|

시장보고서

상품코드

2072930

의료용 이동 보조 장치 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Mobility Aids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

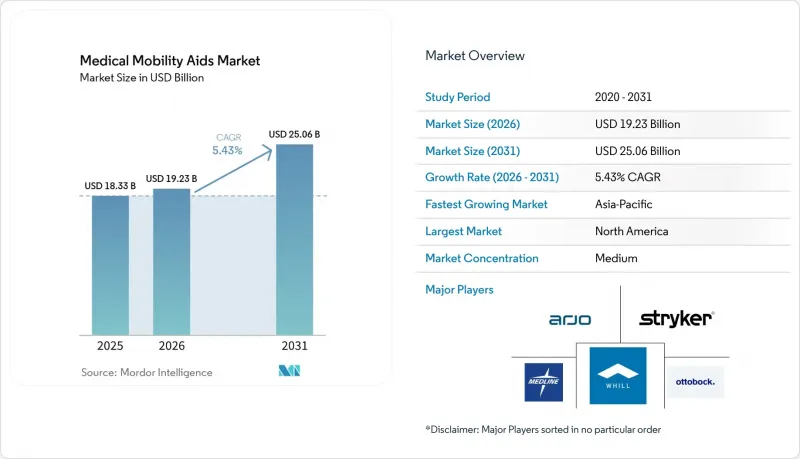

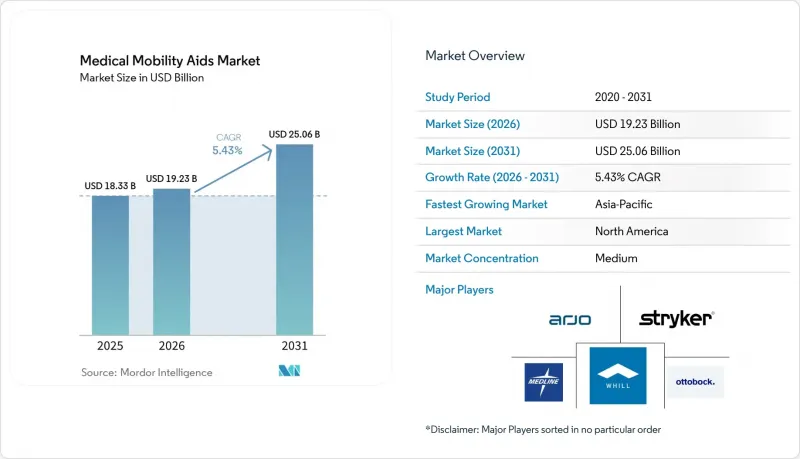

Mordor Intelligence에 의하면, 의료용 이동 보조 장치 시장 규모는 2025년에 183억 3,000만 달러로 평가되었고, 2026년에 192억 3,000만 달러로 추정되고, 2031년까지 250억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR5.43%로 성장할 전망입니다.

본 보고서는 제품 유형별(휠체어, 보행기, 스쿠터, 목발, 환자 리프트, 의지, 기타), 기술별(수동식, 전동식, 하이브리드식, 커넥티드 및 스마트), 최종 사용자별(재택 간호 환경 등), 유통 채널별(오프라인, 온라인, 의료용품 공급업체, 의료기관), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 의료용 이동 보조 장치 시장 동향 및 인사이트

고령화와 장기적인 이동 지원의 필요성

의료용 이동 보조기 시장은 고령 인구의 꾸준한 증가와 밀접한 관련이 있습니다. 이는 이동 능력의 저하가 수년에 걸쳐 진행되는 경우가 많으며, 일반적으로 일회성 구매가 아니라 제품의 반복적인 사용, 교체, 조정 및 유지보수가 필요하기 때문입니다. 2030년까지 전 세계 인구의 6명 중 1명이 60세 이상이 될 것이며, 80세 이상 인구는 2050년까지 계속해서 급증할 것으로 예측됩니다. 이로 인해 이동 지원 제품에 대한 수요 기반은 더욱 광범위하고 지속 가능한 것으로 자리 잡을 것입니다. 평균 수명의 연장은 수요의 경제적 측면에도 변화를 가져옵니다. 사용자가 더 오랜 기간 동안 활동적인 상태를 유지하는 반면, 고가 기기는 누적된 마모에 노출되기 때문에 실질적인 교체 주기가 단축되고, 애프터마켓의 수익 잠재력이 높아질 가능성이 있기 때문입니다. 일본의 돌봄 접근 방식은 지자체 급여 제도와 고령자의 이동 지원을 연계하고 있다는 점에서 두드러지며, 장기간에 걸친 지원 기간 동안 증가하는 돌봄 수요에 대응하고자 하는 다른 고령화 사회들에게 주목할 만한 모델이 되고 있습니다. 업그레이드가 가능한 부품, 조절 가능한 좌석, 유지보수가 용이한 프레임을 갖춘 모듈식 제품을 설계하는 제조업체는 초기 판매에만 의존하지 않고, 장기적인 사용자 관계를 통해 더 많은 가치를 창출할 수 있으므로 의료용 이동 보조 장치 시장에서 유리한 입지를 차지하고 있습니다.

만성 질환 및 급성기 이후 재활 수요 증가

의료용 이동 보조기 시장은 기능적 제한이 있는 사람이나 재활이 필요한 사람들 증가, 그리고 병원이나 급성기 의료시설에서 퇴원한 후에도 계속되는 회복 과정에 힘입어 성장하고 있습니다. 『BMC Geriatrics』에 게재된 2025년 메타분석에 따르면, 전 세계 고령자의 기본 일상생활 활동(ADL) 장애 통합 유병률은 26.07%인 반면, 도구적 일상생활 활동(IDL) 장애는 45.15%에 달하며, 이는 고령화 사회에서 이동 지원 솔루션에 대한 지속적인 수요가 있음을 시사합니다. 또한, OECD 보고서에 따르면, 24개 OECD 회원국에서 저소득층 노인들 사이에서 자신의 건강 상태를 '나쁨' 또는 '매우 나쁨'이라고 평가하는 비율이 여전히 현저히 높은 것으로 나타나고 있으며, 이는 이동 지원 및 재활 서비스 이용에 대한 수요가 지역에 따라 편차는 있지만 여전히 뿌리 깊게 존재하고 있음을 뒷받침하고 있습니다. 입원 기간이 단축됨에 따라, 이동 지원에 대한 수요의 상당 부분이 급성기 이후의 돌봄 환경으로 옮겨가고 있습니다. 이는 의료기기의 처방 사례가 시설 내에서 장기간 치료를 받는 것이 아니라, 재활센터, 장기 요양 시설 및 재택으로의 퇴원 과정에서 점점 더 많이 발생하고 있음을 의미합니다. 이러한 변화는 의료용 이동 보조 장치 시장에서 재활 수요를 확대되고 있습니다. 왜냐하면, 임상적으로 적합한 장비, 서류 작성 지원 및 신속한 납품을 제공할 수 있는 공급업체는 회복을 목적으로 한 조달이 이루어지는 현장에 더 가까이 위치해 있기 때문입니다.

고급형 및 전동 기기의 고액 본인 부담금

의료용 이동 보조 장치 시장은 여전히 심각한 경제적 장벽에 직면해 있습니다. 많은 국가에서 첨단 전동 휠체어, 스마트 기기 및 복잡한 재활 기술은 여전히 가구 소득에 비해 가격이 비싸며, 보험 환급 제도가 있더라도 그 비용의 일부만 지원되는 경우가 많기 때문입니다. 기본 보장 범위와 프리미엄 기능의 가격 차이 문제는 특히 중요한 사안입니다. 많은 사용자는 기능적인 기본 모델은 이용할 수 있지만, 고급 제어 기능, 스마트 기능, 혹은 고성능 부품에 대해서는 구매 시 본인 부담으로 지불해야 하기 때문입니다. 독일에서는 승인된 기기 수준에서 보다 유리한 이용 체계가 마련되어 있습니다. 이는 법정 보험 가입자가 지정된 보조 기구에 대해 제한된 본인 부담금만 지불하기 때문이지만, 그럼에도 불구하고 보험 적용 대상인 필수 기능과 옵션인 프리미엄 사양 간의 구분은 최종 사용자에게 여전히 중요한 문제로 남아 있습니다. 아시아태평양이나 남미의 저소득 지역에서는 그 부담이 각 가구에 직접적으로 전가되기 때문에 기능적인 측면에서는 전동식이 더 적합하더라도 저비용의 수동식 기기가 구매되는 경향이 있습니다. 이로 인해 판매량은 유지되지만, 의료용 이동 보조 장치 시장 전체의 제품 구성이 개선되는 데에는 한계가 있어, 단계적인 제품 라인업, 보다 간소화된 자금 조달 옵션, 혹은 핵심 기능을 기반으로 한 저비용 제품을 제공하는 공급업체에게 우위가 생기고 있습니다.

부문별 분석

2025년, 휠체어는 의료용 이동 보조 기구 시장 점유율의 41.73%를 차지했으며, 이러한 위상은 병원, 재활 시설, 장기 요양 시설 및 가정 내 일상적인 이동 수요 등 다양한 상황에서 활용될 수 있는 적응성을 반영한 것입니다. 또한, 이러한 우위는 확립된 상환 절차와 익숙한 처방 절차에 기인하며, 이는 새로운 카테고리나 라이프스타일 지향형 기기와 비교했을 때 임상의, 보험사 및 공급업체가 직면하는 장벽을 낮추고 있습니다. 모빌리티 스쿠터 시장은 2031년까지 연평균 6.76%의 성장률이 예상되며, 이러한 성장 요인은 의료적 필요성과 소비자의 편의성 사이에서 균형을 이루고 있다는 점에 있습니다. 특히, 복잡한 의료기기로 완전히 전환하지 않고도 지역 사회 내 이동성을 높이고자 하는 고령 사용자에게는 그 장점이 두드러집니다. 따라서 의료용 이동 보조기 업계에서는 제품 유형별로 뚜렷한 양극화가 나타나고 있습니다. 휠체어는 폭넓은 임상 분야에서 계속해서 표준적인 해결책으로 자리 잡고 있는 반면, 스쿠터는 '익숙한 곳에서 노후를 보내다'라는 경향과 표준 사양으로 구하기 쉬운 점 덕분에 더욱 급속한 성장을 이루고 있기 때문입니다.

보행기나 롤러터는 이동 능력 저하의 초기 단계, 수술 후 회복기, 심장 재활, 그리고 외래 진료 및 재택 간호 과정에서 공통적으로 나타나는 일반적인 지원 요구에 적합하기 때문에 꾸준한 수요를 유지하고 있습니다. 환자용 리프트나 이송 보조 기구 역시 장기 요양 및 시설 환경에서 그 중요성이 커지고 있습니다. 이러한 환경에서는 인력 부족, 간병인의 부담, 안전상의 우려로 인해 일상 업무에서 이동 지원 솔루션의 필요성이 높아지고 있기 때문입니다. 의지·보조기를 활용한 이동 지원 솔루션은 여전히 제품군 중에서도 보다 전문적이고 프리미엄한 분야이며, 그 성장 양상은 표준적인 기계식 보조기에 비해 혁신 주기가 짧고, 임상적 복잡성이 높으며, 이익률 구조가 더욱 차별화되어 있다는 점에 의해 형성되고 있습니다. 목발, 지팡이, 기타 보행 보조 기구는 여전히 많은 사용자층에게 이용되고 있지만, 가격 및 판매량 측면에서 압박을 받고 있으며, 가치를 유지하기 위해서는 핵심 기능을 대폭 변경하기보다는 인체공학에 기반한 개선, 경량 소재의 채택, 그리고 사용 편의성 향상에 의존하는 경향이 강해지고 있습니다.

2025년에는 수동식 기기가 시장의 50.32%를 차지했으며, 이러한 규모는 저렴한 구입 비용, 보험 환급 제도에 대한 폭넓은 이해, 간편한 유지보수, 그리고 반드시 전동 보조 기능을 필요로 하지 않는 이동 수요를 가진 대규모 사용자층을 반영한 것입니다. 전동 기기는 2031년까지 연평균 7.88%의 성장률을 보일 것으로 예상되며, 배터리 비용의 하락, 모터의 소형화, 그리고 재활 현장에서 전동 기기의 성과와 일상적인 사용 편의성에 대한 신뢰도가 높아짐에 따라 가장 빠르게 성장하고 있는 기술 분야로 자리매김하고 있습니다. 이로 인해 의료용 이동 보조기 시장 내에서는 서로 다른 이익률 구조가 형성되고 있습니다. 판매량은 여전히 수동 제품이 주를 이루고 있는 반면, 가치 증가세가 빠른 것은 전동식 및 기능이 강화된 이동 플랫폼이기 때문입니다. 따라서 의료용 이동 보조기 업계는 수동식에서 전동식으로 단숨에 전환되고 있는 것은 아닙니다. 이러한 전환은 보험 환급, 이용자의 능력, 가정 내 사용 적합성, 유지보수 요건 등의 요소가 동시에 작용하여 이루어지기 때문입니다.

하이브리드형 및 파워 어시스트형 제품은 이러한 전환 과정에서 중요한 중간층을 형성하고 있습니다. 이는 수동식 기기의 형태와 무게에 대한 기대치, 그리고 보험 보상 관행과의 유사성을 유지하면서도 사용자에게 전동식의 장점을 어느 정도 제공할 수 있기 때문입니다. 파모빌의 'SmartDrive MX2+'는 그러한 가교 역할의 한 예로, 추진력을 최대 80%까지 줄임으로써 기존의 전동식 기기 범주로 완전히 전환하지 않고도 보조 기능이 탑재된 이동 수단이 어떻게 확대될 수 있는지를 보여주고 있습니다. 커넥티드 및 스마트 보조 기기는 현재 시장 점유율이 아직 낮긴 하지만, 원격 모니터링, 예측 유지보수, 간병인과의 연계, 그리고 장기적인 데이터를 기반으로 한 차별화를 지원할 수 있기 때문에 전략적으로 중요한 위치를 차지하고 있습니다. 가장 큰 제약 요인은 하드웨어 준비 상황뿐만 아니라, 이동 지원 기기와 의료 기록 및 의료 제공업체 시스템 간의 통합이 불충분하다는 점에도 있습니다. 즉, 데이터 기능의 상업적 가치는 예측 기간 전반에 걸쳐 상호 운용성을 강화하고 실증 자료를 창출하는 데 달려 있다고 할 수 있습니다.

지역별 분석

2025년, 북미는 의료용 이동 보조 장치 시장 규모의 38.41%를 차지했으며, 이에 따라 성숙한 보험 급여 환경, 견고한 내구성 의료장비 인프라, 그리고 처방전 및 서류 작성 워크플로우를 지원할 수 있는 인증 공급업체의 대규모 도입 기반이 형성되었습니다. 또한, 보조 기기에 대한 높은 인지도, 프리미엄 기기의 높은 보급률, 그리고 많은 개발도상국 시장에 비해 가정 내 사용이나 시설에서의 조달을 위한 길이 폭넓게 열려 있다는 점도 이 지역의 경쟁 우위를 뒷받침하고 있습니다. 캐나다에서는 주 정부 차원의 보조 기기 지원 및 민간 보험사의 참여를 통해 지역 수요가 더욱 확대되고 있지만, 주마다 급여 범위가 달라 제품의 접근성 및 품목 구성에 여전히 영향을 미치고 있습니다. 이 지역에서는 소비자가 다양한 선택지를 쉽게 비교할 수 있고, 표준 모델을 보다 직접적으로 구매할 수 있으며, 또한 고도의 의료적 요구가 수반되는 복잡한 임상 조달 절차를 거치지 않고도 지역 사회나 주거 환경에서 이동용 스쿠터를 이용할 수 있기 때문에 해당 제품은 유리한 입지에 있다고 볼 수 있습니다.

유럽은 여전히 2위 지역 시장이며, 그 구조는 각국마다 다른 상환 제도에 의해 특징지어집니다. 이는 진입 장벽이 되는 한편, 규제 대응 및 판로 구축 능력이 뛰어난 기업에게는 분명한 기회도 창출하고 있습니다. 독일은 이러한 추세에서 중심적인 역할을 하고 있습니다. 해당 국가의 법적 체계에서는 승인된 이동 보조 기기가 인증된 공급 경로나 지정 제품을 통해 제공되므로, 대상 이용자의 접근성을 확보하는 동시에, 보험 급여 중심의 구매를 인증된 공급자와 밀접하게 연계하는 구조로 되어 있습니다. 이러한 구조는 보험 적용 대상 제품의 고부가가치 판매를 뒷받침하고 있지만, 한편으로는 온라인 직접 판매 모델이 보험 적용 범주에 어느 정도까지 침투할 수 있는지를 제한하는 요인이 되기도 합니다. 또한, 제조업체나 대형 그룹들이 피팅, 서비스, 서류 작성을 보다 적절하게 관리하기 위해 현지 유통 자산을 인수하거나 통합하고 있기 때문에 유통 경로의 통합에 따라 지역 간 경쟁 환경도 재편되고 있습니다. 따라서 유럽의 의료용 이동 보조 장치 시장은 매력적이면서도 동시에 치열한 시장이기도 합니다. 왜냐하면 상업적 성공은 제품의 품질뿐만 아니라, 보험 환급 제도의 적절한 활용, 유통업체와의 관계 구축, 그리고 규정 준수의 철저한 이행에도 크게 좌우되기 때문입니다.

아시아태평양은 2031년까지 연평균 6.51%의 성장이 예상되며, 일본, 한국, 중국 및 해당 지역의 기타 지역에서 고령화가 가속화되는 한편, 공공기관 및 시설의 조달 경로가 점차 확대되고 있어 가장 빠르게 성장하는 지역 시장이 될 전망입니다. 일본에서는 표준적인 이동 보조 기구가 장기 요양 보험의 적용 대상이 된다는 점이 장점으로 작용하고 있으며, 이를 통해 기본적인 수요가 뒷받침되고 있습니다. 다만, 고급형 스마트 기기는 대개 일반 보험 적용 대상에서 제외되는 경우가 많아, 별도로 본인 부담금을 지불하는 프리미엄 계층을 형성하고 있습니다. 한국도 국민건강보험 제도를 통해 기본적인 이동 보조 기기를 지원하고 있으며, 한편 중국에서는 배리어프리화 추진을 통해 이동 보조 제품의 장기 이용 환경이 지속적으로 강화되고 있습니다. 인도 및 동남아시아의 중요성이 커지고 있으며, 가계의 상환 여력이 제한적이라 하더라도 공공 조달의 확대를 통해 이동 지원 기기가 보다 체계적인 구매 환경에 임베디드될 가능성이 있기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the medical mobility aids market size is projected to be USD 18.33 billion in 2025, USD 19.23 billion in 2026, and reach USD 25.06 billion by 2031, growing at a CAGR of 5.43% from 2026 to 2031.

This report is Segmented by Product Type (Wheelchairs, Walkers, Scooters, Crutches, Patient Lifts, Prosthetics, Other), Technology (Manual, Powered, Hybrid, Connected and Smart), End User (Home Care Settings, and More), Distribution Channel (Offline, Online, Medical Suppliers, Institutional), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Value (USD).

Global Medical Mobility Aids Market Trends and Insights

Aging Population and Longer Mobility Support Horizons

The medical mobility aids market is closely tied to the steady increase in the elderly population, because mobility decline often extends over many years and usually requires repeated product use, replacement, adjustment, and servicing rather than a one-time purchase. By 2030, 1 in 6 people worldwide will be aged 60 or older, and the number of people aged 80 and above is expected to keep rising sharply through 2050, which supports a broader and more durable demand base for mobility support products. Longer life expectancy also changes the economics of demand, because users remain active for longer periods and premium devices face more cumulative wear, which can shorten practical replacement cycles and lift aftermarket revenue potential. Japan's long-term care approach continues to stand out because it links municipal coverage to elderly mobility support, and that makes it a visible model for other aging economies that are trying to manage rising care needs over longer support periods. Manufacturers that design modular products with upgradeable parts, adaptable seating, and serviceable frames are better placed in the medical mobility aids market because they can capture more value across a long user relationship instead of relying only on first-unit sales.

Rising Chronic Disease and Post-Acute Rehabilitation Demand

The medical mobility aids market is also supported by a larger population living with functional limitations, rehabilitation needs, and recovery pathways that continue after discharge from hospitals and acute care settings. A 2025 meta-analysis in BMC Geriatrics reported a pooled prevalence of 26.07% for disability in basic daily living activities among older adults globally, while disability in instrumental daily living activities reached 45.15%, which points to a sustained need for supportive mobility solutions across aging populations. OECD reporting also showed that self-rated poor or very poor health remained much higher among older adults in lower-income groups across 24 OECD countries, and that reinforces the uneven but persistent need for mobility support and rehabilitation access. Shorter hospital stays are pushing more mobility-related needs into post-acute settings, which means device prescription events are increasingly occurring in rehabilitation centers, long-term care environments, and home discharge pathways rather than staying inside institutional care for longer periods. That shift strengthens rehabilitation demand inside the Medical Mobility Aids Market because providers that can supply clinically suitable devices, documentation support, and faster fulfillment are positioned closer to the point where recovery-driven procurement now takes place.

High Out-of-Pocket Cost for Premium and Powered Devices

The medical mobility aids market still faces a serious affordability barrier, because advanced powered wheelchairs, smart devices, and complex rehabilitation technologies remain expensive relative to household income in many countries and are often only partly covered even where reimbursement exists. The gap between basic coverage and premium feature pricing is especially important because many users can access a functional base model while advanced controls, smart features, or higher-performance components remain self-funded at the point of sale. Germany offers a more favorable access structure at the approved device level, since statutory insurer members face only a limited co-payment for listed aids, but even there, the distinction between covered necessity and optional premium configuration remains important for end users. In lower-income parts of Asia-Pacific and South America, the burden falls much more directly on households, which pushes procurement toward lower-cost manual devices even when powered options could better match functional need. This keeps volume flowing, but it also limits product mix improvement across the medical mobility aids market and creates an advantage for suppliers that offer tiered portfolios, simpler financing options, or lower-cost products built around core functionality.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Home-Based Care and Ageing in Place

- Smart, Powered, and Connected Device Adoption

- Limited Reimbursement and Fragmented Coverage Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wheelchairs held 41.73% of the medical mobility aids market share in 2025, and that position reflected their broad fit across hospitals, rehabilitation settings, long-term care use, and daily home mobility needs. Their lead also came from established reimbursement pathways and familiar prescription routines, which lower friction for clinicians, payers, and suppliers compared with newer or more lifestyle-oriented device categories. Mobility scooters are projected to grow at 6.76% through 2031, and that growth comes from their ability to sit between medical necessity and consumer convenience, especially for older users who want more community mobility without moving fully into complex clinical devices. The medical mobility aids industry, therefore, shows a clear split inside product type, because wheelchairs remain the default solution for broad clinical use while scooters capture faster growth through aging-in-place behavior and easier access in standard configurations.

Walkers and rollators continue to hold stable demand because they fit early-stage mobility decline, post-surgical recovery, cardiac rehabilitation, and general support needs that are common across outpatient and residential care pathways. Patient lifts and transfer aids are also gaining importance in long-term care and facility settings, where labor shortages, caregiver strain, and safety concerns make assisted transfer solutions more necessary in daily operations. Prosthetics and orthotics mobility solutions remain a more specialized and premium part of the mix, and their growth pattern is shaped by shorter innovation cycles, higher clinical complexity, and more differentiated margin profiles than standard mechanical aids. Crutches, canes, and other ambulatory aids still serve large user groups, but their pricing and volume profile are under pressure, which means value retention depends more on ergonomic upgrades, lighter materials, and better usability than on major shifts in core function.

Manual devices accounted for 50.32% of the market in 2025, and that scale reflected lower acquisition cost, wider reimbursement familiarity, simpler maintenance, and a large user base whose mobility needs do not always require powered assistance. Powered devices are forecast to expand at 7.88% through 2031, which makes them the fastest-growing technology segment as battery costs ease, motors become smaller, and rehabilitation settings gain more confidence in powered outcomes and daily usability. This creates a different margin structure inside the medical mobility aids market because volume still sits with manual products, while faster value growth is moving toward powered and enhanced mobility platforms. The medical mobility aids industry is therefore not shifting in a single step from manual to powered use, because the transition is being shaped by reimbursement, user capability, home suitability, and maintenance requirements at the same time.

Hybrid and power-assist products form an important middle layer in this transition, because they give users some powered benefit while staying closer to the form, weight expectations, and reimbursement familiarity of manual devices. Permobil's SmartDrive MX2+ is an example of that bridge, since it reduces push effort by up to 80% and shows how assisted mobility can expand without requiring a full jump into traditional powered device categories. Connected and smart aids remain smaller in current share, but they carry strategic weight because they can support remote monitoring, predictive servicing, caregiver coordination, and data-based differentiation over time. The biggest limiting factor is not only hardware readiness, but also the weak integration between mobility devices and health records or provider systems, which means the commercial value of data features will depend on stronger interoperability and evidence generation across the forecast period.

Complete Report Scope:

- By Product Type

- Wheelchairs

- Walkers and Rollators

- Mobility Scooters

- Crutches and Canes

- Patient Lifts and Transfer Aids

- Prosthetics and Orthotics Mobility Solutions

- Other Medical Mobility Aids

- By Technology

- Manual

- Powered

- Hybrid and Power-Assist

- Connected and Smart Mobility Aids

- By End User

- Home Care Settings

- Hospitals and Clinics

- Rehabilitation and Long-Term Care Centers

- Other End Users

- By Distribution Channel

- Offline Retail

- Online Retail

- Medical Equipment Suppliers

- Institutional Procurement

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 38.41% of the medical mobility aids market size in 2025, and that led to a mature reimbursement environment, strong durable medical equipment infrastructure, and a large installed base of certified suppliers able to support prescription and documentation workflows. The regional position is also supported by high awareness of assistive products, stronger uptake of premium devices, and a wider pathway for home use and facility procurement than in many developing markets. Canada adds to regional demand through provincial assistive-device support and private insurance participation, though coverage differences by province still affect access and product mix. Mobility scooters appear well placed in this region because consumers can increasingly compare options, purchase standard models more directly, and use them in community and residential settings without moving through the full complexity of high-acuity clinical procurement.

Europe remained the second-largest regional market, and its structure is defined by different national reimbursement systems that create both barriers to entry and clear opportunities for companies with stronger regulatory and channel capabilities. Germany is central to this pattern because its statutory framework routes approved mobility aids through certified supply channels and listed products, which supports access for eligible users while keeping reimbursement-led purchasing closely tied to accredited providers. That structure sustains higher-value sales for covered products, but it also limits how far direct online models can extend into reimbursed categories. Regional competition is also being reshaped by channel consolidation, because manufacturers and larger groups are buying or integrating local distribution assets to gain better control over fitting, servicing, and documentation. The European picture is therefore attractive but demanding in the medical mobility aids market, since commercial success depends on reimbursement navigation, dealer relationships, and compliance discipline as much as on product quality alone.

Asia-Pacific is forecast to grow at 6.51% through 2031, making it the fastest regional market as aging accelerates in Japan, South Korea, China, and other parts of the region while procurement pathways broaden gradually across public and institutional settings. Japan benefits from long-term care coverage for standard mobility aids, and that supports baseline demand even though higher-end smart devices often sit outside routine reimbursement and create a separate premium out-of-pocket layer. South Korea also supports basic mobility devices through national insurance channels, while China's accessible infrastructure agenda continues to reinforce long-term use conditions for mobility support products. India and Southeast Asia are increasingly relevant because public procurement expansion can bring mobility aids into more structured purchase environments, even when household reimbursement remains limited.

- Arjo AB

- Benmor Medical

- Briggs Healthcare

- Drive DeVilbiss Healthcare

- Evolution Technologies Inc.

- GF Health Products, Inc.

- Golden Technologies

- Invacare

- Karma Mobility Co., Ltd.

- Louwman Group

- Medline Industries

- Nova Medical Products

- Ottobock SE and Co. KGaA

- Permobil AB

- Pride Mobility Products

- Rollz International

- Sunrise Medical

- Stryker

- WHILL, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Longer Mobility Support Horizons

- 4.2.2 Rising Chronic Disease and Post-Acute Rehabilitation Demand

- 4.2.3 Shift Toward Home-Based Care and Ageing in Place

- 4.2.4 Smart, Powered, and Connected Device Adoption

- 4.2.5 Disability Inclusion, Access Funding, and Public Procurement Support

- 4.2.6 Micro-Fit and Customization Requirements for Diverse User Physiques

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Cost for Premium and Powered Devices

- 4.3.2 Limited Reimbursement and Fragmented Coverage Rules

- 4.3.3 Repair, Maintenance, and Battery Service Burden for Powered Devices

- 4.3.4 Retail Channel Trust Gaps for High-Value Assistive Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Wheelchairs

- 5.1.2 Walkers and Rollators

- 5.1.3 Mobility Scooters

- 5.1.4 Crutches and Canes

- 5.1.5 Patient Lifts and Transfer Aids

- 5.1.6 Prosthetics and Orthotics Mobility Solutions

- 5.1.7 Other Medical Mobility Aids

- 5.2 By Technology

- 5.2.1 Manual

- 5.2.2 Powered

- 5.2.3 Hybrid and Power-Assist

- 5.2.4 Connected and Smart Mobility Aids

- 5.3 By End User

- 5.3.1 Home Care Settings

- 5.3.2 Hospitals and Clinics

- 5.3.3 Rehabilitation and Long-Term Care Centers

- 5.3.4 Other End Users

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.2 Online Retail

- 5.4.3 Medical Equipment Suppliers

- 5.4.4 Institutional Procurement

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Arjo AB

- 6.3.2 Benmor Medical Ltd.

- 6.3.3 Briggs Healthcare

- 6.3.4 Drive DeVilbiss Healthcare

- 6.3.5 Evolution Technologies Inc.

- 6.3.6 GF Health Products, Inc.

- 6.3.7 Golden Technologies

- 6.3.8 Invacare Corporation

- 6.3.9 Karma Mobility Co., Ltd.

- 6.3.10 Louwman Group

- 6.3.11 Medline Industries, LP

- 6.3.12 Nova Medical Products

- 6.3.13 Ottobock SE and Co. KGaA

- 6.3.14 Permobil AB

- 6.3.15 Pride Mobility Products Corp.

- 6.3.16 Rollz International

- 6.3.17 Sunrise Medical LLC

- 6.3.18 Stryker Corporation

- 6.3.19 WHILL, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment