|

시장보고서

상품코드

2072910

육계 사료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Broiler Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

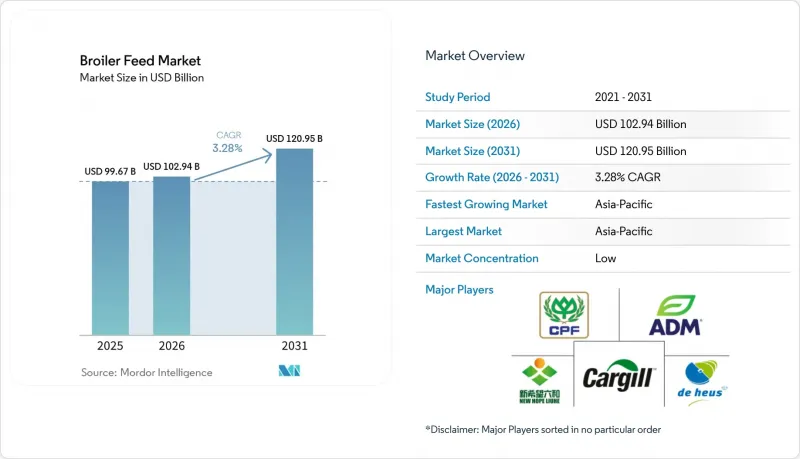

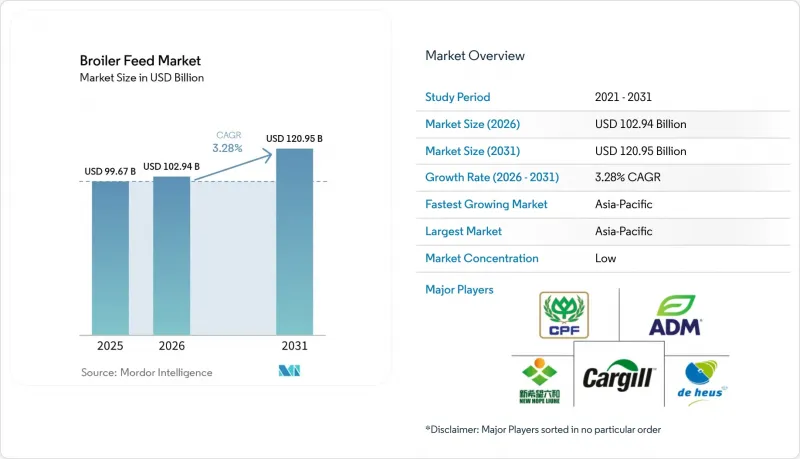

Mordor Intelligence에 의하면, 육계 사료 시장 규모는 2025년 996억 7,000만 달러에서 2026년에는 1,029억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 3.28%로 성장을 지속하여, 2031년에는 1,209억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 사료 단계(스타터, 그로워, 피니셔), 형태(펠렛, 크럼블, 매시, 기타), 원료 유형(곡물, 유지종자박, 당밀, 어유 및 어분, 첨가제, 기타 원료 유형), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 육계 사료 시장 동향과 인사이트

가금류 소비 확대와 단백질 섭취의 용이성

가금류 고기는 전 세계 식생활에서 그 역할이 확대되고 있으며, 이것이 육계 사료 수요를 직접 뒷받침하고 있습니다. 경제협력개발기구(OECD)와 유엔식량농업기구(FAO)는 2034년까지 전 세계 육류 소비량 증가분의 62%를 가금류가 차지할 것으로 예측하고 있으며, 이러한 증가분의 상당 부분이 개발도상 지역에 집중될 것으로 전망됩니다. 또한, 가금류 고기는 여전히 비교적 저렴한 동물성 단백질 공급원 중 하나로, 가계의 식비 예산이 압박받는 상황에서도 소비를 유지하는 데 도움이 되고 있습니다. 다른 단백질 원료가 더 심각한 대체 위험에 직면해 있더라도, 안정적인 육류 수요가 사료 소비량을 뒷받침하기 때문에 합리적인 가격은 육계 사료 시장에 있어 중요한 요소가 됩니다. MHP SE는 2025년 9개월간의 매출액이 26억 4,000만 달러를 기록해 전년 동기 대비 16% 증가했다고 보고했습니다. 이러한 성장은 견조한 가금류 수요, 안정적인 시장 가격, 그리고 스페인 가금류 생산 업체인 Grupo UVESA의 인수를 통해 뒷받침되었습니다. 가금류 생산량 증가와 생산 능력 확충에는 상업용 사료 소비량의 꾸준한 증가가 필수적이기 때문에 이러한 추세는 육계 사료에 대한 지속적인 수요를 뒷받침하고 있습니다.

상업용 육계 사육의 확대와 사료 외주화

가금류 사육이 가정 뒷마당 방식에서 상업적·계약 기반의 양계로 전환됨에 따라, 육계 사료 시장은 더욱 꾸준히 성장할 것입니다. 대규모 육계 사육 사업에서는 성장 목표, 군의 균일성 및 가공업체의 요구 사항으로 인해 농장에서의 비균일한 배합을 허용할 여지가 거의 없기 때문에 표준화된 배합 사료에 의존하고 있습니다. 생산자가 통합형 또는 계약형 모델로 전환하면, 일반적으로 자금 조달, 수의사의 지원, 그리고 구매자와의 계약이 해당 시스템에 연계되어 있기 때문에 공식적인 사료 공급 체제에 계속 의존하게 됩니다. ForFarmers N.V.는 2026년 사료 생산과 양계·가공 사업을 통합하여 ForFarmers Polska를 설립함으로써, 사료가 체계화된 가금류 공급망에 얼마나 깊이 통합되고 있는지를 보여주었습니다. 또한, Koninklijke De Heus Voeders B.V.도 2026년 3월 CJ Feed and Care를 인수함으로써 아시아에서의 입지를 확대하고, 17곳의 사료 공장을 추가하는 한편, 주요 가금류 생산 시장에서의 사업 범위를 넓혔습니다. 이러한 추세는 양계업의 규모가 확대되고, 더욱 조직화되며, 외부 사료 공급에 대한 의존도가 높아질수록 육계 사료 시장이 가장 큰 혜택을 보게 된다는 견해를 뒷받침하고 있습니다.

유럽연합(EU)의 산림파괴 규제(EUDR)와 관련된 대두 추적성 프리미엄

유럽연합(EU)의 산림 파괴 규제(EUDR)는 특히 대두박에 대한 의존도가 높은 공급망에서 육계 사료 시장에 새로운 규정 준수 요건을 추가하는 것입니다. 이 규정은 대상 상품 및 제품에 대해 구획 단위의 추적성을 의무화하고 있으며, 대규모 및 중규모 사업자는 2026년 12월 30일까지 이에 대응해야 합니다. 규정을 위반할 경우, 사업자의 EU 내 연간 매출액의 최대 4%에 해당하는 벌금이 부과될 수 있습니다. 유럽 사료 제조업체 연합(EFF)은 규정 준수 체계가 아직 완전히 갖춰지지 않아 대두 거래에 혼란이 발생할 위험이 있다고 보고했으며, 이로 인해 조달 환경은 더욱 엄격해지고 유연성이 떨어지고 있습니다. 이러한 요건으로 인해 유럽 관련 수요에 대응하는 수출업체 및 사료 제조업체의 서류 작성 비용이 증가하게 됩니다. 또한, 강력한 추적 관리 체계를 갖추지 못한 정유시설의 경우, 대두 조달이 더욱 어려워질 것입니다. 실질적으로는 이로 인해 조달 프리미엄이 상승하게 되어, 육계 사료 시장에서 보다 다양한 단백질 원료에 대한 검토가 촉진될 것입니다.

부문별 분석

사료 단계별 부문 중 가장 큰 비중을 차지한 것은 피니셔(비육기)였으며, 2025년에는 육계 사료 시장 점유율의 42.6%를 차지했습니다. 이러한 1위 성적은 생산자들이 도체 수율과 사료 효율에 주력하는 최종 성장기에 나타나는 높은 사료 섭취량을 반영한 것입니다. 상업적인 육계 생산 시스템에서는 최종 단계가 판매 가능한 생산량과 가공 수익에 직접적인 영향을 미치기 때문에 피니셔용 사료에 큰 중점을 두고 있습니다. 가장 빠르게 성장하고 있는 사료 단계 부문은 스타터이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.1%로 성장할 것으로 전망됩니다. 이러한 급속한 성장세는 현재 더 많은 생산자들이 생후 초기 영양을 단순한 기초 사료가 아닌 생산 성능의 토대로 인식하고 있음을 보여줍니다.

스타터 사료가 주목을 받고 있는 이유는 장의 발달, 면역력, 영양소 흡수가 생산 주기의 초기 단계에서 결정되기 때문입니다. 성장기는 초기 발달 단계와 대량 생산이 이루어지는 마무리 단계를 연결하는 중요한 역할을 담당하고 있기 때문에 여전히 중요한 균형 조정 역할을 수행하고 있습니다. 2026년 『Poultry Science』지에 게재된 연구에 따르면, 저에너지 육계 사료에 B-만나나제를 첨가함으로써 영양소 이용 효율과 성장 성적이 향상된 것으로 밝혀졌습니다. 이는 생산성을 유지하면서 사료 비용을 절감하기 위한, 효소를 활용한 사료 재조성 전략에 대한 업계의 관심이 여전히 높음을 보여줍니다. 이는 육계 사료 시장에서 가치의 확대가 단순히 판매량 증가에 그치지 않고, 각 단계에서 더욱 정밀한 사료 급여 판단에도 반영되고 있음을 의미합니다. 2026년 3월, Cooperatie Koninklijke Agrifirm U.A.는 Hamlet Protein 인수를 합의했는데, 이는 생후 초기 및 특수 영양 분야가 여전히 사업 확장을 위한 매력적인 영역임을 입증하고 있습니다.

지역별 분석

아시아태평양은 2025년에 육계 사료 시장 점유율의 46.5%를 차지하는 최대 지역 부문이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.3%를 나타낼 것으로 전망되는 가장 빠르게 성장하는 지역 부문이기도 합니다. 이러한 위상은 가금류에 대한 활발한 수요, 상업적 생산의 확대, 그리고 많은 인구 밀집 지역에서 닭고기가 널리 보급되고 가격이 저렴하다는 점을 반영하고 있습니다. 경제협력개발기구(OECD)와 유엔식량농업기구(FAO)의 전망도 이러한 추세를 뒷받침하고 있으며, 2034년까지 가금류 소비량 증가분 대부분은 아시아 및 기타 개발도상 지역에서 발생할 것으로 예측됩니다. Koninklijke De Heus Voeders B.V.는 2026년 3월, CJ Feed and Care를 통해 아시아 내 사업 기반을 확대하고 있으며, 이는 해당 지역의 육계 사료 시장이 여전히 장기적인 투자처로서 매력적임을 입증하고 있습니다.

남미는 가금류 생산과 사료 수요가 곡물 및 유지종자공급 상황과 밀접하게 연관되어 있기 때문에 육계 사료 시장에서 여전히 중요한 지역입니다. 브라질은 견고한 가금류 생산 기반은 물론, 사료 배합과 관련된 농업 원료 공급에서 중요한 역할을 담당하고 있기 때문에 특히 큰 영향력을 행사하고 있습니다. 카길사는 2025년, 브라질의 Mig-Plus사를 인수하기 위한 구속력 있는 제안을 발표했습니다. 이는 영양 관련 기업들이 주요 생산 시장에서 사업 기반을 더욱 확대할 여지가 여전히 남아 있음을 보여줍니다. 북미는 생산량 측면에서 보다 성숙한 시장이기 때문에 경쟁의 초점은 사료 생산량의 대폭적인 증가보다는 효율성, 배합 개선 및 첨가제의 성능에 맞추어져 있습니다. 즉, 북미와 남미의 육계 사료 시장은 남미의 규모에서 비롯된 수요와 북미의 성능 중심형 차별화가 결합된 형태를 띠고 있습니다.

유럽은 육계 사료 시장에서 성장률은 낮지만, 규제 준수의 중요성이 더 큰 지역으로 남아 있습니다. 유럽연합(EU)의 산림 파괴 규제에 따라 사료 제조업체들은 2026년 12월 30일까지 추적 가능성이 더 높은 대두 조달 시스템을 구축해야 합니다. 아프리카와 중동에서는 인구가 급속히 증가하고 식량 수요 패턴이 변화하는 시장 상황에서 가금류가 여전히 실용적인 단백질 공급원으로서 자리 잡고 있어 향후 성장 여지가 크다고 할 수 있습니다. 또한, 기후 온난화에 따라 이러한 지역, 특히 가금류 생산이 지속적인 온도 스트레스에 노출되어 있는 지역에서는 기능성 사료 및 내열성 사료 솔루션의 중요성이 커지고 있습니다. 그 결과, 육계 사료 시장에서는 지역별로 뚜렷한 우선순위가 나타나는데, 아시아태평양에서는 생산 규모가 중시되고, 유럽에서는 규제 준수에 초점이 맞추어지며, 아프리카 및 중동에서는 시장 접근성, 공급망의 회복탄력성, 그리고 업계의 규범화가 우선시되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the broiler feed market size is anticipated to grow from USD 99.67 billion in 2025 to USD 102.94 billion in 2026 and is forecast to reach USD 120.95 billion by 2031 at 3.28% CAGR over 2026-2031.

This report is Segmented by Feed Phase (Starter, Grower, and Finisher), by Form (Pellets, Crumbles, Mash, and Others), by Ingredient Type (Cereals, Oilseed Meal, Molasses, Fish Oil and Fish Meal, Additives, and Other Ingredient Types), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Broiler Feed Market Trends and Insights

Rising Poultry Meat Consumption and Protein Affordability

Poultry meat is expanding its role in global diets, which directly supports demand for broiler feed. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization projected that poultry will account for 62% of additional global meat consumption through 2034, with much of that increase concentrated in developing regions. Poultry also remains one of the more affordable animal proteins, which helps sustain consumption when household food budgets come under pressure. Affordability matters for the broiler feed market because stable meat demand protects feed volumes, even when other proteins face a sharper substitution risk. MHP SE reported nine-month 2025 revenue of USD 2.64 billion, representing a 16% year-on-year increase. The growth was supported by strong poultry demand, stable market pricing, and the consolidation of Spanish poultry producer Grupo UVESA. This trend supports sustained demand for broiler feed, as growing poultry output and capacity expansion require consistent increases in commercial feed consumption.

Commercial Broiler Farming Expansion and Feed Outsourcing

The broiler feed market grows more steadily when poultry production shifts from backyard systems to commercial and contract-based farming. Larger broiler operations depend on standardized compound feed because growth targets, flock uniformity, and processor requirements leave little room for inconsistent farm mixing. Once growers move to integrated or contract models, they usually remain tied to formal feed supply because financing, veterinary support, and buyer agreements are tied to that system. ForFarmers N.V. formed ForFarmers Polska in 2026 by combining feed production with poultry farming and processing, demonstrating how feed is being drawn deeper into organized poultry chains. Koninklijke De Heus Voeders B.V. also widened its position in Asia in March 2026 through the acquisition of CJ Feed and Care, adding 17 feed mills and extending its reach in major poultry-producing markets. These developments support the view that the broiler feed market benefits most when poultry farming becomes larger, more formal, and more dependent on outsourced feed.

European Union Deforestation Regulation (EUDR)-Linked Soy Traceability Premiums

The European Union Deforestation Regulation (EUDR) adds a new compliance layer to the broiler feed market, especially for supply chains with heavy soybean meal exposure. The regulation mandates plot-level traceability for covered commodities and products, with large and medium-sized operators required to comply by December 30, 2026. Non-compliance can result in penalties of up to 4% of an operator's annual European Union turnover. The European Feed Manufacturers' Federation reported disruption risk in the soy trade due to compliance systems that were still not fully ready, creating a tighter, less flexible sourcing environment. These requirements increase documentation costs for exporters and compounders that serve Europe-linked demand. They also make soy procurement less straightforward for mills that lack strong traceability systems. In practical terms, this raises sourcing premiums and encourages the broiler feed market to examine more diversified protein inputs.

Other drivers and restraints analyzed in the detailed report include:

- Higher Focus on Feed Conversion and Cost Efficiency

- Shift toward Antibiotic-Free and Additive-Led Feed Programs

- Climate-Driven Mycotoxin and Ingredient-Quality Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The largest feed phase segment was finisher, which held 42.6% of the broiler feed market share in 2025. This lead reflects the high feed intake during the final growth window, when producers focus on carcass yield and feed efficiency. Commercial broiler systems place strong emphasis on finisher diets because the last stage directly affects saleable output and processing returns. The fastest-growing feed phase segment is the starter, projected to grow at a 4.1% CAGR during 2026-2031. That faster pace shows that more producers now treat early-life nutrition as a performance foundation rather than a basic opening ration.

Starter diets are gaining more attention because gut development, immunity, and nutrient uptake are set early in the production cycle. The grower phase still plays a key balancing role because it connects early development with the high-volume finisher stage. Research published in Poultry Science in 2026 found that B-mannanase supplementation in reduced-energy broiler diets improved nutrient utilization and growth performance, highlighting continued industry interest in enzyme-enabled feed reformulation strategies to maintain productivity while reducing feed costs. This means value growth in the broiler feed market is not limited to higher volumes, but also reflects more precise feeding decisions across each phase. Cooperatie Koninklijke Agrifirm U.A. agreed to acquire Hamlet Protein in March 2026, underscoring that early-life and specialty nutrition remain attractive areas for commercial expansion.

Complete Report Scope:

- By Feed Phase

- Starter

- Grower

- Finisher

- By Form

- Pellets

- Crumbles

- Mash

- Others

- By Ingredient Type

- Cereals

- Oilseed Meal

- Molasses

- Fish Oil and Fish Meal

- Additives

- Other Ingredient Types

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- Thailand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific was the largest regional segment with 46.5% of the broiler feed market share in 2025, and it is also the fastest regional segment with a projected 4.3% CAGR during 2026-2031. This position reflects strong poultry demand, rising commercial production, and the broad affordability of chicken across many large population centers. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization outlook support this direction, as much of the added poultry consumption through 2034 is projected to come from Asia and other developing regions. Koninklijke De Heus Voeders B.V. has expanded its Asian platform in March 2026 through CJ Feed and Care, reinforcing that the broiler feed market in the region remains attractive for long-term investment.

South America remains an important region in the broiler feed market because poultry production and feed demand are closely connected to grain and oilseed availability. Brazil remains especially influential because it combines a strong poultry base with a major role in agricultural raw materials tied to feed formulation. Cargill, Incorporated, announced in 2025 a binding offer to acquire Mig-Plus in Brazil, indicating that nutrition companies still see room to deepen their footprint in major producing markets. North America is more mature by volume, so competition there centers more on efficiency, formulation upgrades, and additive performance than on large jumps in feed tonnage. This means the broiler feed market in the Americas combines scale-driven demand in South America with performance-led differentiation in North America.

Europe remains a lower-growth but higher-compliance part of the broiler feed market. The European Union Deforestation Regulation is pushing feed manufacturers to build more traceable soy sourcing systems before the December 30, 2026, deadline. Africa and the Middle East show stronger room for expansion because poultry remains a practical protein source in markets with fast population growth and changing food demand patterns. Hotter climate conditions also make functional and heat-support feed solutions more relevant in these regions, especially where flock performance is exposed to sustained temperature stress. As a result, the broiler feed market exhibits distinct regional priorities, with Asia-Pacific emphasizing production scale, Europe focusing on regulatory compliance, and Africa and the Middle East prioritizing market access, supply chain resilience, and industry formalization.

- New Hope Liuhe Co., Ltd.

- Charoen Pokphand Foods Public Company Limited

- Cargill, Incorporated

- Archer Daniels Midland Company

- Land O'Lakes, Inc.

- Koninklijke De Heus Voeders B.V.

- Guangdong Haid Group Co., Ltd.

- Nutreco N.V.

- Japfa Ltd.

- Wen's Foodstuff Group Co., Ltd.

- AB Agri Limited

- ForFarmers N.V.

- Cooperatie Koninklijke Agrifirm U.A.

- Godrej Agrovet Limited

- Suguna Foods Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising poultry meat consumption and protein affordability

- 4.2.2 Commercial broiler farming expansion and feed outsourcing

- 4.2.3 Higher focus on feed conversion and cost efficiency

- 4.2.4 Shift toward antibiotic-free and additive-led feed programs

- 4.2.5 AI-enabled precision nutrition in broiler feed formulation

- 4.2.6 Heat-stress mitigation demand for functional feed

- 4.3 Market Restraints

- 4.3.1 Corn and soybean meal price volatility

- 4.3.2 Tighter antimicrobial-use regulation

- 4.3.3 European Union Deforestation Regulation(EUDR)-linked soy traceability premiums

- 4.3.4 Climate-driven mycotoxin and ingredient-quality risk

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Feed Phase

- 5.1.1 Starter

- 5.1.2 Grower

- 5.1.3 Finisher

- 5.2 By Form

- 5.2.1 Pellets

- 5.2.2 Crumbles

- 5.2.3 Mash

- 5.2.4 Others

- 5.3 By Ingredient Type

- 5.3.1 Cereals

- 5.3.2 Oilseed Meal

- 5.3.3 Molasses

- 5.3.4 Fish Oil and Fish Meal

- 5.3.5 Additives

- 5.3.6 Other Ingredient Types

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Indonesia

- 5.4.4.6 Thailand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 New Hope Liuhe Co., Ltd.

- 6.4.2 Charoen Pokphand Foods Public Company Limited

- 6.4.3 Cargill, Incorporated

- 6.4.4 Archer Daniels Midland Company

- 6.4.5 Land O'Lakes, Inc.

- 6.4.6 Koninklijke De Heus Voeders B.V.

- 6.4.7 Guangdong Haid Group Co., Ltd.

- 6.4.8 Nutreco N.V.

- 6.4.9 Japfa Ltd.

- 6.4.10 Wen's Foodstuff Group Co., Ltd.

- 6.4.11 AB Agri Limited

- 6.4.12 ForFarmers N.V.

- 6.4.13 Cooperatie Koninklijke Agrifirm U.A.

- 6.4.14 Godrej Agrovet Limited

- 6.4.15 Suguna Foods Private Limited