|

시장보고서

상품코드

2072919

미국의 손 보호장비 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Hand Protection Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

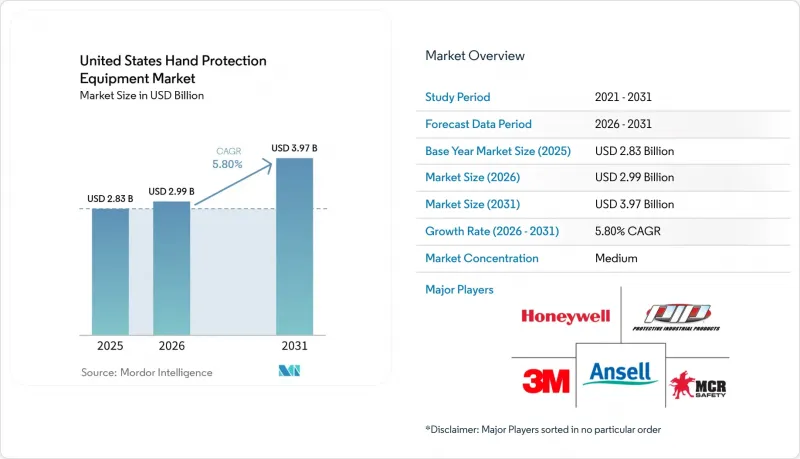

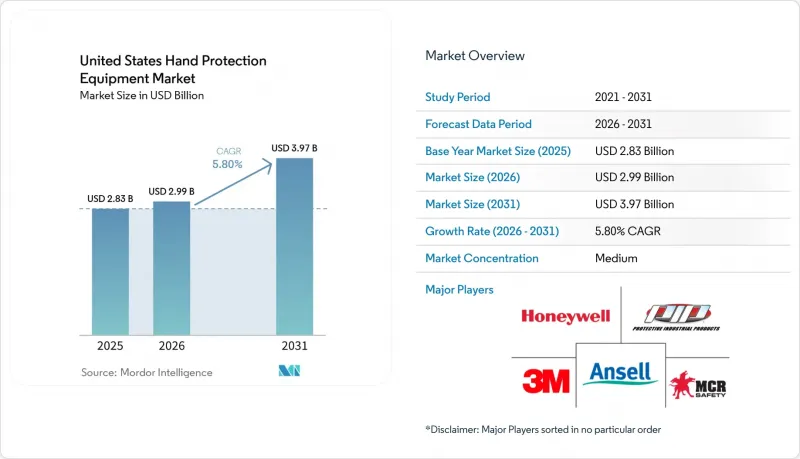

Mordor Intelligence에 의하면, 미국의 손 보호장비 시장 규모는 2025년에 28억 3,000만 달러로 평가되었고 2026년 29억 9,000만 달러에서 2031년까지 39억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.8%를 나타낼 전망입니다.

본 보고서는 제품 유형(일회용 장갑, 재사용 가능 장갑), 원재료(천연 고무·라텍스, 니트릴, 네오프렌, 비닐, 고성능 폴리에틸렌, 기타 원재료) 및 최종 용도(의료 및 제약, 건설, 석유 및 가스, 식품 산업, 광업, 기타 최종 용도)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 손 보호장비 시장 동향과 인사이트

산업 및 의료 분야의 각 업무 프로세스에서 OSHA가 주도하는 PPE 규정 준수

미국의 손 보호장비 시장에서 규제 준수는 수요를 지탱하는 가장 견고한 기둥이 되고 있습니다. 2024년 12월, OSHA는 29 CFR 1926.95의 개정안을 발표하고, 건설업 고용주에게 각 근로자에게 장갑을 포함한 적절하게 맞는 개인보호장비(PPE)를 제공하도록 의무화했습니다. 2025년 1월 이 규정 개정에 따라, 고용주들이 제한된 재고 구성에서 벗어나 더 폭넓은 사이즈 라인업을 추구하게 되면서 교환 수요가 증가하고 있습니다. 이러한 변화는 조달 과정을 복잡하게 만들고 있으며, 대부분의 경우 재고 규모가 더 큰 대형 유통업체나 평판이 좋은 브랜드에 이익이 되고 있습니다. 의료 분야에서는 CMS가 2025년 4월 28일, "강화된 차단 예방 조치(Enhanced Barrier Precautions)" 적용 범위를 확대하여, 만성 상처나 삽입형 의료기기를 착용한 요양 시설 입소자의 간호 시 장갑 사용 시나리오를 더욱 구체화했습니다. 이러한 규제 변경은 종합적으로 볼 때 미국 개인 보호장비 시장의 지속적인 수요를 뒷받침하고 있으며, 장갑 착용이 더 이상 단순한 선택 사항이 아니라 의무화된 관행이 되었음을 여실히 보여주고 있습니다.

라텍스 프리 및 내화학성 니트릴로의 전환이 진행되고 있습니다.

의료, 연구소, 식품 취급 및 화학 물질을 많이 사용하는 산업 전반에 걸쳐, 미국의 손 보호장비 시장은 점점 더 니트릴 제품으로 전환되고 있습니다. 2025년 1월 1일부터 미국 무역대표부(USTR)의 관세표에 따라 중국산 의료용 니트릴 장갑에 대한 관세가 50%로 인상되며, 2026년 1월 1일에는 100%로 추가 인상될 예정입니다. 이러한 대대적인 정책 전환으로 인해 미국으로 수입되는 중국산 제품의 도착 비용이 변동되었습니다. 그 결과, 수입업체나 기관 구매 담당자들은 조달처의 다각화를 모색하게 되었으며, 말레이시아, 베트남, 인도 및 일부 국내 생산 능력에 주목하고 있습니다. 니트릴의 매력은 라텍스가 함유되어 있지 않다는 점, 내천자성이 향상되었다는 점, 그리고 뛰어난 화학적 호환성에 있으므로, 까다로운 사용 조건이 요구되는 용도에 가장 적합합니다. 병원 및 연구소의 사양에서는 항암제 내성과 관련된 ASTM D6978 등의 성능 기준이 점점 더 중요시되면서, 미국 손 보호장비 시장에서 프리미엄화 추세가 가속화되고 있습니다.

자동화와 AI 덕분에 일부 산업 업무에서 수작업에 대한 의존도가 낮아졌습니다.

미국의 손 보호장비 시장 일부, 특히 수작업이 체계적으로 배제되고 있는 산업 분야에서는 자동화의 영향이 뚜렷하게 나타나고 있습니다. 2025년, 북미의 로봇 수주량은 6.6% 증가했으며, 이는 자동 조립, 이송, 검사가 자동차 부문뿐만 아니라 더 광범위한 제조 분야로 확대되고 있음을 보여줍니다. 제약 제조 분야에서는 무균 충전 및 마무리 공정 등에서 수작업이나 장갑 사용에 대한 의존도를 최소화하기 위해, 배리어 기술 및 자동화 시스템으로의 전환이 진행되고 있습니다. 이러한 변화는 의료 및 푸드서비스 분야의 장갑 수요를 크게 억제하는 것은 아니지만, 특정 프리미엄 산업 부문 수요 성장세를 둔화시키고 있습니다. 그 영향은 갑작스럽게 나타나기보다는 서서히 나타나고 있지만, 미국 손 보호장비 시장의 특정 부문에서는 판매량 증가에 사실상 상한선이 설정되어 있습니다. 그 결과, 견실한 산업용 제품 포트폴리오를 보유한 기업들에게는 판매량 예측을 고부가가치 혁신 추진 및 교체 수요에 대한 집중과 조화시키는 것이 필수적입니다.

부문별 분석

2025년, 일회용 장갑은 미국 손 보호장비 시장을 휩쓸며 58.1%의 점유율을 차지해 다른 부문을 압도적으로 앞질렀습니다. 이러한 보급은 의료, 식품 가공, 청소 등 다양한 분야에 걸쳐 있으며, 오염을 억제하기 위한 일회용 관행에 대한 지속적인 수요를 여실히 보여주고 있습니다. 이 부문의 호황을 여실히 보여주듯, 2025년 첫 7개월 동안만 해도 미국의 일회용 장갑 수입량은 무려 441억 개에 달했습니다. 특히 식품 관련 및 의료 분야에서 구매자들이 일관된 품질을 중요시하기 때문에 엄격한 제품 기준과 규정 준수 요건이 이 부문을 뒷받침하고 있습니다. 그러나 이 부문은 많은 프리미엄 카테고리에 비해 조달 측면에서 상품화가 진행되고 있습니다. 이러한 추세는 판매량 증가로 이어지지만, 부가가치 창출을 복잡하게 만들며, 공급업체들은 착용감, 안정적인 성능, 혹은 확실한 공급과 같은 요소를 통해 차별화를 꾀할 수밖에 없게 되었습니다.

재사용 가능한 장갑은 미국 손 보호장비 시장에서 가장 빠르게 성장하는 부문으로 부상하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.8%를 나타낼 것으로 전망됩니다. 가장 두드러진 성장이 나타나는 분야는 화학물질 취급, 건설, 광업, 중공업 등 구매자가 장갑의 단가보다 비용을 우선시하는 분야입니다. 이러한 분야에서는 장갑의 수명, 절단 저항성 및 내화학성이 최우선으로 고려됩니다. 또한, 재사용 가능한 장갑과 지속가능성을 연결하는 뚜렷한 추세가 나타나고 있으며, 기관들은 제품 수명 주기 전반에 걸쳐 환경 부하를 줄이고 확실한 환경 실적을 자랑하는 제품을 점점 더 선호하고 있습니다. 2025년 『Antimicrobial Resistance &Infection Control』지에 게재된 기사에서는 장갑 사용을 최적화함으로써 얻을 수 있는 두 가지 이점, 즉 환자의 안전을 강화하는 동시에 의료비를 관리할 수 있다는 점이 강조되었습니다. 재사용 가능한 장갑은 아직 일회용 장갑을 능가하지는 못하지만, 미국의 손 보호장비 시장에서 프리미엄 제품의 매출 점유율을 점차 확대되고 있습니다. 이러한 추세로 인해, 입지를 굳힌 전문 공급업체들은 대량 생산되는 범용 제품 라인에 크게 의존하고 있는 기업들보다 유리한 입장에 서 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states protection equipment market size was valued at USD 2.83 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 3.97 billion by 2031, at a CAGR of 5.8% during the forecast period (2026-2031).

This report is Segmented by Product Type (Disposable Gloves, Reusable Gloves), Raw Material (Natural Rubber and Latex, Nitrile, Neoprene, Vinyl, High-Performance Polyethylene, Other Raw Materials), and End Use (Healthcare and Pharmaceuticals, Construction, Oil and Gas, Food Industry, Mining, Other End Uses). The Market Forecasts are Provided in Terms of Value (USD).

United States Hand Protection Equipment Market Trends and Insights

OSHA-Driven PPE Compliance Across Industrial and Healthcare Workflows

In the U.S. protection equipment market, regulatory compliance stands as the most steadfast pillar of demand. In December 2024, OSHA rolled out revisions to 29 CFR 1926.95, mandating that construction employers provide each worker with properly fitting PPE, including gloves. This January 2025 rule change amplifies replacement demand, as employers now seek a broader size range, moving away from a limited stock profile. The shift complicates procurement, often benefiting larger distributors and established brands with more extensive inventories. In the healthcare sector, CMS, on April 28, 2025, broadened the Enhanced Barrier Precautions, specifying more scenarios for glove use when caring for nursing home residents with chronic wounds or indwelling devices. Collectively, these regulatory shifts bolster the recurring demand in the U.S. protection equipment market, underscoring that glove usage is now a mandated practice, not just an optional purchase.

Rising Shift Toward Latex-Free and Chemical-Resistant Nitrile Adoption

Across healthcare, laboratories, food handling, and chemical-intensive industries, the U.S. market for protective equipment is increasingly leaning towards nitrile. Starting January 1, 2025, the USTR tariff schedule hiked duties on Chinese medical-grade nitrile gloves to 50%, with a further increase to 100% set for January 1, 2026. This significant policy shift altered the landed cost of Chinese supplies entering the U.S. As a result, importers and institutional buyers are now more inclined to diversify their sources, turning to Malaysia, Vietnam, India, and select domestic capacities. Nitrile's appeal lies in its latex-free nature, enhanced puncture resistance, and superior chemical compatibility, making it ideal for demanding applications. Specifications in hospitals and laboratories are increasingly prioritizing performance standards, such as ASTM D6978 for chemotherapy-drug resistance, driving a trend of premiumization in the U.S. protective equipment market.

Automation and AI Lowering Manual-Hand Exposure in Some Industrial Tasks

Parts of the U.S. protection equipment market are feeling the pinch of automation, particularly in industrial workflows where manual touch is being systematically eliminated. In 2025, North American robot orders climbed by 6.6%, underscoring the shift of automated assembly, handling, and inspection from just the automotive sector to a wider array of manufacturing applications. In the realm of pharmaceutical manufacturing, operations such as sterile fill-finish are turning to barrier technologies and automated systems to minimize reliance on manual, glove-dependent tasks. While this shift doesn't significantly dampen demand for gloves in healthcare or food services, it does temper demand intensity in select premium industrial sectors. The impact unfolds gradually, not suddenly, but it effectively caps volume growth in certain segments of the U.S. protection equipment market. As a result, companies boasting robust industrial portfolios are finding it essential to align their volume expectations with a push towards higher-value innovations and a focus on replacement demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing Workplace Injury Prevention Spending in High-Hazard Industries

- Aging Workforce and Higher Safety Protocol Intensity in Healthcare and Manufacturing

- Volatility in Nitrile, Latex, and Polymer Feedstock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, disposable gloves dominated the U.S. protection equipment market, commanding a 58.1% share, clearly outpacing other segments. Their widespread adoption spans healthcare, food processing, and cleaning sectors, underscoring the ongoing need for single-use practices to control contamination. Highlighting the segment's vitality, U.S. imports of disposable gloves reached a staggering 44.1 billion units in the first seven months of 2025 alone. Stringent product standards and compliance regulations anchor this segment, as buyers prioritize consistent quality, especially for food-related and medical applications. However, this segment grapples with greater commoditization in procurement than many premium categories. While this dynamic boosts volume, it complicates value creation, pushing suppliers to stand out through factors like fit, consistent performance, or reliable supply.

Reusable gloves are emerging as the fastest-growing segment of the U.S. protective equipment market, with projections indicating an 8.8% CAGR from 2026 to 2031. The strongest growth is observed in sectors where buyers prioritize cost over the glove's unit price, such as chemical handling, construction, mining, and heavy industry. Here, glove lifespan, cut resistance, and chemical resilience take precedence. Furthermore, there's a notable trend linking reusable gloves to sustainability, with institutions increasingly favoring products that boast reduced lifecycle impacts and robust environmental credentials. A 2025 piece in Antimicrobial Resistance & Infection Control highlighted the dual benefits of optimizing glove use: bolstering patient safety while managing healthcare costs. While reusable gloves aren't yet overshadowing disposables, they're carving out a larger share of premium revenue in the U.S. protective equipment market. This trend positions established specialty suppliers more favorably than those leaning heavily on high-volume commodity lines.

Complete Report Scope:

- By Product Type

- Disposable Gloves

- Reusable Gloves

- By Raw Material

- Natural Rubber and Latex

- Nitrile Gloves

- Neoprene

- Vinyl

- High-Performance Polyethylene

- Other Raw Materials

- By End Use

- Healthcare and Pharmaceuticals

- Construction

- Oil and Gas

- Food Industry

- Mining

- Other End Uses

List of Companies Covered in this Report:

- Ansell Limited

- Honeywell International Inc.

- 3M

- Protective Industrial Products, Inc.

- MCR Safety

- Superior Glove Works Ltd.

- SHOWA Group

- Top Glove Corporation Bhd

- Hartalega Holdings Berhad

- Kimberly-Clark Corporation

- Medline Industries, LP

- Cardinal Health, Inc.

- W. W. Grainger, Inc.

- Delta Plus Group

- The Glove Company

- United Glove, Inc.

- Lakeland Industries, Inc.

- Carolina Glove Company

- Magid Glove and Safety Manufacturing Company LLC

- Radians, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OSHA-driven PPE compliance across industrial and healthcare workflows

- 4.2.2 Rising shift toward latex-free and chemical-resistant nitrile adoption

- 4.2.3 Growing workplace injury prevention spending in high-hazard industries

- 4.2.4 Aging workforce and higher safety protocol intensity in healthcare and manufacturing

- 4.2.5 Sensor-enabled and smart glove adoption for human-machine interaction

- 4.2.6 Sustainability pressure on single-use glove materials and waste handling

- 4.3 Market Restraints

- 4.3.1 Automation and AI lowering manual-hand exposure in some industrial tasks

- 4.3.2 Volatility in nitrile, latex, and polymer feedstock costs

- 4.3.3 Certification delays for novel materials and performance claims

- 4.3.4 Procurement price pressure and commoditization in standard disposable gloves

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Disposable Gloves

- 5.1.2 Reusable Gloves

- 5.2 By Raw Material

- 5.2.1 Natural Rubber and Latex

- 5.2.2 Nitrile Gloves

- 5.2.3 Neoprene

- 5.2.4 Vinyl

- 5.2.5 High-Performance Polyethylene

- 5.2.6 Other Raw Materials

- 5.3 By End Use

- 5.3.1 Healthcare and Pharmaceuticals

- 5.3.2 Construction

- 5.3.3 Oil and Gas

- 5.3.4 Food Industry

- 5.3.5 Mining

- 5.3.6 Other End Uses

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ansell Limited

- 6.4.2 Honeywell International Inc.

- 6.4.3 3M

- 6.4.4 Protective Industrial Products, Inc.

- 6.4.5 MCR Safety

- 6.4.6 Superior Glove Works Ltd.

- 6.4.7 SHOWA Group

- 6.4.8 Top Glove Corporation Bhd

- 6.4.9 Hartalega Holdings Berhad

- 6.4.10 Kimberly-Clark Corporation

- 6.4.11 Medline Industries, LP

- 6.4.12 Cardinal Health, Inc.

- 6.4.13 W. W. Grainger, Inc.

- 6.4.14 Delta Plus Group

- 6.4.15 The Glove Company

- 6.4.16 United Glove, Inc.

- 6.4.17 Lakeland Industries, Inc.

- 6.4.18 Carolina Glove Company

- 6.4.19 Magid Glove and Safety Manufacturing Company LLC

- 6.4.20 Radians, Inc.