|

시장보고서

상품코드

2072861

사이버 나이프 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)CyberKnife - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

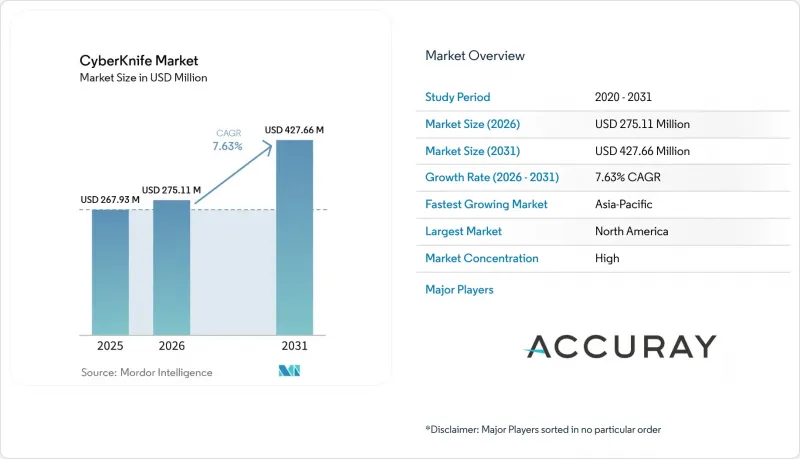

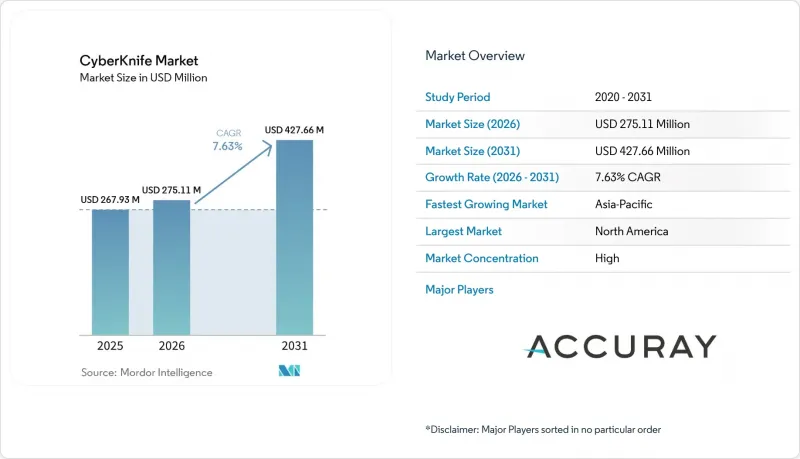

Mordor Intelligence에 의하면, 사이버 나이프 시장 규모는 2025년 2억 6,793만 달러, 2026년 2억 7,511만 달러에서 2031년까지 4억 2,766만 달러로 확대한다고 예측되고 있어 2026-2031년까지 연평균 복합 성장률(CAGR)은 7.63%를 나타낼 전망입니다.

본 보고서는 제품 유형(사이버 나이프 시스템, 소프트웨어 솔루션, 서비스), 적응증(종양 및 암, 혈관 기형, 기타), 최종 사용자(병원·대학 부속 의료센터, 독립형 방사선 치료 센터, 외래 진료 센터), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

세계 사이버 나이프 시장 동향 및 분석

암으로 인한 부담 증가와 치료 수요 증가

사이버 나이프 시장은 주요 의료 시스템 전반에 걸쳐 암 환자 수가 꾸준히 증가하고 사례가 복잡해지는 추세에 힘입어 성장하고 있습니다. 세계보건기구(WHO)에 따르면, 2050년까지 전 세계 암 환자 수는 연간 3,500만 명을 넘어설 것으로 예상되며, 이에 따라 치료 인프라를 그만큼 확충하지 않더라도 더 많은 환자를 수용할 수 있는 정밀 방사선 치료 플랫폼에 대한 장기적인 수요가 꾸준히 증가하고 있습니다. 이러한 수요는 뇌 전이, 척추 전이, 전립선암에서 특히 두드러지며, 원발암 치료로 인한 생존 기간이 연장됨에 따라 국소 집중 치료가 필요한 환자 수가 증가하고 있습니다. 호주의 암 진단 건수는 2045년까지 21만 2,332건에서 31만 8,285건으로 증가할 것으로 예측되며, 이는 고정밀 치료 네트워크에 대한 접근성 확대의 사업적 타당성을 뒷받침하는 것입니다. 오스트리아에서도 방사선 치료 장비공급은 여전히 부족하며, 그 이용률은 EU 평균보다 27%, 경제 수준이 비슷한 국가들보다 34% 낮습니다. 이로 인해 서비스가 미치지 않는 지역에서 사이버 나이프를 새롭게 도입할 여지가 생겨나고 있습니다. 이러한 공급 격차가 지속되는 가운데, 암 치료 수요가 방사선 치료 수용 능력을 웃도는 속도로 증가하고 있는 지역에서 사이버 나이프 시장이 가장 큰 수혜를 볼 것으로 전망됩니다.

비침습적이며 장기를 보존하는 치료 방식에 대한 지향

사이버 나이프 시장은 임상 결과가 동등한 경우 수술을 피하려는 비침습적 치료에 대한 광범위한 선호 추세로부터도 혜택을 받고 있습니다. 사이버 나이프의 실시간 동작 추적 기능인 Synchrony를 통해, 임상의는 환자의 움직임에 맞추어 지속적으로 조정을 하면서 흉부, 간, 척추의 표적을 치료할 수 있게 되었으며, 이에 따라 프레임을 이용한 두개내 치료에 그치지 않고 그 용도가 확대되고 있습니다. 2025년에 전정 신경초종 환자를 대상으로 실시된 장기 추적 연구에 따르면, 사이버 나이프 치료 후 25년 시점에서 국소 통제율이 89.3%, 전체 생존율이 97.1%로 보고되었으며, 이는 장기 보존 요법의 지속성에 대한 신뢰를 한층 더 높여주는 결과입니다. 또한, 2025년 베이징 연합 의과대학 병원(Peking Union Medical College Hospital)이 실시한 임상 연구에서는 뇌하수체 선종 및 폐선암의 척추 전이 사례에서 주변 조직에 대한 손상을 최소화하면서 매우 정밀한 선량 조사이 가능함이 확인되어, 두개골 외 부위에서의 보다 광범위한 사용이 지지받고 있습니다. 그 결과, 사이버 나이프 시장은 정확성, 조직 보존, 그리고 수술실 밖에서의 회복을 중시하는 치료 지향적 경향의 확산에 힘입어 성장을 거듭하고 있습니다.

높은 초기 투자 비용과 서비스 부하

사이버 나이프 시장은 시스템 도입 시 발생하는 고액의 초기 비용과 설치 후 지속적으로 발생하는 지원 비용이라는 큰 장벽에 여전히 직면해 있습니다. 일반적인 시스템의 가격은 차폐 공사나 시운전 전 단계에서 500만-700만 달러에 달하기 때문에 신규 프로젝트는 자금력이 있는 대학병원이나 3차 의료기관으로 제한되고 있습니다. 이러한 부담은 설치 후에 더욱 커지게 됩니다. 서비스 계약, 업그레이드, 유지보수로 인해 자산의 사용 연한 동안 지속적인 비용이 발생하기 때문입니다. Accuray의 보고서에 따르면, 2026 회계연도 1-9개월 동안 서비스 매출은 전년 동기 대비 3% 증가한 1억 6,910만 달러를 기록한 반면, 제품 매출은 21% 감소했습니다. 이는 설비 투자 주기의 둔화와 도입 기반의 성숙화가 신규 도입을 위축시키는 한편, 서비스에 대한 의존도를 높이고 있음을 보여줍니다. 멕시코에서는 IMSS가 2025년 12월 첫 사이버 나이프 시스템 가동을 위해 870만 달러를 투자했습니다. 이는 공공 기관이라 할지라도 이러한 프로젝트가 얼마나 대규모인지를 여실히 보여주고 있습니다. 이 때문에 사이버 나이프 시장은 자본 지출과 장기적인 서비스 부담을 모두 감당할 수 있는 의료 시스템에 집중되는 양상이 지속되고 있습니다.

부문별 분석

2025년, 사이버 나이프 시스템 부문은 사이버 나이프 시장 점유율의 48.31%를 차지하며, 하드웨어는 사이버 나이프 시장에서 여전히 가장 큰 제품 카테고리로 자리매김했습니다. 한편, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 8.38%를 기록하며 성장할 것으로 예상되며, 제품 유형별로는 사이버 나이프 시장에서 가장 빠르게 성장하는 분야가 될 전망입니다. 이러한 변화가 중요한 이유는 신규 하드웨어 수주가 주춤하더라도 이미 도입된 시스템이 예방 정비, 원격 진단, 교육, 소프트웨어 업그레이드를 통해 지속적인 수익을 창출하기 때문입니다. Accuray는 2026 회계연도 1-9개월 동안 서비스 매출이 전년 동기 대비 3% 증가한 1억 6,910만 달러를 기록한 반면, 제품 매출은 감소했습니다. 이는 사이버 나이프 시장에서 개별 장비 판매보다 이미 도입된 시스템이 점점 더 중요해지고 있다는 관점을 뒷받침하는 것입니다.

소프트웨어는 치료 계획, 적응형 방사선 치료 및 신속한 가동 개시를 지원하기 위해 광범위한 플랫폼 스택 내에서 여전히 가장 역동적인 계층으로 자리 잡고 있습니다. Accuray는 2024년 6월, 중국 국가의약품감독관리국(NMPA)으로부터 Accuray Precision Treatment Planning System의 승인을 획득했으며, 2025년 9월에는 적응형 방사선 치료 기능과 CyberComm 가동 시작 도구를 통합한 Stellar 솔루션을 출시했습니다. 이번 발표는 사이버 나이프 업계가 소프트웨어, 서비스, 워크플로우의 통합을 통해 초기 판매 이후의 고객 유지를 강화하는 모델로 전환하고 있음을 보여줍니다. 또한, 이는 조달 부서가 단가 자체보다 수명 주기 소유 비용을 더 중요하게 여긴다는 것을 의미합니다. 실제로 사이버 나이프 시장의 서비스 부문 규모는 2031년까지 연평균 성장률(CAGR) 8.38%로 확대될 것으로 예상되며, 이는 판매 후 지속적인 수익이 공급업체의 수익 구조에서 핵심적인 위치를 차지하고 있음을 시사합니다.

지역별 분석

2025년 기준 북미는 45.22%의 점유율을 차지했으며, 이 지역은 사이버 나이프 시장에서 최대의 위상을 차지함과 동시에 가장 확고한 사업 환경을 갖추고 있었습니다. 미국은 대규모 도입 실적, 로봇 영상 유도 방사선 수술에 대한 CMS(연방의료보험서비스센터)의 확립된 보상 코드, 그리고 첨단 종양 치료 기기 조달에 있어 오랜 역사를 바탕으로 계속해서 핵심적인 위치를 유지하고 있습니다. 이처럼 성숙한 환경에서도 지역 의료에 대한 접근성은 여전히 확대되고 있으며, 2025년 10월 샌디에이고에 도입된 사이버 나이프 S7이 그 대표적인 예입니다. 이 시설은 캘리포니아주에서 단 두 곳뿐이며, 남부 캘리포니아에서는 유일하게 도입된 시설이라고 설명되어 있습니다. 멕시코는 여전히 소규모 시장이었지만, 2025년 12월 IMSS를 통해 공공 부문에 도입된 것은 정부 주도의 조달이 고소득 국가 이외의 시스템에서도 사이버 나이프 시장의 발전을 뒷받침할 수 있음을 보여준 점에서 이 지역에 있어 중요한 한 걸음이 되었습니다.

유럽에서는 국가별 및 시설 유형별로 시장이 더욱 집중되어 있으며, 학술 기관이 사이버 나이프 시장에서 주도적인 역할을 하고 있습니다. 독일은 여전히 이 지역에서 가장 확고한 거점이며, 베를린의 샤리테 대학병원은 사이버 나이프 치료를 시행하는 주요 대학병원으로서의 위상을 유지하고 있습니다. 오스트리아에서는 2025년 5월, CyberKnife Center Salzburg가 사이버 나이프 S7 시스템을 활용한 SRS 및 SBRT 환자 치료를 시작하면서 새로운 확장 거점이 추가되었습니다. 이 프로젝트는 오스트리아의 방사선 치료 장비 보급률이 EU 평균보다 27% 낮은 구조적인 공급 격차도 드러냈습니다. 이는 의료 인프라가 미흡한 상황에서 사이버 나이프 시장이 더욱 성장할 여지가 있음을 시사합니다. 이 지역 전체에서 EU 의료기기 규정을 준수하는 것은 공급업체와 시설 운영자 모두에게 계속해서 비용 증가와 엄격한 운영 체계를 요구하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.65%를 기록하며 성장할 것으로 전망되며, 사이버 나이프 시장에서 가장 빠르게 성장하고 있는 지역 블록으로 자리매김하고 있습니다. 2025년 1월 중국 국가의약품감독관리국(NMPA)이 사이버 나이프 S7 시스템에 대한 승인을 내림에 따라, 차세대 시스템을 도입할 수 있는 병원 기반이 대폭 확대되었으며, 이 플랫폼을 통해 세계 최대 규모의 암 의료 시스템 중 하나에 대한 접근성이 개선되었습니다. 인도에서는 라크나우와 우타르프라데시 주 서부 지역의 도입 사례가 보여주듯이, 도입이 최상위권 대도시권을 넘어 확산되고 있지만, 규제 당국의 승인이 여전히 가동 시작 일정을 좌우하고 있습니다. 호주 역시 2025년 10월 5D Clinics와 Icon Group의 합작 투자를 통해 멜버른에서 도입이 시작되었으며, 동부 해안 전역으로 확대될 계획인 만큼 주목할 만한 성장 시장이 되었습니다. 중동 및 아프리카에서는 타왐 병원(Tawam Hospital)이 아부다비에서 최초로 사이버 나이프 S7을 도입했으며, 케냐에서는 사하라 이남 아프리카에서 최초로 사이버 나이프가 가동을 시작했습니다. 한편, 남미는 여전히 도입 초기 단계에 있으며, 브라질과 콜롬비아에서는 이미 운영이 시작되었고, 멕시코도 2025년에 이 지역의 도입 거점에 합류하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the cyberKnife market size is projected to expand from USD 267.93 million in 2025 and USD 275.11 million in 2026 to USD 427.66 million by 2031, registering a CAGR of 7.63% between 2026 to 2031.

This report is Segmented by Product Type (CyberKnife System, Software Solutions, Services), Indication (Tumor and Cancer, Vascular Malformation, Other Indications), End User (Hospitals & Academic Medical Centers, Independent Radiotherapy Centers, Ambulatory/Outpatient Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Forecasts are Provided in Terms of Value (USD).

Global CyberKnife Market Trends and Insights

Rising Cancer Burden and Treatment Demand

The CyberKnife market is gaining support from the steady rise in cancer volume and case complexity across major care systems. The World Health Organization said annual global cancer cases are expected to exceed 35 million by 2050, which keeps long-term demand strong for precise radiation platforms that can absorb more patients without a matching increase in treatment infrastructure. This demand is especially relevant for brain metastases, vertebral metastases, and prostate cancer, where longer survival in primary oncology is increasing the number of patients who need focused local treatment. Australia's cancer diagnoses are projected to rise from 212,332 cases to 318,285 by 2045, which supports the business case for expanding access to high-precision treatment networks. Austria also remains under-supplied in radiotherapy equipment, with availability 27% below the EU average and 34% below economic peers, which creates room for new CyberKnife market installations in under-served regions. As these supply gaps persist, the CyberKnife market is likely to benefit most in locations where cancer demand is rising faster than radiotherapy capacity.

Preference for Non-Invasive and Organ-Sparing Treatment

The CyberKnife market is also benefiting from the broader preference for non-invasive care that avoids surgery when clinical outcomes are comparable. CyberKnife's Synchrony real-time motion-tracking capability helps clinicians treat thoracic, hepatic, and spinal targets with continuous adjustment for patient movement, which broadens its use beyond frame-based intracranial treatment. A 2025 long-term study of vestibular schwannoma patients reported 89.3% local control and 97.1% overall survival at 25 years after CyberKnife treatment, which reinforces confidence in durable organ-sparing management. A 2025 clinical study from Peking Union Medical College Hospital also found highly accurate dose delivery with minimal damage to surrounding tissue in pituitary adenoma and lung adenocarcinoma vertebral metastasis cases, which supports broader extracranial use. As a result, the CyberKnife market is gaining from a treatment preference that values precision, tissue preservation, and recovery outside the operating room.

High Capital Cost and Service Intensity

The CyberKnife market still faces a major barrier from the high upfront cost of system acquisition and the ongoing cost of support after installation. A typical system costs USD 5 million to USD 7 million before shielding construction and commissioning, which limits new projects to well-capitalized academic and tertiary providers. This burden becomes even more important after installation because service contracts, upgrades, and maintenance add recurring obligations over the asset life. Accuray reported that service revenue rose 3% year over year to USD 169.1 million in the first 9 months of fiscal 2026, while product revenue fell 21%, which shows how a slower capital cycle and a maturing installed base can weigh on fresh placements while raising service dependence. In Mexico, IMSS spent USD 8.7 million, to commission its first CyberKnife system in December 2025, which underlines how large these projects are even for public institutions. Because of this, the CyberKnife market remains concentrated in health systems that can absorb both capital and long-term service intensity.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Outpatient and Ambulatory Radiosurgery Delivery

- Faster Adoption of Hypofractionated Treatment Pathways

- Prior Authorization and Reimbursement Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The CyberKnife System segment held 48.31% of the CyberKnife market share in 2025, which kept hardware as the largest product category in the CyberKnife market. Services, however, are projected to grow at an 8.38% CAGR through 2031, making them the fastest-rising layer of the CyberKnife market by product type. This change matters because installed systems generate recurring revenue through preventive maintenance, remote diagnostics, training, and software upgrades even when new hardware orders slow. Accuray reported service revenue of USD 169.1 million in the first 9 months of fiscal 2026, up 3% year over year, while product revenue declined, which supports the view that the installed base is becoming more important to the CyberKnife market than single equipment sales.

Software is still the most dynamic layer inside the broader platform stack because it supports planning, adaptive delivery, and faster commissioning. Accuray received NMPA approval in China for the Accuray Precision Treatment Planning System in June 2024, and in September 2025 launched the Stellar solution, which brought adaptive radiotherapy capabilities together with CyberComm commissioning tools. That launch shows how the CyberKnife industry is moving toward a model where software, service, and workflow integration deepen customer retention after the initial sale. It also means procurement teams are placing more weight on lifetime ownership cost than on unit price alone. In practical terms, the CyberKnife market size for services is projected to expand at 8.38% CAGR through 2031, which signals that recurring post-sale revenue is becoming central to vendor economics.

Complete Report Scope:

- By Product Type

- CyberKnife System

- Software Solutions

- Services

- By Indication

- Tumor and Cancer

- Vascular Malformation

- Other Indications

- By End User

- Hospitals & Academic Medical Centers

- Independent Radiotherapy/Cancer Centers

- Ambulatory/Outpatient Radiosurgery Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 45.22% share in 2025, which gave the region the largest position in the CyberKnife market and the most established operating environment. The United States remained the anchor because of its large installed base, established CMS reimbursement codes for robotic image-guided radiosurgery, and long history of high-technology oncology procurement. Even in this mature setting, access is still expanding into community care, as shown by the October 2025 San Diego CyberKnife S7 launch, which was described as one of only 2 sites in California and the only one in Southern California. Mexico remained a smaller market, but its December 2025 public-sector installation through IMSS marked a meaningful regional step because it showed that government-backed procurement can support CyberKnife market development outside high-income systems.

Europe remains more concentrated by country and by site type, with academic centers playing a leading role in the CyberKnife market. Germany continued to be the region's most established base, and Charite Berlin remained a prominent university hospital site for CyberKnife treatment. Austria added a fresh point of expansion in May 2025 when the CyberKnife Center Salzburg started SRS and SBRT patient treatments using the CyberKnife S7 system. That project also highlighted a structural supply gap, since Austria's radiotherapy equipment availability remained 27% below the EU average, which supports room for further CyberKnife market growth in under-equipped systems. Across the region, compliance under EU medical device rules continues to add cost and operating discipline for both vendors and center operators.

Asia-Pacific is projected to grow at a 9.65% CAGR through 2031, which makes it the fastest-expanding regional block in the CyberKnife market. China's January 2025 NMPA approval of the CyberKnife S7 system opened a much larger hospital base to next-generation deployment and improved the platform's access to one of the world's largest cancer care systems. In India, installations in Lucknow and Western Uttar Pradesh show that adoption is moving beyond top-tier metro centers, although regulatory approvals still shape commissioning timelines. Australia also became a visible growth market after the October 2025 Melbourne launch through a joint venture between 5D Clinics and Icon Group, with plans to expand across the East Coast. In the Middle East and Africa, Tawam Hospital introduced the first CyberKnife S7 deployment in Abu Dhabi and Kenya commissioned the first CyberKnife in sub-Saharan Africa, while South America remained early stage with Brazil and Colombia already active and Mexico joining the regional installed base in 2025.

- Accuray

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cancer Burden and Treatment Demand

- 4.2.2 Preference for Non-Invasive and Organ-Sparing Treatment

- 4.2.3 Expansion of Outpatient and Ambulatory Radiosurgery Delivery

- 4.2.4 Faster Adoption of Hypofractionated Treatment Pathways

- 4.2.5 Reimbursement Optimization for Complex High-Cost Procedures

- 4.2.6 Movement-Tracking and Real-Time Imaging Differentiation

- 4.3 Market Restraints

- 4.3.1 High Capital Cost and Service Intensity

- 4.3.2 Prior Authorization and Reimbursement Friction

- 4.3.3 Site-of-Care Concentration in Specialized Centers

- 4.3.4 Installed Base Dependence and Slow Conversion Cycles

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 CyberKnife System

- 5.1.2 Software Solutions

- 5.1.3 Services

- 5.2 By Indication

- 5.2.1 Tumor and Cancer

- 5.2.2 Vascular Malformation

- 5.2.3 Other Indications

- 5.3 By End User

- 5.3.1 Hospitals & Academic Medical Centers

- 5.3.2 Independent Radiotherapy/Cancer Centers

- 5.3.3 Ambulatory/Outpatient Radiosurgery Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products, Recent Developments)

- 6.2.1 Accuray Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment