|

시장보고서

상품코드

2072958

AI 기반 에너지 관리 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

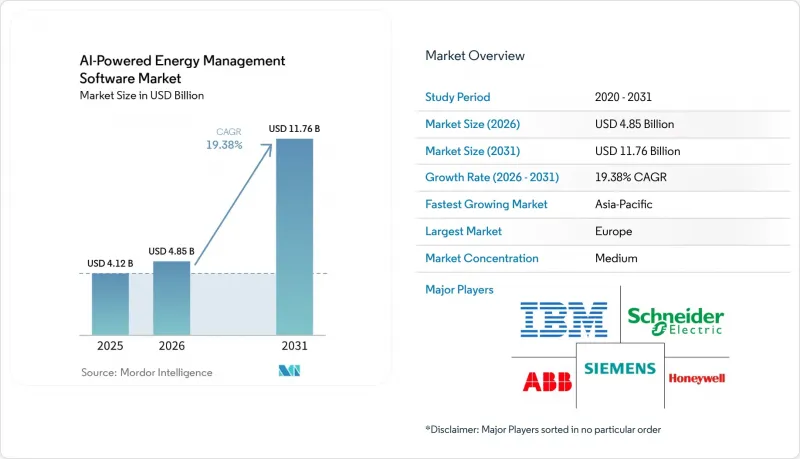

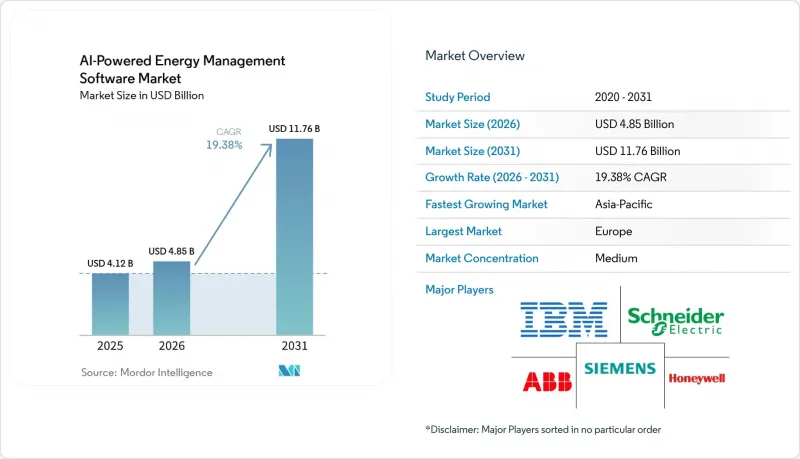

Mordor Intelligence에 의하면, AI 기반 에너지 관리 소프트웨어 시장 규모는 2025년 41억 2,000만 달러로 평가되었고, 2026년에는 48억 5,000만 달러로 추정되고, 2026-2031년 CAGR 19.38%로 성장을 지속할 전망이며, 2031년에는 117억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형), 용도별(에너지 소비 및 수요 최적화, 자산 성능 및 예측 유지보수 등), 최종 사용자별(유틸리티, 상업용 건물, 산업 시설 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 AI 기반 에너지 관리 소프트웨어 시장 동향 및 인사이트

상업시설 및 산업 시설에서 실시간 에너지 최적화에 대한 수요가 증가하고 있습니다.

실시간 최적화는 소프트웨어를 수동적인 보고서 작성 도구에서 능동적인 운영 도구로 전환하기 때문에 AI 기반 에너지 관리 소프트웨어 시장에서 단기적으로는 가장 명확한 가치 창출 요인으로 부상하고 있습니다. 상업 및 산업 분야 사용자들은 전력 가격 변동이 심해지고, 시간대별 요금제의 적용 범위가 확대됨에 따라, 가동 시간에 영향을 주지 않으면서도 피할 수 있는 피크 수요를 줄여야 한다는 내부적인 압박이 커지고 있습니다. 따라서 고정된 규칙이 아닌, 실시간 가격, 생산 주기 및 변화하는 현장 상황에 맞추어 부하 일정을 조정해야 하는 시설에서 AI 기반 에너지 관리 소프트웨어 시장이 성장세를 보이고 있습니다. 2026년 연구에 따르면, 생산 일정을 입력으로 활용한 일정 대응형 XGBoost 모델은 RMSE 2.67 kW, R² 0.9698을 달성했으며, 이는 내부 센서에 의한 완전한 가시성에 의존하지 않고도 다중 라인 산업 환경에서 고정밀 예측이 가능함을 입증하고 있습니다. 플랜트 데이터가 불완전하여 기존 최적화 도구의 효과가 제한되기 쉬운 실제 운영 환경에서 AI를 활용할 수 있게 해준다는 점에서 이러한 성능은 중요합니다. 변동이 심한 요금 대역에서 수요 요금 절감 및 에너지 사용량 안정화를 목표로 하는 시설이 늘어남에 따라, AI 기반 에너지 관리 소프트웨어 시장은 장기적인 지속가능성 프로젝트보다 일상적인 운영 비용 절감과 점점 더 밀접하게 연결되고 있습니다.

스마트 그리드 및 분산형 에너지 자원과의 AI 통합

분산형 에너지 자원의 부상 또한 AI 기반 에너지 관리 소프트웨어 시장의 성장을 뒷받침하고 있습니다. 현재 전력망의 상황은 옥상 태양광 발전, 배터리, 전기차 충전, 그리고 끊임없는 조정이 필요한 유연한 부하에 의해 형성되고 있기 때문입니다. 전력의 흐름이 양방향으로 바뀌고, 소수의 집중형 발전 거점이 아닌 수천 개에 달하는 소규모 자산 전반에 걸쳐 의사결정을 내려야 하는 경우, 기존의 발전 제어 로직으로는 대응하기 어려워집니다. 이러한 변화로 인해, AI 기반 에너지 관리 소프트웨어 시장의 역할은 현장 수준의 최적화에서 예측, 균형 조정, 배전 등이 연계되어 기능해야 하는 '그리드를 고려한 오케스트레이션'으로 확대되고 있습니다. 2026년에 발표된 엣지 AI를 활용한 재생에너지 마이크로그리드 제어에 관한 논문은 IoT로 연결된 자산 간에 안전하고 에너지 효율이 높은 연동 기술의 성숙도를 입증하고 있으며, 분산형 에너지 시스템에서 AI 주도형 제어로의 광범위한 전환을 뒷받침하고 있습니다. 일본이 2026년도부터 저전압 분산형 에너지 자원을 수요 반응 시장에 개방하기로 결정함에 따라, 국내 자원 집계업체(Resource Aggregator) SaaS 플랫폼 시장은 2024년도부터 2035년도에 걸쳐 33.5배로 확대되어 67억 엔(이미 4,400만 달러로 환산됨)에 달할 것으로 예측됩니다. 따라서 AI 기반 에너지 관리 소프트웨어 시장은 연결되는 자산 증가뿐만 아니라, 이러한 자산을 수익 창출이 가능한 유연한 자원으로 전환할 수 있게 해주는 규제 변화로부터도 혜택을 받게 될 것입니다.

기존 OT 시스템과 IT 시스템 간의 통합이 지닌 복잡성

많은 플랜트, 전력 회사, 대규모 빌딩에서는 현대적인 AI 워크플로우에 맞추어 구축되지 않은 개별 데이터 레이어, 독자적인 사양의 히스토리안, 산업용 프로토콜이 여전히 사용되고 있어, 레거시 운영 환경이 큰 제약 요인으로 작용하고 있습니다. 이러한 환경에서 벤더가 가동 중인 업무를 중단시키지 않고 SCADA, 빌딩 관리 시스템, 기업 소프트웨어, 엣지 디바이스를 연동할 수 없다면, AI 기반 에너지 관리 소프트웨어 시장은 원활하게 확대될 수 없습니다. 이는 단순한 소프트웨어 호환성 문제에 그치지 않습니다. IT와 OT의 엄격한 분리로 인해, 벤더들은 부문화된 네트워크, 로컬 추론, 그리고 관리형 데이터 교환을 중심으로 도입 방식을 재설계할 수밖에 없는 경우가 많기 때문입니다. 록웰 오토메이션은 2025년 보고서에서 IT와 OT 보안 운영 센터를 완전히 통합한 조직이 고작 30%에 불과하다고 지적하며, AI가 두 환경에서 일관되게 작동할 수 있게 되기까지는 여전히 기초적인 조정 작업이 남아 있음을 부각시키고 있습니다. 2025년에 발표된 에너지 시스템의 사이버-물리적 상황 인식에 관한 기술 보고서 역시, 첨단 제어 환경이 단순한 데이터 접근이 아닌 안전하고 구조화된 통합에 의존하고 있음을 보여주고 있습니다. 따라서 AI 기반 에너지 관리 소프트웨어 시장은 아키텍처상의 과제가 소프트웨어의 기능만큼이나 중요한 기존 시스템(브라운필드) 환경에서 도입 주기의 지연을 겪고 있습니다.

부문별 분석

2025년 기준으로 소프트웨어 시장 점유율은 69.85%를 차지했으며, 지출의 대부분은 여전히 주변 지원 분야가 아닌 핵심 플랫폼에 집중되어 있는 것으로 나타났습니다. 이러한 우위는 전환 위험이 높고 통합 이력이 중요하게 여겨지는 유틸리티 제어실, 빌딩 시스템 및 산업용 최적화 환경에 이미 통합되어 있는 공급업체의 도입 기반에서의 우위를 반영하고 있습니다. AI 기반 에너지 관리 소프트웨어 시장에서 이러한 소프트웨어 플랫폼은 일반적으로 대시보드, 예측 엔진, 디스패치 로직, 탄소 회계 모듈 및 기존 제어 시스템을 대체하는 것이 아니라, 그 위에 중첩되어 작동하는 오버레이를 결합하고 있습니다. 이러한 위상은 데이터 네트워크 효과의 혜택도 받고 있습니다. 즉, 플랫폼을 사용하는 기간이 길수록 모델 조정이나 고객 관계 유지에 있어 그 운영 이력의 가치가 높아집니다. 따라서 구매자의 요구 사항이 확대되더라도 소프트웨어 부문은 견실한 수익 기반을 유지하고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 20.12%를 나타낼 것으로 예측되며, AI 기반 에너지 관리 소프트웨어 시장에서 가장 두드러진 성장세를 보일 것으로 전망됩니다. 그 주된 이유는 지역의 부하 동향, 요금 체계 변경, 기상 변화, 새로운 자산 구성 등을 반영하기 위해 정기적인 재학습을 실시하지 않으면 에너지 AI의 정확도가 떨어지기 때문입니다. 2026년에 수행된 예측 유지보수를 위한 캐시 확장형 멀티모달 생성형 AI에 관한 연구에서 에너지 집약형 장비의 실시간 이상 감지 시 이 아키텍처가 단독 분석 기법보다 우수한 성능을 보임에 따라, 지속적인 모델 지원의 가치가 입증되었습니다. 또한 구매자의 입장에서는 특히 AI를 활용하여 ISO 50001이나 내부 성과 평가를 지원하는 경우, 통합, 모델 거버넌스, 사용자 지원, 감사 대응이 가능한 보고서 작성을 위한 서비스 지원도 필요합니다. 이러한 추세에 따라 수익원은 일회성 라이선스 판매에 그치지 않고 확대되고 있으며, AI 기반 에너지 관리 소프트웨어 업계에서 지속적인 거래 관계가 더욱 촉진되고 있습니다.

2025년에는 AI 기반 에너지 관리 소프트웨어 시장 점유율 중 66.41%를 클라우드 기반 도입이 차지했습니다. 이는 클라우드가 신속한 도입, 간편한 업데이트, 그리고 기업의 데이터 환경과의 원활한 통합을 가능하게 하기 때문입니다. 이 모델은 대규모 온사이트 인프라에 대한 투자 없이도 분석, 보고서 작성, 최적화를 필요로 하는 상업용 건물 운영자나 중규모 산업 사용자에게 적합합니다. AI 기반 에너지 관리 소프트웨어 시장에서 클라우드 기반 서비스는 포트폴리오를 통합적으로 시각화할 수 있게 해줍니다. 이는 단일 소유주가 여러 거점에 걸쳐 있는 다수의 시설을 관리하는 경우에 중요합니다. 이러한 규모의 이점은 공급업체가 새로운 기능을 보다 신속하게 도입할 수 있을 뿐만 아니라, 고객이 단일 환경 내에서 각 거점의 에너지 성능을 비교할 수 있다는 점에서 큰 의미를 지닙니다. 그 때문에 사용자들이 거점별로 세밀한 제어를 요구하게 되었음에도 불구하고, 클라우드는 여전히 판매량 1위를 유지하고 있습니다.

하이브리드 구축 시장은 2031년까지 연평균 성장률(CAGR) 19.92%를 나타낼 것으로 예측되며, 전력 회사와 대규모 산업 사업자들이 에지에서의 응답성과 클라우드 분석 기능을 모두 요구하는 가운데, 하이브리드 구축용 AI 기반 에너지 관리 소프트웨어 시장도 연평균 성장률(CAGR) 19.92%로 확대될 것으로 전망됩니다. 이러한 경향이 강화되고 있는 배경에는 많은 고부가가치 이용 사례에서 현장에서의 저지연 대응이 필요한 반면, 부하가 더 높은 예측 및 최적화 워크로드는 여전히 클라우드에 의존하고 있다는 사정이 있습니다. 2025년에 발표된 엣지 AI를 활용한 장애 감지에 관한 기사에 따르면, 응답 시간이 150밀리초 미만일 경우 감지율이 92.0%에 달한 반면, 클라우드 기반의 대체 방식은 200밀리초가 소요되었으며, 추론 주기당 에너지 소비량도 더 적었던 것으로 보고되었습니다. 2026년에 발표된 재생에너지 마이크로그리드 제어에 관한 또 다른 연구 역시, 에너지를 소모하는 사이버-물리 시스템 간의 연동에 엣지 AI를 도입해야 한다는 점을 더욱 뒷받침하고 있습니다. 데이터 주권이나 중요 인프라 요건으로 인해 원격 처리가 제한되는 상황에서는 온프레미스 배포가 여전히 명확한 역할을 수행하고 있지만, 가장 두드러진 성장이 예상되는 것은 어느 한쪽의 극단적인 형태가 아니라 혼합 아키텍처로의 전환입니다.

지역별 분석

2025년, 유럽은 AI 기반 에너지 관리 소프트웨어 시장 점유율의 34.56%를 차지했습니다. 이는 건물, 에너지 성능 및 보고에 관한 규제가 다른 지역에 비해 유럽에서 더 잘 정비되어 있기 때문입니다. 개정된 EPBD는 2024년에 발효되며, EU 회원국들은 2026년 5월 29일까지 이를 국내법에 반영해야 합니다. 이로 인해 대규모 비주거용 건물에서 빌딩 자동화 및 제어 시스템의 실용적 중요성이 더욱 커지고 있습니다. 기술 보고서 CEN/TR 18276:2026에는 EPBD 프레임워크에 기반한 빌딩 자동화 규정 준수 체크리스트가 추가되어, 디지털 에너지 관리 시스템의 보다 공식적인 도입 과정을 뒷받침하고 있습니다. 독일, 영국, 프랑스, 이탈리아가 여전히 주요 시장을 차지하고 있지만, 북유럽 및 중동유럽 국가들에서는 개보수 공사, 전기화, 그리고 더욱 엄격해진 효율 기준에 힘입어 시장이 활기를 띠고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 20.45%를 기록하며 성장할 것으로 예상되며, AI 기반 에너지 관리 소프트웨어 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 중국은 송전망의 현대화, 산업 규모의 크기, 그리고 '이산화탄소 배출량의 정점 도달과 탄소 중립'이라는 목표에 따라 전력 시스템 및 시설 시스템 전반에 걸친 최적화에 대한 수요가 크게 증가하고 있어, 지역 내 도입량에서 1위를 차지하고 있습니다. 또한, 주요 산업 회랑, 특히 대규모 에너지 소비자들이 더욱 엄격한 모니터링 및 감사 요구에 직면해 있는 지역에서 규제 준수와 관련된 에너지 관리 수요가 증가함에 따라 인도의 중요성도 커지고 있습니다. 일본에서는 2026년도부터 저전압 분산형 에너지 자원이 수요 반응(Demand Response)에 참여하게 되며, 유연한 자산을 집약 및 제어할 수 있는 소프트웨어의 경제적 이점이 확대됨에 따라 추가적인 성장 동력이 더해질 것입니다. 한국과 호주 역시 재생에너지 도입 확대와 송전망의 디지털화를 통해 이 지역의 전망을 뒷받침하고 있습니다. 한편, 동남아시아에서는 생산 능력 확대에 따라 기존 산업 시설의 개보수 분야에서 장기적인 성장 여지가 예상됩니다.

북미는 2025년, 성숙한 수요 반응 체계, 상업용 건물에서의 광범위한 도입, AI 관련 인프라에 대한 적극적인 투자에 힘입어 큰 시장 점유율을 차지했습니다. 또한, 이 지역에는 보안 및 제어 요건이 충족된다면 운영 데이터를 클라우드 규모의 AI 환경에 연결하는 것을 주저하지 않는 수많은 전력 회사와 기업 사업자가 존재한다는 점도 강점으로 꼽힙니다. 2026년 4월, AWS는 지멘스 에너지의 전략적 클라우드 제공업체로 선정되었습니다. 이는 에너지 분야에서 주요 공급업체들이 운영 분야의 전문 지식과 하이퍼스케일 컴퓨팅 지원을 어떻게 융합하고 있는지를 반영하고 있습니다. 남미는 AI 기반 에너지 관리 소프트웨어 시장에서 여전히 신흥 지역이지만, 중동 및 아프리카는 도입 초기 단계에 있음에도 불구하고 재생에너지의 확대와 인프라 현대화가 진행됨에 따라 계속해서 선별적인 투자를 유치하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the AI-powered energy management software market size is expected to grow from USD 4.12 billion in 2025 to USD 4.85 billion in 2026 and is forecast to reach USD 11.76 billion by 2031 at 19.38% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, and More), End User (Utilities, Commercial Buildings, Industrial Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Powered Energy Management Software Market Trends and Insights

Rising Need For Real-Time Energy Optimization in Commercial And Industrial Facilities

Real-time optimization is emerging as the clearest near-term value driver for the AI-powered energy management software market because it transforms software from a passive reporting layer into an active operating tool. Commercial and industrial users are facing sharper power price swings, wider time-of-use tariff exposure, and tighter internal pressure to reduce avoidable peak demand without affecting uptime. That is why the AI-powered energy management software market is gaining traction in facilities that need load schedules to adjust against live prices, production cycles, and changing site conditions rather than against fixed rules. A 2026 study showed that a schedule-aware XGBoost model using production-schedule inputs achieved an RMSE of 2.67 kW and an R2 of 0.9698, supporting the case for high-accuracy forecasting in multi-line industrial settings without relying on full internal sensor visibility. This kind of performance matters because it makes AI useful in real operating environments where incomplete plant data often limits traditional optimization tools. As more sites seek to cut demand charges and stabilize energy use during volatile tariff windows, the AI-powered energy management software market is increasingly tied to daily operational savings rather than longer-cycle sustainability projects.

AI Integration With Smart Grids and Distributed Energy Resources

The rise of distributed energy resources is also driving the AI-powered energy management software market, as grid conditions are now shaped by rooftop solar, batteries, EV charging, and flexible loads that require constant coordination. Conventional dispatch logic struggles when power flows become bidirectional and when decisions must be made across thousands of small assets rather than a few centralized generation points. That shift is expanding the role of the AI-powered energy management software market from site-level optimization to grid-aware orchestration, where forecasting, balancing, and dispatch must work together. A 2026 paper on edge-AI-enabled renewable microgrid control demonstrated the technical maturity of secure, energy-efficient coordination across IoT-linked assets, reinforcing the broader move toward AI-led control in distributed energy systems. Japan's decision to open low-voltage distributed energy resources to demand-response markets from FY2026 is expected to expand the domestic resource aggregator SaaS platform market by 33.5 times between FY2024 and FY2035, to JPY 6.7 billion, which was already converted to USD 44 million. The AI-powered energy management software market, therefore, benefits not only from more connected assets but also from rule changes that turn those assets into monetizable flexibility resources.

Integration Complexity Across Legacy OT and IT Systems

Legacy operational environments remain a major restraint because many plants, utilities, and large buildings still run on separate data layers, proprietary historians, and industrial protocols that were not built for modern AI workflows. In those environments, the AI-powered energy management software market cannot scale smoothly unless vendors can bridge SCADA, building management systems, enterprise software, and edge devices without disrupting live operations. This is a bigger issue than software compatibility alone, because strict IT-OT separation often forces vendors to redesign deployment patterns around segmented networks, local inference, and controlled data exchange. Rockwell Automation reported in 2025 that only 30% of organizations had fully integrated IT and OT security operations centers, underscoring the foundational coordination work that remains before AI can operate consistently across both environments. A 2025 technical report on cyber-physical situational awareness in energy systems also reflected how advanced control environments depend on secure, structured integration rather than simple data access. The AI-powered energy management software market, therefore, faces slower deployment cycles in brownfield settings, where architectural challenges are as important as software capabilities.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Automated Demand Response and Peak Load Management

- Expansion of ESG Reporting and Carbon Accounting Workflows

- Data Quality, Interoperability, and Sensor Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 69.85% share in 2025, indicating that most spending still sat in core platforms rather than in surrounding support layers. That lead reflects the installed-base advantage of vendors already embedded in utility control rooms, building systems, and industrial optimization environments, where switching risk is high and integration history matters. In the AI-powered energy management software market, these software platforms usually combine dashboards, forecasting engines, dispatch logic, carbon accounting modules, and overlays that sit above existing control systems rather than replacing them. This position also benefits from data network effects: the longer a platform remains in use, the more valuable its operational history becomes for tuning models and maintaining customer relationships. The software category, therefore, keeps a durable revenue base even as buyers broaden their requirements.

Services are projected to grow at a 20.12% CAGR through 2031, making them the fastest-growing component of the AI-powered energy management software market. The main reason is that energy AI becomes less accurate without regular retraining to account for local load behavior, changing tariffs, weather shifts, and new asset configurations. A 2026 study on cache-augmented multimodal generative AI for predictive maintenance supported the value of ongoing model support because the architecture outperformed standalone analytical approaches in real-time anomaly detection for energy-intensive equipment. Buyers also need service support for integration, model governance, user enablement, and audit-ready reporting, especially when they use AI to support ISO 50001 or internal performance reviews. That pattern is widening the revenue pool beyond one-time license sales and pushing more recurring relationships into the AI-powered energy management software industry.

Cloud-based deployment accounted for 66.41% of the AI-powered energy management software market share in 2025, as it supports faster onboarding, simpler updates, and easier integration with enterprise data environments. This model works well for commercial building operators and mid-sized industrial users that want analytics, reporting, and optimization without large on-site infrastructure commitments. In the AI-powered energy management software market, cloud delivery also enables centralized portfolio visibility, which is important when a single owner manages many facilities across multiple locations. The scale advantage is meaningful because it allows vendors to roll out new functions faster and lets customers compare energy performance across sites within one environment. That is why cloud remains the volume leader even as users ask for more site-specific control.

Hybrid deployment is projected to grow at a 19.92% CAGR through 2031, and the AI-powered energy management software market for hybrid deployment is projected to expand at a 19.92% CAGR as utilities and large industrial operators seek both edge responsiveness and cloud analytics. This pattern is gaining strength because many high-value use cases need low-latency action at the site while still depending on heavier forecasting and optimization workloads in the cloud. A 2025 article on edge AI fault detection reported 92.0% detection rates with response times below 150 milliseconds, compared with 200 milliseconds for cloud alternatives, while using less energy per inference cycle. A separate 2026 study on renewable microgrid control further supported the deployment of edge AI for energy-critical cyber-physical coordination. On-premises deployment still plays a defined role, where data sovereignty and critical infrastructure requirements limit remote processing, but the strongest growth is toward mixed architectures rather than either extreme alone.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 34.56% of the AI-powered energy management software market share in 2025, as regulation around buildings, energy performance, and reporting is more developed there than in other regions. The recast EPBD entered into force in 2024, and EU member states must transpose it into national law by May 29, 2026, thereby increasing the practical relevance of building automation and control systems in large non-residential properties. The technical report CEN/TR 18276:2026 adds a compliance checklist for building automation under the EPBD framework, which supports more formal implementation pathways for digital energy management systems. Germany, the United Kingdom, France, and Italy remain the main country markets, while the Nordics and Central and Eastern Europe are building momentum through renovation activity, electrification, and stricter efficiency standards.

Asia-Pacific is projected to grow at a 20.45% CAGR through 2031, making it the fastest-growing region in the AI-powered energy management software market. China leads regional deployment volume because grid modernization, industrial scale, and dual-carbon goals create a large need for optimization across power and facility systems. India is also becoming more important as compliance-linked energy management demand builds in major industrial corridors, especially where large energy users face tighter monitoring and audit expectations. Japan adds another growth layer as low-voltage distributed energy resources enter demand-response participation from FY2026, expanding the economic case for software that can aggregate and control flexible assets. South Korea and Australia are also supporting the regional outlook through higher renewable integration and grid digitization, while Southeast Asia offers a longer runway in brownfield industrial retrofits as manufacturing capacity expands.

North America held a substantial share in 2025, supported by mature demand-response structures, deep adoption of commercial buildings, and strong investment in AI-related infrastructure. The region also benefits from a large base of utilities and enterprise operators willing to connect operational data to cloud-scale AI environments when security and control requirements are met. AWS was named a strategic cloud provider for Siemens Energy in April 2026, reflecting how major vendors are combining operational domain expertise with hyperscale computing support in the energy field. South America remains an emerging part of the AI-powered energy management software market, while the Middle East and Africa are still earlier in adoption but continue to attract selective investment as renewable buildout and infrastructure modernization advance.

- Bidgely Inc.

- C3.ai, Inc.

- Grid4C Ltd.

- Innowatts, Inc.

- EnergyCAP, LLC

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Honeywell International Inc.

- Johnson Controls International plc

- IBM Corporation

- Oracle Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Enel X S.r.l.

- GridPoint, Inc.

- AutoGrid Systems, Inc.

- Dexma Sensors, S.L.

- Rockwell Automation, Inc.

- Energy Intelligence Group, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities

- 4.2.2 Integration of AI With Smart Grid and Distributed Energy Resources

- 4.2.3 Increasing Demand for Automated Demand Response and Peak Load Management

- 4.2.4 Expansion of ESG Reporting and Carbon Accounting Workflows

- 4.2.5 Edge AI Adoption for Site-Level Energy Control and Fault Detection

- 4.2.6 Growing Retrofit Demand From Aging Building and Industrial Infrastructure

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity With Legacy OT and IT Systems

- 4.3.2 Data Quality, Interoperability, and Sensor Fragmentation Issues

- 4.3.3 Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets

- 4.3.4 Payback Uncertainty in Small and Mid-Sized Sites With Limited Load Density

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bidgely Inc.

- 6.4.2 C3.ai, Inc.

- 6.4.3 Grid4C Ltd.

- 6.4.4 Innowatts, Inc.

- 6.4.5 EnergyCAP, LLC

- 6.4.6 Siemens AG

- 6.4.7 Schneider Electric SE

- 6.4.8 ABB Ltd.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Johnson Controls International plc

- 6.4.11 IBM Corporation

- 6.4.12 Oracle Corporation

- 6.4.13 Microsoft Corporation

- 6.4.14 Amazon Web Services, Inc.

- 6.4.15 Enel X S.r.l.

- 6.4.16 GridPoint, Inc.

- 6.4.17 AutoGrid Systems, Inc.

- 6.4.18 Dexma Sensors, S.L.

- 6.4.19 Rockwell Automation, Inc.

- 6.4.20 Energy Intelligence Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment