|

시장보고서

상품코드

2072878

미세조류 기반 수산 사료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Microalgae-Based Aquafeed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

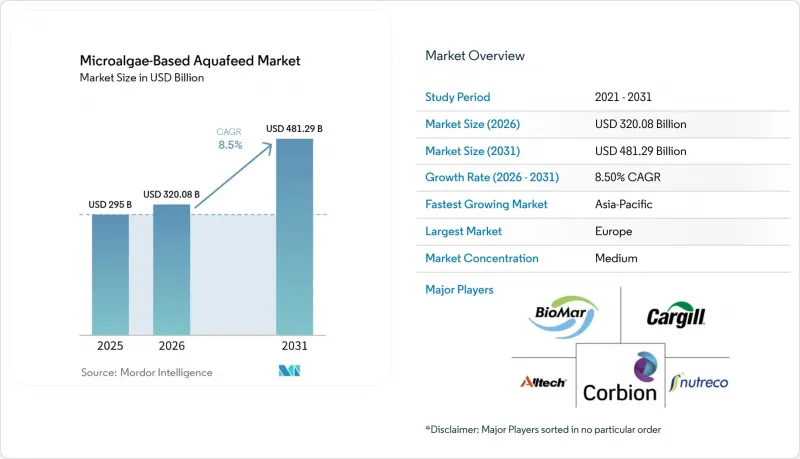

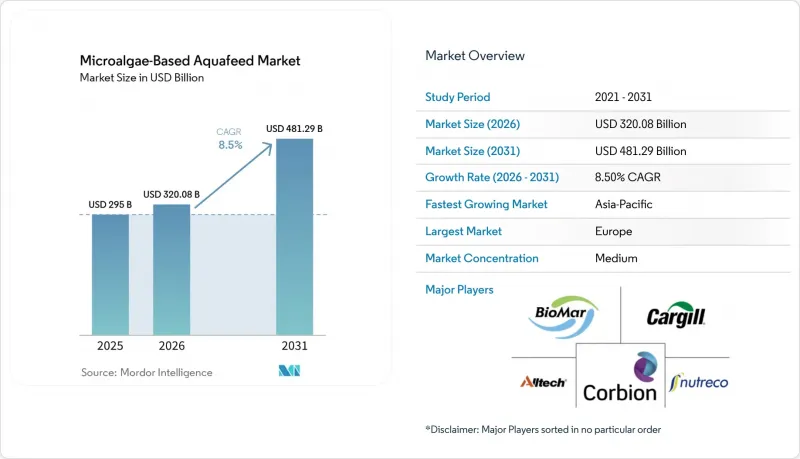

Mordor Intelligence에 의하면, 미세조류 기반 수산 사료 시장 규모는 2025년 2억 9,500만 달러, 2026년 3억 2,008만 달러에서 2031년까지 4억 8,129만 달러로 확대되어 2026-2031년까지 CAGR 8.5%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(모든 미세조류, 조류 밀 또는 분말, DHA가 풍부한 조류유, 조류 단백질 분리물, 기타), 종별(스피루리나, 클로렐라, 난노클로로프시스, 스키조티트리움, 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 미세조류 기반 수산 사료 시장 동향과 인사이트

밀폐형 광생물반응기를 이용한 양식 비용의 급격한 감소

밀폐형 광생물반응기를 통해 건조 바이오매스 1kg당 운영 비용이 3달러 미만으로 절감되었으며, 이로 인해 어분과의 역사적인 가격 차이가 해소되어 고급 연어 및 새우 사료에 조류를 더욱 광범위하게 활용하는 것이 촉진되고 있습니다. Algiecel은 2024년에 5,000만 덴마크 크로네(670만 달러)를 조달하여 산업 배출원에 모듈식 장치를 도입했습니다. 이를 통해 발생원에서 배출되는 이산화탄소를 포집하는 이동식 시스템의 확장성이 입증되었습니다. 라이프사이클 분석에 따르면, 스피루리나의 생산 비용은 본격 생산 단계에 접어들면 1kg당 1.30달러까지 낮아질 가능성이 있으며, 현물 가격이 톤당 1,700달러를 상회하는 한, 이 조류의 가격은 어분과 거의 비슷한 수준이 될 것으로 전망됩니다. 또한, 밀폐 시스템의 설계 덕분에 미코톡신 및 중금속으로 인한 오염이 배제되며, 이는 미세조류 기반 수산 사료 시장에서 프리미엄 배합 사료의 중요한 요건이 되고 있습니다. 미국 식품의약국(FDA) 및 유럽식품안전청(EFSA)과 같은 규제 당국은 추적성 측면에서 광생물반응기에서 배양된 균주를 선호하며, 이로 인해 개방형 양식장에서 생산된 대체품에 비해 승인까지 걸리는 기간이 단축됩니다.

항생제를 사용하지 않은 수산물에 대한 프리미엄 가격 책정 기회

유럽과 북미의 소매업체들은 항생제를 사용하지 않은 연어와 새우에 대해 두 자릿수의 프리미엄 가격을 지불하고 있으며, 이로 인해 양식업자들에게는 면역력을 높이는 조류 기반 원료를 채택할 직접적인 경제적 유인이 생기고 있습니다. 1억 4,300만 마리의 칠레산 연어를 대상으로 한 ‘Veramaris Big Data Chile 2026’ 조사에 따르면, 에이코사펜타엔산(EPA)과 도코사헥사엔산(DHA)을 합쳐 7.2% 이상 함유한 사료를 급여한 결과, 사료 전환율이 개선되고 품질 등급 하락이 최대 100% 감소한 것으로 나타나, 조류를 배합하는 것의 비용 대비 효과에 대한 근거가 입증되었습니다. Microchloropsis gaditana를 이용한 시험에서 필레의 오메가-3 함량이 23% 증가했고, 세균 감염이 85.68% 감소함에 따라 항생제 사용량이 현저히 줄었습니다. 새우에서도 유사한 효과가 확인되었으며, 스피루리나를 10% 첨가함으로써 최종 체중이 10.82그램으로 증가했고, 비브리오균에 의한 사망률이 절반으로 감소했습니다. 이를 통해 미세조류 기반 수산 사료 시장 솔루션이 건강과 경제 양면에서 이점을 가져다준다는 사실이 입증되었습니다. 소비자의 인식이 지속적으로 높아지는 가운데, ‘항생제 미사용’ 표기는 차별화 요소에서 프리미엄 시장의 필수 조건으로 전환되고 있으며, 고부가가치 수산 양식 분야에서 조류의 역할이 확고해지고 있습니다.

신규 조류 균주의 규제 승인 지연

미국 식품의약국(FDA)의 ‘일반적으로 안전하다고 인정되는(GRAS)’ 인증 절차나 유럽연합(EU)의 신규 식품 규제로 인해, 신주 품종의 상용화까지 2-3년의 기간과 막대한 서류 작성 비용이 추가로 발생할 가능성이 있습니다. 이러한 지연 현상은 우수한 지질 프로파일을 지닌 CRISPR 편집을 통해 생산된 고EPA 조류에서 특히 심각합니다. 이러한 조류들은 특히 유전자 편집에 대한 대중의 회의적인 시각이 뿌리 깊은 유럽이나 일본에서 더욱 엄격한 심사를 받고 있습니다. KnipBio 등 기업들은 2025년에 박테리아 바이오매스에 대해 미국 및 캐나다에서 승인을 획득했으나, 유럽에서의 승인은 아직 기다리고 있는 상황이며, 이로 인해 미세조류 기반 수산 사료 시장 전체의 생산 확대가 제한되고 있습니다. 규제의 분절로 인해 생산자들은 별도의 생산 라인을 유지할 수밖에 없어, 비용 중복이 발생하고 세계 시장 진출이 지연되고 있습니다. 코덱스 알리멘타리우스(국제식품규격)에 따른 조화가 이루어지지 않고 있기 때문에 승인 지연은 중기적으로 구조적인 제약으로 남게 될 것입니다.

부문별 분석

2025년, 미세조류 기반 수산 사료 시장에서 조류유가 38.0%라는 가장 큰 점유율을 차지했습니다. 이는 연어 생산자들이 프리미엄급 필레 가격을 확보하기 위해 조류유에 함유된 도코사헥사엔산(DHA)의 안정적인 함량에 의존하고 있기 때문입니다. 반면, 단백질 분리물은 가장 빠르게 성장하는 부문으로, 태국, 에콰도르, 인도의 새우 부화장들이 치새우의 생존율을 높이는 고단백 농축 사료에 어분을 대체하고 있는 만큼, 2026년부터 2031년까지 연평균 성장률(CAGR) 13.5%로 성장할 것으로 전망됩니다. 미국 식품의약국(FDA)의 ‘일반적으로 안전하다고 인정되는(GRAS)’ 규정이나 유럽연합(EU)의 신규 식품 심사 과정에서 안전성 검증을 효율화할 수 있는 표준화된 성분이 선호됨에 따라, 미세조류 기반 수산 사료 시장의 분리 단백질 부문 규모는 더욱 확대되고 있습니다. 밀폐형 광생물 반응기의 비용 절감과 탄소 크레딧 수익화가 가능해짐에 따라 어분과의 가격 차이가 줄어들고 있으며, 이로 인해 가장 빠르게 성장하는 이 부문의 도입이 촉진되고 있습니다.

모든 미세조류 및 조류 분말은 세포벽으로 인해 소화율이 낮아지는 단점이 있음에도 불구하고, 5-15%의 배합 비율로 틸라피아와 관상어에게 색소 형성 및 면역 강화의 이점을 제공하는 틈새 시장을 차지하고 있습니다. 조류유는 다년간공급 계약을 통해 고급 연어 및 해양성 어류의 사료 시장에서 안정적인 수요가 확보되어 있는 만큼, 2031년까지 견실한 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다. 2026년에 Fermentalg가 출시한 Omega Origins와 같은 다기능 오일에는 에이코사펜타엔산(EPA)이 40%, 도코사헥사엔산(DHA)이 20% 함유되어 있습니다. 이러한 오일은 후속 공정의 단계를 줄여 완성 사료의 원가를 절감합니다. 모듈식 시스템 내에서 여러 균주를 공동 배양할 수 있는 생산자는 나머지 부문의 다양한 영양 목표를 충족하는 혼합 원료를 공급할 수 있는 유연성을 확보할 수 있습니다.

지역별 분석

2025년, 시장에서 유럽이 35.5%라는 가장 큰 점유율을 차지했습니다. 이는 노르웨이와 덴마크의 연어 양식업자들이 해양관리협의회(MSC)의 추적성 기준 및 항생제 미사용 기준을 충족하기 위해 조류 기반 오일을 도입했기 때문입니다. 아시아태평양은 가장 빠르게 성장하는 지역으로, 인도의 조류유에 대한 무관세 정책과 중국의 대체 단백질에 대한 우대 조치를 배경으로 2026년부터 2031년까지 연평균 성장률(CAGR) 10.7%로 확대될 것으로 전망됩니다. 유럽에서는 수산 양식 폐수를 정화하는 미세조류 바이오리파이너리에 대한 공공 자금 지원이 계속되고 있는 반면, 아시아태평양에서는 수입 관세 인하를 활용해 어분과의 비용 격차를 좁히고 있습니다. 이처럼 대조적이면서도 서로 보완하는 정책 요인들이, 가장 규모가 크고 성장 속도가 가장 빠른 지역 시장에서 서로 다른 성장 경로를 뒷받침하고 있습니다.

북미에서는 미국 식품의약국(FDA)의 승인을 통해 새로운 균주를 도입할 수 있게 되었으며, 또한 연어 생산자들이 스코프 3 배출량을 줄이기 위해 사료에 조류를 첨가하고 있어 꾸준한 성장을 이루고 있습니다. 남미에서는 조류 기반 오일에 포함된 장쇄 오메가-3 지방산의 총 함량이 7.2%를 초과하면 사료 전환율이 향상되고 품질 등급 하락이 줄어든다는 칠레의 데이터가 긍정적인 요인으로 작용하고 있습니다. 중동에서는 해수 적응형 스피루리나 및 클로렐라 생산 시설을 확대하고 있으며, 이는 탄소 포집과 내륙 양식 확대를 연계하고 있습니다. 아프리카는 여전히 초기 단계에 있으며, 이집트와 남아프리카공화국에서 진행 중인 시범 프로젝트는 본격적인 상용화를 위해 추가적인 비용 절감을 기다리고 있는 상황입니다.

지역별 투자 동향은 생산 능력 확대가 가속화되고 있음을 보여주고 있습니다. 스코틀랜드와 프랑스에 위치한 유럽의 광생물반응기 거점은 2027년까지 생산 능력을 수 배로 확대하는 것을 목표로 하고 있으며, 한편 일본과 한국에서는 본격적인 상용화에 앞서 시범 프로젝트를 통해 기술의 유효성이 검증되고 있습니다. 노르웨이와 캘리포니아에서 도입된 새로운 탄소 크레딧 제도는 생산 비용의 최대 15%를 상쇄해 주어, 미세조류의 경쟁력을 높이고 대륙을 넘어선 관심을 불러일으키고 있습니다. 어분 가격 변동이 지속되고 지속가능성에 관한 기준이 강화되는 가운데, 주요 수산 양식 지역 모두에서 조류의 이용이 확대될 것으로 예상되며, 그 결과 전 세계 미세조류 기반 수산 사료 시장이 전반적으로 성장할 전망입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the microalgae-based aquafeed market size is anticipated to expand from USD 295 million in 2025 and USD 320.08 million in 2026 to USD 481.29 million by 2031, registering a 8.5% CAGR between 2026 to 2031.

This report is Segmented by Product Type (Whole Microalgae, Algae Meal or Flour, Algal Oil DHA-Rich, Algae Protein Isolate, and Others), by Species (Spirulina, Chlorella, Nannochloropsis, Schizochytrium, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Microalgae-Based Aquafeed Market Trends and Insights

Rapid Cost Decline in Closed-Photobioreactor Farming

Closed photobioreactors are cutting operating expenses below USD 3 per kilogram of dry biomass, closing the historical gap with fishmeal and spurring wider use of algae in premium salmon and shrimp feeds. Algiecel secured DKK 50 million (USD 6.7 million) in 2024 to deploy modular units at industrial emission points, demonstrating the scalability of mobile systems that capture waste carbon dioxide at source. Lifecycle analyses indicate Spirulina production costs could fall to USD 1.30 per kilogram at full scale, positioning algae near price parity with fishmeal as long as spot prices stay above USD 1,700 per metric ton. The closed-system design also eliminates contamination from mycotoxins and heavy metals, a key requirement for premium formulations in the microalgae-based aquafeed market. Regulators such as the United States Food and Drug Administration and the European Food Safety Authority favor photobioreactor-grown strains for their traceability, shortening approval times versus open-pond alternatives.

Premium Pricing Opportunity for Antibiotic-Free Seafood

Retailers in Europe and North America pay double-digit premiums for antibiotic-free salmon and shrimp, giving farmers a direct economic incentive to adopt immune-boosting algal ingredients. The Veramaris Big Data Chile study 2026 study covering 143 million Chilean salmon showed diets containing at least 7.2% combined eicosapentaenoic acid and docosahexaenoic acid improved feed conversion ratios and cut quality downgrades by up to 100%, reinforcing the cost-benefit case for algae inclusion. Trials with Microchloropsis gaditana increased fillet omega-3 content by 23% and reduced bacterial infections by 85.68%, demonstrably lowering antibiotic use. Similar effects were observed in shrimp, where Spirulina at 10% inclusion increased final weight to 10.82 grams and halved Vibrio mortality, demonstrating that microalgae-based aquafeed market solutions can drive both health and financial gains. As consumer awareness continues to rise, antibiotic-free labeling is moving from a differentiator to a prerequisite in premium channels, cementing algae's role in high-value aquaculture.

Regulatory Approval Lag for Novel Algae Strains

The United States Food and Drug Administration's Generally Recognized as Safe pathway and the European Union's Novel Food regulation can add 2-3 years and significant documentation costs before the commercial launch of new strains. This delay is acute for CRISPR-edited high-EPA algae that offer superior lipid profiles yet face stricter scrutiny, especially in Europe and Japan, where public skepticism toward gene editing persists. Companies such as KnipBio secured United States and Canadian approvals for bacterial biomass in 2025 but still await European clearance, limiting scale-up across the microalgae-based aquafeed market. Regulatory fragmentation forces producers to maintain separate production lines, duplicating costs and slowing global rollouts. Lack of harmonization under Codex Alimentarius keeps the approval lag a structural restraint in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Pledges are Accelerating Algae Inclusion

- Regenerative Aquaculture Certifications are Emerging

- Public Perception of Genetically Edited Algal Feeds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Algal oil held the largest 38.0% share of the microalgae-based aquafeed market in 2025, as salmon producers rely on its stable docosahexaenoic acid profile to secure premium fillet pricing. In contrast, protein isolates are the fastest segment and are projected to grow at a 13.5% CAGR during 2026-2031 as shrimp hatcheries in Thailand, Ecuador, and India replace fishmeal with high-protein concentrates that lift larval survival. The microalgae-based aquafeed market size for isolates is expanding further as the United States Food and Drug Administration's Generally Recognized as Safe rules and the European Union's Novel Food reviews favor standardized compositions that streamline safety checks. Cost declines in closed photobioreactors and the ability to monetize carbon credits narrow the price gap with fishmeal, reinforcing the adoption of the fastest segment.

Whole microalgae and algal meal occupy niche positions that deliver pigmentation and immune benefits to tilapia and ornamental fish at 5-15% inclusion, even when cell wall barriers reduce digestibility. Algal oil is still forecast to grow at a solid CAGR through 2031 as multi-year supply contracts ensure steady demand in premium salmon and marine finfish feeds. Multi-functional oils, such as the Omega Origins launched by Fermentalg in 2026, contain 40% eicosapentaenoic acid and 20% docosahexaenoic acid. These oils reduce post-processing steps and lower finished-feed costs. Producers that can co-cultivate multiple strains inside modular systems gain flexibility to supply blended ingredients that meet diverse nutrient targets across the remaining segments.

Complete Report Scope:

- By Product Type

- Whole Microalgae

- Algae Meal/Flour

- Algal Oil (DHA-rich)

- Algae Protein Isolate

- Others

- By Species

- Spirulina

- Chlorella

- Nannochloropsis

- Schizochytrium

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

Europe delivered the largest 35.5% share of the microalgae-based aquafeed market in 2025, as Norwegian and Danish salmon farmers adopted algal oils to meet Marine Stewardship Council traceability and antibiotic-free standards. Asia-Pacific is the fastest region, forecast to expand at a 10.7% CAGR from 2026-2031 on the back of India's zero-tariff algal oil policy and China's alternative-protein incentives. Europe continues to channel public funding into microalgae biorefineries that clean aquaculture effluent, while Asia-Pacific leverages import duty cuts to narrow the cost gap with fishmeal. These contrasting yet complementary policy drivers underpin divergent growth paths in the largest and fastest regional markets.

North America is growing steadily as Food and Drug Administration approvals open the door for novel strains and as salmon producers integrate algae to curb Scope 3 emissions. South America benefits from Chilean data showing improved feed conversion ratios and fewer downgrades when algal oils exceed 7.2% combined long-chain omega-3 content. The Middle East scales seawater-adapted Spirulina and Chlorella facilities that link carbon capture with inland aquaculture expansion. Africa remains early-stage, with pilot projects in Egypt and South Africa awaiting further cost declines before commercial rollouts.

Regional investment patterns signal accelerating capacity additions. European photobioreactor hubs in Scotland and France target multi-fold capacity jumps by 2027, while Japanese and South Korean pilots validate technology ahead of full commercialization. New carbon-credit programs in Norway and California offset up to 15% of production cost, making algae more competitive and fuelling cross-continental interest. As fishmeal volatility persists and sustainability labels harden, every major aquaculture zone is projected to widen algae usage, collectively expanding the global microalgae-based aquafeed market.

- Cargill, Incorporated

- Corbion N.V.

- BioMar Group A/S

- Nutreco N.V. (Skretting)

- Alltech, Inc.

- DSM-Firmenich AG

- Archer-Daniels-Midland Company

- AlgaEnergy, S.A.

- Innovafeed SAS

- KnipBio, Inc.

- Cyanotech Corporation

- Algatech Ltd.

- Mowi ASA (Mowi Feed)

- Aller Aqua A/S

- Qualitas Health Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid cost decline in closed-photobioreactor farming

- 4.2.2 Premium pricing opportunity for antibiotic-free seafood

- 4.2.3 Corporate net-zero pledges are accelerating algae inclusion

- 4.2.4 Regenerative aquaculture certifications are emerging

- 4.2.5 Carbon-credit monetization for algae feed plants

- 4.2.6 Marine ingredient supply volatility post-2025 El Nino events

- 4.3 Market Restraints

- 4.3.1 Price gap versus fishmeal persists in developing nations

- 4.3.2 Regulatory approval lag for novel algae strains

- 4.3.3 Mycotoxin and heavy-metal contamination risk

- 4.3.4 Public perception of "genetically edited" algal feeds

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Whole Microalgae

- 5.1.2 Algae Meal/Flour

- 5.1.3 Algal Oil (DHA-rich)

- 5.1.4 Algae Protein Isolate

- 5.1.5 Others

- 5.2 By Species

- 5.2.1 Spirulina

- 5.2.2 Chlorella

- 5.2.3 Nannochloropsis

- 5.2.4 Schizochytrium

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 Australia and New Zealand

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis (2025)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Corbion N.V.

- 6.4.3 BioMar Group A/S

- 6.4.4 Nutreco N.V. (Skretting)

- 6.4.5 Alltech, Inc.

- 6.4.6 DSM-Firmenich AG

- 6.4.7 Archer-Daniels-Midland Company

- 6.4.8 AlgaEnergy, S.A.

- 6.4.9 Innovafeed SAS

- 6.4.10 KnipBio, Inc.

- 6.4.11 Cyanotech Corporation

- 6.4.12 Algatech Ltd.

- 6.4.13 Mowi ASA (Mowi Feed)

- 6.4.14 Aller Aqua A/S

- 6.4.15 Qualitas Health Inc.