|

시장보고서

상품코드

2072826

음성 바이오마커 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vocal Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

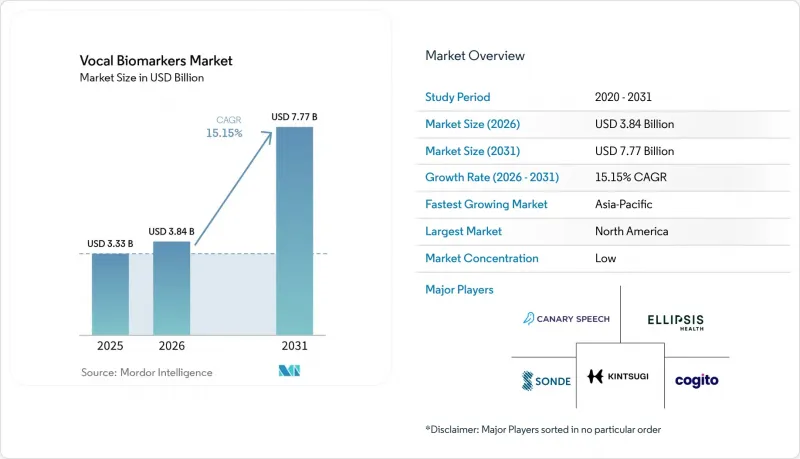

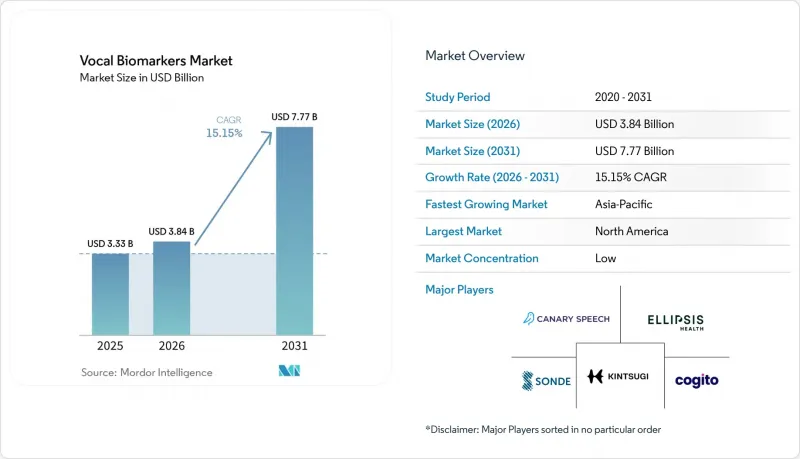

Mordor Intelligence에 의하면, 음성 바이오마커 시장 규모는 2025년에 33억 3,000만 달러로 평가되었고, 2026년에 38억 4,000만 달러로 추정되고, 2031년까지 77억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 15.15%로 성장할 전망입니다.

본 보고서는 기술별(음향 특징, 프로소디 등), 플랫폼 유형별(클라우드 기반 플랫폼, 웹형 플랫폼 등), 용도별(정신 건강 모니터링 등), 최종 사용자별(병원, 제약 및 바이오기술 기업 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 음성 바이오마커 시장 동향 및 인사이트

비침습적 디지털 헬스 도구로서 음성 활용 확대

음성 바이오마커 시장은 일반 스마트폰을 이용해 음성 데이터를 수집할 수 있다는 점을 원동력으로 삼아 호황을 누리고 있습니다. 이러한 혁신을 통해 채혈, 영상 진단 시스템, 웨어러블 센서와 같은 침습적인 방법이 더 이상 필요하지 않게 됩니다. 이러한 도입의 용이성은 의료 서비스 이용이 제한된 지방이나 의료 서비스가 충분히 제공되지 않는 지역에서 특히 유용합니다. 이번 조사에서는 단 6초 분량의 모음 녹음만으로도 천식 악화 위험을 평가할 수 있는 Sonde Health사의 음성 바이오마커 도구가 주목을 받았습니다. 특히 주목할 점은 미국 및 인도(인도 5개 언어 대상) 코호트에서 정규화 점수가 높을수록 악화 위험이 3.57배 높아진다는 사실이 밝혀졌습니다는 점입니다. 이러한 실용적인 증거는 언어별로 모델을 재구축할 필요 없이 다국어 지역에 확대 적용할 수 있는 음성 바이오마커 시장의 잠재력을 입증하고 있습니다. 또한, 우울증 선별 검사 분야에서도 뚜렷한 수요가 나타나고 있습니다. 『Annals of Family Medicine』지는 뚜렷한 대조를 지적하고 있습니다. 정기적인 선별검사가 권장되고 있음에도 불구하고, 2025년 시점에서 1차 진료 환자 중 선별검사를 받은 비율은 고작 4%에 그쳤습니다. 이러한 격차는 초기 분류 과정에서 간이형 음성 도구의 잠재력을 여실히 보여주고 있습니다.

AI와 머신러닝을 통한 신호 추출 정확도 향상

음성 바이오마커 시장은 모델 설계의 발전에 따라 진화하고 있으며, 좁은 의미로 정의된 특징에서 다양한 임상 데이터셋을 통해 학습된 보다 광범위한 표현으로 전환되고 있습니다. 2026년 5월, Bridge2AI 컨소시엄은 독자적인 음성 데이터셋으로 학습된 듀얼 인코더 모델 'VoiceFM'을 발표했습니다. 이 모델은 사이트 간 일반화, 영어·스페인어·중국어에서 파킨슨병 감지, 그리고 다중 질환 분류 등에서 인상적인 성능을 보여주었습니다. 2025년에 발표된 또 다른 연구에서는 설명 가능성을 갖춘 MFCC 특징량을 활용하여 파킨슨병의 조기 진단에서 91.11%의 정확도와 0.9125의 AUC를 달성한 CNN-MLP-RNN 하이브리드 모델이 주목을 받았습니다. 임상의와 규제 당국은 뛰어난 성능을 발휘하고, 특징량 수준에서 이해하기 쉬운 추론을 제공하는 시스템을 선호하기 때문에 이러한 발전은 음성 바이오마커 시장에 있어 매우 중요합니다. 설명 가능하고 범용성이 높은 모델을 보유한 공급업체는 병원, 규제 당국 및 제약 업계에서 더 높은 수용을 얻을 수 있는 여건을 갖추고 있습니다.

언어 및 인구통계학적 요인에 걸친 임상적 표준화의 부족

언어, 녹음 조건, 샘플 설계의 편차가 모델의 신뢰성에 영향을 미치기 때문에 표준화는 음성 바이오마커 시장에 있어 여전히 중대한 과제로 남아 있습니다. 2025년 리뷰에서는 1만 7,298건의 비압축 오디오 샘플 분석을 바탕으로, MP3, M4A, WMA 등의 압축 오디오 형식이 지터와 시머를 왜곡한다는 점이 지적되었습니다. 또 다른 리뷰에서는 주요 우울 장애에 관한 67건의 머신러닝 연구 중 94%가 100명 미만의 피험자를 대상으로 했으며, 증상의 중증도 차이를 고려한 연구는 고작 13%에 불과하다는 점이 지적되었습니다. 이러한 과제로 인해, 공개된 정확도에 대한 주장을 일상 진료나 전 세계적인 적용 과정에서 신뢰성 있게 활용하는 데 차질이 생기고 있으며, 보다 대규모이고 일관성 있는 데이터 세트가 표준으로 자리 잡을 때까지는 검증과 확장성이 제한될 수밖에 없습니다.

부문별 분석

2025년, 음성 바이오마커 시장에서 기술별 점유율 측면에서 음향 특징량 추출이 34.58%를 차지하며 가장 큰 부문이 되었습니다. 이러한 우위는 지터, 시머, MFCC, 기본 주파수 등의 매개변수를 활용하고, 임상 현장에서 입증된 사용 실적을 바탕으로 한 것입니다. 이러한 특징들은 초기 알고리즘 및 제품 개발에 반영되어 왔기 때문에 병원, 연구 그룹, 임상시험 관리자들에게 여전히 기초가 되고 있습니다. 프로소디적 특징량은 정서 장애나 파킨슨병과 관련된 발화 변화 분석에 중요한 반면, 스펙트럼 특징량은 호흡기 및 심혈관계 평가에 필수적입니다.

하이브리드 특징량 모델은 2031년까지 연평균 성장률(CAGR) 16.52%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 기술이 될 전망입니다. 이러한 성장은 질환, 언어, 연령대를 아우르는 범용성을 갖춘 모델에 대한 수요를 반영하고 있습니다. 업계에서는 검증 요건이 더욱 복잡해졌음에도 불구하고, 하이브리드 시스템이 상업적으로 보급됨에 따라 음향 특징량을 운영 기반으로 유지해 나갈 가능성이 높을 것으로 보입니다.

2025년, 음성 바이오마커 시장에서 클라우드 기반 플랫폼은 67.88%를 차지하며 주도적인 위치를 유지했습니다. 이러한 장점은 하드웨어의 제약 없이 대규모 모델을 실행할 수 있다는 점, 도입 후에도 모델을 업데이트할 수 있다는 점, 그리고 API를 통해 EHR 시스템과 통합할 수 있다는 점에 기인합니다. 이 아키텍처는 헬스케어 분야의 기존 데이터 관리 관행과 부합하며, 통합된 모델 거버넌스를 지원합니다.

클라우드 기반 플랫폼은 2031년까지 연평균 성장률(CAGR) 17.30%를 기록하며 가장 빠르게 성장하는 플랫폼 유형으로 자리매김할 것으로 전망됩니다. 또한, 임베디드형 SDK 및 API 솔루션의 보급이 확대되면서 원격 의료 플랫폼, 콜센터, 문서 작성 도구와의 원활한 통합이 가능해졌습니다. 이 두 가지 접근 방식을 통해 클라우드 플랫폼이 주도적인 위치를 유지하는 한편, 임베디드 솔루션은 시장 점유율을 확대되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 음성 바이오마커 시장 매출의 38.99%를 차지하며 최대 지역 블록으로서의 위상을 유지했습니다. 이 지역은 견고한 디지털 헬스 인프라, 활발한 임상 연구 네트워크, 그리고 소프트웨어 주도의 엔드포인트 개발에 대한 제약 기업의 적극적인 참여라는 이점을 누리고 있습니다. 미국은 상환 제도의 불균형이라는 과제가 있기는 하지만, 의료 소프트웨어에 대한 규제 방향이 명확하기 때문에 시장을 선도하고 있습니다. 캐나다는 학술 및 임상 연구 파트너십을 통해 기여하고 있으며, 멕시코는 도입 초기 단계에 있는 원격의료의 확대가 건강 증진 및 선별 검사에 중점을 둔 음성 솔루션을 주도하고 있어 미래성을 보여주고 있습니다.

유럽은 2025년에 시장 점유율 2위를 차지할 전망이며, 독일, 영국, 프랑스의 병원 디지털화와 임상 연구의 진전이 이를 주도하고 있습니다. 또한, 이 분야는 기준 및 거버넌스에도 영향을 미치고 있으며, eVoiceNet과 같은 이니셔티브를 통해 음성 바이오마커 개발을 위한 통일된 원칙을 추진하고 있습니다. 음성 데이터를 개인정보로 취급하는 GDPR(EU 개인정보보호규정) 규정은 동의, 데이터 이용 및 저장과 관련하여 더 엄격한 요건을 부과하고 있으며, 국경을 넘는 데이터 교환을 지연시키는 한편, 보다 견고한 개인정보 보호 및 검증 관행을 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 16.64%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 고령화 사회, 높은 스마트폰 보급률, 그리고 음성 기반 모니터링과 연계된 AI를 활용한 노인 돌봄 노력을 통해 이 지역을 선도하고 있습니다. 이 연구에서는 지역별 고유 모델의 가치가 강조되고 있으며, 일본의 음향 모델은 우울증 분류에서 AUC 0.992를 달성했습니다. 인도에서는 비용 대비 효과가 높은 다국어 음성 데이터를 수집할 수 있으며, 중국에서는 현지 언어의 표준화가 진행되고 있지만, 보다 광범위한 상용화는 임상 프레임워크의 성숙도에 달려 있습니다. 중동 및 아프리카와 남미는 여전히 소규모 시장이지만, 브라질은 포르투갈어 연구의 중심지로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the vocal biomarkers market size is projected to be USD 3.33 billion in 2025, USD 3.84 billion in 2026, and reach USD 7.77 billion by 2031, growing at a CAGR of 15.15% from 2026 to 2031.

This report is Segmented by Technique (Acoustic Features, Prosodic, and More), Platform Type (Cloud-Based Platforms, Web-Based Platforms, and More), Application (Mental Health Monitoring, and More), End User (Hospitals, Pharma and Biotech, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Vocal Biomarkers Market Trends and Insights

Rising Use of Voice as a Non-Invasive Digital Health Tool

The vocal biomarkers market is thriving, driven by the ability to collect voice data using standard smartphones. This innovation eliminates the need for invasive methods like blood sampling, imaging systems, and wearable sensors. Such ease of deployment is particularly beneficial in rural and underserved areas, where access to healthcare is limited. Research highlighted Sonde Health's vocal biomarker tool, which can assess asthma exacerbation risk using just 6-second vowel recordings. Notably, higher normalized scores indicated a 3.57-fold increased risk of exacerbation in cohorts from both the U.S. and India, spanning five Indian languages. This commercial evidence underscores the vocal biomarkers market's potential to expand into multilingual regions without the need to reconstruct models for each language. Furthermore, there's a noticeable demand in depression screening. The Annals of Family Medicine noted a stark contrast: while routine screening is recommended, only 4% of primary care patients were screened as of 2025. This gap highlights the potential of short-form voice tools in early triage processes.

AI and Machine Learning Improve Signal Extraction Accuracy

The vocal biomarkers market is advancing as model designs evolve, shifting from narrowly defined features to broader representations trained on diverse clinical datasets. In May 2026, the Bridge2AI Consortium unveiled VoiceFM, a dual-encoder model trained on their Voice dataset. This model demonstrated impressive capabilities, including cross-site generalization, Parkinson's detection across English, Spanish, and Mandarin, and multi-condition classification. Another study in 2025 highlighted a hybrid CNN-MLP-RNN model achieving 91.11% accuracy and an AUC of 0.9125 for early Parkinson's detection, utilizing MFCC features with explainability. Such advancements are pivotal for the vocal biomarkers market as clinicians and regulators favor systems that perform well and provide understandable reasoning at the feature level. Vendors with explainable and versatile models are poised for heightened acceptance in hospitals, regulatory circles, and pharmaceutical endpoints.

Limited Clinical Standardization Across Languages and Demographics

Standardization remains a critical challenge for the vocal biomarkers market due to variations in language, recording conditions, and sample design, which affect model reliability. A 2025 review highlighted that compressed audio formats like MP3, M4A, and WMA distort jitter and shimmer, based on an analysis of 17,298 uncompressed voice samples. Another review noted that 94% of 67 machine learning studies on major depressive disorder used fewer than 100 participants, with only 13% addressing varying symptom severity. These gaps hinder the reliable application of published accuracy claims in routine care or global deployment, limiting validation and scalability until larger, harmonized datasets become standard.

Other drivers and restraints analyzed in the detailed report include:

- Remote Patient Monitoring Expands Clinical Utility

- Broader Utility Across Mental Health, Neurology, and Cardiology

- Regulatory Uncertainty for Diagnostic and Monitoring Use Cases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, acoustic feature extraction held a 34.58% share of the vocal biomarkers market by technique, making it the largest segment. This dominance is due to its established use in clinical settings, leveraging parameters like jitter, shimmer, MFCCs, and fundamental frequency. These features remain the foundation for hospitals, research groups, and trial managers, given their integration into earlier algorithms and product development. Prosodic features are significant for affective disorders and Parkinson's-related speech changes, while spectral features are vital for respiratory and cardiovascular assessments.

Hybrid feature models are expected to grow at a 16.52% CAGR through 2031, making them the fastest-growing technique. This growth reflects the need for models that generalize across diseases, languages, and age groups. The industry is likely to retain acoustic features as the operational base while hybrid systems gain commercial traction, despite their more complex validation requirements.

Cloud-based platforms accounted for 67.88% of the vocal biomarkers market in 2025, maintaining their leadership position. Their dominance is driven by the ability to run large models without hardware constraints, update models post-deployment, and integrate with EHR systems via APIs. This architecture aligns with existing data management practices in healthcare and supports centralized model governance.

Cloud-based platforms are projected to grow at a 17.30% CAGR through 2031, remaining the fastest-growing platform type. Embedded SDK and API solutions are also gaining traction, enabling seamless integration into telehealth platforms, call centers, and documentation tools. This dual approach positions cloud platforms as dominant while embedded solutions expand market reach.

Complete Report Scope:

- By Technique

- Acoustic Features

- Prosodic Features

- Spectral Features

- Linguistic Features

- Hybrid Feature Models

- By Platform Type

- Cloud-Based Platforms

- Web-Based Platforms

- Mobile Applications

- Embedded SDK and API Solutions

- By Application

- Mental Health Monitoring

- Neurological Disorder Detection

- Respiratory Condition Monitoring

- Cardiovascular Condition Monitoring

- General Wellness and Preventive Screening

- Clinical Research and Trial Monitoring

- By End User

- Hospitals and Clinics

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations

- Academic and Research Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 38.99% of the global vocal biomarkers market revenue, maintaining its position as the largest regional block. The region benefits from a strong digital health infrastructure, active clinical research networks, and significant pharmaceutical involvement in software-driven endpoint development. The U.S. leads due to clearer regulatory pathways for medical software, despite challenges with uneven reimbursement. Canada contributes through academic and clinical research partnerships, while Mexico, though in early adoption stages, shows potential with telehealth expansion driving wellness and screening-focused voice solutions.

Europe held the second-largest market share in 2025, driven by advancements in hospital digitization and clinical research in Germany, the U.K., and France. The region also influences standards and governance, with initiatives like eVoiceNet promoting unified principles for vocal biomarker development. GDPR regulations, treating voice data as personal information, impose stricter requirements on consent, data usage, and storage, which, while slowing cross-border data exchange, encourage stronger privacy and validation practices.

Asia-Pacific is projected to grow at a 16.64% CAGR through 2031, making it the fastest-growing region. Japan leads with its aging population, high smartphone penetration, and AI-driven elder care initiatives aligning with voice-based monitoring. Studies highlight the value of region-specific models, with Japanese acoustic models achieving an AUC of 0.992 in depression classification. India supports cost-effective multilingual voice data collection, while China progresses with local language standardization, though broader commercialization depends on maturing clinical frameworks. The Middle East, Africa, and South America remain smaller markets, but Brazil is emerging as a hub for Portuguese-language research.

- audEERING GmbH

- Beyond Verbal Communication Ltd.

- Biosensics, Inc.

- Boston Technology Corporation

- Canary Speech, Inc.

- Cogito Corporation

- ConversationHealth Inc.

- Ellipsis Health, Inc.

- EVOCAL Health GmbH

- IBM

- Kintsugi Mindful Wellness, Inc.

- Medical Information Technology

- Noah Labs GmbH

- PST Inc.

- Sharecare, Inc.

- Sonde Health

- VoiceMed Italia S.r.l.

- VoiceSense Ltd.

- Winterlight Labs Inc.

- Zana Technologies GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Use of Voice as a Non-Invasive Digital Biomarker

- 4.2.2 AI and Machine Learning Improve Signal Extraction From Short Speech Samples

- 4.2.3 Remote Patient Monitoring Expands Clinical and At-Home Use Cases

- 4.2.4 Broader Utility Across Mental Health, Neurology, Respiratory Care, and Cardiology

- 4.2.5 Integration Into Telehealth, Call Centers, and Enterprise Wellness Programs

- 4.2.6 Growing Research Validation and Clinical Trial Adoption

- 4.3 Market Restraints

- 4.3.1 Limited Clinical Standardization Across Languages, Accents, and Recording Conditions

- 4.3.2 Regulatory Uncertainty for Diagnostic and Monitoring Claims

- 4.3.3 Need for Larger Longitudinal Datasets and External Validation

- 4.3.4 Data Privacy, Consent, and Governance Complexity for Voice Data

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Technique

- 5.1.1 Acoustic Features

- 5.1.2 Prosodic Features

- 5.1.3 Spectral Features

- 5.1.4 Linguistic Features

- 5.1.5 Hybrid Feature Models

- 5.2 By Platform Type

- 5.2.1 Cloud-Based Platforms

- 5.2.2 Web-Based Platforms

- 5.2.3 Mobile Applications

- 5.2.4 Embedded SDK and API Solutions

- 5.3 By Application

- 5.3.1 Mental Health Monitoring

- 5.3.2 Neurological Disorder Detection

- 5.3.3 Respiratory Condition Monitoring

- 5.3.4 Cardiovascular Condition Monitoring

- 5.3.5 General Wellness and Preventive Screening

- 5.3.6 Clinical Research and Trial Monitoring

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Pharmaceutical and Biotechnology Companies

- 5.4.3 Contract Research Organizations

- 5.4.4 Academic and Research Institutes

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 audEERING GmbH

- 6.3.2 Beyond Verbal Communication Ltd.

- 6.3.3 Biosensics, Inc.

- 6.3.4 Boston Technology Corporation

- 6.3.5 Canary Speech, Inc.

- 6.3.6 Cogito Corporation

- 6.3.7 ConversationHealth Inc.

- 6.3.8 Ellipsis Health, Inc.

- 6.3.9 EVOCAL Health GmbH

- 6.3.10 IBM Corporation

- 6.3.11 Kintsugi Mindful Wellness, Inc.

- 6.3.12 Medical Information Technology, Inc.

- 6.3.13 Noah Labs GmbH

- 6.3.14 PST Inc.

- 6.3.15 Sharecare, Inc.

- 6.3.16 Sonde Health, Inc.

- 6.3.17 VoiceMed Italia S.r.l.

- 6.3.18 VoiceSense Ltd.

- 6.3.19 Winterlight Labs Inc.

- 6.3.20 Zana Technologies GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment