|

시장보고서

상품코드

2073005

간헐적 카테터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Intermittent Catheters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

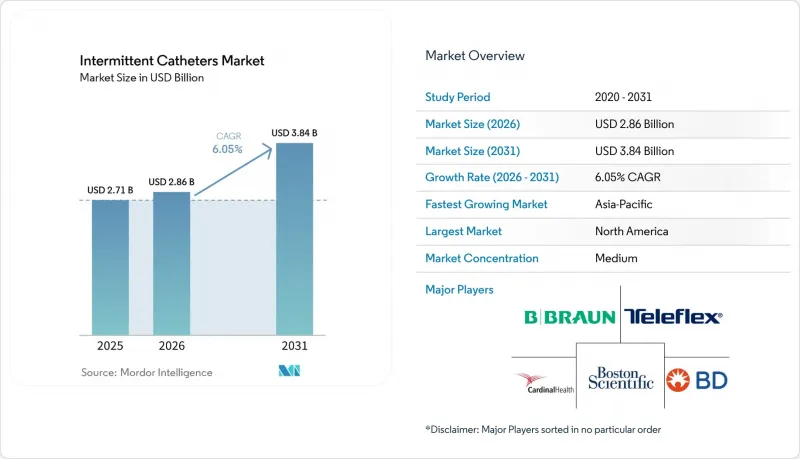

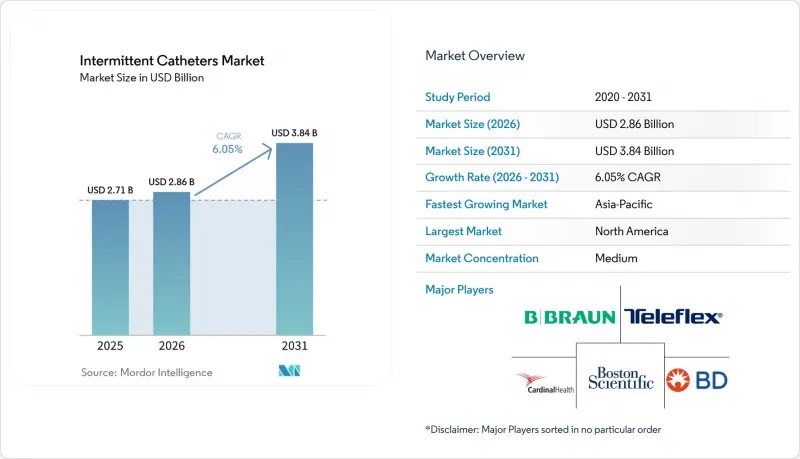

Mordor Intelligence에 의하면, 간헐적 카테터 시장 규모는 2025년 27억 1,000만 달러, 2026년 28억 6,000만 달러에서 2031년까지 38억 4,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.05%를 나타낼 전망입니다.

본 보고서는 제품 유형(코팅 처리, 비코팅), 카테고리(남성용, 여성용, 소아용), 팁 유형(스트레이트, 쿠데, 특수), 소재(PVC, 실리콘, 라텍스, 기타), 용도(신경성 방광, 요실금 등), 최종 사용자, 유통 채널, 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 간헐적 카테터 시장 동향 및 분석

신경성 방광에 가해지는 부담 증가

간헐적 카테터 시장은 신경성 방광 관리 분야에서 지속적인 수요를 얻고 있습니다. 이는 방광 기능 장애가 척수 손상 환자의 대다수에게 영향을 미치며, 다발성 경화증 환자 중에서도 상당수에게 영향을 미치고 있기 때문입니다. 2025년 중국에서 실시된 연구에 따르면, 만성 척수 손상 환자들 사이에서 간헐적 카테터 삽입법이 주요 방광 관리 방법으로 사용되고 있으며, 이 방법을 사용하는 환자들은 삽입형 기기에 의존하는 환자들에 비해 비뇨기과 입원 횟수가 적었던 것으로 나타났습니다. 환자층은 카테터를 가끔 사용하는 것이 아니라 장기간에 걸쳐, 종종 여러 의료 현장에서 지속적으로 사용하기 때문에 이와 유사한 임상 양상이 지속적인 수요를 뒷받침하고 있습니다. 간헐적 카테터 시장에는 입원 중인 척수 손상 환자의 치료 과정에서 여전히 지침을 따르지 않는 측정 방법이 일반적이라는 사실도 영향을 미치고 있습니다. 이러한 상황은 훈련 지원, 간호사가 주도하는 교육, 그리고 제조업체가 제공하는 치료 순응도 지원 도구에 대한 여지를 남겨두고 있습니다. 소아 환자 수요도 이 기반에 더해집니다. 선천성 신경 질환으로 인해 평생 카테터를 사용해야 하기 때문에 단기적인 치료 수요가 아니라 안정적인 교체 수요가 발생하고 있는 것입니다.

친수성 및 사전 윤활 처리된 카테터로의 전환

간헐적 카테터 시장은 친수성 및 사전 윤활 처리된 기기로 계속해서 전환되고 있습니다. 이러한 제품들은 요도 손상을 최소화하고, 일상적인 자가 카테터 삽입 시 사용 편의성이 향상되었기 때문입니다. 웰스펙트사는 2026년, LoFric Elle Pro 및 LoFric Origo Pro의 출시를 통해 이러한 추세를 더욱 확대할 예정입니다. 두 제품 모두 한 번의 배뇨로 방광을 완전히 비우는 것을 목적으로 하는 12개의 매끄러운 구멍이 특징입니다. 또한, 콜로플라스트사는 자사의 "Luja" 카테터 플랫폼이 요실금 관리 분야의 성장에 크게 기여했다고 보고되고 있으며, 이는 프리미엄 제품의 성능이 단순한 임상적 논의에 그치지 않고 상업적 성과로 이어지고 있음을 보여줍니다. 2026년 1월 CMS(미국 의료보험서비스센터)가 시행한 코딩 개정은 이러한 변화를 더욱 가속화하고 있습니다. 이는 메디케어 청구에서 코팅 제품과 비코팅 제품이 더 이상 단일한 종합적 환급 범주로 취급되지 않기 때문입니다. 따라서 간헐적 카테터 시장에서는 임상적 근거와 지불 조건의 명확성이라는 두 가지 요소가 모두 뒷받침하는 프리미엄 제품으로의 전환이 진행되고 있으며, 이는 어느 한 가지 요인만으로는 얻을 수 없는 강력한 시너지 효과를 발휘하고 있습니다.

프리미엄 카테터의 고액 본인 부담금

간헐적 카테터 시장은 여전히 큰 경제적 장벽에 직면해 있습니다. 이는 상환 체계가 취약한 제도 하에서는 프리미엄 친수성 장치의 가격이 표준적인 비코팅 제품보다 훨씬 비싸기 때문입니다. 이러한 가격 차이는 환자가 소모품을 직접 구매할 때 가장 큰 문제가 됩니다. 왜냐하면 매일, 그리고 장기간에 걸쳐 사용해야 하는 특성상, 제품 선택이 지속적인 경제적 부담으로 이어지기 때문입니다. 부적절한 지급을 대상으로 한 OIG의 감사 결과에서도, 규정 준수 심사가 강화됨에 따라 일부 미국 수급자들의 환급 접근성이 제한될 가능성이 시사되고 있습니다. 이는 자금이 충분히 확보된 제도라 하더라도, 간접적으로 프리미엄 제품의 구성 비율 확대를 둔화시킬 우려가 있습니다. 그 결과, 구조적인 상충 관계가 발생하여 일부 환자들은 비용을 절감하기 위해 카테터를 재사용하고 있지만, 재사용은 일회용 간헐적 카테터 요법이 지닌 위생상의 이점을 훼손하게 됩니다. 이러한 제약은 간헐적 카테터 시장에서 여전히 중요한 요소로 작용하며, 고부가가치 제품으로의 전환을 제한하고, 대규모 환자 집단에서 저비용 제품 형태에 대한 수요가 지속되는 요인이 되고 있습니다.

부문별 분석

2025년, 코팅 처리된 간헐적 카테터는 간헐적 카테터 시장 점유율의 56.21%를 차지하고 있으며, 이는 확립된 의료 제도 하에서 보험 급여 지원 및 임상 지침이 프리미엄 제품 형태를 얼마나 강력하게 뒷받침하고 있는지를 보여줍니다. 간헐적 카테터 시장에서 친수성 제품은 삽입의 용이성, 신체에 가해지는 부담의 경감, 그리고 일상적인 사용 시의 청결성을 강점으로 내세우고 있어, 코팅 처리된 기기 중에서도 판매량의 주요 원동력으로 자리 잡고 있습니다. 이는 특히 일회용 프로토콜이 더욱 보편화되고, 조달 결정 시 제품 가격뿐만 아니라 품질 지표도 점점 더 중요하게 여겨지고 있는 북미 및 북유럽에서 두드러지게 나타납니다. 항균 코팅 제품은 여전히 소규모 시장 부문이지만, 감염에 민감한 치료 과정에서 카테터의 취급 및 사용 시 더욱 철저한 오염 관리가 요구되는 상황에서는 그 중요성이 커지고 있습니다. 또한, 2026년 1월 메디케어 코딩 변경에 따라 친수성 제품의 보험 급여가 표준 청구 범주와 더욱 명확하게 구분되게 되었기 때문에 간헐적 카테터 시장에서도 코팅 제품에 상업적 우위가 생기고 있습니다.

코팅이 없는 카테터 시장은 2031년까지 연평균 성장률(CAGR) 6.81%를 나타낼 것으로 예측되며, 시장 점유율은 낮지만 가장 빠르게 성장하는 제품 유형입니다. 이러한 경향은 아시아태평양, 중동 및 아프리카, 그리고 라틴아메리카에서 나타난 비용 대체 현상을 반영한 것입니다. 이 지역에서는 병원, 진료소 및 본인 부담 환자들의 경우, 여전히 가격의 합리성이 제품 선택에 있어 중요한 결정 요인으로 작용하고 있습니다. 간헐적 카테터 업계에서 이러한 추세는 코팅 처리된 기기의 프리미엄 혁신과 기본적인 PVC 기반 제품의 꾸준한 판매량 호조 사이에서 양극화를 초래하고 있습니다. 또한, EU의 MDR(의료기기 규정)과 관련된 문서화 부담은 코팅이 적용되지 않은 제품을 취급하는 소규모 공급업체에게 더 큰 부담이 될 것입니다. 이는 이익률이 낮은 부문에서는 규정 준수 비용을 감당하기 어렵기 때문입니다. 그 결과, 간헐적 카테터 시장에서는 코팅 처리된 기기가 프리미엄 매출의 핵심으로 자리매김할 것으로 예상되는 반면, 가격에 민감한 환경에서는 코팅이 적용되지 않은 제품이 시장 진입과 판매량 확대에 있어 여전히 필수적인 역할을 할 것으로 보입니다.

2025년, 남성용 길이의 카테터는 간헐적 카테터 시장 규모의 42.83%를 차지했습니다. 이는 척수 손상의 유병률이 남성에게서 특히 높게 나타나는 점과, 성인 남성 자가 카테터 삽입 사용자의 기반이 크다는 점을 반영한 것입니다. 이러한 선도적인 입지는 대규모 임상 데이터 세트에서 척수 손상 환자 집단 내 남성의 비율이 여전히 높다는 사실에 의해 뒷받침되며, 이는 표준 남성용 길이의 제품에 대한 장기적인 수요를 지탱하고 있습니다. 여성용 길이의 제품은 제조업체가 컴팩트한 디자인, 눈에 띄지 않는 포장, 사용 편의성을 중시한 기능을 채택하여 의료 기관 이외의 일반 사용자층에서의 보급을 촉진하고 있기 때문에 전략적으로 중요한 위치를 계속 차지하고 있습니다. 콜로플라스트사는 2025/26 회계연도 2분기에 프랑스와 영국에서 여성용 카테터 "Luja"의 채택이 호조를 보였습니다고 보고하고 있으며, 이는 사용자 중심의 제품 설계가 성숙한 유럽 시장에서 판매 호조로 이어지고 있음을 시사합니다. 따라서 간헐적 카테터 시장에서는 길이뿐만 아니라 해부학적 구조, 일상생활 습관, 그리고 포장에 대한 기대에 따라 카테고리의 발전 방향이 결정되고 있습니다.

소아용 카테터 시장은 2031년까지 연평균 성장률(CAGR) 7.94%로 확대될 것으로 예상되며, 간헐적 카테터 시장에서 가장 빠르게 성장하는 부문으로 자리매김하고 있습니다. 이러한 성장은 소아 신경학 및 재활 서비스의 확대에 힘입은 바가 크며, 특히 선천성 신경 질환으로 인해 장기간 카테터를 사용해야 하는 환자들이 계속해서 발생하고 있는 개발도상국에서 두드러지게 나타납니다. 이분척추나 신경성 방광 진단을 받은 어린이들은 성인이 되어서도 카테터를 계속 사용하는 경우가 많기 때문에 조기 진단은 단기적인 치료 주기가 아니라 수년에 걸친 지속적인 수요를 뒷받침하게 됩니다. 또한, 소아용 제품 라인에 직경 축소, 삽입 시 부담 경감, 어린이 친화적인 포장이 도입되는 것도 간헐적 카테터 시장에 긍정적인 요인이 될 것입니다. 왜냐하면 장기적인 지속 사용은 임상적 필요성뿐만 아니라 일상적인 수용성에도 좌우되기 때문입니다. 이러한 요인들이 복합적으로 작용하여, 소아 부문은 현재 시장 규모만으로는 예상되는 것 이상으로 계속해서 전략적인 주목을 받고 있습니다.

2025년에는 스트레이트 팁 카테터가 59.64%의 시장 점유율을 차지했습니다. 이는 표준적인 요도 해부학적 구조에 폭넓게 부합한다는 점과, 많은 훈련 프로토콜에서 기본 선택지로 자리 잡고 있다는 점을 반영한 것입니다. 간헐적 카테터 시장에서 스트레이트 팁 형태가 여전히 주요 진입점으로 자리 잡고 있는 이유는 임상의들이 보다 전문적인 구성을 고려하기 전에 일반적으로 환자에게 간단한 기기로부터 사용을 시작하게 하기 때문입니다. 그 주도적 지위는 규모 면에서도 뒷받침되고 있습니다. 대규모 병원이나 의료기관의 조달 프로그램에서는 복잡성을 줄이면서도 일상적인 수요의 폭넓은 범위를 아우르는 제품이 선호되는 경향이 있기 때문입니다. 이로 인해 스트레이트 팁 제품은 최초 처방부터 재공급 주기에 이르기까지 지속적인 수요 기반의 중심적인 위치를 계속 차지하고 있습니다. 따라서 간헐적 카테터 시장에서는 스트레이트 팁 장치가 여전히 판매량이 가장 많은 팁 카테고리로 자리 잡고 있습니다.

쿠데칩 카테터 시장은 양성 전립선 비대증, 요도 협착 및 수술 후 해부학적 문제를 겪는 환자들을 주요 대상으로 하여, 2031년까지 연평균 성장률(CAGR) 7.33%로 성장할 것으로 전망됩니다. CMS(미국 의료보험서비스센터)는 관련 친수성 코드 하에서 쿠데 팁을 사용할 경우, 명확한 의료적 필요성을 입증하는 문서를 요구하고 있으며, 이는 미국 의료 제도 내에서 팁 유형별 보상 기준의 확립과 보다 명확한 임상적 근거의 제시를 뒷받침하고 있습니다. 특수 첨단 제품은 여전히 규모는 작지만, 보다 유연한 설계나 개별적으로 조정된 설계를 통해 삽입의 어려움을 줄일 수 있는 소아 의료 및 복잡한 신경 질환 치료 분야에서 그 입지를 다져가고 있습니다. 원격 진료도 이 부문을 뒷받침하고 있으며, 해부학적 문제를 안고 있는 환자들은 대면 진료 횟수를 줄이면서도 더 신속하게 전문의의 진단을 받고, 더 적절한 첨단 치료법을 선택할 수 있게 됩니다. 간헐적 카테터 업계에서 이에 따라 쿠데형 및 특수 형상의 제품은 프리미엄이자 임상적으로 차별화된 제품 라인 내에서 그 범위는 좁지만 꾸준히 중요한 역할을 수행하고 있습니다.

지역별 분석

2025년, 북미는 간헐적 카테터 시장 점유율의 33.41%를 차지하며, 금액 기준으로 가장 규모가 큰 지역 블록이 되었습니다. 이 지역이 주도적인 위치를 차지하고 있는 것은 미국에서 확립된 보험 환급 제도, 높은 일회용 제품 채택률, 그리고 간헐적 기기를 장기간 사용하는 신경성 방광 환자의 방대한 환자 기반이 맞물려 이러한 요인들이 시너지 효과를 발휘하고 있기 때문입니다. 2026년 1월의 HCPCS 개혁은 친수성 코팅 제품에 대해 코드 A4295, A4296 및 A4297을 통해 보다 명확한 청구 경로를 제공한다는 점에서 특히 중요하며, 이를 통해 코팅 제품으로의 전환 및 환자에 대한 직접 공급이 촉진될 것입니다. 캐나다에서는 척수 손상 및 신경성 방광 관리에 대한 각 주의 체계적인 보상 제도를 통해 시장의 안정성이 확보되어 있는 반면, 멕시코에서는 규모는 작지만 민간 의료 수요의 기반이 확대되고 있습니다. 북미의 간헐적 카테터 시장은 젊은 층이나 활동적인 자가 카테터 삽입 환자들이 정기적인 공급 일정을 유지할 수 있도록 돕는 디지털 지원 도구가 조기에 도입된 점도 호재로 작용하고 있습니다.

2025년, 유럽은 간헐적 카테터 시장에서 2위 지역 클러스터가 되었으며, 독일, 영국, 프랑스가 이를 주도했습니다. 콜로플라스트사는 2025/26 회계연도 상반기 보고서에서 이들 국가를 배설 관리 분야의 성장에 주요하게 기여하는 국가로 지목했으며, 이는 각국의 주요 의료 제도가 가진 구매력을 뒷받침하는 것입니다. 독일의 2026년 개정판 임상 지침에서는 신경성 하부 요로 기능 장애에 대한 권고 기준으로 "청결 간헐적 카테터법" 이를 통해 해당 지역에 더 많은 제도적 지원이 제공되고 있습니다. 동시에, EU의 MDR(의료기기 규정)로의 전환에 따라 문서화 및 사후 관리 요건이 강화되고 있으며, 이에 따라 규제 대응 체계를 갖춘 대형 공급업체들이 점차 유리한 입지를 확보하고 있습니다. 남유럽 및 동유럽에서는 특히 의사의 연수나 환자 교육이 북유럽에 비해 아직 충분하지 않은 지역에서 여전히 확대의 여지가 있습니다.

아시아태평양의 간헐적 카테터 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.82%로 확대될 것으로 예상되며, 본 조사 대상 지역 중 가장 빠른 성장세를 보이고 있습니다. 중국은 이러한 성장 과정에서 여전히 중심적인 역할을 하고 있습니다. 2025년 임상 증거에 따르면, 만성 척수 손상 환자에게서 간헐적 카테터법이 주요 방광 관리법이며, 상주 카테터 사용에 비해 비뇨기과 입원 건수가 적다는 사실이 밝혀졌기 때문입니다. 인도에서는 척추이분증과 관련된 수요, 비뇨기과 서비스 이용 가능성의 확대, 그리고 대도시권 이외 지역에서의 재활 치료 접근성 향상이 맞물려 시장의 성장세를 뒷받침하고 있습니다. 일본은 고령화 사회와 요실금 및 전립선 전적출술 후 관리 분야에서 확립된 이용 기반을 바탕으로 안정적인 수요를 뒷받침하고 있습니다. 한국과 호주는 친수성이 뛰어나고 컴팩트한 제품 형태가 높은 의료 수준과 자가 관리에 따른 사용 수용도와 잘 부합하여, 해당 지역 내 프리미엄 시장을 형성하고 있습니다. 중동 및 아프리카 및 남미는 전체적으로 여전히 규모가 작은 편이지만, GCC(걸프협력회의) 국가들에서는 프리미엄 수요 증가세가 나타나고 있으며, 브라질에서는 재활 및 공립병원 경로를 통해 CIC(간헐적 카테터법)의 지속적인 사용량에 대한 견고한 임상 도입 기반이 형성되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the intermittent catheters market size is projected to expand from USD 2.71 billion in 2025 and USD 2.86 billion in 2026 to USD 3.84 billion by 2031, registering a CAGR of 6.05% between 2026 to 2031.

This report is Segmented by Product Type (Coated, Uncoated), Category (Male, Female, Pediatric), Tip Type (Straight, Coude, Specialty), Material (PVC, Silicone, Latex, Others), Application (Neurogenic Bladder, Urinary Incontinence, and More), End User, Distribution Channel, Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Intermittent Catheters Market Trends and Insights

Rising Neurogenic Bladder Burden

The intermittent catheters market draws durable demand from neurogenic bladder management because bladder dysfunction affects a large share of people with spinal cord injury and a meaningful share of those living with multiple sclerosis. A 2025 study from China showed that intermittent catheterization was the leading bladder management method among chronic spinal cord injury patients, and those using it had fewer urological hospitalizations than those relying on indwelling devices. The same clinical pattern supports recurring demand because the patient base does not use catheters occasionally, but over long periods and often across several care settings. The intermittent catheters market is also influenced by the fact that guideline-discordant measurement practices remain common in hospitalized spinal cord injury care, which leaves room for training support, nurse-led education, and adherence tools from manufacturers. Pediatric demand adds to this base because congenital neurological conditions create a long lifetime of catheter use, which supports steady replacement volume rather than short-cycle treatment demand.

Shift Toward Hydrophilic and Pre-Lubricated Catheters

The intermittent catheters market continues to move toward hydrophilic and pre-lubricated devices because these products are associated with lower urethral trauma and better ease of use in routine self-catheterization. Wellspect expands this direction in 2026 with the LoFric Elle Pro and LoFric Origo Pro launches, both built around 12 smooth eyelets intended to support complete bladder emptying in one flow. Coloplast also reported that its Luja catheter platform was a main contributor to continence care growth, which shows that premium product performance is translating into commercial results rather than remaining only a clinical discussion. The January 2026 CMS coding revision strengthens this shift because coated and non-coated products are no longer treated as one bundled reimbursement category in Medicare billing. The intermittent catheters market is therefore seeing premium conversion supported by both clinical evidence and payment clarity, which is a stronger combination than either factor alone.

High Out-of-Pocket Cost for Premium Catheters

The intermittent catheters market still faces a meaningful affordability barrier because premium hydrophilic devices cost far more than standard uncoated alternatives in systems with weak reimbursement. This price gap matters most where patients buy supplies directly, because the daily and long-duration nature of use turns a product choice into a sustained financial burden. The OIG audit on improper payments also suggests that tighter compliance reviews can narrow reimbursement access for some U.S. beneficiaries, which may indirectly slow premium mix expansion even in a well-funded system. The result is a structural tradeoff in which some patients reuse catheters to control cost, even though reuse weakens the hygiene advantage that supports single-use intermittent protocols. This restraint remains important for the intermittent catheters market because it limits conversion toward higher-value products and keeps lower-cost formats relevant in large patient populations.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Support for Disposable Intermittent Catheters

- Closed System Adoption in Infection-Sensitive Care Pathways

- Reuse Behavior and Supply Inconsistency in Price-Sensitive Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated intermittent catheters held 56.21% of the intermittent catheters market share in 2025, which shows how strongly reimbursement support and clinical guidance favor premium formats in established healthcare systems. In the intermittent catheters market, hydrophilic products remain the main volume engine inside coated devices because they are positioned around easier insertion, lower trauma, and cleaner daily use. This is especially visible in North America and Northern Europe, where single-use protocols are more established and where procurement decisions increasingly reflect quality metrics as well as product price. Antimicrobial-coated devices remain a smaller tier, but they are gaining relevance where infection-sensitive care pathways require stronger contamination control during catheter handling and use. The intermittent catheters market also gives coated products a commercial advantage because January 2026 Medicare coding changes now differentiate hydrophilic reimbursement from standard billing categories in a more direct way.

Uncoated catheters are projected to grow at a 6.81% CAGR through 2031, which makes them the fastest-moving product type even though their share base is smaller. That pattern reflects cost substitution in Asia-Pacific, the Middle East and Africa, and Latin America, where affordability still determines much of product choice across hospitals, clinics, and out-of-pocket users. In the intermittent catheters industry, this creates a split between premium innovation in coated devices and steady volume resilience in basic PVC-based products. EU MDR documentation also needs to weigh more heavily on smaller suppliers of uncoated products because compliance costs are harder to absorb in lower-margin categories. As a result, the intermittent catheters market is likely to keep coated devices at the center of premium revenue while uncoated products remain essential for access and volume growth in price-sensitive settings.

Male length catheters accounted for 42.83% share of the intermittent catheters market size in 2025, reflecting the strong male skew in spinal cord injury prevalence and the large installed base of adult male self-catheterization users. This leading position is supported by the fact that spinal cord injury cohorts in large clinical datasets continue to show a high male representation, which feeds long-term demand for standard male length products. Female length products remain strategically important because manufacturers are using compact designs, discreet packaging, and easier handling features to improve adoption among daily users outside institutional settings. Coloplast reported strong uptake for the Luja female catheter in France and the United Kingdom during Q2 2025/26, which suggests that user-centered product design is translating into sales momentum in mature European markets. The intermittent catheters market is therefore seeing category development shaped by anatomy, daily routine, and packaging expectations rather than by length alone.

Pediatric length catheters are projected to rise at a 7.94% CAGR through 2031, which makes them the fastest-growing category in the intermittent catheters market. This growth is supported by expanding pediatric neurology and rehabilitation services, particularly in developing countries where congenital neurological conditions continue to create long-duration catheter users. Children diagnosed with spina bifida or neurogenic bladder often continue catheter use into adulthood, so early diagnosis supports many years of recurring demand rather than a short treatment cycle. The intermittent catheters market also benefits when pediatric lines incorporate smaller diameters, gentler insertion features, and child-friendly packaging, because long-term adherence depends on routine acceptability as much as clinical need. That combination keeps the pediatric segment under stronger strategic focus than its current size alone would suggest.

Straight tip catheters commanded 59.64% share in 2025, which reflects their broad suitability across standard urethral anatomies and their role as the default option in many training protocols. In the intermittent catheters market, straight tip formats remain the main entry point because clinicians commonly begin patients on simpler devices before considering more specialized configurations. Their leadership is also helped by scale, since large hospital and institutional purchasing programs often prefer products that cover a wide range of routine needs with less complexity. This keeps straight tip products central to the recurring demand base across both initial prescriptions and repeat supply cycles. The intermittent catheters market therefore continues to rely on straight tip devices as its broadest-volume tip category.

Coude tip catheters are projected to expand at a 7.33% CAGR through 2031, driven by patients with benign prostatic hyperplasia, urethral strictures, and post-surgical anatomical difficulty. CMS requires explicit medical necessity documentation for coude use under the relevant hydrophilic code, which supports tip-specific reimbursement discipline and clearer clinical justification in the U.S. system. Specialty tip products remain smaller, but they are building a place in pediatric and complex neurological care where softer or more tailored designs can reduce insertion difficulty. Remote consultations also support this segment because patients with anatomy-related challenges can reach specialists faster and move to more suitable tip types without as many in-person visits. In the intermittent catheters industry, that gives coude and specialty formats a narrower but steadily deepening role within premium and clinically differentiated product lines.

Complete Report Scope:

- By Product Type

- Coated Intermittent Catheters

- Hydrophilic Coated Catheters

- Antimicrobial Coated Catheters

- Uncoated Intermittent Catheters

- PVC Intermittent Catheters

- Latex Intermittent Catheters

- Coated Intermittent Catheters

- By Category

- Male Length Catheters

- Female Length Catheters

- Pediatric Length Catheters

- By Tip Type

- Straight Tip Catheters

- Coude Tip Catheters

- Specialty Tip Catheters

- By Material

- PVC

- Silicone

- Latex

- Polyurethane

- Polyethylene

- By Application

- Neurogenic Bladder

- Urinary Retention

- Urinary Incontinence

- Spinal Cord Injury

- Prostate Surgery

- Multiple Sclerosis

- By End User

- Hospitals

- Home Care Settings

- Ambulatory Surgical Centers

- Long-Term Care Facilities

- Specialty Clinics

- By Distribution Channel

- Institutional Sales

- Retail Pharmacies

- Online and Direct-To-Patient

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 33.41% of intermittent catheters market share in 2025, which made it the largest regional block by value. The region leads because the United States combines established reimbursement, high single-use adoption, and a large diagnosed base of neurogenic bladder patients who use intermittent devices over long periods. The January 2026 HCPCS reform is especially important because it gives hydrophilic-coated products clearer billing pathways through codes A4295, A4296, and A4297, which supports coated conversion and direct-to-patient supply. Canada adds stability through structured provincial reimbursement for spinal cord injury and neurogenic bladder care, while Mexico adds a smaller but growing private healthcare demand base. The intermittent catheters market in North America also benefits from earlier adoption of digital support tools that help younger and active self-catheterizing patients stay on routine supply schedules.

Europe was the second-largest regional cluster in the intermittent catheters market in 2025, led by Germany, the United Kingdom, and France. Coloplast identified these countries as key contributors to continence care growth in its H1 2025/26 reporting, which underlines the purchasing strength of their major health systems. Germany's revised 2026 clinical guidance gives the region added institutional support by positioning clean intermittent catheterization as the preferred standard for neurogenic lower urinary tract dysfunction. At the same time, the EU MDR transition is raising documentation and follow-up demands, which gradually favors large suppliers with stronger regulatory infrastructure. Southern and Eastern Europe still offer room for expansion, especially where physician training and patient education remain less developed than in Northern Europe.

The intermittent catheters market size for Asia-Pacific is projected to expand at 7.82% CAGR through 2031, the fastest regional pace in this study. China remains central to that growth because 2025 clinical evidence showed intermittent catheterization as the leading bladder management method among chronic spinal cord injury patients, with fewer urological hospitalizations than indwelling use. India adds momentum through a combination of spina bifida-linked need, broader urology service availability, and rehabilitation access beyond the largest metro centers. Japan supports steady demand through its aging population and its established use base in urinary incontinence and post-prostatectomy care. South Korea and Australia represent premium regional pockets where hydrophilic and compact formats fit well with higher healthcare standards and greater acceptance of self-managed use. Middle East and Africa and South America remain smaller overall, but the GCC shows premium demand growth while Brazil provides a strong clinical adoption base for recurring CIC volume through rehabilitation and public hospital channels.

- Adapta Medical, Inc.

- Amsino International, Inc.

- Bactiguard Holding AB

- B. Braun

- Beckton Dickinson

- Boston Scientific

- Cardinal Health

- Coloplast

- Convatec

- Cook Group

- Cure Medical, LLC

- Flexicare

- Hollister

- HR HealthCare, Inc.

- Medline Industries

- Medtronic

- Pennine Healthcare Ltd

- Romsons Group of Industries

- Teleflex

- Wellspect HealthCare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Neurogenic Bladder Burden

- 4.2.2 Shift Toward Hydrophilic and Pre-Lubricated Catheters

- 4.2.3 Expansion of Home-Based Self-Catheterization

- 4.2.4 Reimbursement Support for Disposable Intermittent Catheters

- 4.2.5 Closed System Adoption in Infection-Sensitive Care Pathways

- 4.2.6 Data-Driven Training and Remote Support Improves Adherence

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Cost for Premium Catheters

- 4.3.2 Reuse Behavior and Supply Inconsistency in Price-Sensitive Markets

- 4.3.3 Limited Urology Training and Patient Technique Variability

- 4.3.4 Material and Biocompatibility Compliance Burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Coated Intermittent Catheters

- 5.1.1.1 Hydrophilic Coated Catheters

- 5.1.1.2 Antimicrobial Coated Catheters

- 5.1.2 Uncoated Intermittent Catheters

- 5.1.2.1 PVC Intermittent Catheters

- 5.1.2.2 Latex Intermittent Catheters

- 5.1.1 Coated Intermittent Catheters

- 5.2 By Category

- 5.2.1 Male Length Catheters

- 5.2.2 Female Length Catheters

- 5.2.3 Pediatric Length Catheters

- 5.3 By Tip Type

- 5.3.1 Straight Tip Catheters

- 5.3.2 Coude Tip Catheters

- 5.3.3 Specialty Tip Catheters

- 5.4 By Material

- 5.4.1 PVC

- 5.4.2 Silicone

- 5.4.3 Latex

- 5.4.4 Polyurethane

- 5.4.5 Polyethylene

- 5.5 By Application

- 5.5.1 Neurogenic Bladder

- 5.5.2 Urinary Retention

- 5.5.3 Urinary Incontinence

- 5.5.4 Spinal Cord Injury

- 5.5.5 Prostate Surgery

- 5.5.6 Multiple Sclerosis

- 5.6 By End User

- 5.6.1 Hospitals

- 5.6.2 Home Care Settings

- 5.6.3 Ambulatory Surgical Centers

- 5.6.4 Long-Term Care Facilities

- 5.6.5 Specialty Clinics

- 5.7 By Distribution Channel

- 5.7.1 Institutional Sales

- 5.7.2 Retail Pharmacies

- 5.7.3 Online and Direct-To-Patient

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East & Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East & Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Adapta Medical, Inc.

- 6.3.2 Amsino International, Inc.

- 6.3.3 Bactiguard Holding AB

- 6.3.4 B. Braun SE

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Cardinal Health, Inc.

- 6.3.8 Coloplast A/S

- 6.3.9 ConvaTec Group Plc

- 6.3.10 Cook Medical LLC

- 6.3.11 Cure Medical, LLC

- 6.3.12 Flexicare (Group) Limited

- 6.3.13 Hollister Incorporated

- 6.3.14 HR HealthCare, Inc.

- 6.3.15 Medline Industries, LP

- 6.3.16 Medtronic plc

- 6.3.17 Pennine Healthcare Ltd

- 6.3.18 Romsons Group of Industries

- 6.3.19 Teleflex Incorporated

- 6.3.20 Wellspect HealthCare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment