|

시장보고서

상품코드

2072961

의료용 스마트 텍스타일 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Smart Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

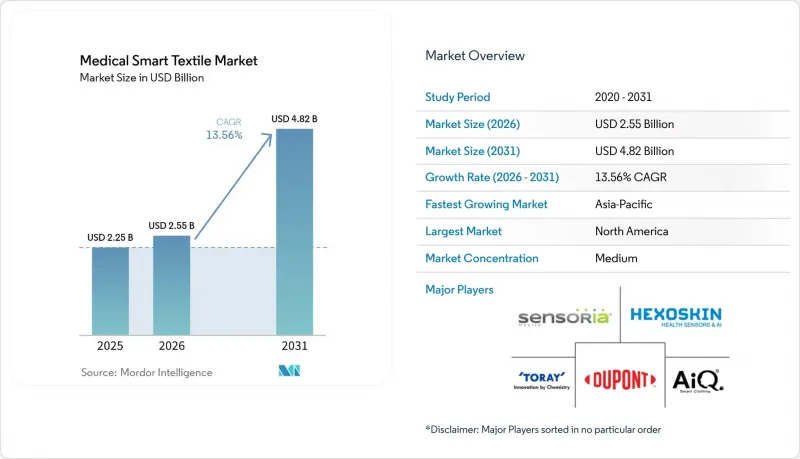

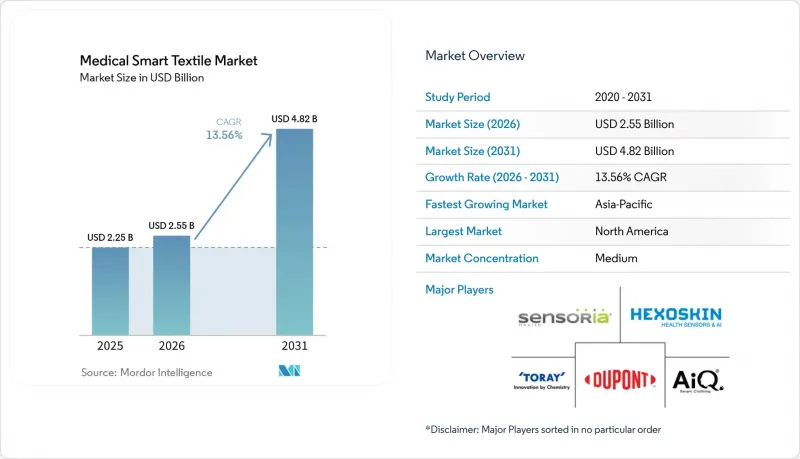

Mordor Intelligence에 의하면, 의료용 스마트 텍스타일 시장 규모는 2025년에 22억 5,000만 달러, 2026년에 25억 5,000만 달러되어, 2031년까지 48억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 13.56%로 성장할 전망입니다.

본 보고서는 유형별(패시브형 스마트 텍스타일, 액티브형 스마트 텍스타일, 울트라 스마트 텍스타일), 기술별(텍스타일 센서, 웨어러블 기술 등), 용도별(생체 모니터링, 외과 수술, 치료·웰니스 등), 최종 사용자별(병원 및 진료소, 학술·산업 연구 등), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 의료용 스마트 텍스타일 시장 동향 및 인사이트

원격 환자 모니터링에 대한 수요 증가

원격 환자 모니터링은 만성 질환 관리에서 일상적인 요소로 자리 잡고 있으며, 이러한 변화에 따라 의료용 스마트 텍스타일 시장에는 단순한 단기 입원 치료에 그치지 않는 보다 광범위하고 지속적인 활용 사례가 등장하고 있습니다. CMS의 ACCESS 모델은 2026년 7월에 시작되며, 고혈압, 당뇨병, 만성 근골격계 통증 등의 질환을 앓고 있는 메디케어 수급자를 대상으로 한 기술 기반 만성 질환 관리에 FDA 승인을 받은 웨어러블 기기가 직접 통합될 예정입니다. 이는 중요한 의미를 지닙니다. 왜냐하면 생리 데이터를 수집하는 의류는 패치나 별도의 모니터링 기기보다 일상생활에 자연스럽게 녹아들 수 있어, 장기적인 치료 순응도 향상으로 이어지기 때문입니다. 2026년 6월 듀크 대학교 헬스 시스템에서 실시된 전향적 연구에 따르면, 웨어러블 모니터링을 통해 눈에 띄는 임상 증상이 나타나기 전에 수술 후 조기 악화를 감지할 수 있는 것으로 나타났으며, 이는 입원 기간을 넘어서는 지속적인 모니터링의 유효성을 입증합니다. 그 상업적 영향은 장기적인 질환 관리에 그치지 않고, 수술 후 관리나 급성기 이후의 관리에서도 더 짧은 기간의 모니터링이 경제적으로 합리적인 선택지가 될 수 있게 되었기 때문에 더욱 광범위해졌습니다. 그 결과, 의료용 스마트 텍스타일 시장은 입원 치료와 완전히 관리되지 않는 재택 회복의 중간 단계에 위치한, 더 광범위한 환자층에 접근할 수 있게 되고 있습니다.

주요 시장에서 커넥티드 케어에 대한 보험 급여 지원

상환 제도의 일관성은 의료용 스마트 텍스타일 시장에 있어 가장 뚜렷한 수요 촉진요인 중 하나입니다. 이는 지급 규정이 실제 임상 현장에서의 커넥티드 케어 제공 방식에 더욱 적절하게 부합하게 되었기 때문입니다. CMS(미국 의료보험 및 의료서비스 센터)는 2025년 7월, 원격 환자 모니터링 코드와 관련하여 기존의 최소 16일 요건에서 30일 기간 중 단 2일 동안만 데이터가 전송된 경우에도 적용 가능하도록 하는 방안을 제시했습니다. 이를 통해 에피소드형 치료 및 퇴원 후 사후 관리에 대한 적용 범위가 확대됩니다. 이 변경 사항은 중요한 의미를 지닙니다. 왜냐하면, 텍스타일 기반 기기는 수술 후나 퇴원 후, 혹은 1개월 미만의 치료 기간 동안 환자의 경과 관찰이 필요한 경우에 가장 유용하게 쓰이는 경우가 많기 때문입니다. 2025년 1월, 몰룬리케 헬스케어는 사이렌 케어사에 800만 달러를 투자했습니다. 이 회사의 체온 감지 기능이 탑재된 당뇨병용 발 양말은 당뇨병성 족부 궤양 발생 위험을 68%, 절단 수술을 83% 줄여준다고 보고되었으며, 환자 1인당 연간 치료비도 절감하고 있습니다. 이러한 움직임은 보험 적용에 관한 논의가 센서의 혁신성뿐만 아니라 측정 가능한 의료비 성과에 의해 점점 더 좌우되고 있음을 보여줍니다. 따라서 의료용 스마트 텍스타일 시장에서 환자 개개인의 비용 절감 효과를 입증할 수 있는 기업은 이에 상응하는 임상적·경제적 근거 없이 우수한 하드웨어 성능만을 제공하는 기업보다 유리한 입장에 있다고 할 수 있습니다.

높은 제조 및 검증 비용

의료용 스마트 텍스타일 시장은 많은 기존 의료기기 카테고리와는 다른 비용 구조에 직면해 있습니다. 그 이유는 검증에 필요한 비용이 하드웨어 생산 예산을 크게 초과할 가능성이 있기 때문입니다. 원단, 실, 그리고 내장형 센서 부품은 대량 생산이 가능하더라도, 승인이나 보험 적용에 필요한 임상시험에는 대개 훨씬 더 많은 자금이 소요되기 때문입니다. 『Journal of the Textile Institute』지 2024년 총설에서는 전도성 부품이 반복적인 세탁 주기로 인해 예측하기 어렵고, 시험에 막대한 비용이 소요되는 방식으로 열화되기 때문에 세탁 내성과 내구성이 여전히 뿌리 깊은 장벽으로 남아 있다고 지적하고 있습니다. 이로 인해 서로 다른 환자 집단, 의류 유형, 사용 환경에 걸친 장기적인 성능을 입증하는 데 드는 비용이 급증하고 있습니다. 또한, 보험 적용과 관련된 많은 논의에서 비용 절감의 근거가 기술적 기능과 동등하게 중요시되게 되면서, 보험사 측의 기대도 높아지고 있습니다. 이로 인해 의료용 스마트 텍스타일 시장의 소규모 혁신 기업들은 압박을 받고 있습니다. 왜냐하면 제품 아이디어를 가장 신속하게 현실로 구현하는 기업이야말로 대규모 선행 연구에 자금을 투입할 능력이 가장 부족한 경우가 많기 때문입니다.

부문별 분석

2025년 의료용 스마트 텍스타일 시장의 제품 유형별 점유율에서는 "울트라 스마트 텍스타일"이 38.31%를 차지했습니다. 이는 의료 서비스 제공업체들이 다중 매개변수 감지 기능과 더욱 정교한 기능을 결합한 의류에 대해 더 높은 대가를 지불할 의향이 있음을 보여줍니다. 병원이나 스텝다운 치료 현장에서는 단 하나의 의류를 착용한 상태에서 심전도, 호흡수, 근육 활동, 피부 온도를 단일 폼 팩터로 측정할 수 있기 때문에 이러한 시스템이 높은 평가를 받았습니다. 이로 인해 여러 대의 기기를 사용해야 할 필요가 줄어들었고, 치료 제공 중에 개별 데이터 스트림을 수집해야 하는 부담이 경감되었습니다. 이러한 유형 구성은 예산 결정자가 어디에서 가장 실질적인 수익을 기대하고 있는지를 반영하고 있습니다. 기기 통합을 통해 워크플로가 개선된다면, 단가가 높아지더라도 받아들일 수 있기 때문입니다. 의료용 스마트 텍스타일 업계에서는 중증도가 높은 의료 현장에서의 조달 결정에 있어, 여러 모니터링 절차를 한 번에 대체할 수 있는 제품이 계속해서 선호되고 있습니다.

액티브형 스마트 텍스타일은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.38%를 나타낼 것으로 예측되며, 의료용 스마트 텍스타일 시장에서 가장 빠르게 성장하는 부문으로 꼽히고 있습니다. 이러한 성장은 단순한 감지에 그치지 않는 제품, 즉 재활 지원, 치료 반응 및 기타 폐쇄 루프 기능을 위해 설계된 시스템 등에 기인합니다. 패시브형 스마트 텍스타일은 압박 요법, 항균성 상처 드레싱, 자세 유지 보조 기구 등의 분야에서 여전히 중요한 역할을 하고 있으며, 이러한 분야에서는 내장된 지능보다는 긴 수명과 저렴한 비용이 더 중시되고 있습니다. 2025년 『npj Flexible Electronics』지에 게재된 논문에서는 전기적, 열적, 화학적 양상을 아우르는 섬유 기반 치료 시스템에 필요한 재료 및 구조적 요건이 개괄되어 있으며, 이는 반응성이 더욱 뛰어난 스마트 소재의 지속적인 개발을 촉진하고 있습니다. 앞으로 프로그래밍 가능한 기능이 더 폭넓은 가격대에 보급됨에 따라, 액티브 스마트 텍스타일과 울트라 스마트 텍스타일 간의 경계가 점차 모호해질 가능성이 있습니다. 이러한 변화로 인해 의료용 스마트 텍스타일 시장은 엄격한 카테고리 분류 자체보다는 기능과 임상적 용도에 계속 초점을 맞출 것으로 보입니다.

2025년, 웨어러블 기술은 매출 점유율의 38.24%를 차지하며 의료용 스마트 텍스타일 시장에서 가장 큰 기술 부문이 되었습니다. 이러한 우위는 임상 현장과 재택 환경 모두에서 심폐 기능 추적, 활동량 모니터링, 수면 관련 관찰 등 의류형 건강 모니터가 상업적으로 성숙해졌기 때문입니다. 이 부문이 채택된 배경에는 일반적으로 의류가 단독형 기기나 부착형 기기보다 환자의 일상생활에 더 잘 녹아든다는 점이 있습니다. 또한, 웨어러블 의류는 환자에 대한 개입을 최소화하면서도 더 장기간에 걸친 관찰을 가능하게 하므로, 의료진에게도 이점이 있었습니다. 이러한 사용 편의성과 임상적 중요성의 확대가 맞물리면서, 웨어러블 기술은 계속해서 수요의 중심이 되었습니다.

바이오메디컬 웨어러블 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.52%를 나타낼 것으로 예측되며, 이는 의료용 스마트 텍스타일 시장의 기술 부문 중 가장 빠른 성장 속도입니다. 이 분야의 성장은 범용 웨어러블 제품보다는 보다 구체적인 측정, 치료 반응 또는 진단 지원이 필요한 질환 특이적 용도와 밀접한 관련이 있습니다. 텍스타일 센서나 E-텍스타일은 독립적인 수익 부문이라기보다는 대규모 시스템 내의 기반 계층으로 기능하는 경향이 강해지고 있으며, 이로 인해 직접 판매의 가시성은 낮아지는 반면, 밸류체인 내에서의 역할은 확대되고 있습니다. 스마트 패브릭은 항균성 병원용 의류나 체온 조절 용도 등 중요한 특수 용도 분야에서 계속해서 중요한 역할을 수행하고 있습니다. 2025년 2월 『Nature』지에 게재된 연구에서는 텍스타일 네트워크 내에서 분산 추론이 가능한 단일 섬유 컴퓨터가 소개되었으며, 이는 향후 예측 기간 동안 센싱과 처리가 더욱 긴밀하게 연계될 가능성을 시사하고 있습니다. 이러한 추세가 진행됨에 따라, 의료용 스마트 텍스타일 시장에서는 재료 과학, 신호 처리, 기기의 사용 편의성을 단일 제품 아키텍처에 통합할 수 있는 기업이 우위를 점할 것으로 예측됩니다.

지역별 분석

2025년, 북미는 의료용 스마트 텍스타일 시장 점유율의 38.22%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역의 경쟁력은 FDA 승인 파이프라인이 탄탄하다는 점, 원격 생리 모니터링이 널리 보급되고 있다는 점, 그리고 웨어러블 기기를 활용한 만성 질환 관리를 점점 더 지원해 주는 보험 급여 제도에 있다고 할 수 있습니다. 미국은 제품 승인 절차와 지불 체계가 다른 대부분 시장보다 잘 갖춰져 있어 여전히 주요 견인 역할을 하고 있습니다. 캐나다에서는 Hexoskin이나 Myant와 같은 기업들이 기관 조사 파트너와의 협력을 지속하는 한편, 보다 광범위한 국제 의료 프로그램으로의 판매를 확대함으로써 혁신의 기반을 더욱 공고히 하고 있습니다.

유럽은 의료용 스마트 텍스타일 시장에서 여전히 2위의 규모를 자랑하며, 또한 규제가 가장 엄격한 지역 중 하나이기도 합니다. 독일, 영국, 프랑스 및 북유럽 국가들은 디지털 헬스 인프라, 예방 의료에 대한 집중, 그리고 확립된 섬유·의료 기술 역량을 모두 갖추고 있어, 도입이 가장 활발히 진행되고 있는 클러스터를 형성하고 있습니다. 독일은 그 산업의 깊이에서 두각을 나타내고 있으며, KOB GmbH는 국제적인 연구 협력 관계를 유지하면서 의료용 스마트 텍스타일 전문 팀을 구축했습니다. 유럽연합 집행위원회와 Euratex는 2025년에 "미래의 섬유" 파트너십을 출범하고, 2030년까지 6,000만 유로(6,480만 달러)를 출연하기로 결정했습니다. 이로 인해 EU MDR(의료기기 규정) 준수가 상업적 우선순위를 계속해서 좌우하는 상황에서도 혁신의 기세가 유지되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.65%로 확대될 것으로 예상되며, 의료용 스마트 텍스타일 시장 규모 성장률 측면에서 지역별 가장 높은 성장률을 보이고 있습니다. 이 지역은 다른 지역에서는 유례를 찾기 힘들 정도로 강력한 인구 동향에 따른 수요와 제조 규모라는 두 가지 이점을 모두 누리고 있습니다. 일본은 세계적으로 손꼽히는 고령화 사회이며, 이러한 점이 지속적인 재택 모니터링 수요를 뒷받침하고, 임상적으로 검증된 스마트웨어가 노인 돌봄 프로그램에서 확고한 입지를 다지는 요인이 되고 있습니다. 또한, 도레이나 아사히카세이 같은 기업들이 전 세계 스마트 텍스타일 플랫폼을 뒷받침하는 특수 섬유를 공급하고 있기 때문에 이 지역은 소재 측면에서도 높은 경쟁력을 갖추고 있습니다. 중국은 대규모 전도성 섬유 생산을 담당하고 있으며, 이를 통해 광범위한 제품군의 비용 경쟁력이 향상되고 있습니다. 한국도 다른 주요 규제 체계와 보조를 맞추며 의료기기 규제 환경이 성숙해짐에 따라 그 중요성이 커지고 있습니다. 남미, 중동 및 아프리카는 여전히 초기 단계 시장이지만, 의료 인프라와 디지털 헬스의 보급이 지속적으로 개선되는 가운데, 브라질과 GCC 국가들이 첫 번째 주목할 만한 성장 거점으로 주목받고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the medical smart textile market size is projected to be USD 2.25 billion in 2025, USD 2.55 billion in 2026, and reach USD 4.82 billion by 2031, growing at a CAGR of 13.56% from 2026 to 2031.

This report is Segmented by Type (Passive Smart Textiles, Active Smart Textiles, Ultra-Smart Textiles), Technology (Textile Sensors, Wearable Technology, and More), Application (Bio-Monitoring, Surgery, Therapy and Wellness, and More), End User (Hospitals and Clinics, Academic and Industrial Research, and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Smart Textile Market Trends and Insights

Rising Demand for Remote Patient Monitoring

Remote patient monitoring is becoming a regular part of chronic disease management, and that shift is giving the medical smart textile market a wider and more durable use case than short hospital episodes alone. The CMS ACCESS Model launches in July 2026 and directly includes FDA-authorized wearables within technology-supported chronic care for Medicare beneficiaries with conditions such as hypertension, diabetes, and chronic musculoskeletal pain. That matters because garments that collect physiological data can fit more naturally into daily routines than patches or separate monitoring hardware, which supports better adherence over longer periods. A June 2026 prospective study at Duke University Health System showed that wearable monitoring detected early postoperative deterioration before visible clinical presentation, which supports continuous monitoring beyond the hospital stay. The commercial effect is broader than long-term disease management because shorter monitoring windows can now make economic sense in post-surgical and post-acute care. As a result, the medical smart textile market is gaining access to a larger patient pool that sits between inpatient care and fully unmanaged home recovery.

Reimbursement Support for Connected Care in Key Markets

Reimbursement alignment has become one of the clearest demand supports for the medical smart textile market because payment rules now better match how connected care is delivered in real clinical practice. CMS proposed in July 2025 that remote patient monitoring codes could apply when data is transmitted for as few as 2 days in a 30-day period, rather than the prior 16-day minimum, which expands the fit for episodic care and discharge follow-up. That change is important because textile-based devices are often most useful when patients need observation after surgery, after discharge, or during therapy periods that do not last a full month. In January 2025, Molnlycke Health Care invested USD 8 million in Siren Care, whose temperature-sensing diabetic foot socks were reported to reduce diabetic foot ulcer risk by 68% and amputations by 83%, while also lowering annual treatment costs per patient. That move shows that coverage discussions are increasingly shaped by measurable cost-of-care outcomes rather than by sensor novelty alone. Companies in the medical smart textile market that can show patient-level savings are therefore in a better position than companies offering strong hardware performance without comparable clinical and economic proof.

High Production and Validation Costs

The medical smart textile market faces a cost structure that differs from many conventional device categories because validation needs can outweigh hardware production budgets by a wide margin. The fabric, yarn, and embedded sensor components may be manageable at scale, but the clinical studies required for clearance and reimbursement often consume far more capital. A 2024 review in the Journal of the Textile Institute noted that washability and durability remain persistent barriers because conductive components can degrade across repeated wash cycles in ways that are hard to predict and expensive to test. That raises the cost of proving long-term performance across different patient groups, garment types, and use settings. Payer expectations are also increasing because cost-reduction evidence now matters as much as technical function in many coverage discussions. This leaves smaller innovators in the medical smart textile market under pressure because the same firms that move fastest on product ideas are often least able to fund large prospective studies.

Other drivers and restraints analyzed in the detailed report include:

- Textile Sensor Miniaturization and Washability Improvements

- Wearable Integration With Digital Care Pathways

- Regulatory and Certification Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ultra-Smart Textiles held 38.31% of the medical smart textile market share within the type split in 2025, showing that providers were willing to pay more for garments that combined multi-parameter sensing with more advanced functionality. Hospitals and step-down care settings valued these systems because one garment could capture ECG, respiratory rate, muscle activity, and skin temperature in a single form factor. That reduced the need for multiple devices and lowered the burden of gathering separate data streams during care delivery. The type mix also reflects where budget holders see the greatest practical return, since higher unit costs can still be acceptable when device consolidation improves workflow. In the medical smart textile industry, procurement decisions in higher-acuity settings continue to favor products that can replace several monitoring steps at once.

Active Smart Textiles are projected to grow at a 14.38% CAGR from 2026 to 2031, which makes them the fastest-moving type category in the medical smart textile market. Their growth is tied to products that do more than sense, including systems designed for rehabilitation support, therapeutic response, and other closed-loop functions. Passive Smart Textiles remain relevant in compression therapy, antimicrobial wound dressings, and positioning aids, where long wear life and lower cost matter more than embedded intelligence. A 2025 paper in npj Flexible Electronics outlined the material and structural requirements for textile-based therapeutic systems across electrical, thermal, and chemical modalities, which supports continued development in more responsive smart formulations. Over time, the boundary between Active and Ultra-Smart Textiles is likely to narrow as programmable features move into broader price ranges. That shift would keep the medical smart textile market focused on function and clinical use rather than on rigid category labels alone.

Wearable Technology commanded 38.24% revenue share in 2025, which made it the largest technology segment in the medical smart textile market. Its lead came from the commercial maturity of garment-based health monitors across cardiopulmonary tracking, activity monitoring, and sleep-related observation in both clinical and home settings. Adoption favored this segment because garments usually fit patient routines better than separate devices or adhesive formats. Providers also benefited because wearable garments could support longer observation windows with less patient handling. That combination of ease of use and expanding clinical relevance kept Wearable Technology at the center of demand.

Biomedical Wearables are forecast to grow at a 14.52% CAGR from 2026 to 2031, the fastest pace within the technology split of the medical smart textile market. Growth here is tied to disease-specific uses that require more focused measurement, therapeutic response, or diagnostic support than broader wearable products. Textile Sensors and E-Textiles are increasingly functioning as enabling layers within larger systems rather than as standalone revenue categories, which compresses their direct sales visibility while widening their role in the value chain. Smart Fabrics continue to serve important specialty uses, including antimicrobial hospital apparel and thermal regulation applications. Research published in Nature in February 2025 described a single-fibre computer capable of distributed inference inside textile networks, which suggests that sensing and processing may become more tightly linked during the forecast period. As that happens, the medical smart textile market is likely to reward companies that can integrate material science, signal processing, and device usability into one product architecture.

Complete Report Scope:

- By Type

- Passive Smart Textiles

- Active Smart Textiles

- Ultra-Smart Textiles

- By Technology

- Textile Sensors

- Smart Fabrics

- Wearable Technology

- E-Textiles

- Biomedical Wearables

- By Application

- Bio-Monitoring

- Surgery

- Therapy and Wellness

- Rehabilitation

- Wound Care and Drug Delivery

- By End User

- Hospitals and Clinics

- Academic and Industrial Research

- Home Healthcare and Patients

- Rehabilitation Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.22% of the medical smart textile market share in 2025, which made it the largest regional contributor. The region's lead rests on a stronger FDA clearance pipeline, wider use of remote physiological monitoring, and reimbursement structures that increasingly support wearable-enabled chronic care. The United States remains the main engine because product clearance activity and payment alignment are both more developed than in most other markets. Canada adds an innovation layer through companies such as Hexoskin and Myant, which continue to work with institutional research partners while selling into broader international healthcare programs.

Europe remained the second-largest geography in the medical smart textile market and also one of the most regulation-heavy. Germany, the United Kingdom, France, and the Nordic countries form the strongest adoption cluster because they combine digital health infrastructure, preventive care focus, and established textile and medical technology capabilities. Germany stands out for its industrial depth, and KOB GmbH has built a dedicated smart medical textiles team while maintaining international research collaborations. The European Commission and Euratex launched the Textiles of the Future partnership in 2025 with EUR 60 million, or USD 64.80 million, committed through 2030, which supports innovation momentum even as EU MDR compliance continues to shape commercial priorities.

Asia-Pacific is forecast to expand at a 15.65% CAGR through 2031, the fastest regional rise in medical smart textile market size. The region benefits from strong demographic demand and manufacturing scale at the same time, which few other geographies can match. Japan has one of the world's oldest populations, which supports continuous home monitoring demand and gives clinically validated smart garments a clear place in aging care programs. The region also has strong materials capability because companies such as Toray Industries and Asahi Kasei supply specialty fibers that support smart textile platforms globally. China contributes large-scale conductive-fiber manufacturing, which improves cost positions for broader product tiers. South Korea is also becoming more relevant as its device regulation environment matures in step with other major frameworks. South America and the Middle East and Africa remain earlier-stage opportunities, with Brazil and GCC countries acting as the first visible growth points as healthcare infrastructure and digital health coverage continue to improve.

- AiQ Smart Clothing Inc.

- Asahi Kasei

- BioSerenity

- Chronolife SAS

- DuPont

- Embro GmbH

- Hexoskin

- Interactive Wear AG

- Johnson & Johnson

- Loomia Technologies, Inc.

- Medtronic

- Myant Corp.

- NexTiles, Inc.

- Ohmatex ApS

- Pireta Limited

- Schoeller Textil AG

- Sensing Tex S.L.

- Sensoria Health

- Siren Care, Inc.

- Toray Industries, Inc.

- Tytex A/S

- Vista Medical Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Remote Patient Monitoring

- 4.2.2 Shift Toward Continuous, Non-Invasive Vital Sign Tracking

- 4.2.3 Wearable Integration With Digital Care Pathways

- 4.2.4 Hospital Push for Post-Acute and Home-Care Extensions

- 4.2.5 Textile Sensor Miniaturization and Washability Improvements

- 4.2.6 Reimbursement Support for Connected Care in Key Markets

- 4.3 Market Restraints

- 4.3.1 High Production and Validation Costs

- 4.3.2 Regulatory and Certification Complexity

- 4.3.3 Data Accuracy and Long-Term Reliability Concerns

- 4.3.4 Interoperability Friction With Clinical IT Systems

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Passive Smart Textiles

- 5.1.2 Active Smart Textiles

- 5.1.3 Ultra-Smart Textiles

- 5.2 By Technology

- 5.2.1 Textile Sensors

- 5.2.2 Smart Fabrics

- 5.2.3 Wearable Technology

- 5.2.4 E-Textiles

- 5.2.5 Biomedical Wearables

- 5.3 By Application

- 5.3.1 Bio-Monitoring

- 5.3.2 Surgery

- 5.3.3 Therapy and Wellness

- 5.3.4 Rehabilitation

- 5.3.5 Wound Care and Drug Delivery

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Academic and Industrial Research

- 5.4.3 Home Healthcare and Patients

- 5.4.4 Rehabilitation Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AiQ Smart Clothing Inc.

- 6.3.2 Asahi Kasei Corporation

- 6.3.3 BioSerenity

- 6.3.4 Chronolife SAS

- 6.3.5 DuPont de Nemours, Inc.

- 6.3.6 Embro GmbH

- 6.3.7 Hexoskin

- 6.3.8 Interactive Wear AG

- 6.3.9 Johnson and Johnson

- 6.3.10 Loomia Technologies, Inc.

- 6.3.11 Medtronic

- 6.3.12 Myant Corp.

- 6.3.13 NexTiles, Inc.

- 6.3.14 Ohmatex ApS

- 6.3.15 Pireta Limited

- 6.3.16 Schoeller Textil AG

- 6.3.17 Sensing Tex S.L.

- 6.3.18 Sensoria Health

- 6.3.19 Siren Care, Inc.

- 6.3.20 Toray Industries, Inc.

- 6.3.21 Tytex A/S

- 6.3.22 Vista Medical Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment