|

시장보고서

상품코드

2072820

중국의 광업 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China Mining Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

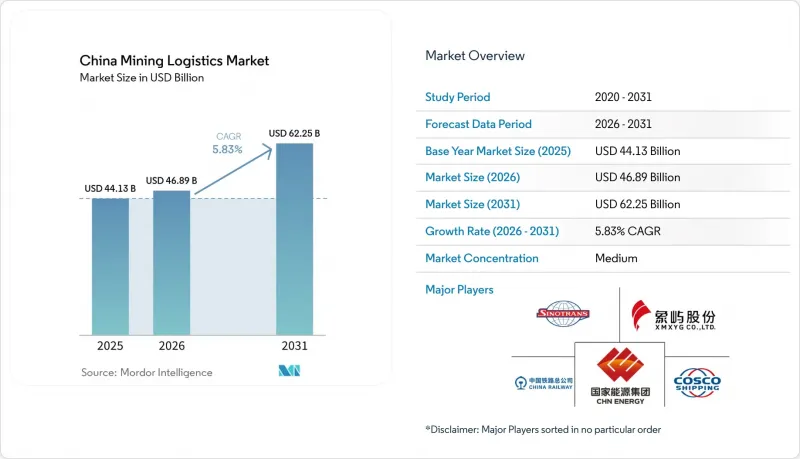

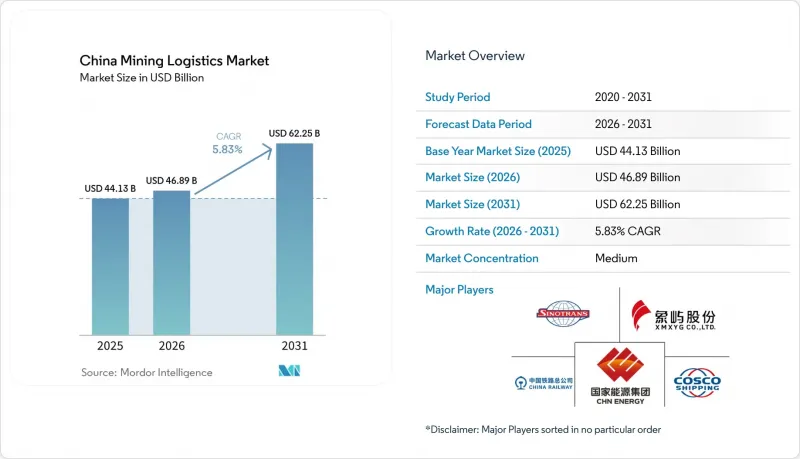

Mordor Intelligence에 의하면, 중국 광업 물류 시장 규모는 2025년에 441억 3,000만 달러 라고 추계되고 있어 2026년 468억 9,000만 달러에서 2031년까지 628억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.83%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 서비스별(운송(도로, 철도, 해상 및 내륙 수로, 항공), 창고·재고 관리, 부가가치 서비스), 상품별(철광석, 야금용·일반 석탄, 비금속(Cu, Zn, Ni), 금 등), 지역별(중국 북부, 북동부, 동부, 중부, 남부, 남서부, 북서부)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국 광업 물류 시장 동향과 인사이트

석탄 및 광석 수송을 위한 철도·수로 회랑의 확대

중국의 광업 물류 시장은 석탄 및 광석 운송 노선에서 벌크 화물의 흐름을 재편하는 철도·수운 회랑의 개발에 힘입어 그 양상이 새롭게 바뀌고 있습니다. 2025년 첫 5개월 동안 중국의 철도 화물 수송량은 전년 동기 대비 3.1% 증가한 16억 톤에 달했으며, 표준화된 복합운송 제품의 보급에 힘입어 철도와 수운 간 컨테이너 수송량은 18.4% 증가했습니다. 이러한 운영상의 변화가 중요한 이유는 개별 항만이나 철도 거래가 아니라, 통합된 운송의 경제성을 강화하기 때문입니다. 중국 남서부 지역의 회랑 확장은 내륙 생산 거점과 수출 관문 간의 접근성을 높여, 이를 통해 내륙 지방의 광물 생산에 대한 상업적 타당성을 높이고 있습니다. 단일 계약 물류 구조 하에서 운송되는 화물이 늘어남에 따라, 중국 광업 물류 시장에서는 내륙에서의 화물 집하, 간선 철도, 항만 하역, 하류 지역으로의 배송을 하나의 서비스 체인으로 통합할 수 있는 사업자에게 계속해서 혜택이 돌아갈 것입니다.

전략적 광물 및 에너지 안보에 대한 투자

중국의 광업 물류 시장은 에너지 안보 및 중요 광물 가공과 관련된 국가 주도의 투자에 의해서도 뒷받침되고 있습니다. 설황철도는 2025년 4월까지 석탄 누적 수송량이 50억 톤을 돌파했으며, 이는 서쪽에서 동쪽으로의 에너지 유통을 이미 뒷받침하고 있는 전용 인프라의 규모를 여실히 보여주고 있습니다. 이러한 논리에 따르면, 중국의 정제 체계는 여전히 중심적인 역할을 하고 있으며, 국제에너지기구(IEA)는 2025년 전략적으로 중요한 20유형의 광물 중 19유형에 대해 중국이 평균 70%의 정제 점유율을 차지했다고 발표했습니다. 이러한 높은 집중도 덕분에, 단기적으로 상품 시장이 침체되더라도 제련소 및 가공 클러스터로 이어지는 물류 회랑은 전략적으로 중요한 위치를 유지하고 있습니다. 중국의 광업 물류 시장에서 물류 인프라는 상업적 화물 수요뿐만 아니라 국가공급 안보에도 기여하고 있어, 이에 따라 회랑에 대한 투자에 견고한 지지 기반이 형성되고 있습니다.

대량 물류 거점의 환경 규제 대응을 위한 설비 투자

환경 규제에 대응함에 따라 중국의 광업 물류 시장, 특히 벌크 터미널과 내륙 하역 거점에서의 자본 집약도가 높아지고 있습니다. 사업자들은 항만 및 중계 기지에서 분진 억제 시스템, 밀폐형 컨베이어, 배수 관리 및 전동 기기 활용 확대를 요구받고 있습니다. CHN Energy사의 황화항 5단계 프로젝트는 2025년에 16가지 유형의 친환경 기술을 갖춘 '거의 탄소 제로' 터미널로 발표되었으며, 차세대 벌크 인프라에 현재 필요한 투자 규모를 보여주고 있습니다. 항만 개발은 보다 광범위한 공공 정책 및 에너지 정책의 우선 과제와 밀접하게 연관되어 있기 때문에 국가가 지원하는 대형 사업자는 이러한 비용을 보다 수월하게 감당할 수 있습니다. 한편, 중국의 광업 물류 시장에서는 중소규모 민간 벌크 사업자들이 여전히 위험에 노출되기 쉬운 상황에 놓여 있습니다. 이는 취급량이 감소하는 시기에는 규정 준수 관련 지출이 운전 자본과 직접적으로 경쟁하게 되기 때문입니다.

부문별 분석

2025년, 중국 광업 물류 시장에서 운송 부문의 점유율은 68.18%를 차지하고 있으며, 이는 국내를 횡단하는 석탄, 철광석, 정광의 운송량이 매우 많음을 반영하고 있습니다. 공공 정책, 화물 회랑에 대한 자금 지원, 항만 투자 등이 모두 대규모 벌크 수송을 뒷받침하고 있기 때문에 철도, 해상 수송, 내륙 수로가 여전히 주요 수송 수단으로 자리 잡고 있습니다. 철도망이 미비한 산간 지역이나 내륙의 광산 지역에서는 도로 운송이 여전히 '퍼스트 마일'에서 필수적인 역할을 수행하고 있습니다. 항공 물류는 광업 화물의 경우 일반적으로 중량당 단가가 낮고 중량이 큰 탓에 서비스 구성에서 차지하는 비중이 극히 미미하지만, 정제 금속이나 중요한 예비 부품의 경우 납기가 중요한 상황에서는 여전히 더 신속한 운송 수단이 이용되고 있습니다.

가장 빠른 성장세를 보이고 있는 분야는 부가가치 서비스로, 제철소가 블렌딩, 품위 최적화, 수분 관리를 항만 물류 사업자에게 위탁함에 따라 2031년까지 연평균 성장률(CAGR) 6.49%로 확대될 것으로 전망됩니다. 제철소나 발전소에서는 조달 주기를 평준화하고, 운송 차질이 발생했을 때 가동을 유지하기 위한 완충 재고가 필요하기 때문에 창고 보관 및 재고 관리는 여전히 중요한 역할을 하고 있습니다. 일조항에 위치한 바오우(Baowu)의 1,000만 톤 규모 스마트 광석 혼합 센터는 중국의 광업 물류 업계가 단순한 화물 운송에서 벗어나, 고로 투입 품질을 향상시키고 현장의 하역 수요를 줄여주는 서비스 단계로 전환되고 있음을 보여줍니다. 이 모델이 보급됨에 따라, 중국의 광업 물류 시장에서는 운송 및 하역 요금뿐만 아니라 맞춤형 가공 계약을 통한 수익 비중이 더욱 높아질 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the china mining logistics market size was estimated at USD 44.13 billion in 2025 and is expected to increase from USD 46.89 billion in 2026 to USD 62.85 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

This report is Segmented by Service (Transportation (Road, Rail, Sea and Inland Waterways, Air), Warehousing and Inventory Management, Value-Added Services), by Commodity (Iron Ore, Metallurgical and Thermal Coal, Base Metals (Cu, Zn, Ni), Gold, and More) and by Geography (North, Northeast, East, Central, South, Southwest, Northwest China). The Market Forecasts are Provided in Terms of Value (USD).

China Mining Logistics Market Trends and Insights

Rail-Water Corridor Expansion for Coal and Ore

The China mining logistics market is being reshaped by rail-water corridor development that is redirecting bulk flows across coal and ore routes. China's railways carried 1.6 billion tons of freight in the first 5 months of 2025, up 3.1% year on year, while rail-water intermodal container volumes rose 18.4% as standardized multimodal products gained traction. That operating shift matters because it strengthens the economics of integrated movement instead of isolated port or rail transactions. Corridor expansion in Southwest China is also widening access between inland production centers and export gateways, thereby improving the commercial case for mining output from interior provinces. As more cargo moves under single-contract logistics structures, the China mining logistics market should continue to reward operators that can combine inland pickup, mainline rail, port handling, and downstream delivery into one service chain.

Strategic Mineral and Energy Security Investment

The China mining logistics market is also supported by state-backed investment tied to energy security and critical mineral processing. The Shuohuang Railway has passed 5 billion cumulative tons of coal moved by April 2025, which shows the scale of dedicated infrastructure already supporting west-to-east energy flows. China's refining position remains central to this logic, with the IEA stating in 2025 that China held an average 70% refining share across 19 of 20 strategically important minerals IEA. That level of concentration keeps inbound logistics corridors to smelter and processing clusters strategically important even when short-term commodity markets soften. In the China mining logistics market, this creates a durable floor for corridor investment because logistics infrastructure is serving national supply security as much as commercial freight demand.

Environmental Compliance Capex for Bulk Nodes

Environmental compliance is raising capital intensity for the China mining logistics market, especially at bulk terminals and inland handling nodes. Operators are being pushed toward dust suppression systems, sealed conveyors, wastewater controls, and higher use of electrified equipment at ports and transfer stations. CHN Energy's Huanghua Port Phase V project was presented in 2025 as a near-zero carbon terminal with 16 categories of green technology, showing the scale of investment now needed in new-generation bulk infrastructure. Large state-backed operators can more easily absorb these costs because port development is tied to broader public and energy priorities. In the China mining logistics market, smaller private bulk operators remain more exposed because compliance spending directly competes with working capital during weaker throughput periods.

Other drivers and restraints analyzed in the detailed report include:

- Deepwater Ore-Terminal Capacity Expansion

- Lower Logistics Cost and Modal-Shift Policy Push

- Steel-Cycle and Ore-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 68.18% of the China mining logistics market share in 2025, which reflects the sheer weight of coal, iron ore, and mineral concentrate movement across the country. Rail and sea and inland waterways remain the dominant transport sub-modes because public policy, freight corridor funding, and port investment all favor bulk movement at scale. Road transport still plays an essential first-mile role in mountain and interior mining areas where rail connectivity is incomplete. Air logistics remains a very small part of the service mix because mining cargo is usually heavy and low value per unit of weight, though refined metals and critical spare parts still use faster modes when timing matters.

The fastest growth is in value-added services, which are projected to expand at a 6.49% CAGR through 2031 as mills outsource blending, grade optimization, and moisture management to logistics operators at ports. Warehousing and inventory management remain important because steel mills and power plants need buffer stocks to smooth procurement cycles and protect operations during transport disruptions. Baowu's 10-million-ton intelligent ore blending center at Rizhao Port shows how the China mining logistics industry is shifting from pure cargo movement toward service layers that improve furnace input quality and lower on-site handling needs. As that model spreads, the China mining logistics market should see a larger share of revenue come from customized processing contracts rather than only transport and handling fees.

Complete Report Scope:

- By Service

- Transportation

- Road

- Rail

- Sea and Inland Waterways

- Air

- Warehousing and Inventory Management

- Value-Added Services

- Transportation

- By Commodity

- Iron Ore

- Metallurgical and Thermal Coal

- Base Metals (Cu, Zn, Ni)

- Gold

- Other Minerals/Metals

- By Geography

- North China

- Northeast China

- East China

- Central China

- South China

- Southwest China

- Northwest China

List of Companies Covered in this Report:

- China Energy Investment Corporation (CHN Energy)

- Sinotrans Limited

- COSCO SHIPPING Logistics and Supply Chain Management Co., Ltd.

- China Logistics Group Co., Ltd.

- China State Railway Group (CR)

- Ningbo Zhoushan Port Company Limited

- Shandong Port Group Co., Ltd.

- Tianjin Port (Group) Co., Ltd.

- Hebei Port Group Co., Ltd.

- China Minmetals Corporation

- Shandong Energy Group Co., Ltd.

- Jizhong Energy Group Co., Ltd.

- Jiayou International Logistics Co., Ltd.

- Xiamen Xiangyu Co., Ltd.

- Lianyungang Port Group Co., Ltd.

- Beibu Gulf Port Co., Ltd.

- EACON Mining

- CiDi Inc.

- Chongqing Logistics Group

- WAYTOUS (Zhongke Huituo (Beijing) Technology Co., Ltd.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Strategic Logistics Corridor Analysis

- 4.3 Infrastructure and Modal Mix Analysis

- 4.4 Market Drivers

- 4.4.1 Rail-Water Corridor Expansion for Coal And Ore

- 4.4.2 Strategic Mineral and Energy Security Investment

- 4.4.3 Deepwater Ore-Terminal Capacity Expansion

- 4.4.4 Lower-Logistics-Cost and Modal-Shift Policy Push

- 4.4.5 Port-Side Ore Blending and Processing

- 4.4.6 Autonomous Haulage and Smart Dispatch Deployment

- 4.5 Market Restraints

- 4.5.1 Environmental Compliance Capex for Bulk Nodes

- 4.5.2 Steel-Cycle and Ore-Price Volatility

- 4.5.3 First-Mile Mine-to-Mainline Bottlenecks

- 4.5.4 Coastal Hub Disruption Sensitivity

- 4.6 Value / Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Rivalry

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Air

- 5.1.2 Warehousing and Inventory Management

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By Commodity

- 5.2.1 Iron Ore

- 5.2.2 Metallurgical and Thermal Coal

- 5.2.3 Base Metals (Cu, Zn, Ni)

- 5.2.4 Gold

- 5.2.5 Other Minerals/Metals

- 5.3 By Geography

- 5.3.1 North China

- 5.3.2 Northeast China

- 5.3.3 East China

- 5.3.4 Central China

- 5.3.5 South China

- 5.3.6 Southwest China

- 5.3.7 Northwest China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 China Energy Investment Corporation (CHN Energy)

- 6.4.2 Sinotrans Limited

- 6.4.3 COSCO SHIPPING Logistics and Supply Chain Management Co., Ltd.

- 6.4.4 China Logistics Group Co., Ltd.

- 6.4.5 China State Railway Group (CR)

- 6.4.6 Ningbo Zhoushan Port Company Limited

- 6.4.7 Shandong Port Group Co., Ltd.

- 6.4.8 Tianjin Port (Group) Co., Ltd.

- 6.4.9 Hebei Port Group Co., Ltd.

- 6.4.10 China Minmetals Corporation

- 6.4.11 Shandong Energy Group Co., Ltd.

- 6.4.12 Jizhong Energy Group Co., Ltd.

- 6.4.13 Jiayou International Logistics Co., Ltd.

- 6.4.14 Xiamen Xiangyu Co., Ltd.

- 6.4.15 Lianyungang Port Group Co., Ltd.

- 6.4.16 Beibu Gulf Port Co., Ltd.

- 6.4.17 EACON Mining

- 6.4.18 CiDi Inc.

- 6.4.19 Chongqing Logistics Group

- 6.4.20 WAYTOUS (Zhongke Huituo (Beijing) Technology Co., Ltd.)

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment