 AI Governance, Auditability, and Traceability Requirements

- 4.2.6 Multilingual Healthcare Content Processing Across Fragmented Care Settings

- 4.3 Market Restraints

- 4.3.1 Interoperability Gaps With Legacy EHR and Claims Stacks

- 4.3.2 Limited Domain-Labeled Training Data for Specialty Medicine

- 4.3.3 Model Hallucination and Clinical Liability Concerns

- 4.3.4 Data Privacy and Sovereignty Constraints

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By NLP Type

- 5.3.1 Natural Language Understanding

- 5.3.2 Natural Language Generation

- 5.4 By NLP Technique

- 5.4.1 Named Entity Recognition

- 5.4.2 Optical Character Recognition

- 5.4.3 Sentiment Analysis

- 5.4.4 Text Classification

- 5.4.5 Topic Modeling

- 5.4.6 Text Summarization

- 5.4.7 Predictive Risk Analytics

- 5.5 By Application

- 5.5.1 Clinical Operations and Decision Support

- 5.5.2 Patient Care and Engagement

- 5.5.3 Biomedical Research and Drug Development

- 5.5.4 Administrative and Operations Management

- 5.5.5 Genomics and Precision Medicine

- 5.5.6 Clinical Trial Matching

- 5.5.7 Medical Education and Knowledge Dissemination

- 5.5.8 Risk and Compliance Management

- 5.6 By End User

- 5.6.1 Healthcare Providers

- 5.6.2 Healthcare Payers

- 5.6.3 Pharmaceutical and Biotechnology Companies

- 5.6.4 Healthcare Researchers

- 5.6.5 Public Health and Government Agencies

- 5.6.6 Medical Device Companies

- 5.7 By Organization Size

- 5.7.1 Large Enterprises

- 5.7.2 Small and Midsize Enterprises

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East & Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East & Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M

- 6.3.2 Amazon Web Services, Inc.

- 6.3.3 Averbis GmbH

- 6.3.4 Cerner Corporation

- 6.3.5 Clinithink Ltd.

- 6.3.6 CORTI AI ApS

- 6.3.7 Deep 6 AI, Inc.

- 6.3.8 Dolbey Systems, Inc.

- 6.3.9 Edifecs, Inc.

- 6.3.10 Epic Systems Corporation

- 6.3.11 Google LLC

- 6.3.12 IBM Corporation (International Business Machines Corporation)

- 6.3.13 Inovalon Holdings, Inc.

- 6.3.14 IQVIA Holdings Inc.

- 6.3.15 John Snow Labs Inc.

- 6.3.16 Lexalytics, Inc.

- 6.3.17 Microsoft Corporation

- 6.3.18 Notable Health, Inc.

- 6.3.19 Nuance Communications, Inc.

- 6.3.20 Optum, Inc.

- 6.3.21 Oracle Corporation

- 6.3.22 SAS Institute Inc.

- 6.3.23 Suki AI, Inc.

- 6.3.24 Syapse, Inc.

- 6.3.25 Tempus AI, Inc.

- 6.3.26 Xerox Holdings Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment