|

시장보고서

상품코드

2072990

색전술 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Embolotherapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

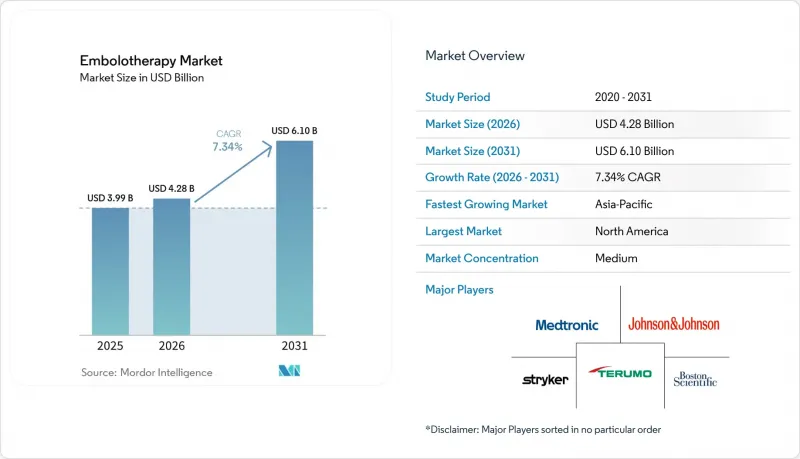

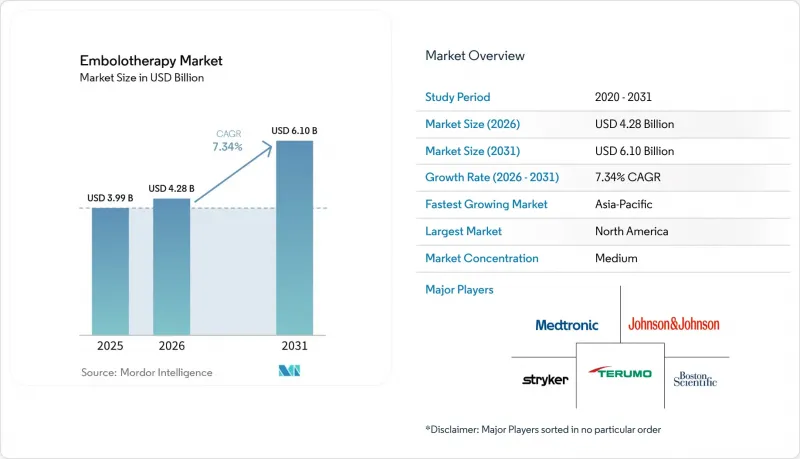

Mordor Intelligence에 의하면, 색전술 시장 규모는 2025년 39억 9,000만 달러로 평가되었고, 2026년에는 42억 8,000만 달러로 추정되고, 2031년까지 61억 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 7.34%로 성장할 전망입니다.

본 보고서는 제품 유형별(색전제, 색전 코일 등), 시술 방법별(경동맥 화학 색전술 등), 적응증별(종양학, 양성 종양, 혈관 이상 등), 최종 사용자별(병원, 외래수술센터(ASC) 등) 및 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 색전술 시장 동향 및 인사이트

암 및 고혈관성 종양으로 인한 부담 증가

색전술 시장은 전 세계 암 부담과 밀접한 관련이 있습니다. 이는 혈관 활동이 활발한 질환의 치료에 있어 색전술이 매우 중요하기 때문입니다. 전 세계 암 환자 수는 2025년에 2,000만 명에 달한 것으로 평가되었으며, 2050년까지 대폭 증가할 것으로 예상에 따라 색전술을 받는 환자층이 확대될 것으로 확실시되고 있습니다. 이러한 경향은 간암, 신장 종양, 골 병변에서 특히 두드러지며, 이러한 질환의 경우 근치적 치료와 완화 치료 모두에서 종양으로의 혈액 공급을 조절하는 것이 필수적입니다. 또한, 수요는 지역별로도 변화하고 있으며, 아시아태평양 및 아프리카 일부 지역에서는 B형 및 C형 간염 바이러스(HBV·HCV)와 관련된 간암 사례가 증가하고 있어, TACE(경동맥 화학 색전술) 및 이와 유사한 시술에 대한 수요를 견인하고 있습니다. 각 제조업체는 더 다양한 병원에 대응할 수 있도록 제품의 설계, 가격 책정 및 교육을 조정하고 있습니다.

저침습적 영상 유도 시술의 활용 확대

색전술 시장은 종양학, 외상, 혈관 치료 분야에서 카테터 기반 치료로 전환되는 추세에 힘입어 성장하고 있습니다. 콘빔 CT나 첨단 투시 유도 기술과 같은 영상 진단 기술의 발전으로 말단 혈관 접근성이 개선되어 시술의 불확실성이 줄어들고 있습니다. 이러한 변화로 인해 보다 정밀한 치료가 가능해졌고, 기술적 장벽도 낮아졌기 때문에 지역 병원이나 중규모 의료기관에서도 복잡한 색전증 환자를 치료할 수 있게 되었습니다. 새로운 코일 시스템은 워크플로우의 효율을 높이고, 대색전술 시 기기로 인한 부담을 줄이도록 설계되었습니다. 그 결과, 질병 발생률 증가와 모든 의료 현장에서 시술이 보편화됨에 따라 시장이 확대되고 있습니다.

적응증 및 의료 현장별 보험 급여의 편차

색전술 시장은 많은 국가에서 의료 적응증의 확대가 보험사 측의 제도 정비를 종종 앞지르고 있기 때문에 보험 급여와 관련된 과제에 직면해 있습니다. 종양학 분야에서의 응용에 대해서는 청구 절차가 명확한 반면, 신경학이나 비뇨기과 분야의 새로운 용도에 대해서는 일관성이 부족합니다. 미국에서는 새로운 원료나 용도에 대한 보험사의 정책이 변화하고 있어, 병원의 처방약 목록에 포함되거나 시장에 널리 보급되는 것이 지연되고 있습니다. 유럽에서는 국가별 의료 기술 평가 및 지급 기관의 해석에 차이가 있어, 규제 당국의 승인을 받았더라도 접근성에 불균형이 발생하고 있습니다. 고가인 차세대 색전제는 당초 진료 코드에 대한 지식, 전문 인력, 그리고 견고한 내부 심사 절차를 갖춘 환자 수가 많은 의료기관에서 도입되기 때문에 시장이 광범위한 상업적 성공을 거두기까지 시간이 더 오래 걸리고 있습니다.

부문별 분석

2025년, 색전제는 색전술 시장에서 58.77%라는 압도적인 점유율을 차지했으며, 다른 모든 제품 카테고리를 앞질렀습니다. 이러한 선도적 지위는 마이크로스피어를 이용한 TACE(경동맥 화학 색전술), 입자 색전술, 그리고 지속적으로 확대되고 있는 액체 색전제 계열의 광범위한 사용에 기인하며, 이 모든 것은 중재적 종양학에 필수적인 요소들입니다. 특정 처치에 국한되는 다른 제품 유형과 달리, 이 그룹은 다양한 치료 환경에서 활약하고 있습니다. 약물 방출형 마이크로스피어는 전신 노출을 최소화하면서 국소적인 항암제 전달을 강화하는 한편, 새로운 액상 제형은 반복 치료나 단계적 암 치료에 유연성을 제공합니다. 가격 책정 및 임상적 차별화에 대한 관심이 높아지고 있음에도 불구하고, 색전제는 여전히 색전술 시장의 수익 기반을 이루고 있습니다.

이 카테고리의 고부가가치 부문은 급속히 발전하고 있습니다. 흡수성이 뛰어나고 적응성이 높은 액체 색전제는 혈관 폐색에서 치료 계획 및 추적 관찰의 유연성으로 초점을 옮겨가고 있습니다. 색전 코일은 특히 신경혈관이나 복잡한 말초혈관 치료에 널리 사용되며, 재위치 가능성과 제어성이 중요하게 여겨지고 있습니다. 2031년까지 연평균 성장률(CAGR) 7.99%를 나타낼 것으로 예측되는 혈관 플러그 및 플러그 시스템은 전립선 동맥 색전술, 자궁근종 수술, 그리고 통제된 폐색이 필요한 외상 사례에서 점점 더 널리 사용되고 있습니다.

TACE는 2025년 색전술 시장에서 34.40%를 차지했으며, 매출 기준 1위를 기록했습니다. 이러한 우위는 간세포암에서 확립된 역할, 치료 경로에의 통합, 그리고 대학병원 및 지역병원에서의 광범위한 도입에 기인합니다. TACE 시술에 대한 숙련도는 간 종양 치료에서 이 시술의 반복적인 사용을 뒷받침하고 있으며, 그 적용 범위를 전이, 신경내분비종양 및 기타 고혈관성 병변까지 확대되고 있습니다. 이러한 범용성 덕분에, 새로운 시술법이 주목을 받고 있는 상황에서도 TACE는 일상적인 색전 치료의 중심적인 위치를 계속 차지하고 있습니다.

2031년까지 연평균 성장률(CAGR) 8.25%를 나타낼 것으로 예측되는 TARE는 특정 환자 집단에서의 임상적 선호도로 인해 주목을 받고 있습니다. 2024-2025년 실시된 메타분석 결과, TACE에 비해 TARE가 반응률, 질병 통제율, 1년 생존율 면에서 더 우수하며, 일반적인 합병증도 적은 것으로 밝혀졌습니다. 2025년 연구에서 문맥 침윤을 동반한 간세포암(HCC) 환자를 대상으로 Y-90 유리 마이크로스피어 요법을 시행한 결과, 83%의 객관적 반응률과 47.2개월의 전체 생존 기간 중앙값이 나타났습니다.

지역별 분석

2025년, 북미는 색전술 시장의 38.79%를 차지했으며, 지역별 최대 기여 지역으로서의 위상을 유지했습니다. 이러한 우위는 탄탄한 중재적 방사선학(영상 진단 하 치료) 인프라, 종양학 및 여성 의료 분야의 폭넓은 시술 기반, 그리고 혁신적인 제품에 대한 승인을 뒷받침하는 규제 당국의 지원에 기인합니다. 미국은 새로운 색전 기술의 주요 도입 거점 역할을 하며, 조기 시장 진입 기회를 제공합니다. 또한 북미는 중경막동맥 색전술의 성장에서도 중심적인 역할을 하고 있으며, 2029년까지 이 시술 건수는 급성 허혈성 뇌졸중 치료 수준에 근접할 것으로 예측됩니다.

2025년, 유럽은 색전술 시장에서 큰 점유율을 차지했으며, 독일, 프랑스, 영국의 선진적인 병원 시스템이 이를 뒷받침하고 있습니다. 이 국가들은 잘 갖춰진 중재적 방사선과 부서와 통합된 종양학 네트워크의 혜택을 받고 있어, TACE, TARE, 자궁근종 색전술, 신경혈관 치료 등의 시술이 가능해졌습니다. 독일의 한 연구에 따르면, 30개 신경혈관 센터에서 718건의 중경막동맥 색전술이 시행된 것으로 보고되었으며, 이는 전문의의 밀도가 높고 임상적 수용도가 높아지고 있음을 반영합니다. 이탈리아와 스페인은 역사적으로 간염 관련 질환의 부담이 컸던 점도 한 요인이 되어, 간을 대상으로 한 종양 치료 건수에 기여하고 있습니다. 유럽은 프로토콜 수립, 제품 검증, 전문의 양성 분야에서 중요한 역할을 수행하고 있으며, 전 세계 색전술 시장에 영향을 미치고 있습니다.

아시아태평양은 2031년까지 8.45%라는 지역별 최고 연평균 성장률(CAGR)을 달성할 것으로 예상되며, 색전술 시장에서 가장 강력한 성장 동력으로 부상하고 있습니다. 해당 지역, 특히 B형 간염 바이러스(HBV) 유병률이 높은 지역에서는 간세포암으로 인한 부담이 증가하고 있습니다. 중국과 인도에서는 중재적 방사선학 분야의 체계 확충이 진행되고 있으며, 주요 도시권 이외의 지역에서도 색전술에 대한 접근성이 확대되고 있습니다. 일본에서는 중경막동맥 색전술의 임상 및 규제 측면에서의 발전이 진행되고 있으며, 이는 신경혈관 분야에 대한 관심이 높아지고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the embolotherapy market size is expected to increase from USD 3.99 billion in 2025 to USD 4.28 billion in 2026 and reach USD 6.10 billion by 2031, growing at a CAGR of 7.34% over 2026-2031.

This report is Segmented by Product Type (Embolic Agents, Embolization Coils, and More), Procedure (Transarterial Chemoembolization, and More), Disease Indication (Oncology, Benign Tumors, Vascular Abnormalities, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Embolotherapy Market Trends and Insights

Rising Burden of Cancer and Hypervascular Tumors

The embolotherapy market is closely tied to the global cancer burden, as embolization is critical for treating diseases with high vascular activity. Global cancer cases are projected to reach 20 million in 2025, with a significant rise expected by 2050, ensuring a growing patient base for embolic procedures. This trend is particularly evident in liver cancer, renal tumors, and bone lesions, where managing tumor blood supply is vital for both curative and palliative treatments. Demand is also shifting geographically, with Asia-Pacific and parts of Africa experiencing a rise in HBV- and HCV-related liver cancer cases, driving the need for TACE and similar procedures. Manufacturers are adapting product designs, pricing, and training to cater to a broader range of hospitals.

Expanding Use of Minimally Invasive Image-Guided Procedures

The embolotherapy market is benefiting from a shift toward catheter-based treatments in oncology, trauma, and vascular care. Enhanced imaging techniques, such as cone-beam CT and advanced fluoroscopic guidance, are improving distal vessel access and reducing procedural uncertainties. This shift enables more precise treatments and lowers technical barriers, allowing community hospitals and mid-sized centers to handle complex embolic cases. Newer coil systems are being designed to enhance workflow efficiency and reduce device burdens during large-vessel embolizations. As a result, the market is expanding through both rising disease incidences and broader procedural adoption across care settings.

Reimbursement Variability Across Indications and Care Settings

The embolotherapy market faces reimbursement challenges as the expansion of medical indications often outpaces payer frameworks in many countries. While oncology applications have clearer billing pathways, newer uses in neurology and urology lack consistency. In the U.S., evolving payer policies for novel materials and applications delay hospital formulary adoption and broader market rollouts. In Europe, variations in health technology assessments and payer interpretations across countries result in uneven access, even with regulatory approvals. Premium-priced next-generation embolics are initially adopted in high-volume centers with coding expertise, specialized staff, and robust internal review processes, slowing the market's ability to achieve widespread commercial success.

Other drivers and restraints analyzed in the detailed report include:

- Broader Adoption of Liquid and Resorbable Embolic Agents

- Evidence Generation for New Indications: Middle Meningeal Artery Embolization

- High Per-Case Device Cost and Inventory Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, embolic agents held a dominant 58.77% share of the embolotherapy market, surpassing all other product categories. This leadership stems from the widespread use of microsphere-based TACE, particle embolization, and the expanding liquid embolic class, all integral to interventional oncology. Unlike other product types confined to specific procedures, this group thrives across diverse treatment settings. Drug-eluting microspheres enhance local chemotherapy delivery while minimizing systemic exposure, while newer liquid systems offer flexibility for repeat or staged cancer treatments. Even with increasing emphasis on pricing and clinical differentiation, embolic agents remain the cornerstone of the embolotherapy market's revenue.

The premium segment of this category is evolving rapidly. Resorbable and conformable liquid embolics are shifting the focus from vessel occlusion to treatment planning and follow-up flexibility. Embolization coils, especially valued in neurovascular and complex peripheral applications, emphasize repositionability and control. Vascular plugs and plug systems, projected to grow at a 7.99% CAGR through 2031, are increasingly utilized in prostate artery embolization, fibroid procedures, and trauma cases requiring controlled occlusion.

TACE accounted for 34.40% of the embolotherapy market in 2025, making it the leading procedure by revenue. Its dominance is attributed to its established role in hepatocellular carcinoma, integration into treatment pathways, and widespread adoption in academic and community hospitals. TACE's procedural familiarity supports its repeated use in liver-directed oncology and extends its application to metastases, neuroendocrine tumors, and other hypervascular lesions. This versatility ensures TACE remains central to routine embolic practices, even as newer procedures gain attention.

TARE, projected to grow at an 8.25% CAGR through 2031, is gaining traction due to its clinical preference in specific patient demographics. A meta-analysis spanning 2024 to 2025 highlighted TARE's superior response, disease control, and one-year survival rates compared to TACE, alongside fewer common complications. A 2025 study showcased an 83% objective response rate and a median overall survival of 47.2 months for HCC patients with portal vein invasion undergoing Y-90 glass microsphere therapy.

Complete Report Scope:

- By Product Type

- Embolic Agents

- Liquid Embolic Agents

- Microspheres

- Particles

- Sclerosants and Adhesives

- Embolization Coils

- Detachable Coils

- Pushable Coils

- Vascular Plugs and Plug Systems

- Flow Diverters

- Support Devices

- Microcatheters

- Guidewires

- Embolic Agents

- By Procedure

- Transarterial Chemoembolization

- Transarterial Radioembolization

- Transcatheter Arterial Embolization

- Stent-Assisted Coiling

- Particle Embolization

- Sac Packing

- Sandwich Technique

- By Disease Indication

- Oncology

- Benign Tumors

- Vascular Abnormalities

- Hemorrhage and Trauma

- Neurology

- Urology and Nephrology

- Peripheral Vascular Disease

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic and Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 38.79% of the embolotherapy market, maintaining its position as the largest regional contributor. This dominance stems from a strong interventional radiology infrastructure, a wide procedural base in oncology and women's health, and regulatory support for innovative product approvals. The U.S. serves as the primary launch platform for new embolic technologies, providing early market access. North America is also central to the growth of middle meningeal artery embolization, with procedure volumes expected to approach acute ischemic stroke treatment levels by 2029.

In 2025, Europe held a significant share of the embolotherapy market, supported by advanced hospital systems in Germany, France, and the U.K. These countries benefit from well-developed interventional radiology departments and centralized oncology networks, enabling procedures like TACE, TARE, fibroid embolization, and neurovascular treatments. A German study documented 718 middle meningeal artery embolization procedures across 30 neurovascular centers, reflecting specialist density and growing clinical acceptance. Italy and Spain contribute to liver-directed oncology volumes, partly due to historical hepatitis-related disease burdens. Europe plays a key role in protocol development, product validation, and specialist training, influencing the global embolotherapy market.

Asia-Pacific is projected to achieve the fastest regional CAGR of 8.45% through 2031, emerging as the strongest growth driver for the embolotherapy market. The region faces a rising burden of hepatocellular carcinoma, particularly in areas with high HBV prevalence. China and India are expanding interventional radiology capacity, increasing access to embolization procedures beyond major urban centers. Japan is advancing clinical and regulatory pathways for middle meningeal artery embolization, signaling a growing neurovascular focus.

- Abbott Laboratories

- Acandis

- Asahi Intecc Co., Ltd.

- B. Braun

- Balt Extrusion

- Boston Scientific

- Cook Group

- Guerbet

- Inari Medical

- Johnson & Johnson

- Kaneka

- Medtronic

- Merit Medical Systems

- MicroVention

- Penumbra

- Shape Memory Medical

- Sirtex Medical Pty Ltd

- Stryker

- Terumo

- Wallaby Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Cancer and Hypervascular Tumors

- 4.2.2 Expanding Use of Minimally Invasive Image-Guided Procedures

- 4.2.3 Broader Adoption of Liquid and Resorbable Embolic Agents

- 4.2.4 Shift of Suitable Cases Toward Ambulatory and Short-Stay Settings

- 4.2.5 Device Innovation in Microcatheters, Delivery Systems, and Visibility Control

- 4.2.6 Evidence Generation for New Indications Such as Middle Meningeal Artery Embolization

- 4.3 Market Restraints

- 4.3.1 Reimbursement Variability Across Indications and Care Settings

- 4.3.2 High Per-Case Device Cost and Inventory Complexity

- 4.3.3 Specialist Dependency and Procedural Learning Curve

- 4.3.4 Limited Access to Interventional Infrastructure in Resource-Constrained Markets

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Embolic Agents

- 5.1.1.1 Liquid Embolic Agents

- 5.1.1.2 Microspheres

- 5.1.1.3 Particles

- 5.1.1.4 Sclerosants and Adhesives

- 5.1.2 Embolization Coils

- 5.1.2.1 Detachable Coils

- 5.1.2.2 Pushable Coils

- 5.1.3 Vascular Plugs and Plug Systems

- 5.1.4 Flow Diverters

- 5.1.5 Support Devices

- 5.1.5.1 Microcatheters

- 5.1.5.2 Guidewires

- 5.1.1 Embolic Agents

- 5.2 By Procedure

- 5.2.1 Transarterial Chemoembolization

- 5.2.2 Transarterial Radioembolization

- 5.2.3 Transcatheter Arterial Embolization

- 5.2.4 Stent-Assisted Coiling

- 5.2.5 Particle Embolization

- 5.2.6 Sac Packing

- 5.2.7 Sandwich Technique

- 5.3 By Disease Indication

- 5.3.1 Oncology

- 5.3.2 Benign Tumors

- 5.3.3 Vascular Abnormalities

- 5.3.4 Hemorrhage and Trauma

- 5.3.5 Neurology

- 5.3.6 Urology and Nephrology

- 5.3.7 Peripheral Vascular Disease

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics

- 5.4.4 Academic and Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Acandis GmbH

- 6.3.3 Asahi Intecc Co., Ltd.

- 6.3.4 B. Braun SE

- 6.3.5 Balt Extrusion

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Cook Medical LLC

- 6.3.8 Guerbet

- 6.3.9 Inari Medical, Inc.

- 6.3.10 Johnson and Johnson

- 6.3.11 Kaneka Corporation

- 6.3.12 Medtronic plc

- 6.3.13 Merit Medical Systems, Inc.

- 6.3.14 MicroVention, Inc.

- 6.3.15 Penumbra, Inc.

- 6.3.16 Shape Memory Medical Inc.

- 6.3.17 Sirtex Medical Pty Ltd

- 6.3.18 Stryker Corporation

- 6.3.19 Terumo Corporation

- 6.3.20 Wallaby Medical

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment