|

시장보고서

상품코드

2072863

미국의 리스티고 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Rystiggo Drug - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

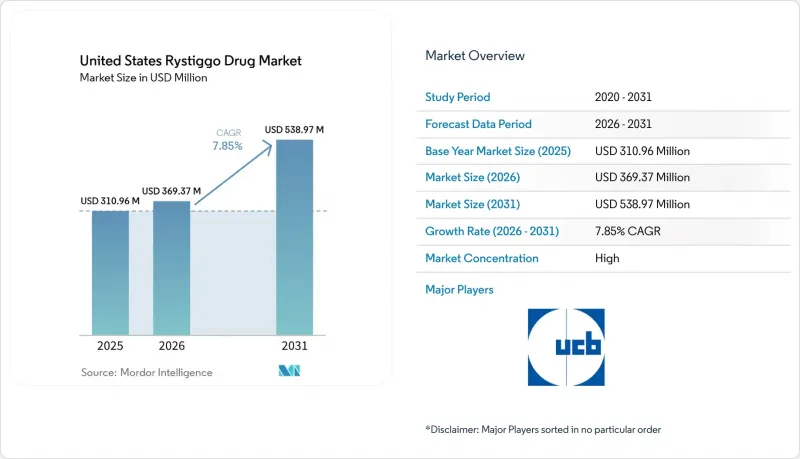

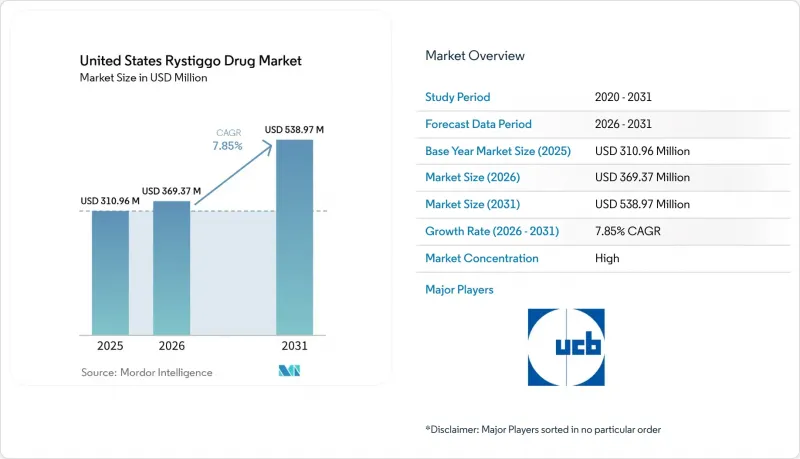

Mordor Intelligence에 의하면, 미국 리스티고 의약품 시장 규모는 2025년 3억 1,096만 달러에서 2026년에는 3억 6,937만 달러로 확대되어 2031년까지 5억 3,897만 달러에 이를 것으로 예상되고 있어 2026-2031년까지 CAGR 7.85%로 성장할 전망입니다.

본 보고서는 항체 유형(AChR 양성, MUSK 양성), 용량(280 mg/2 mL, 420 mg/3 mL, 560 mg/4 mL, 840 mg/6 mL), 유통 채널(전문 약국, 병원 약국, 기타), 최종 사용자(병원, 전문 신경과 클리닉, 재택 간호 시설)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 리스티고 의약품 시장 동향 및 분석

전문 신경과 분야에서 FcRn을 표적으로 하는 생물학적 제제의 급속한 보급

FcRn 억제제 계열은 미국 리스티고 의약품 시장에서 치료의 초점이 광범위한 면역 억제로부터 병인성 자가항체를 표적으로 한 감소로 전환됨에 따라, 신경과 전문의들의 전신성 중증근무력증 치료 접근 방식을 완전히 바꿔 놓았습니다. 로자놀리키즈마브는 FcRn의 재순환을 억제하고, 병원성 AChR 및 MUSK 자가항체를 포함한 순환 IgG 수치를 낮춤으로써 작용합니다. 이러한 작용기전은 아세틸콜린에스테라제 억제제나 비특이적 스테로이드와는 다릅니다. 8건의 무작위 대조 시험 및 873명의 환자를 대상으로 한, 이미 발표된 체계적 문헌고찰 및 메타분석의 증거에 따르면, FcRn 억제제는 위약에 비해 MG-ADL, QMG, MGC 점수를 개선하는 것으로 나타났으며, 이는 신경과 의사들 사이에서 이 약물 군에 대한 신뢰가 높아지고 있음을 뒷받침하는 근거가 되었습니다. 이 수업에 대한 사전 이해가 중요했던 이유는 이미 임상 현장에서 FcRn 요법을 사용하고 있던 의사일수록, 미국의 리스티고 의약품 시장에서 정맥 내 투여를 통한 대체 요법으로는 불완전한 반응만 보였던 환자들에게 리스티고를 적용할 준비가 되어 있었기 때문입니다. 또한 UCB는 2025년에 MG0004 및 MG0007의 공개 연장 임상시험에서 얻은 장기 데이터를 발표했습니다. 이를 통해 증상에 따른 반복 투여 주기에서의 내약성 및 재치료의 유효성이 입증되었습니다. 이러한 데이터는 보험사의 보험 적용 갱신과 의사의 신뢰를 뒷받침했을 뿐만 아니라, 미국의 리스티고 의약품 시장이 일회성 구제 요법 패턴에서 만성 관리 모델로 전환하는 데 일조했습니다.

AChR 및 MUSK에 대한 광범위한 적응증으로 인해 치료 대상 환자층이 확대됨

리스티고가 AChR 양성 및 MUSK 양성 질환 모두에 대해 승인된 사실은 AChR 양성 적응증으로만 제한된 약물보다 더 광범위한 환자층에 접근할 수 있기 때문에 상업적으로 여전히 중요합니다. MUSK 양성 환자는 전체 중증근무력증 사례 중 극히 일부에 불과하지만, 난치성 및 치료 저항성 질환에서 더 큰 비율을 차지하고 있으며, 이 때문에 이 적응증의 폭이 넓다는 점은 표면적인 유병률 수치가 시사하는 것 이상으로 중요한 의미를 지녔습니다. 미국 내 유병률 추정치는 진단받은 환자 수만으로도 약 11만 6,000명에서 더 광범위한 적응증을 고려할 경우 13만 5,000명에 이르기까지 폭이 넓으며, 이로 인해 미국 리스티고 의약품 시장에서 표적 치료의 대상이 되는 명확한 환자층이 형성되었습니다. 해당 그룹 내에서 MUSK 양성 사례는 전체 사례의 6%-8%를 차지했으며, AChR 혈청 음성 환자의 40% 가까이를 차지하고 있었으며, 이로 인해 리스티고는 기존에는 적응증 외 사용에 의존하던 틈새 영역에서도 여전히 중요한 위치를 차지하고 있었습니다. 2025년 4월 IMAAVY의 승인으로, Johnson & Johnson이 정맥 내 투여형 FcRn 억제제를 통해 동일한 AChR 양성 및 MUSK 양성 분야에 진출함에 따라, 리스티고의 적응증에 대한 우위성은 축소되었습니다. 그럼에도 불구하고, 리스티고는 피하 투여라는 투여 경로와 확립된 접근 체계를 통해 실용적인 측면에서 편의성의 우위를 유지했습니다. 이로 인해 지불 주체 입장에서 치료 현장의 경제성이 더욱 중요해지는 가운데, 미국의 리스티고 의약품 시장은 견고한 입지를 유지했습니다.

높은 연간 치료비와 사전 승인 관련 과제

리스티고의 미국 정가는 1mL당 3,155.37달러이며, 중증도가 높은 환자의 경우 6주 치료 주기 1회분에 해당하는 바이알 단위의 비용은 7만 5,000달러에서 9만 달러에 달할 가능성이 있습니다. 이러한 비용으로 인해, 이 치료법은 1회 치료당 비용이 가장 비싼 신경학 분야의 특수 생물학적 제제 중 하나로 꼽히며, 당연히 미국의 리스티고 의약품 시장에서 지불 주체의 심사가 더욱 엄격해지고 있습니다. 주요 민간 보험사들은 사전 승인을 의무화했으며, 승인 시 MGFA 클래스 II-IVa에 해당하는 질환임이 확인되어야 하고, 기존의 면역억제요법 이력이 있어야 한다는 조건을 자주 요구했습니다. 초기 승인 기간은 보통 6개월이며, 갱신 시에는 추가적인 치료 반응에 관한 서류가 필요했기 때문에 치료 이용은 일회성 심사가 아니라 반복되는 행정 절차로 변해버렸습니다. 이것은 중요한 문제입니다. 리스티고는 증상에 기반한 치료 주기를 채택하고 있기 때문에 치료에 반응하고 있는 환자라 하더라도 갱신 시마다 지급 기관이 요구하는 서류 요건을 일관되게 충족하지 못할 경우 치료 시작이 지연될 가능성이 있기 때문입니다. UCB의 지원 체계는 이러한 부담의 일부를 덜어주고 있지만, 비용과 승인 절차의 장벽은 여전히 미국 리스티고 의약품 시장의 단기 성장 속도에 있어 가장 뚜렷한 제약 요인 중 하나로 남아 있습니다.

부문별 분석

2025년, AChR 양성 환자는 미국 내 리스티고 시장 점유율 68.31%를 차지했으며, FDA.GOV의 항체 유형 분류에 따라 계속해서 핵심 치료 대상 집단으로서의 지위를 유지했습니다. 이러한 우위는 성인 전신성 중증근무력증 사례의 대부분에서 AChR 항체가 존재한다는 단순한 사실을 반영한 것이며, 신경과 전문의들은 당연히 먼저 그보다 광범위한 진단 대상 집단에 초점을 맞췄습니다. 실제로, 의사가 피리도스티그민, 코르티코스테로이드 또는 비스테로이드성 면역억제제를 넘어 FcRn 치료로 전환할 때, 이러한 환자들이 주요 처방 대상이 되었습니다. 주요 임상시험인 MycarinG 시험에서는 조사 대상이었던 모든 항체군에서 43일째까지 MG-ADL 점수 및 QMG 점수에서 임상적으로 유의미한 개선이 확인되어, 이러한 사용 패턴을 뒷받침하는 결과가 되었습니다. 이러한 폭넓은 효능이 바로 미국 리스티고 의약품 시장의 항체 부문 구조를 지탱하는 기반이 되었습니다. 왜냐하면, 이 결과를 통해 처방 의사는 본 제제가 여러 가지 면역학적 프로파일에 대응할 수 있다는 확신을 얻었기 때문입니다.

MUSK 양성 환자 수는 2031년까지 연평균 성장률(CAGR) 9.38%로 증가할 것으로 예상되며, 미국 리스티고 의약품 시장 규모 전망에서 가장 빠르게 성장하는 항체 하위 부문이 될 것으로 보입니다. MUSK 항체는 중증근무력증 전체 환자의 약 6%와 AChR 혈청 음성 환자의 약 40%에서 확인되었으며, 이 하위 집단에 있어 진단법의 개선이 특히 중요했습니다. 이 환자들은 종종 더 심각한 안구 및 안면 증상을 보였으며, 콜린에스테라제 억제제에 대한 반응도 미미했기 때문에 표적 치료가 가능한 승인된 치료법에 대한 임상적 수요는 여전히 높았습니다. 2025년 이전에는 승인된 대체 약물이 없었기 때문에 리스티고는 이 틈새 시장에서 매우 유리한 입지를 차지하고 있었습니다. 그리고 그 초기의 발판은 IMAAVY가 등장한 후에도 여전히 중요한 의미를 지니고 있습니다. 따라서, 이러한 성장 전망은 진정한 미충족 의료 수요의 존재와 항체 아형 검사에 대한 의사들의 관심 증가를 모두 반영하고 있으며, 이에 따라 MUSK에 대한 치료량은 미국 리스티고 의약품 시장 전체보다 더 빠른 속도로 계속 확대될 것으로 예측됩니다.

2025년 기준으로, 560 mg/4 mL 바이알은 용량 강도 부문의 39.24%를 차지하며, 미국 리스티고 의약품 시장에서 가장 많이 사용되는 제형이 되었습니다. 이 수치는 체중에 따른 투여량 체계와 일치합니다. 왜냐하면 체중이 70-80 kg 범위인 환자에게 약 7 mg/kg을 투여할 경우, 대부분의 경우 이 구성에 자연스럽게 부합하기 때문입니다. 리스티고는 280 mg/2 mL, 420 mg/3 mL, 560 mg/4 mL 및 840 mg/6 mL 용량의 단회 투여용 바이알로 공급되며, 이러한 제품 라인업을 통해 약국은 체중에 따라 투여량을 보다 정확하게 조절할 수 있습니다. 280 mg/2 mL 및 420 mg/3 mL 제형은 체중이 가벼운 환자나 여러 약물을 혼합하여 조제해야 하는 경우에 여전히 사용되고 있지만, 일상적인 조제량의 주류를 이루고 있는 것으로 보이지는 않습니다. 따라서 560 mg/4 mL 바이알이 가장 큰 시장 점유율을 차지하고 있다는 사실은 미국 리스티고 의약품 시장에서 단순히 포장 형태에 대한 선호도라기보다는 치료를 받는 환자들의 전형적인 특성을 반영한다고 볼 수 있습니다.

840 mg/6 mL 바이알은 2031년까지 연평균 성장률(CAGR) 9.52%를 나타낼 것으로 예측되며, 이는 가장 빠르게 확대되고 있는 용량 규격입니다. 이러한 경향은 체중이 많은 환자나 반복되는 치료 주기를 통해 10 mg/kg의 용량 수준을 유지하고 있는 환자들 사이에서 이 약물이 더 광범위하게 사용되고 있음을 시사합니다. UCB사가 2025년에 강조한 MG0007 및 MG0004의 공개 연장 임상시험 결과는 더 지속적인 질환 부담을 안고 있는 환자들에서 증상에 기반한 여러 치료 주기에 걸친 지속적인 사용을 뒷받침하고 있습니다. 또한, 840 mg/6 mL 제형에는 사용상의 장점도 있습니다. 단일 단위로 조제함으로써, 체중이 많이 나가는 환자를 다루는 전문 약국이나 병원 약국에서 조제의 복잡성을 줄일 수 있기 때문입니다. 이러한 변화로 인해 560 mg/4 mL 바이알이 현재 차지하고 있는 주도적인 지위가 바뀌는 것은 아니지만, 미국 리스티고 의약품 시장에서 더 높은 용량의 단일 바이알 제형이 선호되는 방향으로 치료를 받는 환자층의 구성이 확대되고 있음을 보여줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states rystiggo drug market size is expected to increase from USD 310.96 million in 2025 to USD 369.37 million in 2026 and reach USD 538.97 million by 2031, growing at a CAGR of 7.85% over 2026-2031.

This report is Segmented by Antibody Type (AChR-Positive, MUSK-Positive), Dosage Strength (280 Mg/2 ML, 420 Mg/3 ML, 560 Mg/4 ML, 840 Mg/6 ML), Distribution Channel (Specialty Pharmacies, Hospital Pharmacies, Other Distribution Channels), End User (Hospitals, Specialty Neurology Clinics, Home Care Settings). The Market Forecasts are Provided in Terms of Value (USD).

United States Rystiggo Drug Market Trends and Insights

Rapid Uptake of FcRn-Targeted Biologics in Specialty Neurology

The FcRn inhibitor class changed how neurologists approached generalized myasthenia gravis, because treatment focus moved away from broad immunosuppression toward targeted reduction of pathogenic autoantibodies in the United States Rystiggo drug market. Rozanolixizumab works by blocking FcRn recycling and lowering circulating IgG, including pathogenic AChR and MUSK autoantibodies, which separates it mechanistically from acetylcholinesterase inhibitors and non-specific steroids. Published systematic review and meta-analysis evidence across 8 randomized controlled trials and 873 patients showed that FcRn inhibitors improved MG-ADL, QMG, and MGC scores versus placebo, which supported growing class confidence among neurologists. That prior class familiarity mattered because physicians who had already used FcRn therapy in practice were more prepared to adopt Rystiggo for patients with incomplete response to intravenous alternatives in the United States Rystiggo drug market. UCB also presented long-term evidence from the MG0004 and MG0007 open-label extension studies in 2025, which reinforced tolerability and retreatment efficacy across repeated symptom-driven cycles. Those data supported payer renewals and physician confidence, and they helped the United States Rystiggo drug market move closer to a chronic management model instead of a one-time rescue pattern.

Broad AChR and MUSK Label Expands Treatable Population

Rystiggo's dual approval for both AChR-positive and MUSK-positive disease remains commercially important because it reaches a broader treated pool than agents limited to AChR-positive labeling. MUSK-positive patients accounted for only a small portion of all myasthenia gravis cases, but they represented a larger share of refractory and treatment-resistant disease, which made this label breadth more meaningful than headline prevalence numbers suggested. U.S. prevalence estimates ranged from nearly 116,000 diagnosed patients to 135,000 when broader claims coverage was considered, and that created a defined addressable pool for targeted therapy in the United States Rystiggo drug market. Within that group, MUSK-positive disease represented 6% to 8% of cases and nearly 40% of AChR-seronegative patients, which kept Rystiggo relevant for a niche that historically relied on off-label management. The April 2025 approval of IMAAVY narrowed Rystiggo's label advantage because Johnson & Johnson entered the same AChR-positive and MUSK-positive space with an intravenous FcRn blocker. Even so, Rystiggo preserved a practical convenience edge through its subcutaneous route and established access setup, which kept the United States Rystiggo drug market well positioned as site-of-care economics became more important to payers.

High Annual Therapy Cost and Prior Authorization Friction

Rystiggo's U.S. list price was USD 3,155.37 per mL, and a single 6-week treatment cycle for heavier patients could reach USD 75,000 to USD 90,000 at the vial level. That cost places the therapy among the highest-priced specialty neurology biologics per episode of care, which naturally tightens payer scrutiny in the United States Rystiggo drug market. Major commercial payers required prior authorization and often asked for confirmed MGFA Class II to IVa disease plus prior exposure to conventional immunosuppressive therapy before approval. Initial approvals commonly ran for 6 months and renewals then required additional response documentation, which turned access into a repeated administrative process rather than a one-time review. That matters because Rystiggo uses symptom-driven treatment cycles, and even responding patients can face delays if payer documentation thresholds are not met consistently across renewals. UCB's support structure eases part of that burden, but the cost and authorization barrier remains one of the clearest limits on the near-term growth pace of the United States Rystiggo drug market.

Other drivers and restraints analyzed in the detailed report include:

- Self-Administered or Clinic-Light Dosing Supports Adherence and Site-of-Care Shift

- Orphan Neurology Reimbursement Pathways Support Early Access

- Safety Monitoring Burden, Infection Risk, and Vaccine Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AChR-positive patients held 68.31% of the United States Rystiggo drug market share in 2025, which kept them as the core treated population inside the antibody-type split FDA.GOV. This lead reflected the simple fact that AChR antibodies are present in the majority of adult generalized myasthenia gravis cases, so neurologists naturally focused first on that broader diagnosed base. In practice, these patients formed the main prescribing target when physicians moved beyond pyridostigmine, corticosteroids, or non-steroidal immunosuppressants and stepped into FcRn therapy. The pivotal MycarinG study supported that use pattern because it showed clinically meaningful improvement in MG-ADL and QMG scores by Day 43 across the antibody groups studied. That broad efficacy base anchored the antibody segment structure of the United States Rystiggo drug market, because it gave prescribers confidence that the drug could serve more than one immunologic profile.

MUSK-positive patients are projected to grow at a 9.38% CAGR through 2031, making them the fastest-growing antibody sub-segment in the United States Rystiggo drug market size outlook. MUSK antibodies were found in nearly 6% of all myasthenia gravis cases and in nearly 40% of AChR-seronegative patients, which made diagnostic improvement especially important for this subpopulation. These patients often showed more severe bulbar and facial involvement and had weaker response to cholinesterase inhibitors, so clinical demand for a targeted approved option remained high. Before 2025, the lack of approved alternatives gave Rystiggo a very favorable position in this niche, and that early foothold still matters even after the arrival of IMAAVY. The growth outlook therefore reflects both a real unmet-need base and rising physician attention to antibody subtype testing, which should keep MUSK treatment volumes expanding faster than the broader United States Rystiggo drug market.

The 560 mg/4 mL vial held 39.24% of the dosage-strength segment in 2025, which made it the leading presentation in the United States Rystiggo drug market. That position fits the weight-tiered dosing structure, because patients treated at nearly 7 mg/kg in the 70 kg to 80 kg range often align naturally with this configuration. Rystiggo is supplied in 280 mg/2 mL, 420 mg/3 mL, 560 mg/4 mL, and 840 mg/6 mL single-dose vials, and that portfolio lets pharmacies match dosing more closely to body weight. The 280 mg/2 mL and 420 mg/3 mL formats continue to serve lighter patients and combination-fill needs, but they do not appear to sit at the center of routine dispensing volume. The leading share of the 560 mg/4 mL vial therefore reflects the modal treated patient profile rather than a simple packaging preference inside the United States Rystiggo drug market.

The 840 mg/6 mL vial is forecast to grow at a 9.52% CAGR through 2031, which makes it the fastest-expanding strength format. This pattern points to broader use among heavier patients and among patients maintained on the 10 mg/kg tier across repeated treatment cycles. Open-label extension work from MG0007 and MG0004, which UCB highlighted in 2025, supported continued use across multiple symptom-driven cycles in patients with more persistent disease burden. The 840 mg/6 mL presentation also offers operational advantages because a single-unit fill can reduce dispensing complexity for specialty pharmacies and hospital pharmacies handling higher-weight patients. That shift does not change the current leadership of the 560 mg/4 mL vial, but it shows that treated-patient mix in the United States Rystiggo drug market is broadening in a way that favors stronger single-vial presentations.

Complete Report Scope:

- By Antibody Type

- AChR-Positive

- MUSK-Positive

- By Dosage Strength

- 280 mg / 2 mL

- 420 mg / 3 mL

- 560 mg / 4 mL

- 840 mg / 6 mL

- By Distribution Channel

- Specialty Pharmacies

- Hospital Pharmacies

- Other Distribution Channels

- By End User

- Hospitals

- Specialty Neurology Clinics

- Home Care Settings

List of Companies Covered in this Report:

- UCB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Uptake Of FcRn-Targeted Biologics In Specialty Neurology

- 4.2.2 Broad AChR and MuSK Label Expands Treatable Population

- 4.2.3 Self-Administered Or Clinic-Light Dosing Supports Adherence and Site-of-Care Shift

- 4.2.4 Orphan Neurology Reimbursement Pathways Support Early Access

- 4.2.5 Real-World Evidence Generation Strengthens Formulary Conversion

- 4.3 Market Restraints

- 4.3.1 High Annual Therapy Cost and Prior Authorization Friction

- 4.3.2 Safety Monitoring Burden, Infection Risk, and Vaccine Restrictions

- 4.3.3 Class Competition From Vyvgart, IMAAVY, Soliris, Ultomiris, and Zilbrysq

- 4.3.4 Limited Eligible Pool and Diagnostic Uncertainty Outside Specialty Centers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Antibody Type

- 5.1.1 AChR-Positive

- 5.1.2 MuSK-Positive

- 5.2 By Dosage Strength

- 5.2.1 280 mg / 2 mL

- 5.2.2 420 mg / 3 mL

- 5.2.3 560 mg / 4 mL

- 5.2.4 840 mg / 6 mL

- 5.3 By Distribution Channel

- 5.3.1 Specialty Pharmacies

- 5.3.2 Hospital Pharmacies

- 5.3.3 Other Distribution Channels

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Neurology Clinics

- 5.4.3 Home Care Settings

6 Competitive Landscape

- 6.1 Pipeline Analysis

- 6.2 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products, Recent Developments)

- 6.2.1 UCB S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment