|

시장보고서

상품코드

2072935

요실금 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Urinary Incontinence Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

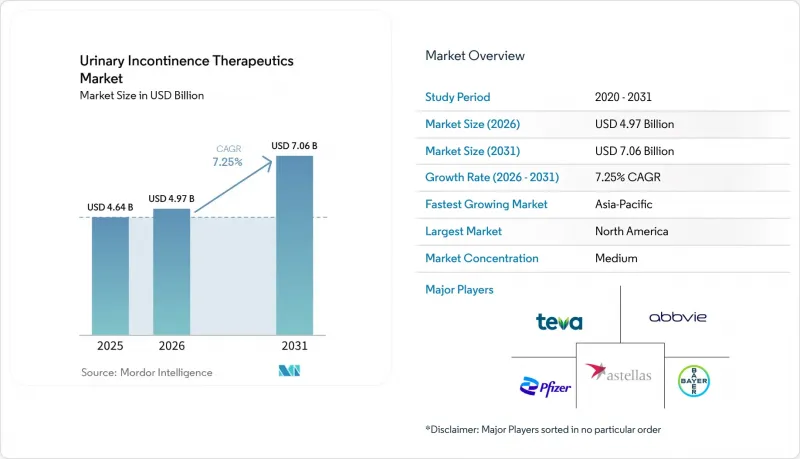

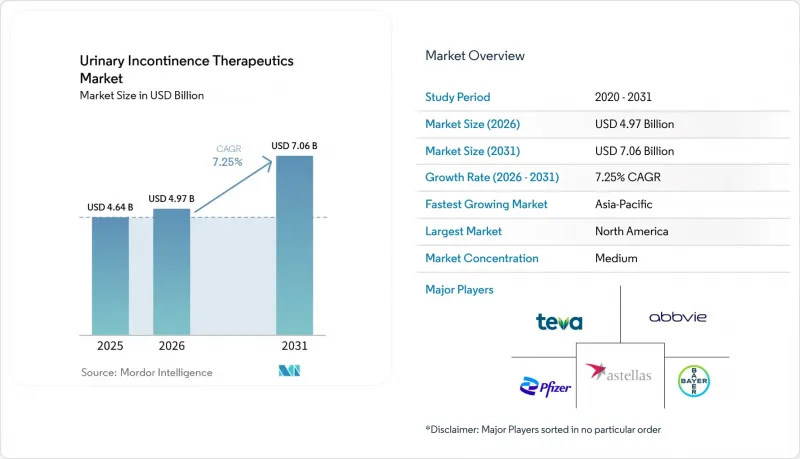

Mordor Intelligence에 의하면, 요실금 치료제 시장 규모는 2025년 46억 4,000만 달러, 2026년 49억 7,000만 달러에서 2031년까지 70억 6,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.25%를 나타낼 전망입니다.

본 보고서는 유형별(복압성, 절박성, 과다배출성, 기능성, 혼합성 요실금), 약물 분류별(항콜린제, β-3 작용제, α-차단제, 에스트로겐, 데스모프레신, 삼환계 항우울제, 기타), 성별(여성, 남성), 판매 채널(병원, 소매, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 요실금 치료제 시장 동향과 인사이트

고령화 및 동반 질환이 있는 집단에서 요실금 유병률 증가

국제요실금학회(International Continence Society)의 보고에 따르면, 20세 이상 성인 중 4억 2,300만 명 이상이 요실금으로 고통받고 있으며, 요실금 치료제 시장은 눈부신 성장을 이루고 있습니다. 노화는 중요한 요인으로, 나이가 들면서 방광 기능, 골반 지지력, 신경 조절 능력이 약해지는 경향이 있으며, 이것이 요실금 발생 증가로 이어지고 있습니다. 또한, 비만, 당뇨병, 신경계 질환의 유병률이 높아짐에 따라, 이러한 질환들이 요실금으로 인한 부담 증가의 한 원인이 되고 있습니다. 인구 고령화와 만성 질환이라는 이중적인 영향으로 인해, 1차 진료, 비뇨기과 및 비뇨기·부인과 현장에서 수요가 증가하고 있습니다. 중요한 점은 이 시장이 단순히 수요를 창출하는 데 그치지 않고, 눈에 띄게 확대되는 환자층을 진단 및 치료를 받은 사례로 능숙하게 전환하고 있다는 것입니다.

임신 및 산후 관리에 대한 인식 확대에 따른 여성 환자층의 확대

요실금 치료제 시장에서는 임신 및 출산 후 증상을 겪는 여성의 수가 매우 많다는 사실이 점점 더 널리 인식되고 있습니다. 질 분만 후 여성의 최대 33%가 산후 요실금을 겪고 있으며, 이는 현재 임상적으로 주목받고 있는 치료의 공백을 여실히 드러내고 있습니다. 골반저 관리가 산후 관리의 필수적인 요소로 자리 잡으면서, 여성들은 이전보다 더 이른 시기에 비뇨기과·산부인과 진료를 의뢰받게 되었습니다. 과거에는 많은 환자들이 단편적인 치료 과정을 거칠 수밖에 없었고, 이로 인해 치료가 수년이나 지연되기도 했던 점을 고려하면, 이는 주목할 만한 변화입니다. 이러한 움직임을 뒷받침하듯, 미국 비뇨기과·산부인과 학회는 초진 시 임상 상담 과정에서 일관된 상담을 실시할 것을 제안하며, 증상 및 치료 계획에 관한 시기적절한 논의를 장려하고 있습니다. 그 결과, 특히 체계적인 산후 관리 체계가 갖춰진 의료 시스템에서 여성을 위한 보다 명확한 치료 경로가 확립되었으며, 시장은 그 혜택을 누리고 있습니다.

사회적 편견으로 인한 보고 누락의 지속

요실금 치료제 시장은 보고 부족과 진단 지연이라는 과제에 직면해 있습니다. 유럽비뇨기과학회(EAU)의 보고에 따르면, 영국에서는 중등도에서 중증의 요실금을 앓고 있는 여성 중 의료 및 사회복지 서비스 지원을 요청한 비율은 3분의 1 미만에 그치고 있습니다. 사회적 편견으로 인해 많은 환자들이 정식 의료 서비스를 받는 것을 주저하고 있으며, 처방 치료보다는 생리대 사용, 생활 습관 개선, 혹은 자가 관리를 선택하는 사람들도 있습니다. 이 문제는 도시 지역이나 교육 수준이 높은 계층에서도 부끄러움 때문에 증상을 털어놓지 못하기 때문에 여전히 지속되고 있습니다. 또한, 각국의 의료 제도에서 시행되는 선별 검사의 방식에 차이가 있다는 점도 시장 성장을 더욱 제한하고 있습니다. 이는 1차 진료나 여성 건강검진을 받을 때에도 증상을 보고하는 것이 여전히 흔하지 않기 때문입니다.

부문별 분석

2025년, 스트레스성 요실금은 요실금 치료제 시장의 30.45%를 차지하며 계속해서 1위를 유지했습니다. 이러한 우위는 특히 출산 후 여성이나 호르몬 균형이 변화하는 시기를 겪고 있는 여성의 경우, 괄약근 약화나 골반저 기능 장애의 유병률이 높다는 점에 기인합니다. 임상의들은 확립된 치료 경로를 바탕으로, 이 분야에서 여전히 많은 환자를 관리하고 있습니다. 초기 치료는 행동 요법과 골반저근 강화에 중점을 두지만, 지속적이거나 일상생활에 지장을 주는 증상의 경우 약물 요법이 여전히 필수적입니다. 새로운 치료법이 점차 보급되고 있는 상황에서도 일관된 처방 패턴 덕분에 이 부문의 안정성이 확보되고 있습니다.

스트레스성 요실금은 산부인과, 1차 진료, 비뇨기과·산부인과 간의 빈번한 협력을 통해 치료에 관한 논의의 기회가 마련되고 있습니다. 이 분야는 출산이나 갱년기 같은 인생의 전환기와 관련이 있기 때문에 확실한 매출 확대의 원동력이 되고 있습니다. 혼합형 및 역류성 증상은 비교적 드물고 복잡하며, 대부분의 경우 여러 작용기전을 결합한 치료가 필요합니다. 기능성 요실금은 여전히 신경학적 또는 구조적 치료에 의존하고 있으며, 관련 의약품의 매출 잠재력은 제한적입니다. 한편, 절박성 요실금은 β-3 작용제 등의 치료법과 약물 요법에 대한 후속 관리 개선에 힘입어 2031년까지 연평균 성장률(CAGR) 7.66%로 성장할 것으로 전망됩니다.

2025년 기준으로, 항콜린제는 요실금 치료제 시장의 34.67%를 차지하며, 최대의 약물군으로서의 지위를 유지하고 있습니다. 이러한 우위는 옥시부티닌, 톨테로진, 솔리페나신과 같이 널리 사용되는 약물에 더해, 높은 비용 대비 효과와 폭넓은 보험 적용 범위에 의해 뒷받침되고 있습니다. 안전에 대한 우려가 커지고 있음에도 불구하고, 의사들이 이 약물군에 익숙해져 있다는 점도 새로운 치료법으로의 전환을 늦추고 있습니다. 그러나 항콜린제는 시장 점유율 면에서는 1위를 차지하고 있지만, 성장세 면에서는 다른 약물에 뒤처지고 있습니다.

β-3 아드레날린 수용체 작용제는 2031년까지 연평균 성장률(CAGR) 8.12%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 약물 군이 될 전망입니다. 이러한 부상은 내약성의 향상, 의사들의 신뢰도 증대, 그리고 최근 적응증 확대에 기인한 것입니다. 2024년 12월, 양성 전립선 비대증을 앓고 있는 남성을 대상으로 한 비베글론의 FDA 승인이 내려짐에 따라, 이 약물의 채택이 더욱 확대되었습니다. 에스트로겐, 데스모프레신, α-차단제, 삼환계 항우울제, 보툴리눔툭신(보톡스) 등 다른 약물군은 비록 틈새 시장이지만 중요한 역할을 계속 수행하며, 치료 기전의 다양성을 확보하고 있습니다.

지역별 분석

2025년, 북미는 요실금 치료제 시장의 40.08%를 차지하며 지역별로는 가장 큰 점유율을 기록했습니다. 높은 진단율, 광범위한 보험 적용 범위, 그리고 1차 진료와 비뇨기과 간의 탄탄한 의뢰 체계가 이러한 경쟁력을 뒷받침하고 있습니다. 미국은 확립된 처방 경로와 환자가 전문의의 진료를 받기 쉬운 환경 덕분에 여전히 주요 수익원으로 자리 잡고 있습니다. 2024년 12월, 양성 전립선 비대증에 따른 과활동성 방광 증상을 보이는 남성을 대상으로 한 비베글론의 FDA 승인이 내려짐에 따라, 처방 건수가 증가할 것으로 예측됩니다. 또한, 이 지역은 경쟁이 치열한 제네릭 시장에 힘입어, 브랜드 의약품 간의 경쟁이 격화되는 상황에서도 치료 건수를 유지하고 있습니다.

유럽 역시 여전히 중요한 시장이며, 독일, 영국, 프랑스가 처방량을 주도하고 있습니다. 유럽비뇨기과학회는 이 질환이 초래하는 사회경제적 부담과 조기 개입의 필요성을 강조하고 있습니다. 2024년 유럽집행위원회의 판매 승인을 계기로, 비베글론을 포함한 새로운 치료법에 대한 접근성이 개선되면서 치료 시장 경쟁 구도가 더욱 치열해지고 있습니다. 그러나 상환 정책과 각국 고유의 접근 경로가 기존 항콜린제에서 새로운 치료법으로의 전환에 계속해서 영향을 미치고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.95%를 기록하며 성장할 것으로 예상되며, 가장 높은 성장세를 보일 지역 부문이 될 전망입니다. 일본에서는 고령화가 진행됨에 따라 수요가 증가하고 있으며, 최신 경구용 치료제로의 전환이 진행되고 있습니다. 중국과 인도에서는 도시 지역의 진단 경로, 전문의에 대한 접근성, 약국 인프라의 개선이 성장에 기여하고 있습니다. 또한, 그동안 제대로 관리되지 않았던 증상에 대한 인식이 높아지고, 치료를 받으려는 의지가 강해짐에 따라 시장 확대에 더욱 박차를 가하고 있습니다. 중동 및 아프리카와 남미는 비교적 작은 시장이지만, 이 지역에서는 민간 클리닉 네트워크의 발전, 인식 제고 활동, 접근성 모델의 구축이 진행되고 있어 향후 성장 가능성이 부각되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the urinary incontinence therapeutics market size is projected to expand from USD 4.64 billion in 2025 and USD 4.97 billion in 2026 to USD 7.06 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

This report is Segmented by Type (Stress, Urge, Overflow, Functional, Mixed Incontinence), Drug Class (Anticholinergics, Beta-3 Agonists, Alpha Blockers, Estrogen, Desmopressin, Tricyclic Antidepressants, Others), Gender (Female, Male), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts are in Value (USD).

Global Urinary Incontinence Therapeutics Market Trends and Insights

Rising Prevalence of Urinary Incontinence in Aging and Comorbid Populations

With over 423 million adults aged 20 and above affected by urinary incontinence, as reported by the International Continence Society, the market for urinary incontinence therapeutics is witnessing significant growth. Aging plays a pivotal role, as bladder function, pelvic support, and neurological control tend to weaken with age, leading to increased instances of urinary incontinence. Furthermore, as obesity, diabetes, and neurological disorders become more prevalent, they contribute to the rising burden of urinary incontinence. This dual influence from demographic aging and chronic diseases bolsters demand in primary care, urology, and urogynecology settings. Importantly, the market isn't merely generating demand; it's adeptly converting a visible and expanding patient pool into diagnosed and treated cases.

Expanding Female Patient Pool After Pregnancy and Postpartum Care Recognition

The urinary incontinence therapeutics market is increasingly recognizing the significant number of women experiencing symptoms post-pregnancy and childbirth. Up to 33% of women face postpartum urinary incontinence after a vaginal delivery, highlighting a treatment gap that is now garnering clinical attention. As pelvic floor care becomes integral to maternity follow-ups, women are being referred for urogynecology evaluations earlier than before. This is a notable shift, considering many patients previously navigated fragmented care pathways and delayed therapy for years. Backing this movement, the American Urogynecologic Society has advocated for consistent counseling during initial clinical contacts, facilitating timely discussions on symptoms and treatment planning. Consequently, the market is benefiting from a more defined treatment pathway for women, especially in health systems with structured postpartum care.

Persistent Underreporting Due to Social Stigma

The urinary incontinence therapeutics market faces challenges due to underreporting and delayed diagnoses. The European Association of Urology reported that in the UK, fewer than one-third of women with moderate to severe urinary incontinence sought health or social services support. Stigma prevents many patients from accessing formal care, with some opting for pads, lifestyle changes, or self-management over prescription treatments. This issue persists even in urban and educated populations, where embarrassment deters disclosure. Inconsistent screening efforts across national health systems further limit market growth, as symptom reporting remains uncommon in primary care and women's health visits.

Other drivers and restraints analyzed in the detailed report include:

- Growing Uptake of Minimally Invasive and Novel Drug Delivery Approaches

- Wider Use of Beta-3 Agonists and Combination Pharmacotherapy Regimens

- Adherence Challenges Linked to Dry Mouth, Constipation, and Cognitive Side Effects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, stress incontinence accounted for 30.45% of the urinary incontinence therapeutics market, maintaining its leading position. This dominance stems from the high prevalence of sphincter weakness and pelvic floor dysfunction, particularly among women post-pregnancy and during hormonal transitions. Clinicians continue to manage a significant patient pool in this segment, supported by established care pathways. While initial treatments focus on behavioral and pelvic floor support, pharmacologic interventions remain essential for persistent or disruptive symptoms. Consistent prescribing patterns ensure the segment's stability, even as newer therapies gain traction.

Stress incontinence benefits from frequent consultations with gynecology, primary care, and urogynecology services, creating opportunities for treatment discussions. The segment is a reliable volume driver due to its association with life events like childbirth and menopause. Mixed and overflow presentations are less common and more complex, often requiring multi-mechanism treatments. Functional incontinence remains reliant on neurological or structural management, limiting its drug revenue potential. Urge incontinence, however, is projected to grow at a 7.66% CAGR through 2031, driven by therapies like beta-3 agonists and improved pharmacotherapy follow-ups.

Anticholinergics held 34.67% of the urinary incontinence therapeutics market in 2025, maintaining their position as the largest drug class. Their dominance is supported by widely used medications such as oxybutynin, tolterodine, and solifenacin, along with their cost-effectiveness and broad formulary presence. Physicians' familiarity with this class also slows the transition to newer options, despite growing safety concerns. However, while anticholinergics lead in market share, they lag in growth momentum.

Beta-3 adrenoceptor agonists are forecast to grow at an 8.12% CAGR through 2031, making them the fastest-growing drug class. Their rise is attributed to better tolerability, increased physician confidence, and recent label expansions. The December 2024 FDA approval for vibegron in men with benign prostatic hyperplasia has further strengthened their adoption. Other drug classes, including estrogen, desmopressin, alpha blockers, tricyclic antidepressants, and botulinum toxin, continue to play niche but important roles, ensuring diversity in therapeutic mechanisms.

Complete Report Scope:

- By Type

- Stress Incontinence

- Urge Incontinence

- Overflow Incontinence

- Functional Incontinence

- Mixed Incontinence

- By Drug Class

- Anticholinergics

- Beta-3 Adrenoceptor Agonists

- Alpha Blockers

- Estrogen

- Desmopressin

- Tricyclic Antidepressants

- Other Drug Classes

- By Gender

- Female

- Male

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 40.08% of the urinary incontinence therapeutics market, making it the largest regional contributor. High diagnosis rates, extensive insurance coverage, and strong referral systems between primary care and urology drive this dominance. The U.S. remains the primary revenue center due to established prescribing pathways and better patient access to specialist care. The FDA approval of vibegron in December 2024 for men with overactive bladder symptoms linked to benign prostatic hyperplasia is expected to boost prescriptions. Additionally, the region benefits from a competitive generic market, sustaining treatment volumes despite evolving branded competition.

Europe remains a significant market, with Germany, the UK, and France leading in prescription volumes. The European Association of Urology has emphasized the socioeconomic burden of the condition and the need for early intervention. Access to newer therapies, including vibegron, has improved following European Commission marketing authorization in 2024, enhancing the competitive treatment landscape. However, reimbursement policies and country-specific access pathways continue to influence the transition from older anticholinergics to newer options.

Asia-Pacific is projected to grow at a CAGR of 8.95% through 2031, making it the fastest-growing regional segment. Japan's aging population drives demand, with a shift toward modern oral therapies. China and India contribute to growth as diagnosis pathways, specialist access, and pharmacy infrastructure improve in urban areas. Increased awareness and a growing willingness to seek treatment for previously unmanaged symptoms further support market expansion. While the Middle East, Africa, and South America represent smaller segments, their developing private clinic networks, awareness initiatives, and access models highlight their potential for future growth.

- Abbvie

- Astellas Pharma

- Bayer

- Boehringer Ingelheim

- Dr. Reddy's Laboratories

- Ferring Pharmaceuticals

- GlaxoSmithKline

- Hisamitsu Pharmaceutical

- Lupin

- Pfizer

- Sanofi

- Sumitomo Pharma Co., Ltd.

- Teva Pharmaceutical Industries

- Viatris

- Zydus Lifesciences Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Urinary Incontinence in Older Adults

- 4.2.2 Expanding Female Patient Pool After Pregnancy and Menopause

- 4.2.3 Growing Uptake of Minimally Invasive and Non-Surgical Therapies

- 4.2.4 Wider Use of Beta-3 Agonists and Combination Pharmacotherapy

- 4.2.5 Underdiagnosis-to-Treatment Conversion Through Digital Screening and Tele-Urology

- 4.2.6 Treatment Adoption Driven by Care-Setting Shift to Home-Based Chronic Management

- 4.3 Market Restraints

- 4.3.1 Persistent Underreporting Due to Social Stigma and Low Care Seeking

- 4.3.2 Adherence Challenges Linked to Dry Mouth, Constipation, and Polypharmacy

- 4.3.3 Reimbursement Friction for Brand-Only and Device-Adjunct Regimens

- 4.3.4 Limited Real-World Differentiation Across Oral Therapies in Cost-Constrained Systems

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Type

- 5.1.1 Stress Incontinence

- 5.1.2 Urge Incontinence

- 5.1.3 Overflow Incontinence

- 5.1.4 Functional Incontinence

- 5.1.5 Mixed Incontinence

- 5.2 By Drug Class

- 5.2.1 Anticholinergics

- 5.2.2 Beta-3 Adrenoceptor Agonists

- 5.2.3 Alpha Blockers

- 5.2.4 Estrogen

- 5.2.5 Desmopressin

- 5.2.6 Tricyclic Antidepressants

- 5.2.7 Other Drug Classes

- 5.3 By Gender

- 5.3.1 Female

- 5.3.2 Male

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Astellas Pharma Inc.

- 6.3.3 Bayer AG

- 6.3.4 Boehringer Ingelheim International GmbH

- 6.3.5 Dr. Reddy's Laboratories Ltd.

- 6.3.6 Ferring B.V.

- 6.3.7 GlaxoSmithKline plc

- 6.3.8 Hisamitsu Pharmaceutical Co., Inc.

- 6.3.9 Lupin Limited

- 6.3.10 Pfizer Inc.

- 6.3.11 Sanofi

- 6.3.12 Sumitomo Pharma Co., Ltd.

- 6.3.13 Teva Pharmaceutical Industries Ltd.

- 6.3.14 Viatris Inc.

- 6.3.15 Zydus Lifesciences Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment