|

시장보고서

상품코드

2072859

의료기기 재처리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Device Reprocessing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

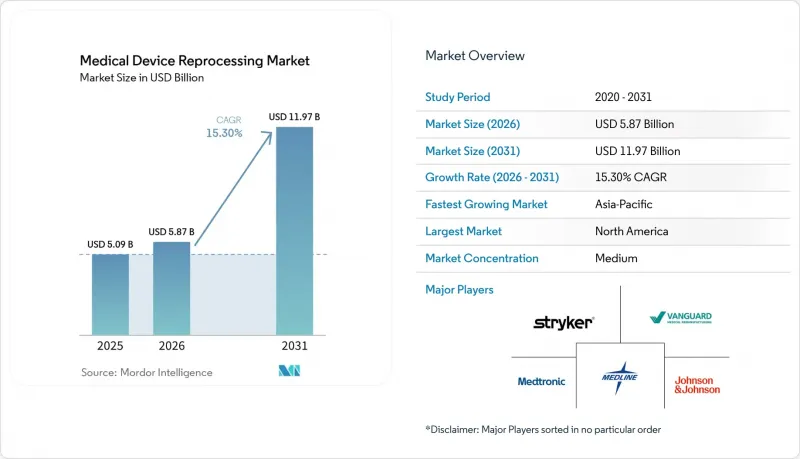

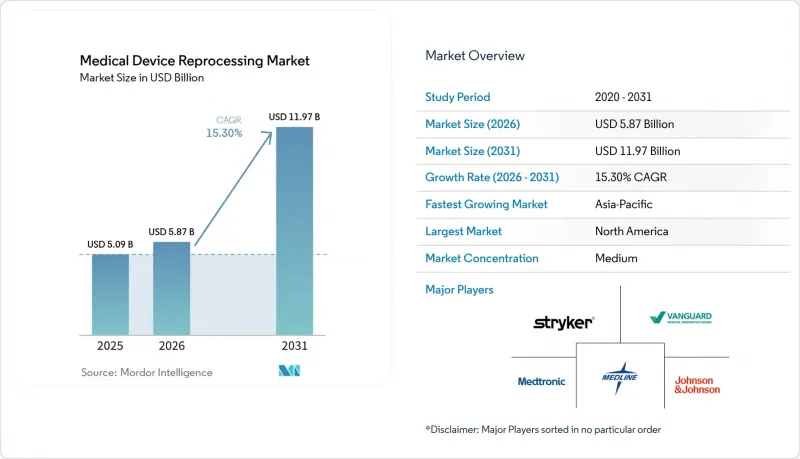

Mordor Intelligence에 의하면, 의료기기 재처리 시장 규모는 2025년 50억 9,000만 달러에서 2026년에는 58억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 15.30%로 성장을 지속하여, 2031년에는 119억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기기 유형(크리티컬, 세미크리티컬, 논크리티컬), 제공 형태(재처리된 기기, 재처리 지원 및 서비스), 적용 분야(순환기, 소화기, 정형외과, 산부인과, 일반외과), 최종 사용자(병원, ASC, 전문 클리닉), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 의료기기 재처리 시장 동향과 인사이트

병원공급 비용 억제 및 시술별 지속적인 비용 절감

2025년, AMDR 가맹 기업들은 18개국 11,458개 의료 기관에 3,938만 7,336개의 재처리된 일회용 의료기기를 판매하여, 병원 측에 4억 9,550만 달러의 입증된 비용 절감 효과를 가져다주었습니다. AMDR는 미국의 모든 병원이 재처리 도입률 상위 10%에 속하는 시설과 동일한 비율로 재처리를 실시할 경우, 연간 최대 24억 3,000만 달러를 절감할 수 있다고 지적했습니다. 이러한 차이는 주요 의료 시스템에서 의료기기 재처리 시장에 대한 관심이 높아지고 있음을 여실히 보여주고 있습니다. 이러한 시스템에서는 구매 결정이 영업이익률, 유동성 및 공급 효율성 측면에서 평가됩니다. 재정적 이해관계는 재향군인 보건국(VHA)을 둘러싼 논의에서도 분명히 드러납니다. AMDR의 추산에 따르면, 현행 규제로 인해 2025년에는 납세자들이 연간 1억 6,700만 달러를 절약할 수 있는 기회가 실현되지 못할 것으로 보입니다. 의료기기 1대당 비용 절감률은 OEM 정가와 비교했을 때 40-60%에 달하는 경우가 많기 때문에 의료기기 재처리 시장은 시술 단위별 지속적인 비용 절감을 우선시하는 조달 전략과 잘 부합합니다.

의료 시스템에 대한 지속가능성 보고 압력

병원 시스템이 스코프 3 배출량에 대한 진척 상황을 공개해야 한다는 압력이 커지는 가운데, 지속가능성 목표는 의료기기 재처리 시장에서 중요한 요소로 부상하고 있습니다. 재처리된 의료기기는 비용과 배출량을 모두 줄일 수 있는 몇 안 되는 공급망 상의 조치로 인식되고 있으며, 조달 팀에게 비용과 기후 목표 간의 균형을 맞추기 위한 명확한 전략을 제시하고 있습니다. 2025 회계연도에 카디널 헬스의 지속가능 기술 사업부는 2,160만 개의 일회용 의료기기를 회수하여 660만 파운드의 폐기물이 매립지로 보내지는 것을 방지하는 동시에, 1,900메트르톤의 이산화탄소 환산 배출량을 감축했습니다. 유럽의 정책 동향도 이러한 추세를 더욱 뒷받침하고 있으며, 덴마크는 2025년 1월에 일회용 의료기기의 상업적 재처리를 승인했고, 프랑스는 2025년 9월에 병원에서 재처리 실험을 시작했습니다. 의료기기 재처리 시장에서 조달 규정상 환경 성과가 공급업체의 가치를 평가하는 데 있어 필수적인 요소로 점점 더 인식되고 있습니다.

OEM 계약 전략과 기기 락인

OEM 계약 관행은 특히 독자적인 시스템의 영향을 받는 고부가가치 부문에서 의료기기 재처리 시장을 여전히 제약하고 있습니다. 2025년 5월, 배심원단은 존슨앤드존슨의 자회사인 바이오센스 웹스터에 대해 불리한 판결을 내렸고, 2025년 9월에는 영구적 금지 명령이 발령되어, 임상 지원을 신규 기기 구매와 연계하는 행위, 이식형 칩을 이용해 재처리된 기기를 무력화하는 행위, 재처리에 필수적인 사용 후 기기의 제공을 보류하는 행위 등이 금지되었습니다. 손해배상액이 3배로 증액된 결과, 총액이 4억 4,200만 달러에 달하면서 이 문제의 상업적 중요성이 부각되었습니다. 그러나 소프트웨어에 의한 접근 차단, 직원 교육 축소, 병원 이전을 방해하는 제한적인 계약 구조 등, 보다 온건한 형태의 저항은 여전히 계속되고 있습니다. 연방 정부 기관은 2025년, 의료기기 부문의 반경쟁적 관행을 신고할 수 있는 익명 신고 포털을 개설하여 이 문제를 해결했습니다. 일부 제품 카테고리에서는 접근성이 개선되었으나, 조달 유연성의 불균형으로 인해 다른 분야의 진전이 여전히 더딘 상황입니다.

부문별 분석

2025년, 의료기기 재처리 시장에서는 "준중요 장비"가 주도적인 위치를 차지하며, 해당 부문 매출의 44.45%를 차지했습니다. 이러한 확고한 입지는 유연 내시경이나 호흡 요법용 회로 등의 제품에 대해 확립된 재처리 공정이 존재하기 때문입니다. 많은 병원의 멸균 공급 부서에서는 이러한 기기에 대한 고수준 소독 절차가 표준화되어 있습니다. 병원에서 풍부한 운영 실적과 명확한 처리 절차가 마련되어 있기 때문에 임상의들은 이러한 범주를 더 쉽게 수용하는 경향이 있습니다. 전극이나 맥박 산소 측정기의 센서 등을 포함하는 "비중요 장비"가 나머지 점유율을 차지했습니다. 이러한 품목에 대해서도 재처리가 허용되고 있지만, 초기 취득 비용이 낮기 때문에 단위당 비용 절감액은 적습니다.

핵심 의료기기는 2031년까지 연평균 성장률(CAGR) 16.45%라는 견조한 성장이 예상되며, 의료기기 재처리 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 급속한 성장은 미국 내 재처리된 전기생리학용 카테터 및 복강경용 기기에 대한 수용 확대는 물론, 유럽에서 EU MDR(의료기기 규정)의 틀 하에 적용 대상 범위가 확대된 것과도 관련이 있습니다. 또한, 2025년 9월 Biosense Webster사에 내려진 금지 명령에 따라, 그동안 규제가 엄격했던 의료기기 분야에 대한 진입 조건이 완화되었습니다. 현재 시장 점유율의 대부분을 차지하고 있는 것은 준중요 의료기기이지만, 가치 창출의 중심이 중요 의료기기로 이동하고 있는 것으로 나타났습니다. 이러한 전환은 디지털 감사 추적 기록 및 검증 시스템의 등장으로 촉진되고 있으며, 임상 및 규제 당국의 심사를 위한 복잡한 재처리 프로그램이 간소화되고 있습니다.

2025년, 재처리 의료기기는 제공 형태별 매출의 62.55%를 차지했으며, 시장이 서비스만 제공하는 계약보다 물리적 기기의 처리량에 더 크게 의존하고 있음이 드러났습니다. 소화기내과나 순환기내과 등의 분야에서 높은 수요가 이 부문을 견인하고 있으며, 병원에서는 이러한 의료기기를 빈번하게 교체하기 때문에 비용 절감 효과를 직접 측정할 수 있기 때문입니다. 이러한 추세는 광범위한 병원 네트워크 전반에 걸쳐 일관된 조달 리듬을 촉진하고 있습니다. 또한, 구매자들은 대개 특정 의료기기 부문을 통해 시장에 진입한 뒤, 이를 바탕으로 더 광범위한 파트너십으로 확대해 나가는 경향을 보여주고 있습니다.

"재처리 지원 및 서비스"는 2031년까지 연평균 성장률(CAGR) 16.77%라는 견실한 성장이 예상되며, 의료기기 재처리 시장에서 가장 역동적인 부문으로서의 입지를 확고히 다져가고 있습니다. 주요 의료 시스템에서는 회수 물류, 검증 지원, 추적 소프트웨어를 개별적으로 구매하기보다는 통합된 프로그램 형태로 요구하는 경향이 강해지면서, 통합 솔루션에 대한 수요가 증가하고 있습니다. 카디널 헬스(Cardinal Health)는 2026년, 이러한 추세를 반영하는 형태로 ValueLink 애널리틱스와 자사의 '지속 가능한 기술' 서비스를 통합하여 대규모 의료 시스템을 위한 밸류체인의 효율성을 높였습니다. 2025년 라이프사이클 조사에서는 환경 개선의 핵심 분야로 회수 물류와 멸균 설계가 강조되었으며, 서비스 주도형 차별화의 중요성이 입증되었습니다. 시장 경쟁으로 인해 의료기기의 이익률이 압박받는 가운데, 비용 절감, 규정 준수, 환경 성능을 통합된 서비스 형태로 제공할 수 있는 사업자는 시장에서 더 큰 가치를 창출할 것으로 전망됩니다.

지역별 분석

2025년, 북미는 의료기기 재처리 시장 전체 매출의 42.99%를 차지하며 지역별 최대 점유율을 기록했습니다. 이러한 우위는 상업적 보급 범위, 강력한 공동구매기구(GPO) 체계, 그리고 제3자 재처리 업체에 제조업체와 동등한 기준을 적용하는 규제 환경에서 비롯됩니다. 2026년 3월, 미국 환경보호청(EPA)이 2024년 에틸렌옥사이드 규제의 일부를 재검토할 것을 제안한 것은 멸균 정책이 지역 공급 능력에 미치는 직접적인 영향을 여실히 드러냈습니다.

유럽은 의료기기 재처리 시장에 있어 여전히 중요한 규제 거점이며, 그 보급 상황은 각국 고유의 법적 체계와 병원의 조달 방침에 크게 좌우되고 있습니다. 2025년, 프랑스는 제2025-895호 정령에 따라 전기생리학용 카테터를 포함한 일회용 의료기기의 재처리에 관한 병원 내 시범 운영을 시작했습니다. 프랑스의 공공 정책 재검토에 따르면, 재처리된 의료기기 1대당 35%에서 59%의 비용 절감이 예상되며, 이 시범 사업이 확대된다면 더 많은 병원이 참여하도록 촉진할 것으로 보입니다. 2025년 1월 덴마크가 일회용 의료기기의 상업적 재처리를 승인한 것은 지속가능성을 중시하는 의료 시스템으로의 전환을 보여주는 것이었습니다. EU MDR 제17조 및 ISO 13485:2016은 여전히 시장 진입 요건을 규정하고 있으며, 검증된 품질 시스템과 탄탄한 문서화 역량을 갖춘 사업자를 우대하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.96%를 기록하며 성장할 것으로 예상되며, 의료기기 재처리 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이러한 성장은 중국, 인도, 한국, 호주, 일본 등 여러 국가에서 수술 건수가 증가하고, 병원 인프라에 대한 투자가 이루어지며, 조달 관행이 개선됨에 따라 주도되고 있습니다. 호주 뉴캐슬 베레스필드에 위치한 카디널 헬스의 재제조 시설은 2027 회계연도에 본격적으로 가동을 시작할 예정이며, 이는 해당 회사의 중요한 국제적 확장을 상징하는 것입니다. 한국과 일본은 규제 측면에서 성숙도가 높은 반면, 중국과 인도에서는 규정 준수 체계가 강화되고 병원의 조달 시스템이 정비됨에 따라 대규모 비즈니스 기회가 창출되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the medical device reprocessing market size is expected to grow from USD 5.09 billion in 2025 to USD 5.87 billion in 2026 and is forecast to reach USD 11.97 billion by 2031 at 15.30% CAGR over 2026-2031.

This report is Segmented by Device Type (Critical, Semi-Critical, Non-Critical), Offering Type (Reprocessed Devices, Reprocessing Support and Services), Application (Cardiology, Gastroenterology, Orthopedics, Gynecology, General Surgery), End User (Hospitals, Ascs, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Medical Device Reprocessing Market Trends and Insights

Hospital Supply Cost Containment and Recurring Per-Procedure Savings

In 2025, AMDR member companies sold 39,387,336 reprocessed single-use devices to 11,458 healthcare facilities across 18 countries, generating USD 495.5 million in documented savings for hospitals. AMDR highlighted that if all US hospitals reprocessed at the rate of the top 10% of adopters, the annual savings opportunity could reach USD 2.43 billion. This gap emphasizes the increasing focus on the medical device reprocessing market within major health systems, where purchasing decisions are evaluated against operating margins, liquidity, and supply efficiency. Financial stakes are also evident in the Veterans Health Administration debate, where AMDR estimated that current restrictions left USD 167 million in annual taxpayer savings unrealized in 2025. With device-level savings often reaching 40 to 60% against OEM list prices, the medical device reprocessing market aligns well with procurement strategies prioritizing repeatable savings at the procedure level.

Sustainability Reporting Pressure on Health Systems

Sustainability goals are becoming a key factor in the medical device reprocessing market as hospital systems face increasing pressure to demonstrate progress on Scope 3 emissions. Reprocessed devices are identified as a rare supply-chain action that reduces both costs and emissions, offering procurement teams a clear strategy to balance cost and climate objectives. In fiscal 2025, Cardinal Health's Sustainable Technologies business collected 21.6 million single-use devices, diverting 6.6 million pounds of waste from landfills, and avoiding 1,900 metric tons of carbon dioxide equivalent emissions. European policy movements further support this trend, with Denmark authorizing commercial single-use device reprocessing in January 2025 and France initiating a hospital reprocessing experiment in September 2025. Procurement rules increasingly recognize environmental performance as integral to supplier value in the medical device reprocessing market.

OEM Contracting Tactics and Device Lock-In

OEM contracting practices continue to limit the medical device reprocessing market, particularly in high-value categories influenced by proprietary systems. In May 2025, a jury ruled against Johnson & Johnson's Biosense Webster unit, and a permanent injunction in September 2025 prohibited actions such as linking clinical support to new device purchases, disabling reprocessed devices with embedded chips, and withholding used devices essential for reprocessing. The damages totaled USD 442 million after being tripled, highlighting the commercial significance of the issue. However, softer resistance persists, including software lockouts, reduced staff training, and restrictive contract structures that hinder hospital transitions. Federal agencies addressed the issue in 2025 by launching an anonymous reporting portal for anticompetitive practices in the medical device sector. While access has improved in some product categories, inconsistent procurement freedom continues to slow progress in other areas.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Tray and Cycle Tracking Improves Compliance

- Expanded OEM Reprocessed-Device Portfolios

- Clinical Trust Barriers for Reprocessed High-Acuity Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Semi-Critical Devices dominated the medical device reprocessing market, accounting for 44.45% of the segment's revenue. This stronghold is attributed to established reprocessing pathways for items like flexible endoscopes and respiratory therapy circuits. Many hospital sterile supply departments have standardized high-level disinfection protocols for these devices. Clinicians are more accepting of these categories due to hospitals' extensive operating experience and clear handling routines. Non-Critical Devices, which include electrodes and pulse oximeter sensors, made up the remaining share. While reprocessing is accepted for these items, the savings per unit are smaller due to their lower original acquisition costs.

Critical Devices are set to experience a robust growth rate of 16.45% CAGR through 2031, making them the fastest-growing category in the medical device reprocessing market. This surge is linked to the growing acceptance of reprocessed electrophysiology catheters and laparoscopic instruments in the U.S., alongside an expansion of eligibility under EU MDR frameworks in Europe. Furthermore, a September 2025 injunction against Biosense Webster has eased access conditions in a previously constrained device class. While Semi-Critical Devices currently dominate the market share, the trend indicates a shift in value creation towards critical devices. This shift is bolstered by the advent of digital audit trails and validation systems, simplifying complex reprocessing programs for clinical and regulatory reviews.

In 2025, Reprocessed Medical Devices made up 62.55% of the offering-type revenue, underscoring the market's reliance on physical device throughput over service-only contracts. High demand in fields like gastroenterology and cardiology drives this segment, as hospitals frequently replace these items and can directly measure savings. This dynamic fosters a consistent procurement rhythm across extensive hospital networks. It also highlights that buyers typically enter the market through specific device categories before branching out into broader partnerships.

Reprocessing Support and Services is on track to grow at a robust 16.77% CAGR through 2031, positioning it as the more dynamic segment of the medical device reprocessing market. Major health systems are increasingly seeking integrated solutions, desiring collection logistics, validation support, and tracking software as a cohesive program rather than standalone purchases. Cardinal Health exemplified this trend in 2026, merging ValueLink analytics with its Sustainable Technologies offering to enhance supply-chain efficiency for large health systems. A 2025 life cycle study emphasized collection logistics and sterilization design as key areas for environmental enhancement, bolstering the case for service-led differentiation. As price competition tightens device margins, operators demonstrating savings, compliance, and environmental performance as a bundled service stand to capture more value in the market.

Complete Report Scope:

- By Device Type

- Critical Devices

- Semi-Critical Devices

- Non-Critical Devices

- By Offering Type

- Reprocessed Medical Devices

- Reprocessing Support and Services

- By Application

- Cardiology

- Gastroenterology

- Orthopedics

- Gynecology

- General Surgery

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 42.99% of global revenue in the medical device reprocessing market, securing the largest regional share. This dominance stems from extensive commercial adoption, strong Group Purchasing Organization frameworks, and a regulatory environment holding third-party reprocessors to standards similar to original manufacturers. The US EPA's March 2026 proposal to revisit parts of the 2024 ethylene oxide rule highlighted the direct impact of sterilization policies on regional supply capacity.

Europe remains a critical regulatory hub for the medical device reprocessing market, with adoption heavily influenced by country-specific legal frameworks and hospital procurement policies. In 2025, France initiated a hospital trial for reprocessing single-use devices, including electrophysiology catheters, under Decret n° 2025-895. A public policy review in France estimated 35% to 59% savings per reprocessed device, supporting broader hospital participation if the pilot expands. Denmark's approval of commercial reprocessing for single-use devices in January 2025 signaled a shift toward sustainability-focused health systems. EU MDR Article 17 and ISO 13485:2016 continue to shape market entry, favoring operators with validated quality systems and strong documentation capabilities.

Asia-Pacific is projected to grow at a 15.96% CAGR through 2031, making it the fastest-growing region in the medical device reprocessing market. Growth is driven by rising surgical volumes, hospital infrastructure investments, and improved procurement practices in countries like China, India, South Korea, Australia, and Japan. Cardinal Health's remanufacturing facility in Beresfield, Newcastle, Australia, set for full operation in FY2027, marks a significant international expansion. While South Korea and Japan offer regulatory maturity, China and India present large-scale opportunities as compliance frameworks strengthen and hospital purchasing systems formalize.

- Arjo AB

- Avante Health Solutions

- B. Braun

- Cardinal Health

- Getinge

- Innovative Health, LLC

- Johnson & Johnson

- Konoike Co., Ltd.

- Medline Industries

- MedSalv Australia Pty Ltd

- Medtronic

- MidWest Reprocessing Center

- NEScientific

- Olympus

- ReNu Medical, Inc.

- SteriPro Canada Inc.

- STERIS

- Stryker

- SureTek Medical

- Vanguard

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Hospital Supply Cost Containment and Recurring Per-Procedure Savings

- 4.1.2 Sustainability Reporting Pressure on Health Systems

- 4.1.3 Expanded OEM Reprocessed-Device Portfolios

- 4.1.4 Heterogeneous Reprocessing Rules Across Key Markets

- 4.1.5 AI-Enabled Tray and Cycle Tracking Improves Compliance Visibility

- 4.1.6 EtO Capacity, Emissions, and Permitting Constraints Shift Demand to Reprocessed Devices

- 4.2 Market Restraints

- 4.2.1 OEM Contracting Tactics and Device Lock-In

- 4.2.2 Clinical Trust Barriers for Reprocessed High-Acuity Devices

- 4.2.3 Limited Device Eligibility and Validation Burden

- 4.2.4 Sterilization Capacity Constraints and Capital Intensity

- 4.3 Value/Supply Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Device Type

- 5.1.1 Critical Devices

- 5.1.2 Semi-Critical Devices

- 5.1.3 Non-Critical Devices

- 5.2 By Offering Type

- 5.2.1 Reprocessed Medical Devices

- 5.2.2 Reprocessing Support and Services

- 5.3 By Application

- 5.3.1 Cardiology

- 5.3.2 Gastroenterology

- 5.3.3 Orthopedics

- 5.3.4 Gynecology

- 5.3.5 General Surgery

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Arjo AB

- 6.3.2 Avante Health Solutions

- 6.3.3 B. Braun SE

- 6.3.4 Cardinal Health, Inc.

- 6.3.5 Getinge AB

- 6.3.6 Innovative Health, LLC

- 6.3.7 Johnson & Johnson

- 6.3.8 Konoike Co., Ltd.

- 6.3.9 Medline Industries, LP

- 6.3.10 MedSalv Australia Pty Ltd

- 6.3.11 Medtronic plc

- 6.3.12 MidWest Reprocessing Center

- 6.3.13 NEScientific, Inc.

- 6.3.14 Olympus Corporation

- 6.3.15 ReNu Medical, Inc.

- 6.3.16 SteriPro Canada Inc.

- 6.3.17 STERIS plc

- 6.3.18 Stryker Corporation

- 6.3.19 SureTek Medical

- 6.3.20 Vanguard AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment