|

시장보고서

상품코드

2072933

자동화 미생물학 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automated Microbiology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

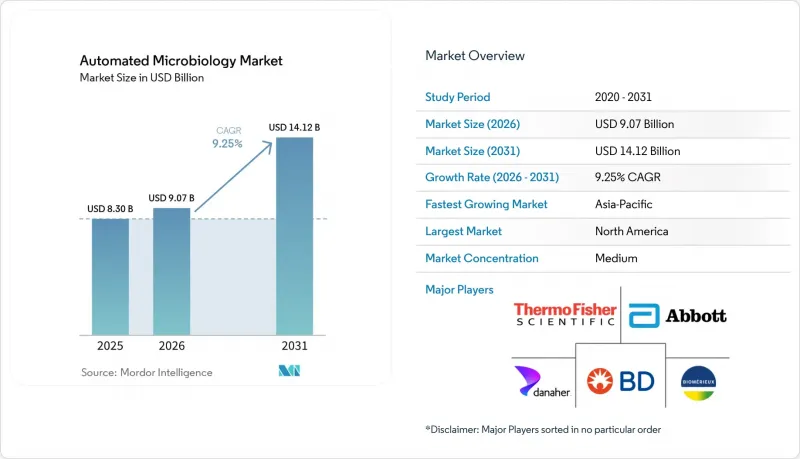

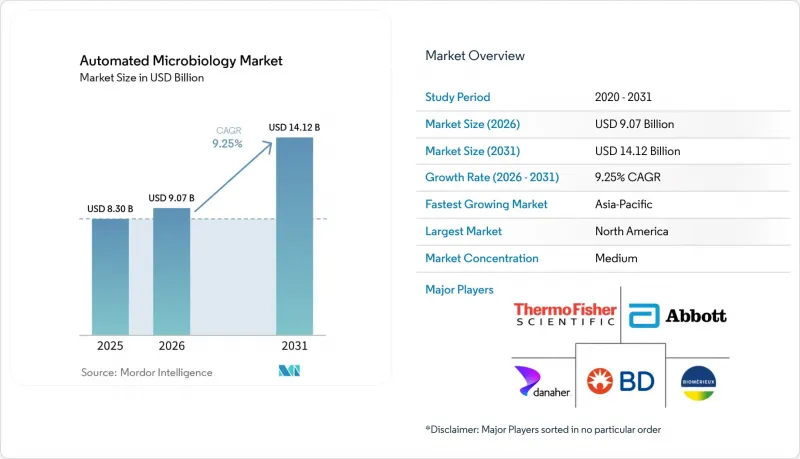

Mordor Intelligence에 의하면, 자동화 미생물학 시장 규모는 2025년 83억 달러에서 2026년에는 90억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.25%로 성장을 지속하여, 2031년에는 141억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(장비(자동 미생물 동정 시스템 등)), 자동화 유형(전자동, 반자동), 용도(임상 진단 등), 최종 사용자(병원 등), 진단 기술(유세포 분석법 등), 검체 유형(혈액 등), 워크플로우(전처리 등), 지역별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 자동화 미생물학 시장 동향 및 인사이트

검사량이 많은 검사실에서 신속한 병원체 동정에 대한 수요가 증가하고 있습니다.

자동화 미생물학 시장에서는 하루당 검체 처리량이 매우 많은 가운데, 인력 증원이나 수동 검사 공정의 확대가 어려운 핵심 검사실에서 수요가 증가하고 있습니다. 노스웰 헬스(Northwell Health)의 핵심 검사실에서는 종합 검사 자동화 플랫폼을 활용해 하루 2,400건 이상의 소변 배양 검사를 처리하고 있는 것으로 보고되고 있으며, 이러한 규모에서는 무인 미생물학 시스템이 단순한 선택적 업그레이드가 아닌 운영상의 필수 요건이 되고 있습니다. 적절한 치료가 지연되면 패혈증의 치료 결과가 악화되므로, 임상적 긴급성이 그 필요성을 더욱 높이고 있습니다. 따라서 혈액 배양의 검출 속도와 결과 보고 시간은 여전히 검사실의 구매 결정에 있어 핵심적인 요소로 남아 있습니다. 검증된 환경에서 토탈 실험실 자동화(TLA)를 도입한 결과, 혈액 배양의 처리 시간은 97시간에서 53.5시간으로, 소변 배양의 음성 판정 보고 시간은 52.1시간에서 28.3시간으로 단축되었습니다. 이는 시간 단축이 단순한 업무 흐름상의 주장이 아니라, 현재 측정 가능한 성과로 자리 잡았음을 보여줍니다. 워터스사는 2026년 6월, BD BACTEC FXI 시스템이 FDA의 510(k) 승인을 획득했으며, 이전 세대 모델에 비해 혈류 감염 검출까지 걸리는 평균 시간을 3시간(15%) 단축했다고 발표했습니다. 이는 확립된 범주에서도 제품 업그레이드가 여전히 임상적으로 의미 있는 성과를 가져오고 있음을 보여줍니다.

AMR 감시 및 관리 프로그램의 확대

자동화 미생물학 시장은 표준화된 감수성 데이터와 국내 및 전 세계 보고 시스템 간의 보다 광범위한 상호 운용성을 필요로 하는 감시 체계에 의해서도 뒷받침되고 있습니다. CDC(미국 질병통제예방센터)의 항생제 내성 검사실 네트워크는 2025년 말까지 150만 건 이상의 검사를 실시했으며, 그 내역은 분리주의 특성 분석 52만 건 이상, 정착 스크리닝 53만 건, 전장 유전체 염기서열 분석 66만 4,000건에 달할 전망입니다. 이는 자동화 미생물학 플랫폼이 감당해야 할 규모가 얼마나 큰지를 여실히 보여줍니다. 이와 관련된 변화로, 분자 수준에서의 내성 검출로 전환되는 추세가 나타나고 있습니다. 이는 기존의 배양 워크플로우에만 의존하는 검사실의 경우, 감시 프로그램에서 표준화되고 기계 판독이 가능한 내성 마커에 대한 수요가 증가함에 따라 더 광범위한 데이터 공백에 직면하게 되기 때문입니다. 『Infection Control & Hospital Epidemiology』지에 게재된 2025년 연구에 따르면, 혈액 배양을 통한 신속한 분자 수준의 항생제 내성(AMR) 검출이 널리 채택될 경우 국가 차원의 감시 데이터 간 비교 가능성에 직접적인 영향을 미칩니다는 점이 지적되었으며, 이는 표현형 및 분자 수준의 결과를 단일 워크플로우로 통합할 수 있는 플랫폼에 대한 수요를 뒷받침하고 있습니다. WHO의 2025년 보고서는 110개국에서 수집된 2,300만 건 이상의 세균학적으로 확인된 감염병 데이터를 바탕으로 하고 있으며, 이러한 광범위한 데이터는 성숙한 검사 네트워크와 확장 중인 검사 네트워크 모두에서 자동화된 검사 인프라에 대한 투자를 지속적으로 촉진하고 있습니다.

높은 초기 투자 비용과 지속적인 서비스 계약에 따른 부담

미생물학 자동화 시장은 여전히 큰 도입 장벽에 직면해 있습니다. 이는 완전 자동화 시스템의 경우 막대한 초기 투자 비용, 전용 공간, 그리고 장기적인 서비스 계약이 필요하며, 많은 소규모 검사실의 경우 이러한 부담을 감당하기 어렵기 때문입니다. 『Frontiers in Cellular and Infection Microbiology』지에 게재된 2026년 다기관 공동 리뷰에 따르면, 고액의 설비 투자, 특수 소모품에 대한 의존도, 전용 검사 공간의 필요성, 그리고 가동 중단 위험이 검사실 완전 자동화 도입의 주요 제약 요인으로 지목되었습니다. 비용 문제는 장비 구입에만 그치지 않습니다. 벤더별 소모품이나 지원 계약으로 인해 시스템은 장기적인 경상비 구조를 띠게 되며, 병원의 예산 심사에서는 보다 분산된 수기 방식의 대안에 비해 불리하게 평가되는 경우가 많기 때문입니다. 신흥 시장에서는 현지 서비스 기술 체계가 제한적일 가능성이 있으며, 수리 지연으로 인해 단일 장비의 고장만으로도 곧바로 검사 업무가 밀리게 되므로 그 부담은 더욱 커집니다. 이러한 요인들이 복합적으로 작용하여, 자동화 미생물학 시장에서 최첨단 자동화 시스템은 검사 건수가 많은 병원 시스템, 참조 검사실 및 재정적 여유가 있는 제약 시설에 집중되어 있습니다.

부문별 분석

2025년, 시약 및 키트는 자동화 미생물학 시장의 48.31%를 차지하고 있으며, 이는 증가하는 도입 기반 전반에 걸쳐 배지, 동정 패널 및 감수성 검사 카드에 대한 지속적인 수요를 반영하고 있습니다. 이 수익원은 분석 장비의 판매와는 구조적으로 다릅니다. 왜냐하면 분석 장비가 설치되고 검사실이 공급 계약을 체결하면 소모품이 지속적으로 공급되기 때문입니다. 이러한 지속적인 수익 구조를 통해, 병원 시스템 간에 설비 투자 주문이 고르지 않게 발생하더라도 공급업체의 수익을 안정적으로 유지할 수 있습니다. 또한 주요 공급업체의 경우, 보다 예측 가능한 현금 흐름 기반을 통해 소프트웨어 업데이트, 검사 항목 확충 및 현장 서비스 대응을 수행할 여지가 생깁니다.

자동화 미생물학 시장에서는 장비 분야의 확대가 가속화될 것으로 예상되며, 검사실이 부분적인 자동화에서 전처리, 분석, 후처리를 보다 통합한 체계로 전환함에 따라 2026년부터 2031년까지 연평균 성장률(CAGR) 11.38%로 성장할 것으로 전망됩니다. AI를 활용한 이미지 분석이 초기 하드웨어 도입 후의 워크플로우 속도, 일관성 및 고객 유지에 영향을 미치게 되면서, 자동화 미생물학 업계에서 소프트웨어의 전략적 중요성이 높아지고 있습니다. 코판사는 2026년 2월, PhenoMATRIX가 여러 유형의 배양 배지를 아우르는 AI 지원 콜로니 플레이트 선별에 대해 FDA의 510(k) 승인(광범위한 사용 목적)을 획득했다고 발표했습니다. 이는 부가가치가 더 높은 소프트웨어 영역에서의 제품 개발 방향을 반영하고 있습니다. 그 결과, 하드웨어와 소프트웨어가 현재 혁신의 주요 쟁점이 되고 있는 반면, 시약은 여전히 비즈니스 모델의 기반을 이루고 있습니다.

2025년에는 완전 자동화 시스템이 시장 매출의 75.24%를 차지하고 있으며, 이는 구매 결정의 주요 기준이 더 이상 분석 성능에만 국한되지 않고 인력 대체와 밀접하게 연관되어 있음을 보여줍니다. 임상 검사 분야의 인력 부족으로 인해 관리자들은 빈번한 수작업 개입이나 전문 미생물학 인력에 대한 장기 연수 기간에 의존하는 업무 흐름을 유지하기가 어려워지고 있습니다. 이러한 상황에서 완전 무인화 시스템은 처리 능력 향상뿐만 아니라, 인력 부족으로 인한 위험과 검사 결과 지연이 반복되는 현상을 줄여준다는 점에서도 가치를 제공합니다. 이것이 바로 대규모 병원이나 검사 위탁 네트워크에서 완전 자동화 플랫폼이 선호되는 이유입니다.

반자동 시스템은 검사 건수가 적은 검사실, 드문 형태나 다양한 균종이 포함된 검체에 대해 여전히 사람이 세심하게 확인해야 하는 검사 환경에서 여전히 중요한 역할을 하고 있습니다. 자동화 미생물학 시장은 모든 지역에서 동일한 속도로 변화하고 있는 것은 아닙니다. 중국, 남아시아, 동남아시아의 많은 중규모 병원들이 여전히 반자동에서 완전 자동화로 전환하는 과정에 있기 때문입니다. 『European Journal of Clinical Microbiology &Infectious Diseases』 저널의 2026년 연구에서는 Autof MS2600 및 EXS3000과 같은 중국의 MALDI-TOF 시스템이 소개되었습니다. 이들 모두 5,189종을 넘는 데이터베이스를 보유하고 있으며, 중견 시장 부문에서 국내 벤더가 점점 더 신뢰할 수 있는 선택지로 자리매김하고 있음을 보여줍니다. 즉, 다음 공유 변동은 검사실이 자동화될지 여부가 아니라, 완전 자동화가 보급되는 과정에서 어떤 공급업체가 업데이트 주기를 선점하느냐에 따라 발생할 가능성이 있습니다.

2025년 자동화 미생물학 시장 규모 중 임상 진단이 54.52%를 차지하고 있으며, 이는 일상적인 검사 건수 측면에서 병원 관련 검사가 여전히 가장 큰 수요원임을 뒷받침하고 있습니다. 혈류 감염증, 요로 감염증 및 호흡기 병원체에 대한 검사는 연기하기 어렵고, 완전히 일원화하기도 힘든 일일 검사 수요를 지속적으로 발생시키고 있습니다. 이로 인해 기본적인 검사 수요가 안정적이기 때문에 설비 투자가 일시적으로 정체되더라도 임상 분야는 견고한 기반을 유지할 수 있습니다. 또한, 항생제 적정 사용 프로그램의 확산도 수요의 지속을 뒷받침하고 있습니다. 이는 개별 임상 사례가 점점 더 표준화된 미생물학 데이터 요건과 연계되어 있기 때문입니다.

바이오의약품 제조 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.25%로 확대될 것으로 예상되며, 이에 따라 자동화 미생물학 시장에서 가장 빠르게 성장하는 응용 분야가 될 것입니다. 이 분야는 세포 및 유전자 치료의 규모 확대, 무균성에 대한 기대감 고조, 그리고 주요 제조 공정에서 신속하고 자동화된 바이오버든 모니터링의 활용 증가에 힘입어 더욱 강화되고 있습니다. bioMerieux사는 2026년 1월에 Accellix사의 인수를 완료했습니다. 이번 인수는 세포 및 유전자 치료의 품질 관리 분야에서 신속한 자동 유세포분석 기술 분야의 해당 기업의 입지를 강화하는 것이며, 이 분야에 전략적 가치가 부여되고 있음을 보여줍니다. 환경·수질 검사 및 식품 및 음료 검사는 규모는 작지만 안정적인 틈새 시장으로, 자동화 미생물학 업계에서 공급업체들이 병원의 경기 변동에 좌우되지 않는 사업 다각화를 도모하는 데 도움이 되고 있습니다.

지역별 분석

2025년 기준으로 북미는 자동화 미생물학 시장 규모의 42.22%를 차지하고 있으며, 이러한 위상은 임상 검사의 높은 실시 빈도, 대규모 의약품 제조 거점, 그리고 규제 환경 하에서 문서화된 자동화가 점점 더 중요시되는 검사 환경을 반영하고 있습니다. 미국은 인력 부족이 특히 두드러지기 때문에 여전히 지역 수요의 중심지 역할을 하고 있습니다. ASCP의 보고에 따르면, 연수 프로그램 졸업생이 8,800명인 반면, 연간 2만 4,000건 이상의 채용 공고가 있는 것으로 나타났습니다. 제품 승인 또한 꾸준한 업데이트 및 업그레이드 주기를 뒷받침하고 있습니다. 여기에는 2025년 4월의 BD Phoenix M50, 2025년 3월의 bioMerieux VITEK COMPACT PRO, 2026년 2월의 Copan PhenoMATRIX, 2026년 6월의 BD BACTEC FXI 등이 포함됩니다. 캐나다와 멕시코는 여전히 시장 기여도가 낮은 편이지만, 캐나다의 검사 서비스 분야 통합과 멕시코의 민간 병원 기반 확충에 힘입어 자동화 미생물학 시장에 대한 수요는 계속해서 서서히 증가하고 있습니다.

유럽의 자동화 미생물학 시장 동향은 공립 병원의 조달 주기와 해당 지역의 견고한 제약 품질 관리 기반에 의해 형성되고 있습니다. 성장 속도는 아시아태평양만큼 빠르지는 않지만, 병원 검사실, 참조 센터, 산업용 사용자들이 모두 장비 및 소모품 수요에 기여하고 있어 수요 구성은 매우 다양합니다. bioMerieux사는 2025년 EMEA 지역의 유기 매출 성장률이 4.6%였습니다고 보고했으며, 해당 지역 전체의 성장을 이끈 것은 산업용 분야였습니다. 이는 제약 품질 관리가 중요한 성장 요인이라는 견해를 뒷받침하는 것입니다. 스페인과 이탈리아에서는 검사실 현대화 및 의료 시스템에 대한 투자를 통해 수요가 지속적으로 증가하고 있으며, 아시아태평양에서 볼 수 있는 것과 같은 급속한 성장률은 보이지 않음에도 불구하고 유럽은 균형 잡힌 성장 양상을 유지하고 있습니다.

아시아태평양은 2026년부터 2031년까지 자동화 미생물학 시장에서 12.65%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되지만, 그 성장 요인은 지역에 따라 크게 다릅니다. 인도에서는 많은 지방 병원과 3차 의료기관이 수동 항생제 감수성 검사(AST) 방식에서 자동화된 표현형 분석 시스템으로 전환하고 있기 때문에 도입 여지는 여전히 크며, 장비를 처음 도입하는 경우에도 충분한 여지가 남아 있습니다. 일본은 보다 성숙한 자동화 시장이며, 현재는 업그레이드 단계에 있습니다. 이는 2026년 4월 BD BACTEC FXI가 PMDA의 승인을 획득한 사실과, 기타 규제 당국의 승인에도 반영되어 있습니다. 중국의 경우, bioMerieux사가 2025년 해당 국가에서 미생물학 관련 매출이 두 자릿수의 유기적 감소를 기록했다고 보고한 반면, 구매가 상위권 병원에서 중견 병원으로 이동함에 따라 중견 병원에서의 도입이 지속적으로 확대되고 있어 상황은 복잡합니다. 한국은 바이오의약품 수출 확대의 혜택을 누리고 있으며, 이로 인해 품질 관리 자동화에 대한 수요가 더욱 증가하고 있습니다. 중동 및 아프리카 및 남미는 여전히 초기 단계 시장이며, GCC(걸프협력회의) 국가들의 의료 인프라 구축 계획과 브라질의 민간 검사 기관이 수요의 기반을 이루고 있지만, 현지에서의 검증 및 서비스 체계가 제한적이기 때문에 보다 광범위한 도입 진전은 여전히 더딘 상태입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the automated microbiology market size is expected to grow from USD 8.30 billion in 2025 to USD 9.07 billion in 2026 and is forecast to reach USD 14.12 billion by 2031 at 9.25% CAGR over 2026-2031.

This report is Segmented by Product Type (Instruments [Automated Microbial Identification Systems and More], and More), Automation Type (Fully Automated, Semi-Automated), Application (Clinical Diagnostics, and More), End User (Hospitals and More), Diagnostic Technology (Flow Cytometry and More), Sample Type (Blood, and More), Workflow (Pre-Analytical, and More), and Geography. Forecasts in Value (USD).

Global Automated Microbiology Market Trends and Insights

Rising Need for Rapid Pathogen Identification in High-Volume Labs

The automated microbiology market is seeing stronger demand from core laboratories that now process very high daily specimen volumes with limited ability to add staff or extend manual review steps. Northwell Health's core laboratory was reported to process more than 2,400 urine cultures each day on a total laboratory automation platform, and that scale makes walk-away microbiology systems an operational requirement rather than a discretionary upgrade. Clinical urgency is reinforcing that demand because sepsis treatment outcomes worsen when appropriate therapy is delayed, which keeps blood culture detection speed and result reporting time at the center of laboratory purchasing decisions. In validated settings, total laboratory automation reduced blood culture turnaround time from 97 hours to 53.5 hours and reduced urine culture negative reporting time from 52.1 hours to 28.3 hours, which shows that time compression is now measurable and not just a workflow claim. Waters announced in June 2026 that the BD BACTEC FXI system received FDA 510(k) clearance and reduced mean time to bloodstream infection detection by 3 hours, or 15%, compared with its predecessor, which shows that product upgrades are still producing clinically relevant gains even in an established category.

Expanding AMR Surveillance and Stewardship Programs

The automated microbiology market is also being supported by surveillance frameworks that require standardized susceptibility data and wider interoperability across national and global reporting systems. The CDC Antimicrobial Resistance Laboratory Network had conducted more than 1.5 million tests through the end of 2025, including more than 520,000 isolate characterizations, 530,000 colonization screenings, and 664,000 whole-genome sequences, which illustrates the scale that automated microbiology platforms must support. A related shift is visible in the move toward molecular resistance detection because laboratories that rely only on conventional culture workflows face wider data gaps when surveillance programs increasingly need standardized and machine-readable resistance markers. A 2025 study in Infection Control & Hospital Epidemiology noted that wide adoption of rapid molecular AMR detection from blood cultures has direct implications for national surveillance comparability, which supports demand for platforms that can combine phenotypic and molecular outputs in one workflow. WHO's 2025 report drew on more than 23 million bacteriologically confirmed infections from 110 countries, and that breadth continues to support investment in automated laboratory infrastructure across both mature and scaling testing networks.

High Capital Cost and Ongoing Service Contract Burden

The automated microbiology market still faces a meaningful adoption barrier because fully automated systems require large upfront spending, dedicated space, and long service commitments that many smaller laboratories struggle to absorb. A 2026 multi-institutional review in Frontiers in Cellular and Infection Microbiology identified high capital investment, dependence on specialized consumables, the need for dedicated laboratory space, and exposure to downtime as the main constraints on total laboratory automation adoption. The cost issue is not limited to instrument purchase because vendor-specific consumables and support contracts turn the system into a long-term recurring expense structure that often compares poorly with more distributed manual alternatives in hospital budgeting reviews. The burden is even heavier in emerging markets because local service engineering capacity may be limited, and delays in repairs can quickly turn a single equipment issue into a testing backlog. That combination keeps the most advanced automation concentrated in higher-volume hospital systems, reference laboratories, and well-funded pharmaceutical facilities within the automated microbiology market.

Other drivers and restraints analyzed in the detailed report include:

- Automation Demand Driven by Technician Shortages and Turnaround-Time Pressure

- Increasing QC Requirements in Pharma, Food, and Water Testing

- Complex Validation, Interoperability, and LIMS Integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits held 48.31% of the automated microbiology market share in 2025, which reflects the recurring demand for culture media, identification panels, and susceptibility cards across a growing installed base. This revenue stream is structurally different from instrument sales because consumables continue to move once an analyzer is placed and a laboratory enters a supply relationship. That recurring profile helps stabilize vendor revenue even when capital ordering becomes uneven across hospital systems. It also gives leading suppliers room to support software updates, menu expansion, and field service through a more predictable cash flow base.

The automated microbiology market will see faster expansion in instruments, which are forecast to grow at 11.38% CAGR from 2026 to 2031 as laboratories replace partial automation with more integrated pre-analytical, analytical, and post-analytical set-ups. Software is becoming more strategically important within the automated microbiology industry because AI-assisted image analysis now influences workflow speed, consistency, and customer retention after the initial hardware placement. Copan stated in February 2026 that PhenoMATRIX received broad intended-use FDA 510(k) clearance for AI-assisted colony plate sorting across multiple culture media types, which reflects the direction of product development in higher-value software layers. As a result, instruments and software are now the main innovation battleground, while reagents continue to anchor the commercial model.

Fully automated systems held 75.24% of market revenue in 2025, which shows that the dominant purchasing logic is no longer limited to analytical performance and is now closely tied to labor substitution. The staffing gap in laboratory medicine has made it harder for administrators to defend workflows that depend on frequent manual intervention or long training periods for specialized microbiology staff. In that setting, full walk-away systems offer value not only through throughput gains but also through lower exposure to open staffing positions and repeated turnaround delays. This is why fully automated platforms have become the preferred format in larger hospital and reference laboratory networks.

Semi-automated systems still retain a role in lower-volume laboratories and in testing settings where uncommon morphologies or polymicrobial specimens continue to need closer human review. The automated microbiology market is not transitioning at the same speed everywhere because many mid-tier hospitals in China, South Asia, and Southeast Asia are still moving from semi-automated to fully automated configurations. A 2026 study in the European Journal of Clinical Microbiology & Infectious Diseases highlighted Chinese MALDI-TOF systems such as Autof MS2600 and EXS3000, both with databases exceeding 5,189 species, which shows that domestic vendors are becoming more credible options in mid-market segments. That means the next wave of share shifts may come not from whether laboratories automate, but from which suppliers capture the replacement cycle as full automation spreads.

Clinical diagnostics accounted for 54.52% of the automated microbiology market size in 2025, which confirms that hospital-associated testing remains the largest demand center by routine volume. Bloodstream infection, urinary tract infection, and respiratory pathogen work continue to generate daily testing demand that is hard to defer and difficult to centralize completely. That gives the clinical segment a durable base even when capital spending pauses because the underlying testing need remains steady. The breadth of antimicrobial stewardship programs also supports continued demand because each clinical episode is increasingly tied to more standardized microbiology data requirements.

Biopharmaceutical production is forecast to expand at 11.25% CAGR from 2026 to 2031, which makes it the fastest-growing application in the automated microbiology market. This segment is being strengthened by cell and gene therapy scale-up, higher sterility expectations, and more frequent use of rapid and automated bioburden monitoring in critical production steps. bioMerieux completed the acquisition of Accellix in January 2026, and the deal supports its position in rapid automated flow cytometry for cell and gene therapy quality control, which signals the strategic value attached to this area. Environmental and water testing, along with food and beverage testing, remain smaller but stable niches that help vendors diversify beyond hospital cycles within the automated microbiology industry.

Complete Report Scope:

- By Product Type

- Instruments

- Automated Microbial Identification Systems

- Automated Blood Culture Systems

- Automated Colony Counters

- Automated Sample Preparation Systems

- Automated Antibiotic Susceptibility Testing Systems

- Automated Microbiology Analyzers

- Automated Incubators

- Automated Media Preparation Systems

- Reagents and Kits

- Software

- Instruments

- By Automation Type

- Fully Automated

- Semi-Automated

- By Application

- Clinical Diagnostics

- Biopharmaceutical Production

- Environmental and Water Testing

- Food and Beverage Testing

- Other Applications

- By End User

- Hospitals and Clinical Laboratories

- Pharmaceutical and Biopharmaceutical Companies

- Food and Beverage Manufacturers

- Contract Research Organizations

- Other End Users

- By Diagnostic Technology

- Molecular Diagnostics

- Mass Spectrometry

- Automated Imaging and Digital Microscopy

- Flow Cytometry

- Other Technologies

- By Sample Type

- Blood

- Urine

- Tissue

- Other Sample Types

- By Workflow

- Pre-Analytical Process

- Analytical Process

- Post-Analytical Process

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 42.22% of the automated microbiology market size in 2025, and that position reflects high clinical testing intensity, a large pharmaceutical manufacturing base, and a laboratory environment that increasingly favors documented automation in regulated settings. The United States remains the center of regional demand because workforce shortages are especially visible there, with ASCP reporting more than 24,000 annual openings against 8,800 graduates from training programs. Product approvals have also supported a steady replacement and upgrade cycle, including BD Phoenix M50 in April 2025, bioMerieux VITEK COMPACT PRO in March 2025, Copan PhenoMATRIX in February 2026, and BD BACTEC FXI in June 2026. Canada and Mexico remain smaller contributors, but consolidation in Canadian laboratory services and the expansion of Mexico's private hospital base continue to add incremental demand to the automated microbiology market.

Europe's position in the automated microbiology market is shaped by public hospital procurement cycles and by the region's strong pharmaceutical quality control base. Growth is steadier than in Asia-Pacific, but the demand mix is broad because hospital laboratories, reference centers, and industrial users all contribute to equipment and consumables demand. bioMerieux reported 4.6% organic sales growth in EMEA in 2025, and industrial applications led the improvement across the region, which supports the view that pharmaceutical quality control is an important growth contributor. Spain and Italy continue to add demand through laboratory modernization and health system investment, which gives Europe a balanced growth profile even without the faster expansion rates seen in Asia-Pacific.

Asia-Pacific will record the highest CAGR at 12.65% from 2026 to 2031 in the automated microbiology market, but the drivers differ widely across the region. India still has a long runway for adoption because many district and tertiary hospitals are moving from manual AST methods to automated phenotypic systems, which leaves substantial room for first-time instrument placement. Japan is a more mature automation market and is now in an upgrade phase, which is reflected in the April 2026 PMDA approval for BD BACTEC FXI alongside its other regulatory clearances. China presents a mixed picture because bioMerieux reported a double-digit organic decline in microbiology revenue there in 2025, while adoption in mid-tier hospitals continues to expand as purchasing shifts beyond the top hospital tier. South Korea is benefiting from biopharma export growth, which is creating additional quality control automation demand. Middle East and Africa and South America remain earlier-stage opportunities, where GCC healthcare infrastructure programs and Brazil's private laboratory base provide demand anchors, while limited local validation and service capacity still slows broader adoption.

- Abbott Laboratories

- Accelerate Diagnostics, Inc.

- Beckton Dickinson

- bioMerieux

- Bio-Rad Laboratories

- Bruker

- Charles River

- Clever Culture Systems Limited

- Copan Diagnostics, Inc.

- Danaher

- DiaSorin

- Merck

- Neogen

- QIAGEN

- Rapid Micro Biosystems, Inc.

- Roche Diagnostics International Ltd.

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Rapid Pathogen Identification in High-Volume Labs

- 4.2.2 Expanding Antimicrobial Resistance Surveillance and Stewardship Programs

- 4.2.3 Automation Demand Driven by Technician Shortages and Turnaround-Time Pressure

- 4.2.4 Increasing QC Requirements in Pharma, Food, and Water Testing

- 4.2.5 Cloud-Connected Workflow Standardization Across Multi-Site Lab Networks

- 4.2.6 Cybersecure AI-Ready Middleware as a Differentiator for Regulated Labs

- 4.3 Market Restraints

- 4.3.1 High Capital Cost and Ongoing Service Contract Burden

- 4.3.2 Complex Validation, Interoperability, and LIMS Integration

- 4.3.3 Limited Skilled Workforce for Instrument Uptime and Advanced Assay Interpretation

- 4.3.4 Data Integrity, Cybersecurity, and AI Governance Concerns in Connected Laboratories

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.1.1 Automated Microbial Identification Systems

- 5.1.1.2 Automated Blood Culture Systems

- 5.1.1.3 Automated Colony Counters

- 5.1.1.4 Automated Sample Preparation Systems

- 5.1.1.5 Automated Antibiotic Susceptibility Testing Systems

- 5.1.1.6 Automated Microbiology Analyzers

- 5.1.1.7 Automated Incubators

- 5.1.1.8 Automated Media Preparation Systems

- 5.1.2 Reagents and Kits

- 5.1.3 Software

- 5.1.1 Instruments

- 5.2 By Automation Type

- 5.2.1 Fully Automated

- 5.2.2 Semi-Automated

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Biopharmaceutical Production

- 5.3.3 Environmental and Water Testing

- 5.3.4 Food and Beverage Testing

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals and Clinical Laboratories

- 5.4.2 Pharmaceutical and Biopharmaceutical Companies

- 5.4.3 Food and Beverage Manufacturers

- 5.4.4 Contract Research Organizations

- 5.4.5 Other End Users

- 5.5 By Diagnostic Technology

- 5.5.1 Molecular Diagnostics

- 5.5.2 Mass Spectrometry

- 5.5.3 Automated Imaging and Digital Microscopy

- 5.5.4 Flow Cytometry

- 5.5.5 Other Technologies

- 5.6 By Sample Type

- 5.6.1 Blood

- 5.6.2 Urine

- 5.6.3 Tissue

- 5.6.4 Other Sample Types

- 5.7 By Workflow

- 5.7.1 Pre-Analytical Process

- 5.7.2 Analytical Process

- 5.7.3 Post-Analytical Process

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East and Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East and Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Accelerate Diagnostics, Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 bioMerieux SA

- 6.3.5 Bio-Rad Laboratories, Inc.

- 6.3.6 Bruker Corporation

- 6.3.7 Charles River Laboratories International, Inc.

- 6.3.8 Clever Culture Systems Limited

- 6.3.9 Copan Diagnostics, Inc.

- 6.3.10 Danaher Corporation

- 6.3.11 DiaSorin S.p.A.

- 6.3.12 Merck KGaA

- 6.3.13 Neogen Corporation

- 6.3.14 QIAGEN N.V.

- 6.3.15 Rapid Micro Biosystems, Inc.

- 6.3.16 Roche Diagnostics International Ltd.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Sysmex Corporation

- 6.3.19 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment