|

시장보고서

상품코드

2072931

화학발광 면역측정 분석기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chemiluminescence Immunoassay Analyzer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

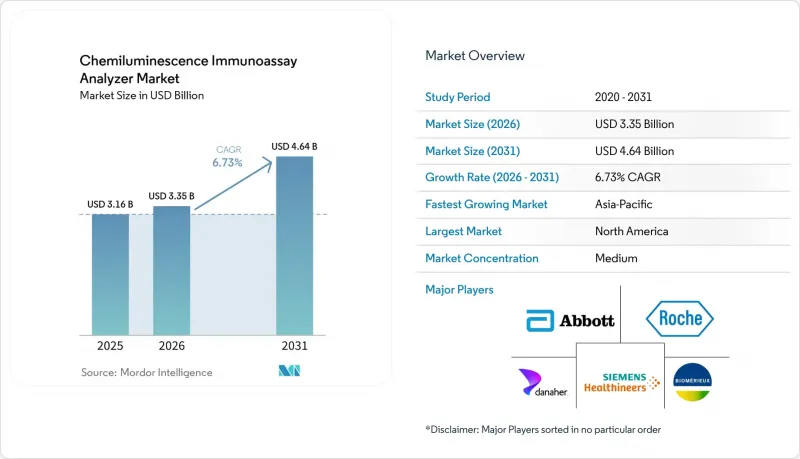

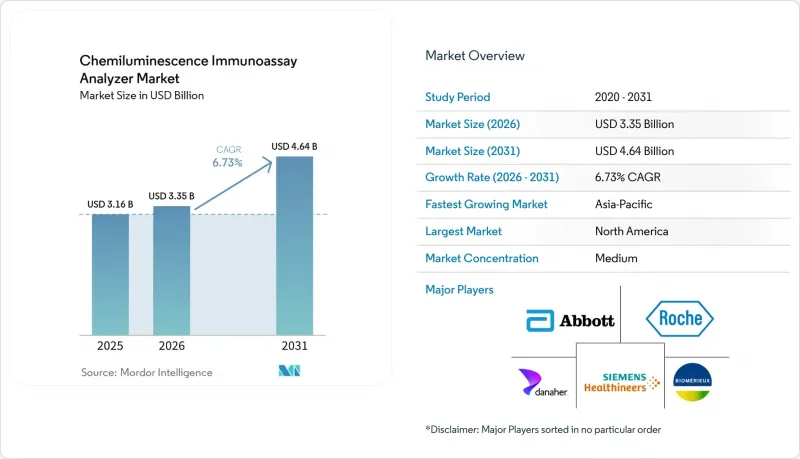

Mordor Intelligence에 의하면, 화학발광 면역측정 분석기 시장 규모는 2025년 31억 6,000만 달러, 2026년 33억 5,000만 달러에서 2031년까지 46억 4,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.73%를 나타낼 전망입니다.

본 보고서는 기술별(전기화학발광 면역 분석법 등), 처리 능력별(고속 처리 등), 검체 유형별(혈액, 혈청·혈장 등), 용도(감염병 등), 최종 사용자(병원 등), 연결성(LIS 및 HL7 통합 등), 지역(북미 등)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

전 세계 화학발광 면역측정 분석기 시장 동향 및 인사이트

고감도 바이오마커 검출에 대한 수요 증가

화학발광 면역측정 분석기 시장은 종양학, 순환기학, 내분비학 및 특정 질환의 모니터링 분야에서 극히 낮은 농도의 바이오마커를 검출해야 할 필요성으로 인해 혜택을 보고 있습니다. 임상 현장에서는 조기 발견, 반복적인 모니터링, 그리고 보다 엄격한 치료 방침 수립을 지원하는 검사로 전환되고 있으며, 이에 따라 분석 감도가 더 높은 플랫폼의 가치가 높아지고 있습니다. 『Sensors & Diagnostics』 저널의 2026년 리뷰에서는 검출 한계가 15 fg/mL에서 230 fg/mL인 8-plex 전기화학발광 시스템이 보고되었으며, 260개의 검체에 대한 급성 심근경색 바이오마커 패널에서 완벽한 임상 민감도와 특이도를 나타냈습니다. 고감도 심장 검사 프로토콜이 대규모 병원에서 응급 진료나 신속한 대응이 요구되는 현장으로 확대됨에 따라, 검사실에서는 워크플로우의 일관성을 해치지 않으면서도 이러한 분석 기준을 충족할 수 있는 분석기가 필요하게 됩니다. 발광체의 화학적 특성을 개선하고 배경 신호를 저감시키는 벤더는 향후 검사법 개발에서의 제휴 및 프리미엄 검사 메뉴 분야에서 더욱 확고한 입지를 다질 가능성이 높을 것입니다.

완전 자동화된 고처리량 검사 워크플로로 전환

화학발광 면역측정 분석기 시장은 병원 네트워크의 통합과, 직원의 개입을 최소화하면서 기기를 지속적으로 가동해야 할 필요성에 힘입어 성장하고 있습니다. 대규모 검사실에서는 현재, 작업자의 시간을 최소화하면서 연속적인 검체 투입, 일상적인 유지보수, 그리고 화학 검사와 면역 측정을 통합한 업무를 처리할 수 있는 "워크어웨이" 시스템이 선호되고 있습니다. 지멘스사는 자사의 "Atellica CI" 분석 장치는 수동 워크플로우 단계를 75% 줄여주며, 하루당 수동 유지보수 시간이 5분 미만으로 충분하다고 밝혔는데, 이는 이러한 구매 경향의 변화를 직접적으로 뒷받침하고 있습니다. 로슈사도, "cobas c 703"를 통해 대용량 통합 검사 기능을 확충했습니다. "cobas pro" 솔루션은 시간당 최대 2,000건의 검사를 처리할 수 있으며, 2026년에 승인을 받았습니다. 이러한 추세에 따라 일부 중규모 검사실에서는 대용량 아키텍처의 소형 버전을 도입하는 움직임이 나타나고 있으며, 그 결과 고처리량 시스템의 성장률이 전체 설치 대수 성장률을 웃도는 속도로 증가하고 있습니다.

중소규모 검사실의 높은 총 소유 비용

화학발광 면역측정 분석기 시장은 소규모 검사 기관이나 지방 의료 기관에게 여전히 높은 보유 비용이라는 명백한 장벽에 직면해 있습니다. 이러한 비용은 장비 본체에만 국한되지 않으며, 구매자는 플랫폼의 전체 수명 기간 동안 시약 계약, 교정용 재료, 서비스 계약, 직원 교육 및 유지보수 비용도 부담하게 됩니다. 독자적인 사양의 시약과의 연계로 인해 장비가 도입되고, 그 비용이 일부 상각된 후라 하더라도 소규모 시설이 운영 비용을 절감할 여지는 제한적입니다. 이러한 압박은 시약 대여 모델이나 자금 조달 옵션이 제한적인 환경에서 가장 심하며, 그 결과 장비 교체 주기가 지연되고 최초 도입도 늦어지게 됩니다. 그 결과, 완전 자동 분석 장치를 도입하면 장기적인 운영 기간 동안 검사당 비용을 절감할 수 있음에도 불구하고, 많은 소규모 시설에서는 처리 능력이 낮은 시스템이나 구형 시스템을 계속 사용하고 있는 것이 현실입니다.

부문별 분석

2025년, 전기화학발광 면역 측정법은 화학발광 면역측정 분석기 시장 점유율의 45.73%를 차지하며, 높은 감도가 요구되는 병원 및 참조 검사실의 전반적인 검사 분야에서 계속해서 주도적인 기술로서의 위상을 유지했습니다. 이러한 확고한 입지는 종양학, 내분비학, 감염증 및 일반 면역 진단 분야에서 광범위한 검사 항목을 지원하는 로슈 및 지멘스 플랫폼의 도입 대수가 수년에 걸쳐 증가해 온 것을 반영합니다. 이 기술은 높은 감도, 폭넓은 검사 항목에 대한 대응 능력, 그리고 대량 처리 환경에서도 안정적인 일상적 성능을 모두 갖추고 있어 여전히 매력적입니다. 이러한 특징 덕분에 시약의 채택률은 높은 수준을 유지하고 있으며, 고객들은 초기 도입 후 다른 플랫폼 제품군으로 전환하는 것을 주저하는 경향이 있습니다.

화학발광 면역측정 분석기 시장에서는 주요 ECL 부문 외에도, 특히 미세입자 화학발광 방식에서 여전히 기술적 성장이 나타나고 있습니다. 미세입자 화학발광 면역분석법은 2031년까지 연평균 성장률(CAGR) 8.32%를 나타낼 것으로 예측되며, 이는 구매자들이 유연한 검사 메뉴의 확대와 일상 검사에서의 높은 경제성을 계속해서 중요하게 여기고 있음을 보여줍니다. 애보트의 “"Alinity i." 플랫폼은 심장 질환 및 감염증 검사 분야의 검사 항목을 지속적으로 확대함으로써 이러한 방향성을 뒷받침하고 있으며, 일상적인 검사실 환경에서 미세입자 기반 워크플로우의 상업적 기반을 강화하고 있습니다. 또한, 화학발광 효소면역측정법 역시 최고 수준의 감도보다는 상온에서 시약을 다루기 쉬운 점이나 물류 과정의 간소화가 중시되는 상황에서 여전히 상업적으로 중요한 위치를 차지하고 있습니다. 화학발광 면역측정 분석기 업계에서 진정한 전환점은 특정 형식이 다른 형식을 완전히 대체하는 것이 아니라, 화학 설계를 검사 항목의 폭, 검사실의 규모 및 운영 모델에 맞추는 데 있다고 할 수 있습니다.

2025년, 중처리량형 분석기는 화학발광 면역측정 분석기 시장 규모의 47.23%를 차지하고 있으며, 이는 이 등급의 기기가 일반 병원 검사실이나 대규모 외래 진료 시설의 요구를 얼마나 잘 충족시키고 있는지를 보여줍니다. 이러한 시스템은 최대 규모의 메가랩 구조로 전환하지 않으면서도, 검사 항목의 폭, 설치 면적, 결과 보고까지 소요되는 시간, 그리고 설비 투자 비용 간의 균형을 맞추어야 하는 시설에 서비스를 제공합니다. 많은 의료 기관에서는 모든 근무 교대 시간 동안 초대용량이 필요하지 않기 때문에 이러한 시스템을 도입함으로써 얻는 이점은 일시적인 것이 아니라 실질적인 것입니다. 또한, 중간 처리량 플랫폼은 광범위한 검사 항목과 관리하기 쉬운 유지보수 요건을 충족하는 경향이 있으며, 이는 정기적인 조달 주기에서 확고한 입지를 유지하는 데 도움이 되고 있습니다.

화학발광 면역측정 분석기 시장에서 처리 능력 증가세가 가장 두드러질 것으로 예상되는 부문은 고처리량 부문이며, 2031년까지 연평균 성장률(CAGR) 9.03%로 확대될 것으로 전망됩니다. 이는 북미 및 유럽에서 기준 실험실의 통합이 계속되고 있으며, 아시아태평양 전역에 걸쳐 새로운 중앙 검사실이 건설되고 있음을 반영한 것입니다. SNIBE사에 따르면, 이 회사의 ““MAGLUMI X10”는 모듈당 시간당 1,000건의 검사를 달성하고 있으며, 이는 입찰 주도형이나 대규모 병원 현장에서 처리 능력 확대가 얼마나 적극적으로 추진되고 있는지를 보여줍니다. 이러한 대규모 시설의 구매 담당자들은 레거시 시스템을 갱신할 때, 처음부터 검사 항목 확충이나 검체 수의 급증에 대비할 여지를 확보하고자 하는 이유로 중형 처리량 단계를 건너뛰는 경향이 강해지고 있습니다. 처리량이 낮은 분석기는 소형 설계와 적당한 일일 처리량이 처리 능력의 획기적인 향상보다 더 중요하게 여겨지는 소규모 진료소, 지방 시설 및 외래 검사실에서 여전히 뚜렷한 틈새 시장을 유지하고 있습니다.

지역별 분석

2025년, 북미는 화학발광 면역측정 분석기 시장 점유율의 41.71%를 차지하며 여전히 최대 지역 블록으로서의 위상을 유지했습니다. 이 지역은 견고한 보험 환급 제도, 주요 OEM 제조업체와의 긴밀한 병원 간 관계, 그리고 지속적인 시약 계약에 따른 대규모 도입 실적을 바탕으로 혜택을 누리고 있습니다. 미국은 여전히 핵심 국가로서의 지위를 유지하고 있으며, 2025년과 2026년에 주요 공급업체들이 잇달아 출시할 분석법 및 시스템 업그레이드가 이를 뒷받침하고 있습니다. 이러한 추가 기능 덕분에 반드시 기기를 새로 구입하지 않아도 플랫폼 이용률이 향상되고, 장기적인 고객 유지가 강화됩니다.

유럽은 화학발광 면역측정 분석기 시장에서 계속해서 2위 지역 시장을 차지하고 있으며, 검사실 수요와 마찬가지로 규제 영향도 여전히 받고 있습니다. EU의 IVDR(체외진단 의료기기 규정) 요건에 따라, 특히 구형 플랫폼에서 문서 업데이트나 규정 준수 지원이 필요한 경우, 레거시 시스템의 업데이트 및 재검증 활동이 촉진되고 있습니다. 또한 서유럽에서는 여러 국가에 걸친 입찰에 대응할 수 있고, 광범위한 서비스망을 갖추고 있으며, 다양한 검사 범주를 아우르는 통합된 제품 포트폴리오를 보유한 세계 공급업체가 선호되고 있습니다. EURIDICE 검사실 보고 프레임워크는 구조화된 데이터 교환 및 추적성 요건을 강화하고 있으며, 이를 통해 연결 기능을 갖춘 분석기에 추가적인 부가가치를 제공합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.85%를 나타낼 것으로 예측되며, 화학발광 면역측정 분석기 시장에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 중국은 주요 성장 동력이며, 조달 개혁에 따라 구매 행태가 변화함에 따라 가격, 현지 서비스, 국내 생산 역량에 대한 중요성이 커지고 있습니다. 인도에서도 민간 진단 체인의 확대와 도시 지역의 3차 의료기관에서 통합형 면역 측정 시스템의 보급이 진행되면서 시장에 활기를 불어넣고 있습니다. 일본, 한국, 호주에서는 중·고기술 플랫폼 및 첨단 측정 메뉴에 대한 안정적인 수요가 계속해서 이어질 것으로 전망됩니다. 중동 및 아프리카 및 남미는 절대 규모 면에서는 여전히 작지만, 걸프 국가들의 집중적인 진단 투자와 브라질 및 아르헨티나에서의 검사실 지속적인 확장에 힘입어, 이들 지역은 장기적인 성장에서 중요한 위치를 계속 차지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the chemiluminescence immunoassay analyzer market size is projected to expand from USD 3.16 billion in 2025 and USD 3.35 billion in 2026 to USD 4.64 billion by 2031, registering a CAGR of 6.73% between 2026 to 2031.

This report is Segmented by Technology (Electrochemiluminescence Immunoassay, and More), Throughput (High-Throughput, and More), Sample Type (Blood, Serum and Plasma, and More), Application (Infectious Diseases, and More), End User (Hospitals, and More), Connectivity (LIS and HL7 Integration, and More), and Geography (North America, and More). The Market Forecasts are Provided in Value (USD).

Global Chemiluminescence Immunoassay Analyzer Market Trends and Insights

Rising Demand for High-Sensitivity Biomarker Detection

The chemiluminescence immunoassay analyzer market is benefiting from the need to detect biomarkers at very low concentrations in oncology, cardiology, endocrinology, and specialty disease monitoring. Clinical use is moving toward assays that support early detection, repeated monitoring, and tighter treatment decisions, which raises the value of platforms with stronger analytical sensitivity. A 2026 review in Sensors & Diagnostics reported 8-plex electrochemiluminescence systems with detection limits from 15 fg/mL to 230 fg/mL, along with full clinical sensitivity and specificity for acute myocardial infarction biomarker panels across 260 samples. As high-sensitivity cardiac protocols move beyond large hospitals into urgent care and faster-response settings, laboratories need analyzers that can meet those analytical thresholds without losing workflow consistency. Vendors that improve luminophore chemistry and reduce background signal are likely to hold stronger positions in future assay development partnerships and premium testing menus.

Shift Toward Fully Automated High-Throughput Laboratory Workflows

The chemiluminescence immunoassay analyzer market is also being driven by hospital network consolidation and the need to keep instruments running with fewer staff interventions. Large laboratories now prefer walkaway systems that can handle continuous loading, routine maintenance, and integrated chemistry and immunoassay work with limited operator time. Siemens states that its Atellica CI analyzer reduces manual workflow steps by 75% and requires fewer than 5 minutes of daily hands-on maintenance, which directly supports this purchasing shift. Roche also expanded high-capacity integrated testing with the cobas c 703, which delivers up to 2,000 tests per hour on the cobas pro solution and was cleared in 2026. This pattern is pushing some mid-sized laboratories to buy smaller versions of high-volume architectures, which is helping high-throughput systems grow faster than the broader installed base.

High Total Cost of Ownership for Small and Mid-Sized Laboratories

The chemiluminescence immunoassay analyzer market still faces a clear barrier in the form of high ownership costs for smaller laboratories and rural providers. The cost is not limited to the instrument, because buyers also carry reagent commitments, calibration materials, service contracts, staff training, and maintenance expenses over the full platform life. Proprietary reagent tie-ins limit the room for smaller facilities to lower running costs even after the instrument has been installed and partly amortized. This pressure is strongest in settings where reagent rental models and financing options are limited, which slows replacement cycles and delays first-time adoption. The result is that many smaller facilities remain on lower-capacity or older systems even when fully automated analyzers would reduce cost per test over a longer operating period.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Decentralized and Stat Testing Networks

- Growth in Multiplex Assay Adoption for Consolidated Testing

- Skilled Operator Shortages for Maintenance and Calibration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrochemiluminescence immunoassay held 45.73% of the chemiluminescence immunoassay analyzer market share in 2025, which kept it as the leading technology across high-sensitivity hospital and reference laboratory testing. Its strong position reflects years of installed base expansion on Roche and Siemens platforms that support broad assay menus in oncology, endocrinology, infectious disease, and general immunodiagnostics. The technology remains attractive because it combines strong sensitivity, broad menu compatibility, and stable routine performance in high-volume environments. That mix keeps reagent attachment rates high and makes customers less willing to shift to a different platform family after initial installation.

The chemiluminescence immunoassay analyzer market is still seeing technology growth beyond the leading ECL segment, especially in microparticle chemiluminescence formats. Microparticle chemiluminescence immunoassay is projected to grow at an 8.32% CAGR through 2031, which shows that buyers continue to value flexible assay expansion and strong routine testing economics. Abbott's Alinity i platform has helped support this direction through continued assay menu expansion in cardiac and infectious disease testing, which reinforces the commercial depth of microparticle-based workflows in routine labs. Chemiluminescence enzyme immunoassay also remains commercially relevant where ambient reagent handling and simpler logistics matter more than the highest possible sensitivity. Within the chemiluminescence immunoassay analyzers industry, the practical divide is less about one format fully replacing another and more about matching chemistry design to menu breadth, laboratory scale, and operating model.

Mid-throughput analyzers represented 47.23% of the chemiluminescence immunoassay analyzer market size in 2025, which shows how closely this tier fits the needs of standard hospital laboratories and larger outpatient facilities. These systems serve sites that must balance assay breadth, physical footprint, turnaround time, and capital cost without moving to the largest mega-lab architecture. Their installed advantage is practical rather than temporary, because many institutions do not need ultra-high capacity across every shift. Mid-throughput platforms also tend to support broad menus and manageable service requirements, which helps them stay entrenched in routine procurement cycles.

The chemiluminescence immunoassay analyzer market is expected to see its strongest throughput growth in the high-throughput tier, which is projected to advance at a 9.03% CAGR through 2031. This reflects continued reference laboratory consolidation in North America and Europe and new central laboratory construction across Asia-Pacific. SNIBE states that its MAGLUMI X10 reaches 1,000 tests per hour per module, which shows how aggressive capacity expansion has become in tender-driven and large-hospital settings. Buyers in these large sites are increasingly skipping the middle tier when they replace legacy systems, because they want room for menu growth and higher sample peaks from the start. Low-throughput analyzers still keep a clear niche in smaller clinics, rural settings, and outreach laboratories where compact design and moderate daily volumes matter more than step-change capacity.

Complete Report Scope:

- By Technology

- Electrochemiluminescence Immunoassay

- Microparticle Chemiluminescence Immunoassay

- Chemiluminescence Enzyme Immunoassay

- By Throughput

- High-Throughput

- Mid-Throughput

- Low-Throughput

- By Sample Type

- Blood

- Serum and Plasma

- Urine

- Saliva

- Cerebrospinal Fluid

- By Application

- Infectious Diseases Testing

- Endocrinology

- Oncology

- Cardiovascular Testing

- Autoimmune Disorders

- Therapeutic Drug Monitoring and Toxicology

- By End User

- Hospitals

- Diagnostic Laboratories

- Specialty Clinics

- Academic and Research Institutes

- Contract Research Organizations

- By Connectivity

- LIS and HL7 Integration

- Middleware Integration

- Remote Monitoring and IoT

- Cybersecurity and Compliance Features

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.71% of the chemiluminescence immunoassay analyzer market share in 2025, which kept it as the largest regional block. The region benefits from strong reimbursement structures, deep hospital relationships with major OEMs, and a large installed base tied to recurring reagent contracts. The United States remains the anchor country, supported by a steady flow of assay launches and system upgrades from major suppliers in 2025 and 2026. Those additions raise platform utilization without always requiring instrument replacement, which strengthens long-term customer retention.

Europe remained the second-largest regional market in the chemiluminescence immunoassay analyzer market and continued to be shaped by regulation as much as by laboratory demand. EU IVDR requirements are pushing replacement and revalidation activity for legacy systems, especially where older platforms need updated documentation and compliance support. Western Europe also favors global suppliers that can manage multi-country tenders, broad service coverage, and integrated product portfolios across several testing categories. The EURIDICE laboratory reporting framework is reinforcing structured data exchange and traceability requirements, which adds another layer of value to connectivity-ready analyzers.

Asia-Pacific is projected to grow at an 8.85% CAGR through 2031, which makes it the fastest-growing regional segment in the chemiluminescence immunoassay analyzer market. China is a major driver because procurement reforms are changing buying behavior and giving more weight to price, local service, and domestic manufacturing strength. India is also adding momentum through private diagnostic chain expansion and broader use of integrated immunoassay systems in urban tertiary hospitals. Japan, South Korea, and Australia continue to contribute stable demand for mid-to-high technology platforms and advanced assay menus. The Middle East and Africa and South America remain smaller in absolute size, but centralized diagnostic investment in Gulf countries and ongoing laboratory growth in Brazil and Argentina keep these regions relevant for long-term expansion.

- Abbott Laboratories

- Agappe Diagnostics Ltd.

- Beijing Hotgen Biotech Co., Ltd.

- bioMerieux

- Danaher

- DiaSorin

- Diazyme Laboratories, Inc.

- Fapon Biotech Inc.

- Roche

- Fujirebio Holdings, Inc.

- Guangzhou Wondfo Biotech Co., Ltd.

- Maccura Biotechnology Co., Ltd.

- QuidelOrtho

- Randox Laboratories

- Mindray

- Shenzhen New Industries Biomedical Engineering

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

- Tosoh

- Werfen S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High-Sensitivity Biomarker Detection

- 4.2.2 Shift Toward Fully Automated High-Throughput Laboratory Workflows

- 4.2.3 Expansion of Decentralized and Stat Testing Networks

- 4.2.4 Growth in Multiplex Assay Adoption for Consolidated Testing

- 4.2.5 Connectivity Demand for LIS, Middleware, and Audit-Ready Data Traceability

- 4.2.6 Reagent Stability and Low Sample Volume Requirements Supporting Lab Efficiency

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Small and Mid-Sized Laboratories

- 4.3.2 Skilled Operator Shortages for Maintenance and Calibration

- 4.3.3 Regulatory Fragmentation Across Multi-Country Procurement Markets

- 4.3.4 Component Sourcing Vulnerability for Optical, Microfluidic, and Semiconductor Inputs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Electrochemiluminescence Immunoassay

- 5.1.2 Microparticle Chemiluminescence Immunoassay

- 5.1.3 Chemiluminescence Enzyme Immunoassay

- 5.2 By Throughput

- 5.2.1 High-Throughput

- 5.2.2 Mid-Throughput

- 5.2.3 Low-Throughput

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Serum and Plasma

- 5.3.3 Urine

- 5.3.4 Saliva

- 5.3.5 Cerebrospinal Fluid

- 5.4 By Application

- 5.4.1 Infectious Diseases Testing

- 5.4.2 Endocrinology

- 5.4.3 Oncology

- 5.4.4 Cardiovascular Testing

- 5.4.5 Autoimmune Disorders

- 5.4.6 Therapeutic Drug Monitoring and Toxicology

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Specialty Clinics

- 5.5.4 Academic and Research Institutes

- 5.5.5 Contract Research Organizations

- 5.6 By Connectivity

- 5.6.1 LIS and HL7 Integration

- 5.6.2 Middleware Integration

- 5.6.3 Remote Monitoring and IoT

- 5.6.4 Cybersecurity and Compliance Features

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agappe Diagnostics Ltd.

- 6.3.3 Beijing Hotgen Biotech Co., Ltd.

- 6.3.4 bioMerieux SA

- 6.3.5 Danaher Corporation

- 6.3.6 DiaSorin S.p.A.

- 6.3.7 Diazyme Laboratories, Inc.

- 6.3.8 Fapon Biotech Inc.

- 6.3.9 F. Hoffmann-La Roche Ltd.

- 6.3.10 Fujirebio Holdings, Inc.

- 6.3.11 Guangzhou Wondfo Biotech Co., Ltd.

- 6.3.12 Maccura Biotechnology Co., Ltd.

- 6.3.13 QuidelOrtho Corporation

- 6.3.14 Randox Laboratories Ltd.

- 6.3.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.16 Shenzhen New Industries Biomedical Engineering Co., Ltd.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Sysmex Corporation

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Tosoh Corporation

- 6.3.21 Werfen S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment