|

시장보고서

상품코드

2072907

토큰화 증권 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Tokenized Securities - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

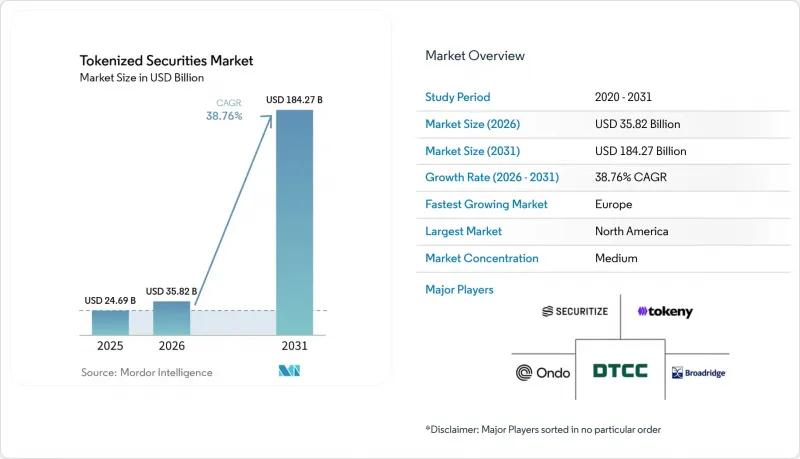

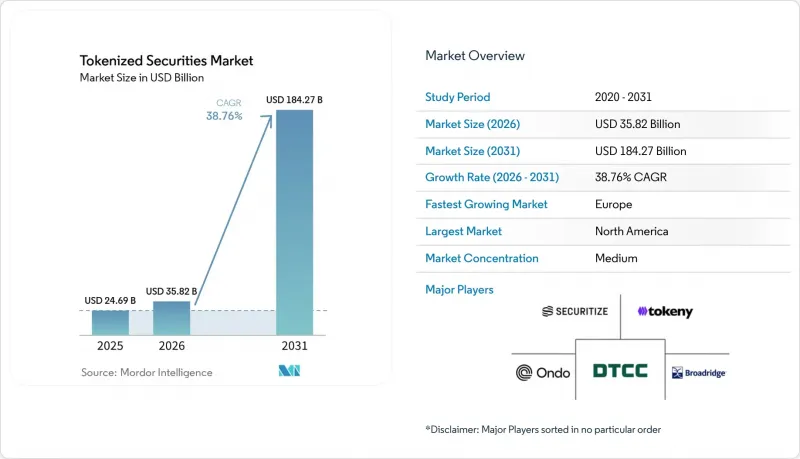

Mordor Intelligence에 의하면, 토큰화 증권 시장 규모는 2025년 246억 9,000만 달러에서 2026년에는 358억 2,000만 달러로 확대되어 2031년까지 1,842억 7,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 38.76%로 성장할 전망입니다.

본 보고서는 자산군(토큰화된 주식 증권 등), 투자자 유형(기관 투자자, 개인 투자자), 토큰화 형태(네이티브 토큰화된 증권 등), 발행 주체 유형(전통적인 금융기관, 기업 발행 주체 등) 및 지역(북미, 남미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 토큰화 증권 시장 동향과 인사이트

주요 금융 중심지의 규제 명확화

2026년 3월 SEC와 CFTC가 발표한 해석 지침을 통해, 디지털 증권을 미국 증권법상의 의무를 전면적으로 준수해야 하는 암호화폐 범주로 정의함으로써, 토큰화 증권 시장의 주요 법적 불확실성이 해소되었습니다. 그 다음 날, SEC는 나스닥에 대해 토큰화된 주식과 기존 주식을 동일한 체결 우선순위를 가진 통합 주문장 상에서 거래하도록 승인했습니다. 이는 규제 대상인 거래소 인프라 내에서 온체인 및 오프체인 증권이 기능적으로 동등하게 취급된다는 것을 시사합니다. 싱가포르에서는 개정된 “자본 시장 상품의 토큰화에 관한 지침”에 따라 발행, 거래, 보관, 결제 각 단계에서 증권 규정 준수에 대한 기대가 높아지면서, 기관을 대상으로 한 종단 간 규정 준수의 명확화를 요구하는 운영 체계가 강화되었습니다. 이러한 동향을 종합해 보면, 주요 금융 중심지들이 보다 명확한 규칙과 신뢰할 수 있는 운영 조건을 제공하게 됨에 따라, 규제가 완화된 역외 시장이 기존에 가지고 있던 비용 측면의 우위는 점차 줄어들고 있습니다. 이러한 변화로 인해 토큰화 증권 시장에서 은행, 자산운용사 및 장기 기관 투자자들의 내부 승인 절차가 가속화되고 있습니다.

토큰화 펀드 및 공모 증권에 대한 기관 투자자의 투자 비중 증가

대기업들이 시범 사업에 활동을 국한하지 않고 규제 대상 상품을 잇달아 출시함에 따라, 토큰화 증권 시장에 기관 투자자들의 참여가 증가하고 있습니다. J.P. 모건 자산운용은 2025년 12월, 자사 최초의 토큰화된 머니마켓 펀드인 ‘MONY”를 출범시켰고, 이어 2026년에는 “JLTXX”를 출시하여, 적격 투자자가 이용할 수 있는 토큰화된 유동성 상품의 범위를 확대했습니다. 골드만삭스와 BNY도 2025년 7월에 토큰화된 머니마켓 펀드 솔루션을 출시했으며, 대형 금융기관들이 토큰화된 펀드의 지분을 단순한 실험적인 ‘래퍼”가 아니라, 실용적인 자본 시장 인프라로 자리매김하고 있음을 보여주었습니다. 수요를 견인하는 요인은 단순히 상품에 대한 접근성뿐만이 아닙니다. 기관 투자자들은 담보 관리, 재무 관리, 결제 등 각 업무 흐름에서 보다 효율적으로 운용할 수 있는 토큰화된 증권을 원하고 있습니다. 그 결과, 토큰화 증권 시장은 기존의 포트폴리오 배분 범위를 벗어난 운용 기능에서도 자본을 유치하고 있습니다.

관할 구역 간 규제의 파편화

토큰화된 증권 시장은 여전히 국경을 초월한 큰 제약에 직면해 있습니다. 이는 각 관할 구역 내의 규제 체계가 명확해지는 속도가, 관할 구역 간의 상호 운용성이 확보되는 속도보다 빠르기 때문입니다. OECD는 2025년 1월, 시장별 법적 취급의 차이가 결제의 확정성을 위협하고 유동성을 국가나 지역의 사일로 안에 가두어버릴 우려가 있으며, 이로 인해 토큰화의 주요 효율성 근거 중 하나가 직접적으로 약화될 것이라고 지적했습니다. 또한, MAS(싱가포르 금융관리청)는 2025년 6월, 싱가포르 규제 체제의 다음 단계에서 디지털 토큰 서비스 제공업체에 대해 더욱 엄격한 라이선스 요건이 부과될 것이라고 밝혔습니다. 이는 혁신에 친화적인 거점이라 할지라도, 규정 준수 요건이 급격히 높아질 가능성이 있음을 보여줍니다. 그 결과, 기업은 유사한 상품을 서로 다른 지역에 판매하기 위해 종종 별도의 법인, 라이선싱 체계 및 관리 체계를 마련해야 합니다. 이로 인해 비용이 증가하고, 도입이 지연되며, 토큰화된 증권 시장이 국경을 넘어 확장되는 속도가 제한될 수밖에 없습니다.

부문별 분석

2025년 기준으로, 토큰화 증권 시장의 61.36%를 채권 및 고정수익 상품이 차지하고 있으며, 다른 자산군을 크게 앞지르며 1위를 차지하고 있습니다. 이 부문이 처음에 규모를 확대할 수 있었던 이유는 단기 미국 국채나 머니마켓 상품이 평가 및 규제가 용이하고, 기관 투자자의 업무 흐름에서 담보 적격 자산으로 분류하기 쉽기 때문입니다. 2025년 하반기에 승인된 DTCC의 시범 프로그램에는 미국 국채와 주요 ETF가 포함되어 있으며, 이는 기존 포스트트레이드 시스템과 토큰화 발행 모델 간의 운영적 가교 역할을 하는 고정수익 자산의 역할을 강화하는 것입니다. J.P. 모건 자산운용, 골드만삭스, BNY가 출시한 상품 역시 이러한 추세를 뒷받침하고 있으며, 토큰화된 머니마켓 및 미국 국채 연동형 구조는 이미 유동성 관리 및 결제 유연성을 높이기 위해 활용되고 있습니다. 실제로 고정 수익 상품은 개념 증명(PoC) 단계에서 기관 투자자들의 지속적인 활용으로 이어지는 가장 명확한 경로를 제공하기 때문에 토큰화 증권 업계의 기반으로서 계속해서 자리 잡고 있습니다.

주식은 가장 빠르게 성장하고 있는 자산군이며, 이 부문의 토큰화 증권 시장 규모는 2031년까지 연평균 성장률(CAGR) 46.21%로 확대될 것으로 전망됩니다. 주문 장부 통합, 주주와의 소통, 기업 활동 처리에 필요한 인프라가 규제된 범위 내에서 더욱 신뢰할 수 있는 형태로 발전하고 있어, 성장이 가속화되고 있습니다. 나스닥이 토큰화된 주식과 기존 주식을 통합된 주문장(order book)에서 거래하도록 허용하는 SEC의 승인은 익숙한 거래소 환경 내에서 상장 주식의 토큰화를 위한 모델을 확립하는 것이며, 이는 큰 진전입니다. 또한, 온도 파이낸스(Ondo Finance)가 브로드리지(Broadridge)와 협력하여 250개 이상의 토큰화된 주식 및 ETF를 지원하게 됨에 따라, 위임장 투표 지원 기능도 개선되었습니다. 이는 주식 도입을 지연시켜 왔던 실무상의 과제 중 하나를 해결하는 것입니다. 투자신탁의 수익권이나 집단투자상품도 이러한 인프라 구축의 혜택을 받고 있습니다. 반면, 사모 신용이나 실물 자산 연동형 상품 등 다른 토큰화 증권은 유통 시장에서의 거래 및 법적 양도에 관한 기준이 개선될 때까지 성장세가 다소 완만할 가능성이 높다고 볼 수 있습니다.

2025년 기준으로 기관 투자자들이 토큰화 증권 시장의 91.48%를 차지하고 있어, 초기 수요가 적격하고 규제 대상인 참여자들에게 집중되어 있음을 여실히 보여주고 있습니다. 대부분의 상품의 경우, 투자자가 매수하거나 보유 자산을 양도하기 전에 KYC(신원 확인) 및 AML(자금 세탁 방지) 심사, 지갑의 화이트리스트 등록, 지속적인 규정 준수 점검이 필요하기 때문에 토큰화 증권 시장의 상품 구조는 여전히 이러한 기반을 반영하고 있습니다. J.P. 모건 자산운용의 “MONY”와 “JLTXX”는 그 대표적인 예이며, 모두 일반 소매 시장에 개방된 것이 아니라 본격적인 유동성 관리 활용 사례를 목적으로, 통제된 판매 및 보고 환경 하에서 운영되고 있습니다. 또한, 법적 소유권의 명확성, 담보로서의 적격성, 그리고 업무의 연속성이 신규성보다 대규모 자산 배분자에게 더 중요하기 때문에 기관 투자자의 우위는 여전히 지속되고 있습니다. 현재로서는 토큰화 증권 업계가 규정 준수 문제의 복잡성을 감당하고 견고한 업무 관리를 요구할 수 있는 기관 투자자들에 의해 계속해서 주도되고 있습니다.

개인 투자자는 가장 빠르게 성장하고 있는 투자자 그룹이며, 토큰화 증권 시장에 대한 이들의 참여는 2031년까지 연평균 성장률(CAGR) 48.72%로 증가할 것으로 전망됩니다. 이러한 변화는 지갑이나 앱을 통해 상장 증권이나 펀드를 소액으로 분할 보유할 수 있게 해주는 소비자용 플랫폼에 의해 뒷받침되고 있습니다. 바이낸스가 2026년에 5달러부터 미국 주식의 분할 보유 서비스를 시작할 예정이며, 계획 중인 ‘bStocks”의 작동 방식은 소비자 대상 판매가 구상 단계에서 실제 제품 설계 단계로 넘어가고 있음을 보여줍니다. 개인 투자자 대상 사업의 확대는 발행사나 플랫폼의 운영 부담도 가중시킵니다. 투자자와의 소통, 적격성 심사, 본인 확인 등을 훨씬 더 방대한 사용자 기반에 대응할 수 있도록 해야 하기 때문입니다. 사용자 기반이 확대됨에 따라, 토큰화된 증권 시장에서는 공시, 거래 기간, 분쟁 해결, 그리고 비기관 투자자에 대한 기업의 행동 처리와 관련하여 더욱 엄격한 규칙이 필요할 것입니다.

지역별 분석

2025년, 북미는 토큰화 증권 시장 점유율의 67.34%를 차지하며 이 분야의 확실한 지역적 중심지로 자리매김했습니다. 이 지역은 미국 시장 인프라의 충실도, 주요 자산운용사 및 시장 인프라 사업자의 집중, 그리고 발행, 거래, 결제를 보다 일관되게 지원하는 일련의 규제 당국의 승인을 통해 혜택을 받고 있습니다. DTCC는 2025년 12월에 토큰화 서비스 인가를 받았으며, 2026년에는 실증 거래 및 상용화 시작이라는 이정표를 확인한 바 있어, 이를 통해 북미는 견고한 기관 투자자 대상 운영 기반을 확립하게 될 것입니다. 2026년 3월 SEC와 CFTC가 해석 지침을 발표하고 나스닥이 이를 승인함에 따라, 법적 및 거래소 차원의 명확성이 더해지면서 해당 지역의 선구자로서의 입지가 더욱 공고해졌습니다. 이러한 요인들이 복합적으로 작용함에 따라, 북미의 토큰화 증권 시장은 이미 시범 운영 단계에서 본격적인 운영 단계로 전환되고 있습니다.

유럽은 가장 빠르게 성장하고 있는 지역 부문이며, 이 지역의 토큰화 증권 시장 규모는 2031년까지 연평균 성장률(CAGR) 44.25%로 확대될 것으로 전망됩니다. 이러한 성장은 도매 시장의 토큰화, 펀드의 토큰화, 그리고 디지털 자산 인프라와 관련된 보다 적극적인 정책 의제에 힘입어 이루어지고 있습니다. 영국에서는 FCA가 2026년 5월에 PS26/7을 발표하여, 토큰화된 인가 펀드의 운용 프레임워크로 “블루프린트” 모델을 수립했습니다. 이를 통해 기업들은 설립 및 감독과 관련하여 보다 명확한 지침을 얻을 수 있게 되었습니다. 또한, 잉글랜드 은행과 FCA는 2026년 5월, 도매 시장에서의 토큰화에 관한 공동 비전을 제시하며, 결제 및 지불 인프라의 장기적인 변화를 뒷받침하고 있습니다. 유럽은 여전히 분류 및 상호운용성과 관련된 과제에 직면해 있지만, 정책 방향에 따라 이 지역은 토큰화 증권 시장에 있어 더욱 매력적인 장소로 자리매김하고 있습니다.

아시아태평양은 현재 시장 점유율이 낮지만, 토큰화 증권 시장의 향후 확대에 있어 여전히 가장 중요한 지역 중 하나입니다. 싱가포르는 개정된 토큰화 지침과 2025년부터 시행될 디지털 토큰 서비스 제공업체에 대한 라이선스 제도의 명확화를 통해 규정 준수 측면에서 높은 기준을 수립함으로써, 기관 투자자를 대상으로 한 발행 및 서비스 제공에 있어 참고할 만한 시장으로 자리매김하고 있습니다. 일본에서는 SBI 홀딩스가 2026년 2월 개인 투자자를 대상으로 한 최초의 보안 토큰 채권 시리즈를 발표했으며, 이는 규제된 국내 체계 하에서 일반 투자자를 위한 보안 토큰 상품도 개발되기 시작했음을 보여줍니다. 중동도 바이낸스가 계획 중인 bStocks 프레임워크 등, ADGM(아부다비 세계 마켓)과 연계된 판매 체제를 통해 점차 입지를 다지고 있습니다. 한편, 남미는 토큰화 증권 시장에서 여전히 초기 탐색 단계에 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the tokenized securities market size is expected to increase from USD 24.69 billion in 2025 to USD 35.82 billion in 2026 and reach USD 184.27 billion by 2031, growing at a CAGR of 38.76% over 2026-2031.

This report is Segmented by Asset Class (Tokenized Equity Securities, and More), by Investor Type (Institutional Investors, Retail Investors), by Tokenization (Native Tokenized Securities, and More), Issuer Type (Traditional Financial Institutions, Corporate Issuers, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Tokenized Securities Market Trends and Insights

Regulatory Clarity in Major Financial Centers

The March 2026 SEC and CFTC interpretive release resolved a central legal uncertainty in the tokenized securities market by defining digital securities as the crypto-asset category subject to full United States securities law obligations. One day later, the SEC approved Nasdaq to trade tokenized and traditional shares on unified order books with identical execution priority, signaling that on-chain and off-chain securities can be treated with functional parity within regulated exchange infrastructure. In Singapore, the revised Guide on the Tokenization of Capital Markets Products raised securities compliance expectations across issuance, trading, custody, and settlement, thereby strengthening the operating framework for institutions seeking end-to-end compliance clarity. Taken together, these actions narrow the old cost advantage of loosely regulated offshore venues because major financial centers now offer clearer rules and more credible operating conditions. That shift is accelerating internal approval cycles across banks, asset managers, and long-term institutional allocators in the tokenized securities market.

Rising Institutional Allocation to Tokenized Funds and Public Securities

Institutional participation in the tokenized securities market is rising because large firms are now launching regulated products rather than limiting activity to pilots. J.P. Morgan Asset Management launched MONY in December 2025 as its first tokenized money market fund, and it followed that with JLTXX in 2026, which broadened the range of tokenized liquidity products available to qualified investors. Goldman Sachs and BNY also launched a tokenized money market fund solution in July 2025, demonstrating that large financial institutions are treating tokenized fund shares as usable capital-market infrastructure rather than as experimental wrappers. The demand driver is not only about product access; institutions also want tokenized securities that can move more efficiently through collateral, treasury, and settlement workflows. As a result, the tokenized securities market is drawing capital from operating functions that sit outside traditional portfolio allocation buckets.

Regulatory Fragmentation Across Jurisdictions

The tokenized securities market still faces a major cross-border limit because regulatory frameworks are becoming clearer within jurisdictions faster than they are becoming compatible across jurisdictions. The OECD noted in January 2025 that differing legal treatments across markets threaten settlement finality and can trap liquidity within national or regional silos, thereby directly weakening one of the main efficiency claims behind tokenization. MAS also clarified in June 2025 that digital token service providers would face a stricter licensing bar under the next phase of Singapore's regime, which shows that compliance thresholds can rise sharply even in innovation-friendly centers. The practical result is that firms often need separate legal entities, licensing structures, and control frameworks to distribute similar products into different regions. That raises cost, slows rollout, and limits how quickly the tokenized securities market can scale across borders.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Fractional Access to Premium Securities and Funds

- Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments

- Smart-Contract, Oracle, and Custody Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Debt and fixed income accounted for 61.36% of the tokenized securities market in 2025, making it the leading asset class by a wide margin. This segment gained scale first because short-duration Treasuries and money market instruments are easier to value, regulate, and position as collateral-grade assets within institutional workflows. The DTCC pilot authorized in late 2025 includes United States Treasuries and major ETFs, which reinforces the role of fixed income as the operational bridge between existing post-trade systems and tokenized issuance models. Product launches from J.P. Morgan Asset Management, Goldman Sachs, and BNY also support this pattern, as tokenized money-market and Treasury-linked structures are already being used to improve liquidity management and settlement flexibility. In practice, fixed income remains the anchor of the tokenized securities industry because it offers the clearest path from proof of concept into repeat institutional use.

Equity securities are the fastest-growing asset class, and the tokenized securities market size for this segment is projected to expand at 46.21% CAGR through 2031. Growth is accelerating because the required infrastructure for order-book integration, shareholder communications, and corporate action handling is now becoming more credible at a regulated scale. The SEC approval that allows Nasdaq to trade tokenized and traditional shares on a unified order book is a major step because it creates a template for listed equity tokenization within a familiar exchange environment. Proxy voting support is also improving, as shown by Ondo Finance's integration with Broadridge for more than 250 tokenized stocks and ETFs, which addresses one of the practical gaps that had slowed equity adoption. Fund shares and collective investment products also benefit from this infrastructure buildout. In contrast, other tokenized securities, such as private credit and real-asset-linked products, are likely to grow more gradually until secondary trading and legal transfer standards improve.

Institutional investors held 91.48% of the tokenized securities market in 2025, underscoring the concentration of early demand among qualified and regulated participants. The product structure of the tokenized securities market still reflects that base, because many offerings require KYC and AML screening, wallet allowlisting, and ongoing compliance checks before investors can subscribe or transfer holdings. J.P. Morgan Asset Management's MONY and JLTXX are clear examples, as both products sit within controlled distribution and reporting environments aimed at serious liquidity management use cases rather than open retail access. Institutional dominance also persists because legal ownership clarity, collateral eligibility, and operational continuity matter more to large allocators than novelty. For now, the tokenized securities industry remains led by institutions that can absorb compliance complexity and demand robust operational controls.

Retail investors are the fastest-growing investor group, and their participation in the tokenized securities market is forecast to rise at 48.72% CAGR through 2031. This shift is being supported by consumer-facing platforms that are opening fractional exposure to public securities and funds through wallet-based or app-based channels. Binance's 2026 launch of fractional United States stock access at USD 5 and its planned bStocks structure illustrate how retail distribution is moving from concept to live product design. Retail expansion also increases the operating burden on issuers and platforms, as investor communication, suitability reviews, and identity verification must scale across a much larger user base. As that user base grows, the tokenized securities market will need stronger rules around disclosures, trading windows, dispute resolution, and treatment of corporate actions for non-institutional holders.

Complete Report Scope:

- By Asset Class

- Tokenized Equity Securities

- Tokenized Debt / Fixed Income Securities

- Tokenized Fund Shares / Collective Investment Schemes

- Other Tokenized Securities

- By Investor Type

- Institutional Investors

- Retail Investors

- By Tokenization

- Native Tokenized Securities

- Non-Native / Represented / Wrapped

- Hybrid Structures

- By Issuer Type

- Traditional Financial Institutions

- Crypto-Native / Specialized Tokenization Platforms

- Public Sector & Development Institutions

- Corporate Issuers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Geography Analysis

North America captured 67.34% of the tokenized securities market share in 2025, which made it the clear regional center of activity. The region benefits from the depth of the United States market infrastructure, the concentration of major asset managers and market utilities, and a sequence of regulatory approvals that now support issuance, trading, and settlement more coherently. DTCC received authorization for its tokenization service in December 2025 and confirmed live-pilot trading and commercial-launch milestones in 2026, which will give North America a strong institutional operating base. The SEC and CFTC interpretive release and the Nasdaq approval in March 2026 added legal and exchange-level clarity, which further strengthened the region's first-mover position. This combination means the tokenized securities market in North America is already moving from pilot activity toward production-grade implementation.

Europe is the fastest-growing regional segment, and the tokenized securities market size in this geography is projected to expand at 44.25% CAGR through 2031. Growth is being supported by a more active policy agenda around wholesale market tokenization, fund tokenization, and digital asset infrastructure. In the United Kingdom, the FCA issued PS26/7 in May 2026 and set the Blueprint model as the operating framework for tokenized authorized funds, providing firms with a clearer path to launch and supervision. The Bank of England and FCA also set out a shared vision for tokenization in wholesale markets in May 2026, which supports longer-term changes in settlement and payments infrastructure. Europe still faces classification and interoperability frictions, but the policy direction is making the region more attractive for the tokenized securities market.

Asia-Pacific accounts for a smaller share today, but it remains one of the most important regions for future expansion in the tokenized securities market. Singapore set a high compliance benchmark with its revised tokenization guide and the 2025 clarification of the licensing regime for digital token service providers, making it a reference market for institutional-grade issuance and servicing. In Japan, SBI Holdings announced its first security token bond series for individual investors in February 2026, indicating that retail-facing security token products are also beginning to develop under regulated local structures. The Middle East is also emerging through ADGM-linked distribution structures such as Binance's planned bStocks framework. At the same time, South America remains at an earlier exploratory stage in the tokenized securities market.

- Securitize

- Ondo Finance

- Broadridge Financial Solutions, Inc.

- DTCC

- tZERO Technologies, LLC

- Tokeny Solutions SA

- INX Digital Company, Inc.

- Fireblocks Inc.

- Chainlink Labs, Inc.

- Polymesh Association

- ADDX Pte. Ltd.

- Apex Group Ltd.

- BlackRock, Inc.

- Franklin Resources, Inc.

- JPMorgan Chase and Co.

- Goldman Sachs Group, Inc.

- BNY

- Citi

- Nasdaq, Inc.

- HSBC Holdings plc

- Deutsche Borse AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Clarity in Major Financial Centers

- 4.2.2 Rising Institutional Allocation to Tokenized Funds and Public Securities

- 4.2.3 Demand for Fractional Access to Premium Securities and Funds

- 4.2.4 Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments

- 4.2.5 Infrastructure Convergence Between Market Utilities, Banks, and Digital Asset Platforms

- 4.2.6 24/7 Secondary Market Demand from Digitally Native Investors

- 4.3 Market Restraints

- 4.3.1 Regulatory Fragmentation Across Jurisdictions

- 4.3.2 Smart-Contract, Oracle, and Custody Risk

- 4.3.3 Limited Standardization of Legal Ownership and Transfer Rights

- 4.3.4 Thin Liquidity Outside a Few Flagship Products

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Asset Class

- 5.1.1 Tokenized Equity Securities

- 5.1.2 Tokenized Debt / Fixed Income Securities

- 5.1.3 Tokenized Fund Shares / Collective Investment Schemes

- 5.1.4 Other Tokenized Securities

- 5.2 By Investor Type

- 5.2.1 Institutional Investors

- 5.2.2 Retail Investors

- 5.3 By Tokenization

- 5.3.1 Native Tokenized Securities

- 5.3.2 Non-Native / Represented / Wrapped

- 5.3.3 Hybrid Structures

- 5.4 By Issuer Type

- 5.4.1 Traditional Financial Institutions

- 5.4.2 Crypto-Native / Specialized Tokenization Platforms

- 5.4.3 Public Sector & Development Institutions

- 5.4.4 Corporate Issuers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Securitize

- 6.4.2 Ondo Finance

- 6.4.3 Broadridge Financial Solutions, Inc.

- 6.4.4 DTCC

- 6.4.5 tZERO Technologies, LLC

- 6.4.6 Tokeny Solutions SA

- 6.4.7 INX Digital Company, Inc.

- 6.4.8 Fireblocks Inc.

- 6.4.9 Chainlink Labs, Inc.

- 6.4.10 Polymesh Association

- 6.4.11 ADDX Pte. Ltd.

- 6.4.12 Apex Group Ltd.

- 6.4.13 BlackRock, Inc.

- 6.4.14 Franklin Resources, Inc.

- 6.4.15 JPMorgan Chase and Co.

- 6.4.16 Goldman Sachs Group, Inc.

- 6.4.17 BNY

- 6.4.18 Citi

- 6.4.19 Nasdaq, Inc.

- 6.4.20 HSBC Holdings plc

- 6.4.21 Deutsche Borse AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment