|

시장보고서

상품코드

2072952

GTM(Go-To-Market) 서비스 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Go-to-Market Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

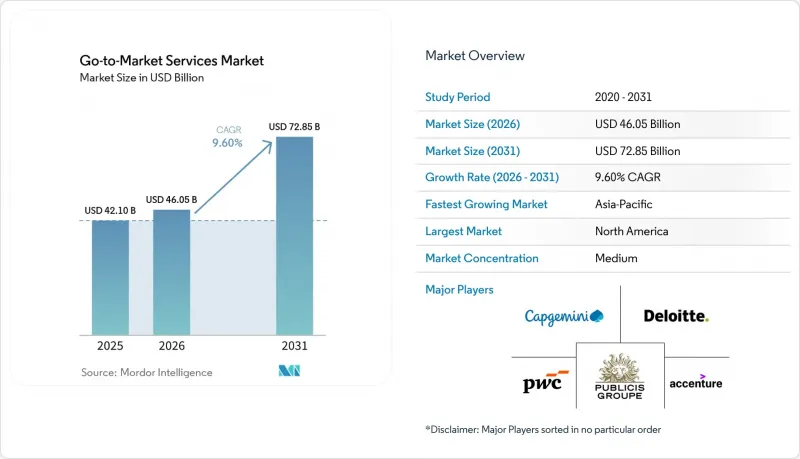

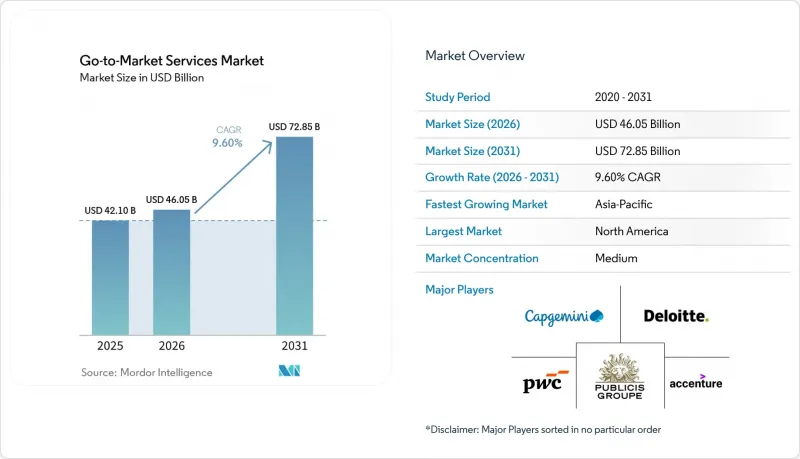

Mordor Intelligence에 따르면 GTM(Go-To-Market) 서비스 시장 규모는 2025년 421억 달러에서 2026년에는 460억 5,000만 달러로 확대되어 2031년까지 728억 5,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 9.60%로 성장할 것으로 전망됩니다.

본 보고서는 서비스 유형(GTM 전략 및 시장 진입, 포지셔닝 및 메시징 전략 등), 제공 모델(온사이트 제공, 원격 제공 등), 기업 규모(대기업, 중견기업 등), 최종 이용 산업(소매·E-Commerce, IT·통신, BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 GTM(Go-To-Market) 서비스 시장의 동향과 인사이트

AI 주도 영업·마케팅 혁신

GTM(Go-To-Market) 서비스 시장은 단순한 워크플로우 자동화를 넘어서는 심층적인 변화에 의해 주도되고 있습니다. 이는 생성형 AI와 에이전트형 AI가 계획, 참여, 측정의 근간을 이루는 기본 전제를 대체하고 있기 때문입니다. 포레스터는 이러한 변화를, 특히 마케팅, 영업, 고객 성공 부서가 여전히 서로 다른 시스템에서 운영되고, 구매자의 진행 상황에 대한 정의도 서로 다른 경우, 기존의 시장 진출 구조를 유지하기 어려워지는 전환점이라고 설명하고 있습니다. 이러한 변화가 중요한 이유는, AI를 통한 구매 행동으로 인해 기존의 수요 지표의 신뢰성이 떨어지기 때문입니다. 이로 인해 사내 팀이 기존의 활동 대시보드를 활용해 예산의 타당성을 설명하기는 어려워지는 반면, 전문 자문가는 측정 방법의 재설계나 실행 체계 구축과 관련된 업무를 수주하기가 더 쉬워집니다. 세일즈포스는 경영진이 영업 부문에서 생성형 AI를 통해 의미 있는 매출 증가를 기대하고 있지만, 그 성과는 영업, 마케팅, 서비스 부서 간의 긴밀한 협업에 달려 있으며, 많은 조직에서는 아직 그러한 체제가 갖춰지지 않았다고 지적하고 있습니다. 또한, EY가 2026년 3월 Snowflake 및 Canva와 공동으로 출시한 ‘에이전트형 영업 오케스트레이션 플랫폼’은 잠재 고객 발굴, 가격 책정 지원, 계약 자동화가 이제 단일 상업 워크플로로 통합되고 있음을 보여주며, 이로 인해 도입의 복잡성이 높아지고 있습니다. 이러한 상황에서 시장 진입 서비스 시장에서는 고립된 도구나 단기적인 실험 지원만을 제공하는 업체가 아니라, AI 오케스트레이션을 실제 수익 창출 업무와 연계할 수 있는 업체가 높이 평가받고 있습니다.

옴니채널 구매와 영업 간의 연계에 대한 수요

또한, B2B 구매 활동이 더 많은 채널과 정보원으로 확대되면서, 구매자가 단편적인 접근 방식이 아닌 일관성을 기대하는 경우가 늘어나고 있는 점도 GTM(Go-To-Market) 서비스 시장에 호재가 되고 있습니다. 가트너는 2026년 5월 보고서에서, 구매자들이 구매 시 여러 정보원을 활용하고 있으며, 45%가 최근 거래에서 생성형 AI를 사용한 반면, 69%는 중요한 단계에서 AI가 생성한 정보의 타당성을 확인하기 위해 여전히 영업 담당자와 상의하고 있었다고 보고했습니다. 이 조사 결과는 디지털 셀프서비스가 확대되고 있더라도, 거래 규모가 커지거나 기술적 요소가 강화되거나 위험이 높아지는 경우, 사람이 직접 검증할 필요가 없어지는 것은 아니라는 단순한 상업적 현실을 뒷받침하고 있습니다. Hokodo의 조사에 따르면, 유럽의 B2B 구매 담당자들은 여러 가지 서로 다른 영업 채널을 원하며, 신속하고 간단하며 정확한 디지털 경험을 기대하고 있는 것으로 나타났습니다. 이는 채널 설계, 데이터 흐름, 영업 담당자의 준비 태세를 통합적으로 재구축할 수 있는 GTM 전문가에 대한 수요를 촉진하는 요인입니다. 포레스터사는 이미 100만 달러를 초과하는 대규모 B2B 거래의 절반 이상이 디지털 셀프서비스 채널을 통해 이루어지게 될 것이라고 지적한 바 있습니다. 이는 신뢰성, 규정 준수, 거래 구조가 가장 중요한 국면에 한해 영업 담당자가 주도하는 교류가 이루어지도록 되어 있음을 의미합니다. 그 결과, GTM(Go-To-Market) 서비스 시장에서는 채널 아키텍처, RevOps 재설계, 그리고 현장 역량 강화를 하나의 연계된 프로그램으로 포괄적으로 다루는 업무에 대한 수요가 지속되고 있습니다.

예산 축소와 프로젝트 기반 조달

GTM(Go-To-Market) 서비스 시장은 고객사의 지출 억제라는 압박에 계속해서 직면하고 있습니다. 특히, 이사회가 보다 명확한 수익 성과를 요구하는 반면 운영 예산은 여전히 제한되어 있는 경우 그 경향이 두드러집니다. 가트너의 '2025년 CMO 지출 조사'에 따르면, 마케팅 예산은 기업 수익의 7.7%로 정체 상태를 이어가고 있으며, 많은 최고 마케팅 책임자(CMO)들이 제한된 자원으로 더 많은 성과를 내야 하는 상황에 놓여 있는 것으로 나타났습니다. 이러한 환경 속에서 많은 바이어들은 기간이 정해지지 않은 리테이너 계약에서 단기간의 마일스톤 기반 계약으로 전환하고 있습니다. 이로 인해 서비스 제공업체는 가치를 더 신속하게 입증해야 하며, 동일한 계약 내에서 더 많은 상업적 위험을 감수하게 됩니다. 애널리틱 파트너스는 2026년 2월, 고위 의사결정자들이 예산 배분 과정에서 계량경제 모델과 비즈니스 분석을 더욱 중시하고 있다고 보고했습니다. 이로 인해, 측정 가능한 기여도를 입증하지 못하는 GTM 제공업체에 대한 선정 기준은 더욱 엄격해지고 있습니다. 펩시코 역시 2025년 공시 자료를 통해 각 지출 부문의 생산성 향상과 연계하여 광고비를 5억 달러 삭감했음을 밝히며, 이와 같은 효율화 추세를 뒷받침했습니다. GTM(Go-To-Market) 서비스 시장에서, 이로 인해 수요가 사라지는 것은 아니지만, 계약 규모는 축소되고 승인 주기는 길어지며, 벤더는 판매 시점에 더 명확한 ROI를 제시해야 하는 상황에 처하게 되었습니다.

부문별 분석

2025년, 수요 창출 및 리드 생성은 GTM(Go-To-Market) 서비스 시장 점유율의 25.67%를 차지했습니다. 이는 구매 행동이 더 이상 직선적이지 않고, 기존의 아웃리치 모델에 대한 반응이 둔화되었음에도 불구하고, 파이프라인 구축이 여전히 예산 배분의 최우선 과제였음을 보여줍니다. 이사회가 계속해서 파이프라인 커버리지, 계약 성사율의 철저한 관리, 그리고 프로젝트 흐름의 가시성이라는 관점에서 영업팀을 평가함에 따라, 포트폴리오의 이 부분은 견조한 모습을 유지했습니다. 이 모든 것이 퍼널의 업스트림 단계에서의 지원을 지출 결정의 핵심으로 계속 자리매김하게 했습니다. 광의의 시장 진입 서비스 업계에서 GTM 전략 및 시장 진입, 포지셔닝과 메시징, 제품 출시와 상품화는 여전히 중요한 역할을 담당하고 있었습니다. 이는 기업들이 AI를 활용한 제안을 명확한 상업적 스토리로 전환하기 위한 지원이 필요했기 때문입니다. 또한, 기존의 파트너 모델에 디지털 셀프서비스가 결합되면서 관리가 어려워졌던 직접 판매와 간접 판매를 결합한 하이브리드 유통 경로를 재검토하려는 움직임이 확산되는 가운데, 채널 파트너 및 유통 전략과 관련된 업무의 중요성도 커졌습니다. '기타' 부문은 규모는 작았지만, AI가 개입하는 환경에서 구매 경로에 영향을 미치는 포지셔닝 재검토나 애널리스트 관계 관리 지원 등 상업적으로 중요한 업무를 담당하고 있었습니다.

세일즈 이네이블먼트 및 go-to-sales 지원 시장은 2031년까지 연평균 성장률(CAGR) 15.86%로 확대될 것으로 예상되며, 고객들이 도구 구매에서 도입 지원으로 관심을 전환함에 따라 GTM(Go-To-Market) 서비스 시장에서 가장 빠르게 성장하는 서비스 유형이 될 전망입니다. 2026년 IDC MarketScape의 ‘생명과학 연구개발(R&D) 전략 컨설팅’ 부문에서 ZS가 차지한 위치와 이 회사의 보다 광범위한 상용 AI 서비스는, 이모빌리테이션이 더 이상 콘텐츠 라이브러리나 교육 세션에만 국한되지 않는 시장을 시사하고 있습니다. Highspot이 제공하는 생명과학 및 헬스케어 분야의 AI 영업 지원 관련 자료에 따르면, 코칭, 상황에 맞는 콘텐츠 제공, 워크플로우 통합이 더욱 깊이 통합된 준비 모델의 일부로 자리 잡고 있는 것으로 나타났습니다. 핵심 과제는 많은 기업이 관리자나 영업 담당자가 이를 소화할 수 있는 속도보다 빠르게 플랫폼을 도입한 데 있으며, 그 결과 행동 변화, 프로세스 설계, 그리고 관리자 주도의 정착 지원에 대한 외부 지원 수요가 확대되었습니다. 사실, 서비스 시장 진입 분야에서는 단순한 소프트웨어 접근보다 도입 및 실행에 대한 체계가 더 중요시되게 되면서, 이네이블먼트의 성장세가 시장 전체를 웃도는 속도로 진행되고 있습니다.

2025년 GTM(Go-To-Market) 서비스 시장 규모 중 하이브리드형 제공이 38.81%를 차지했습니다. 이는 기업들이 단일한 업무 형태에 의존하기보다는, 현장 근무의 접근성과 원격 근무의 효율성을 결합한 모델을 계속해서 선호하고 있음을 반영합니다. 이 방식은 경영진의 신뢰, 신속한 반복, 실질적인 변화 지원이 필요한 활동, 특히 프로젝트가 가격 책정, 영업 프로세스, 파트너 관리, 고객 참여를 동시에 다루는 경우에 효과적입니다. 현장 지원은 위험이 높은 '월룸' 상황, 경영진의 의견 조율, 그리고 워크숍 및 이해관계자의 직접적인 참여를 통해 실행의 질을 향상시킬 수 있는 복잡한 재설계 작업에서 여전히 중요합니다. 원격 제공은 보다 광범위한 실행 지원, 중규모 프로그램 관리, 그리고 분산형 협업이 업무상의 표준이 된 워크스트림에서 계속해서 중요하게 여겨지고 있습니다. 이러한 전반적인 추세를 통해, GTM(Go-To-Market) 서비스 시장에서는 속도와 책임성을 저해하지 않으면서도 인력 배치와 제공 방식을 유연하게 조정할 수 있는 공급업체가 선호되었습니다.

매니지드 딜리버리 시장은 2031년까지 연평균 성장률(CAGR) 15.43%로 확대될 것으로 예상되며, 이는 GTM(Go-To-Market) 서비스 시장에서 일회성 자문에서 지속적인 운영 지원으로의 더 깊은 전환이 일어나고 있음을 보여줍니다. 맥킨지가 2026년 1월 AWS와 공동으로 출시한 서비스는 대기업들이 전략적 계획과 플랫폼 실행, 그리고 측정 가능한 비즈니스 가치를 결합하는 공동 혁신 모델로 전환하고 있음을 보여주었습니다. 이러한 움직임은, 특히 일회성 제안이 아닌 지속적인 조정이 필요한 AI 프로그램의 경우, 시간이나 인력 투입량보다는 성과와 밀접하게 연동된 요금 체계를 원하는 고객의 수요를 반영하고 있습니다. 또한, 매니지드 딜리버리는 고객이 안정적인 서비스 관계 속에서 조직의 노하우를 유지하는 데에도 도움이 됩니다. 이는 수익 창출, 수요 창출 및 역량 강화가 분기마다 개선될 것으로 기대되는 상황에서 중요한 요소입니다. 프로바이더의 경우, GTM(Go-To-Market) 서비스 시장에서는 지속적인 GTM 기능을 운영하면서 동시에 고객의 KPI에 대해 측정 가능한 성과를 입증할 수 있는 기업이 높이 평가받고 있습니다.

지역별 분석

2025년, 북미는 GTM(Go-To-Market) 서비스 시장 점유율의 47.02%를 차지했으며, 이 지역은 기업용 기술 수요가 집중되어 있을 뿐만 아니라 AI의 조기 도입이 진행되고 있어, 안목 있는 구매자들의 대규모 도입 기반을 갖추고 있어 명확한 수익의 중심지로 자리매김하고 있습니다. 미국은 여전히 GTM(Go-To-Market) 서비스 시장에서 가장 큰 기여를 하는 국가이며, 한편 기업들이 북미에서 사업을 확장함에 따라 현지 상황에 맞춘 상업적 실행이 필요해지면서 캐나다와 멕시코도 중요한 지원 역할을 수행했습니다. 니어쇼어링의 동향에 따라 제조 및 기술 기업들이 시장 진출 지원, 파트너 발굴, 현지 시장 진출 전략 수립을 필요로 하는 지역적 상업적 입지를 확립하고 강화함에 따라 멕시코의 중요성은 더욱 높아졌습니다. 북미의 GTM(Go-To-Market) 서비스 시장은 실리콘밸리, 뉴욕, 보스턴과 같은 거점 주변에 AI 네이티브 전문 기업들이 밀집해 있다는 점에서도 혜택을 입어, 서비스 제공 속도와 경쟁 심화 모두 가속화되었습니다. 동시에, 디지털 광고 및 정보 공개에 대한 기대의 변화에 따라, 대규모 기업 고객을 대상으로 한 규정 준수를 중시하는 사업화 지원에 대한 수요가 높아졌습니다.

유럽은 GTM(Go-To-Market) 서비스 시장에서 성숙 단계에 접어들었음에도 여전히 중요한 위치를 차지하고 있으며, 독일, 영국, 프랑스는 AI 도입, 옴니채널 재설계, 규제 준수형 사업 전개 분야에서 주요 수요 거점으로 두각을 나타냈습니다. 영국 및 EU 전역에서 사업을 전개하는 기업들은, 특히 데이터 거버넌스, AI 관련 규제, 국경을 초월한 사업 확장 계획을 단일 비즈니스 모델 내에서 조율해야 하는 경우, 채널 및 규정 준수 측면에서 계속해서 복잡성에 직면해 왔습니다. 스페인과 이탈리아는 시장 진출 지원 서비스 시장에서 아직 개척되지 않은 기회를 품고 있었습니다. 이는 현지 기업들이 국내 비용 관리를 유지하면서 인근 지역으로의 확장을 위한 지원을 점점 더 많이 요구하게 되었기 때문입니다. 남미는 절대적인 규모 면에서는 여전히 작은 수준을 유지했으나, 브라질, 아르헨티나, 칠레는 다국적 기업의 진출 프로그램과 디지털 주도형 국내 시장 확대에서 계속해서 주요 초점으로 남아 있었습니다. 남미 전역에 걸친 규제 차이로 인해 실사, 포지셔닝, 현지화 업무의 중요성은 여전히 유지되었으며, 프로젝트 일정이 제각각이라 하더라도 전문 자문가가 활약할 여지는 남아 있었습니다.

아시아태평양은 디지털 전환과 국경을 초월한 투자가 수요를 지속적으로 견인함에 따라, 2031년까지 연평균 성장률(CAGR) 14.48%를 기록할 것으로 예상되며, 시장 진입 지원 서비스 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 인도에서 AI를 적극적으로 도입하는 추세와, 중국이 사업 확장의 ‘목적지’이자 동시에 ‘출발점’으로서의 역할을 수행하고 있다는 점에 따라, 현지 실행 지원, 파트너 전략, 시장에 특화된 메시징에 대한 수요가 높아지고 있습니다. 일본과 싱가포르 역시 이 지역의 비즈니스 기회를 창출하고 있으며, 일본은 산업 정책 지침을 통해 계획 주기에 영향을 미치고, 싱가포르는 동남아시아 내 사업 전개 프로그램의 주요 거점 역할을 하고 있습니다. 중동에서는 UAE, 사우디아라비아, 카타르가 기업 혁신 의제에서 강력한 수요를 이끌고 있으며, 아프리카는 여전히 초기 단계에 있는 시장도 있지만, 디지털 상거래 인프라와 모바일 우선 구매 행태가 지속적으로 개선되고 있는 남아프리카공화국, 이집트, 나이지리아 등의 시장을 통해 성장하고 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.07.09According to Mordor Intelligence, the go-to-market services market size is expected to increase from USD 42.1 billion in 2025 to USD 46.05 billion in 2026 and reach USD 72.85 billion by 2031, growing at a CAGR of 9.60% over 2026-2031.

This report is Segmented by Service Type (GTM Strategy and Market Entry, Positioning and Messaging Strategy, and More), Delivery Model (Onsite Delivery, Remote Delivery, and More), Enterprise Size (Large Enterprises, Mid-Sized Enterprises, and More), End-Use Industry (Retail and E-Commerce, IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Go-to-Market Services Market Trends and Insights

AI-Led Sales and Marketing Transformation

The go-to-market services market is being pushed forward by a deeper change than simple workflow automation, because generative and agentic AI are replacing core assumptions behind planning, engagement, and measurement. Forrester described this shift as a point where older go-to-market structures become difficult to sustain, especially when marketing, sales, and customer success still operate on separate systems and separate definitions of buyer progress. This change matters because AI-mediated buying weakens older demand metrics, which makes it harder for internal teams to defend spend using legacy activity dashboards and easier for specialist advisers to win work around measurement redesign and execution discipline. Salesforce highlighted that business leaders expect meaningful revenue gains from generative AI in commercial functions, but those gains depend on tight coordination across sales, marketing, and service, which many organizations still do not have in place. EY's March 2026 launch of an agentic sales orchestration platform with Snowflake and Canva also showed how prospecting, pricing support, and contract automation are now being tied together in a single commercial workflow, raising the complexity of implementation. In this setting, the go-to-market services market is rewarding providers that can connect AI orchestration to real revenue operations, rather than those that only offer isolated tools or short-term experimentation support.

Omnichannel Buying and Sales Alignment Demand

The go-to-market services market is also benefiting from the fact that B2B buying is now spread across more channels, more information sources, and more moments where buyers expect continuity rather than disconnected outreach. Gartner reported in May 2026 that buyers used multiple information sources during a purchase and that 45% had used generative AI in a recent transaction, yet 69% still turned to sales representatives to validate AI-generated information at critical stages. That finding supports a simple commercial reality, digital self-service is expanding, but it does not remove the need for human validation when deals become larger, more technical, or more risky. Hokodo found that European B2B buyers wanted several distinct sales channels and expected digital experiences that were fast, simple, and accurate, which reinforces demand for GTM specialists who can rebuild channel design, data flow, and seller readiness together. Forrester had already signaled that more than half of large B2B transactions above USD 1 million would move through digital self-serve channels, which means seller-led interactions are being reserved for the points where confidence, compliance, and deal structure matter most. As a result, the go-to-market services market is seeing sustained demand for work that spans channel architecture, RevOps redesign, and front-line enablement in one connected program.

Budget Compression and Project-Based Procurement

The go-to-market services market continues to face pressure from tighter client spending, especially when boards demand clearer revenue outcomes while leaving operating budgets constrained. Gartner's 2025 CMO Spend Survey showed that marketing budgets remained stalled at 7.7% of company revenue and that many chief marketing officers were being asked to do more with less. In that environment, many buyers are shifting away from open-ended retainers and toward short, milestone-based engagements that require providers to prove value faster and carry more commercial risk within the same contract. Analytic Partners reported in February 2026 that senior decision-makers were leaning more heavily on econometric models and commercial analytics for budget allocation, which raises the screening threshold for any GTM provider that cannot demonstrate a measurable contribution. PepsiCo reinforced the same efficiency mood when its 2025 disclosures pointed to a USD 500 million advertising reduction tied to productivity gains across spending categories. For the go-to-market services market, this does not remove demand, but it does compress deal size, lengthen approval cycles, and push vendors toward clearer ROI framing at the point of sale.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border Expansion and Localization Needs

- Pricing and Monetization Redesign for AI and Subscription Offers

- In-House Martech and AI Teams Reducing Outsourced Execution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Demand generation and lead generation held 25.67% of the go-to-market services market share in 2025, which shows that pipeline creation remained the first budget priority even as buying behavior became less linear and less responsive to older outreach models. This part of the portfolio stayed resilient because boards continued to judge commercial teams on pipeline coverage, conversion discipline, and deal flow visibility, all of which kept top-of-funnel support central to spending decisions. Within the broader go-to-market service industry, GTM strategy and market entry, positioning and messaging, and product launch and commercialization retained a premium role because enterprises needed help translating AI-enabled offers into clear commercial narratives. Channel partner and distribution strategy work also gained relevance as companies revisited hybrid direct and indirect routes that had become harder to govern once digital self-serve motions were layered onto existing partner models. The others segment remained smaller, but it captured commercially important mandates such as positioning refreshes and analyst relations support that influenced buying pathways in a more AI-mediated environment.

Sales enablement and go-to-sales support is projected to expand at a 15.86% CAGR through 2031, making it the fastest-growing service type in the go-to-market services market as clients shift from tool buying to adoption support. ZS's positioning in the 2026 IDC MarketScape for life sciences R&D strategic consulting and its wider commercial AI offerings point to a market where enablement is no longer limited to content libraries and training sessions. Highspot's documentation around AI sales enablement for life sciences and healthcare shows that coaching, contextual content delivery, and workflow integration are becoming part of a more embedded readiness model. The core issue is that many companies adopted platforms faster than managers and sellers could absorb them, which expanded demand for external support around behavior change, process design, and manager-led reinforcement. In effect, the go-to-market services market is seeing enablement grow faster than the overall category because adoption and execution discipline now matter more than simple software access.

Hybrid delivery accounted for 38.81% of the go-to-market services market size in 2025, reflecting continued enterprise preference for models that combine on-site access with remote efficiency rather than relying on only one mode of engagement. This format works well for mandates that need executive trust, rapid iteration, and hands-on change support, especially when projects touch pricing, sales process, partner management, and customer engagement at the same time. On-site delivery still matters for high-stakes war-room situations, leadership alignment, and complex redesign work where workshops and direct stakeholder management can improve execution quality. Remote delivery remained important for broader execution support, mid-tier program management, and workstreams where distributed collaboration has become operationally normal. Across these patterns, the go-to-market services market favored providers that could flex staffing and delivery design without weakening speed or accountability.

Managed delivery is projected to advance at a 15.43% CAGR through 2031, and this marks a deeper shift in the go-to-market services market from episodic advisory toward recurring operating support. McKinsey's January 2026 launch with AWS showed how major firms are moving toward joint transformation models that link strategic planning to platform execution and measurable business value. That move reflects client demand for fee structures tied more closely to outcomes and less to time and staffing inputs, especially in AI programs that need continuous tuning rather than one-time recommendations. Managed delivery also helps clients keep institutional knowledge inside a stable service relationship, which matters when revenue operations, demand generation, and enablement are expected to improve quarter after quarter. For providers, the go-to-market services market is rewarding those that can operate ongoing GTM functions while proving measurable performance against client KPIs.

Complete Report Scope:

- By Service Type

- Strategy and Planning (includes GTM Strategy, Market Entry, Positioning and Messaging Strategy)

- Product Launch and Commercialization

- Channel Partner and Distribution Strategy

- Demand Generation and Lead Generation

- Sales Enablement and Go-to-Sales Support

- Other Service Types

- By Delivery Model

- Onsite Delivery

- Remote Delivery

- Hybrid Delivery

- Managed Delivery

- By Enterprise Size

- Large Enterprises

- Mid-sized Enterprises

- Small Enterprises

- By End-use Industry

- Retail and E-commerce

- Consumer Goods and Beauty

- Media and Entertainment

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Other End-use Industries (Education, Travel and Hospitality, Industrial, Automotive)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 47.02% of the go-to-market services market share in 2025, making it the clear revenue center because the region combines dense enterprise technology demand with early AI adoption and a large installed base of sophisticated buyers. The United States remained the largest national contributor in the go-to-market services market, while Canada and Mexico added meaningful support as companies expanded North American operations and needed localized commercial execution. Mexico gained added relevance as nearshoring trends encouraged manufacturing and technology firms to establish or deepen regional commercial footprints that required market entry support, partner development, and local route-to-market planning. The go-to-market services market in North America also benefited from the density of AI-native boutiques around hubs such as Silicon Valley, New York, and Boston, which raised both delivery speed and competitive intensity. At the same time, evolving digital advertising and disclosure expectations increased the need for compliance-aware commercialization support across larger enterprise accounts.

Europe remained a mature but still meaningful part of the go-to-market services market, with Germany, the United Kingdom, and France standing out as the main demand centers for AI adoption, omnichannel redesign, and regulated commercial execution. Companies operating across the UK and EU continued to face channel and compliance complexity, especially when data governance, AI rules, and cross-border expansion plans had to be coordinated in a single commercial model. Spain and Italy represented underpenetrated opportunities in the go-to-market services market because local enterprises increasingly sought support for expansion into neighboring regions while still managing cost discipline at home. South America stayed smaller in absolute terms, but Brazil, Argentina, and Chile remained the main focal points for multinational entry programs and digitally led domestic expansion. Regulatory variability across South America kept diligence, positioning, and localization work important, which preserved room for specialist advisers even when project timing was uneven.

Asia-Pacific is projected to register a 14.48% CAGR through 2031, making it the fastest-growing region in the go-to-market services market as digital transformation and cross-border investment continue to lift demand. India's strong AI adoption profile and China's role as both a destination and a source of commercial expansion are widening the need for local execution support, partner strategy, and market-specific messaging. Japan and Singapore are also shaping the regional opportunity, with one influencing planning cycles through industrial policy guidance and the other acting as a preferred operating base for Southeast Asian commercialization programs. In the Middle East, the UAE, Saudi Arabia, and Qatar are drawing stronger demand from enterprise transformation agendas, while Africa remains earlier stage but is expanding through markets such as South Africa, Egypt, and Nigeria where digital commercial infrastructure and mobile-first buying behavior continue to improve.

- Deloitte Touche Tohmatsu Limited

- Accenture plc

- PricewaterhouseCoopers International Limited

- Publicis Groupe S.A.

- Capgemini SE

- International Business Machines Corporation

- Ernst & Young Global Limited

- KPMG International Limited

- Bain & Company, Inc.

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Simon-Kucher & Partners Strategy & Marketing Consultants GmbH

- ZS Associates, Inc.

- Cognizant Technology Solutions Corporation

- Infosys Limited

- Wipro Limited

- Tata Consultancy Services Limited

- NMS Consulting, Inc.

- Oliver Wyman, Inc.

- P&C Global, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Led Sales and Marketing Transformation

- 4.2.2 Omnichannel Buying and Sales Alignment Demand

- 4.2.3 Cross-Border Expansion and Localization Needs

- 4.2.4 Pricing and Monetization Redesign for AI and Subscription Offers

- 4.2.5 Agent-Engine Optimization and Machine-Readable Offer Design

- 4.2.6 Channel Governance for Hybrid Direct and Partner Routes

- 4.3 Market Restraints

- 4.3.1 Budget Compression and Project-Based Procurement

- 4.3.2 In-House Martech and AI Teams Reducing Outsourced Execution

- 4.3.3 Data Governance and Agentic AI Readiness Gaps

- 4.3.4 Channel Conflict and Discount Leakage Across Routes-to-Market

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Strategy and Planning (includes GTM Strategy, Market Entry, Positioning and Messaging Strategy)

- 5.1.2 Product Launch and Commercialization

- 5.1.3 Channel Partner and Distribution Strategy

- 5.1.4 Demand Generation and Lead Generation

- 5.1.5 Sales Enablement and Go-to-Sales Support

- 5.1.6 Other Service Types

- 5.2 By Delivery Model

- 5.2.1 Onsite Delivery

- 5.2.2 Remote Delivery

- 5.2.3 Hybrid Delivery

- 5.2.4 Managed Delivery

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Mid-sized Enterprises

- 5.3.3 Small Enterprises

- 5.4 By End-use Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Consumer Goods and Beauty

- 5.4.3 Media and Entertainment

- 5.4.4 IT and Telecom

- 5.4.5 BFSI

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Other End-use Industries (Education, Travel and Hospitality, Industrial, Automotive)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Deloitte Touche Tohmatsu Limited

- 6.4.2 Accenture plc

- 6.4.3 PricewaterhouseCoopers International Limited

- 6.4.4 Publicis Groupe S.A.

- 6.4.5 Capgemini SE

- 6.4.6 International Business Machines Corporation

- 6.4.7 Ernst & Young Global Limited

- 6.4.8 KPMG International Limited

- 6.4.9 Bain & Company, Inc.

- 6.4.10 McKinsey & Company, Inc.

- 6.4.11 Boston Consulting Group, Inc.

- 6.4.12 Simon-Kucher & Partners Strategy & Marketing Consultants GmbH

- 6.4.13 ZS Associates, Inc.

- 6.4.14 Cognizant Technology Solutions Corporation

- 6.4.15 Infosys Limited

- 6.4.16 Wipro Limited

- 6.4.17 Tata Consultancy Services Limited

- 6.4.18 NMS Consulting, Inc.

- 6.4.19 Oliver Wyman, Inc.

- 6.4.20 P&C Global, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment