|

시장보고서

상품코드

2073006

소화기 내시경 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gastrointestinal Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

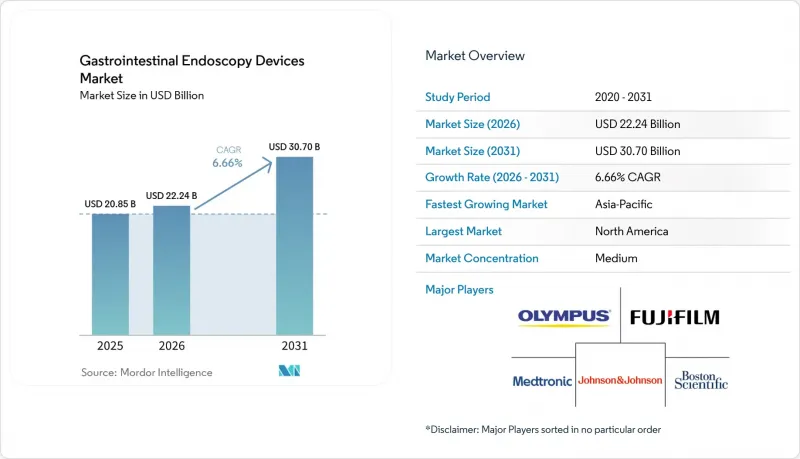

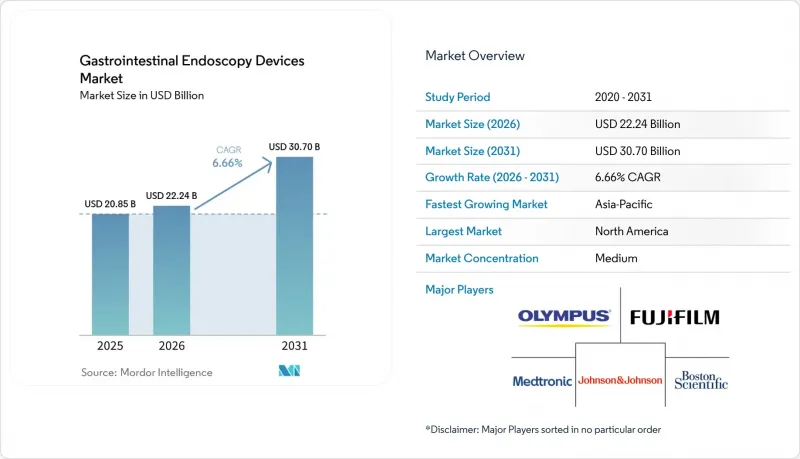

Mordor Intelligence에 의하면, 소화기 내시경 기기 시장 규모는 2025년에 208억 5,000만 달러로 평가되었고, 2026년에 222억 4,000만 달러로 추정되고, 2031년까지 307억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.66%로 성장할 전망입니다.

본 보고서는 제품 유형별(내시경, 영상 표시 장치, 수술용 기기), 재사용 가능성별(재사용 가능, 일회용), 연령대별(성인, 고령자, 소아), 용도별(진단, 치료), 최종 사용자별(병원, 외래수술센터(ASC) 등) 및 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소화기 내시경 기기 시장 동향 및 인사이트

대장암 및 위암 검진 수요 증가

소화기 내시경 기기 시장은 대장암 및 상부 위장관암 검진을 주요 수요원으로 삼고 있으며, 그 수요 기반은 2026년에도 견조한 추세를 보일 것으로 전망됩니다. 미국암협회(American Cancer Society)의 추산에 따르면, 2026년 미국의 대장암 신규 환자 수는 15만 8,850건에 달할 것으로 예상되며, 예상 사망자 5만 5,230명 중 3분의 1은 65세 미만 환자에서 발생할 것으로 전망됩니다. 이러한 상황으로 인해 보험사 및 의료 시스템은 더 폭넓은 연령층이 선별검사를 이용할 수 있도록 조치를 취해야 하는 압박을 받고 있습니다. 두 번째 수요층은 청년층에서 발생하고 있습니다. 2022년 대장암 환자 중 22%가 55세 미만인 것으로 진단되었으며, 이는 1995년의 11%에서 증가한 수치로, 더 많은 환자 집단에서 평생에 걸친 선별검사와 추적 관찰의 필요성이 커지고 있습니다. 검진 수진율도 긍정적인 추세를 보이고 있으며, 미국에서는 45세 이상 성인의 수진율이 2021년 59%에서 2023년에는 65%로 상승했고, 2024년에는 의료기관에서 검진을 받은 환자 총수가 361만 7,246명에 달했습니다. 비침습적 검사에서 양성 결과가 나온 환자는 여전히 대장내시경 검사를 받게 되므로, 새로운 선별 검사 방법은 소화기 내시경 기기 시장의 검사 건수를 빼앗는 것이 아니라, 오히려 해당 시장으로의 환자 유입 경로를 더욱 확대하는 역할을 하고 있습니다. 후지필름의 2026년판 투자자용 자료 역시 이러한 장기적인 수요 전망을 뒷받침하고 있으며, 동사는 성숙 시장과 신흥 시장 모두에서 고령화와 암 발병률 증가를 배경으로, 전 세계 소화기 내시경 분야가 연평균 4%에서 6%의 성장률을 유지할 것으로 예측했습니다.

감염 예방을 위한 일회용 내시경으로의 급속한 전환

소화기 내시경 기기 시장은 감염 예방을 위한 일회용 기기로의 광범위한 전환에 힘입어 성장하고 있습니다. 일회용 내시경의 도입은 당초 십이지장 내시경에서 시작되었으나, 현재는 오염 위험이 임상적·법적으로 더 중대한 의미를 갖는 기관지 내시경 검사나 특정 소화기 계통 검사에서도 이와 유사한 구매 논리가 적용되고 있습니다. 2025년에 발표된 연구 결과에 따르면, 실제 임상 현장에서 고수준 소독을 실시하더라도 미생물을 확실하게 제거할 수 없으며, 재처리된 기기에서 여전히 우려 수준이 높은 미생물이나 다제내성균이 검출되고 있는 것으로 나타났습니다. 이 근거는 2025년 9월에 업데이트된 AHRQ의 일회용 내시경 사용에 관한 검토를 포함하여, 정책 논의 및 기술 평가 작업에 영향을 미치고 있습니다. 또 다른 실질적인 촉진요인은 교육 병원에서 이루어지는 연수의 일관성입니다. 일회용 기기를 사용하면 시술마다 발생하는 마모로 인한 편차가 사라지고, 재처리 품질과 관련된 불확실성이 줄어들기 때문입니다. 점점 더 많은 제조업체들이 적응증과 제품 라인을 확대함에 따라, 재사용의 경제성보다 안전성 확보가 더 중요시되는 환경 속에서 소화기 내시경 기기 시장에서는 일회용 시스템에 대한 지속적인 수요가 예상됩니다.

자본 설비 및 이미징 타워에 드는 막대한 초기 투자 비용

소화기 내시경 기기 시장은 여전히 고성능 영상 진단 시스템, 프로세서, AI 모듈 및 타워 일체형 설비의 비용으로 인해 뚜렷한 성장 한계에 직면해 있습니다. 새로운 플랫폼은 임상적 가치를 높이고 있지만, 많은 지역 병원과 공공 의료 기관이 여전히 설비 투자 예산에 신중한 태도를 보이고 있는 가운데, 도입 비용 상승을 초래하고 있습니다. 후지필름의 'ELUXEO 8000'는 4K 영상, 3단계 노이즈 저감, 그리고 정밀 검사를 목적으로 하는 앰버·레드 컬러 이미징 기능을 탑재하여 이러한 추세를 반영하고 있지만, 시스템 차원의 도입 비용이 높기 때문에 검사 건수가 많은 시설 이외의 곳에서는 보급에 한계가 있을 수 있습니다. 또한, 많은 병원이 영상 진단 장비를 7-10년 주기로 교체하고 있다는 점도 도입의 제약 요인으로 작용하고 있습니다. 이러한 업데이트 주기는 AI 지원 플랫폼으로의 전환이 가속화되고 있는 현재 상황에 비해 느리기 때문입니다. 이 문제는 신흥 시장에서 더욱 두드러지며, 서비스 지원이 미흡하고 조달 예산도 빠듯한 상황에서는 수요가 완전 통합형 플랫폼이 아닌 저비용의 현지 제작 시스템이나 모듈식 구성 요소로 이동할 가능성이 있습니다. 그 때문에 임상 수요가 견조함에도 불구하고, 소화기 내시경 기기 시장의 일부는 도입 주기가 느린 데 얽매인 상태가 계속되고 있습니다.

부문별 분석

2025년에는 내시경이 제품 유형별 시장 점유율의 38.31%를 차지한 것으로 평가되었으며, 이는 진단 및 치료에 있어 소화기 워크플로우 전반에서 유연 대장내시경과 위내시경이 핵심적인 역할을 하고 있음을 반영합니다. 그 규모는 선별 검사, 감시 및 중재 분야에서 일상적으로 사용됨으로써 뒷받침되고 있으며, 소화기 내시경 기기 시장에서 다른 어떤 제품군보다 폭넓은 수요 기반을 갖추고 있습니다. 이 카테고리 내에서는 여전히 유연한 제품이 주류를 이루고 있지만, 감염 위험이 높은 특정 의료 현장에서는 일회용 제품이 급속히 확산되고 있습니다. 생검 집게, 스네어, 클립, 전기 수술 기구 등은 이미 도입된 장비가 많아 병원 설비 투자의 지연에 영향을 덜 받기 때문에 수술용 기기 및 부속품은 지속적인 매출을 창출하고 있습니다.

시각화 기기는 2031년까지 8.38%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 이는 현재의 업그레이드 주기가 내시경 본체뿐만 아니라 프로세서, 모니터, 타워 및 소프트웨어 호환 플랫폼과 점점 더 밀접하게 연계되고 있음을 보여줍니다. 올림푸스는 2025년 5월에 'Extended Depth of Field' 기술을 탑재한 EZ1500 시리즈에 대해 FDA의 510(k) 승인을 획득하여, 이 사이클을 뒷받침했습니다. 이 기술은 근거리에서 이미지의 선명도를 향상시켜, 호환 가능한 기존 시스템을 업데이트해야 할 실질적인 이유를 마련해 주었습니다. 후지필름의 'ELUXEO 8000'은 2026년, 더욱 정교한 내시경 검사 작업을 목적으로 4K 영상 처리 및 앰버·레드 컬러 이미징 기능을 탑재함으로써 이러한 추세를 더욱 공고히 했습니다. 현재, 이미지 처리 장치에 연간 단위의 AI 소프트웨어 라이선스가 결합되는 사례가 늘어나고 있으며, 이로 인해 계약 총액이 증가하고 고객을 더 오랜 기간 동안 단일 벤더의 생태계 내에 묶어둘 수 있게 되어 상업적 매력이 더욱 높아지고 있습니다.

2025년에는 재사용 가능한 내시경이 매출의 80.24%를 차지했습니다. 이는 병원의 소화기 내시경 검사실에서 폭넓게 도입된 실적을 바탕으로, 검사 건수가 많은 시설에서는 재사용을 통해 여전히 건당 비용을 낮게 유지할 수 있다는 점이 배경에 있습니다. 임상의들은 재사용 제품의 취급에 익숙하고, 병원은 이미 필요한 인프라를 갖추고 있으며, 많은 첨단 검사에서는 여전히 재사용 시스템에 의존하고 있기 때문에 이러한 도입 실적은 여전히 중요합니다. 그렇긴 하지만, 소화기 내시경 기기 시장에서는 오염 위험이 용납되기 어려운 경우나 환자의 특성이 더 민감한 경우, 일회용 제품의 성장이 가속화되고 있습니다. 재처리 실패가 임상적, 재정적 또는 법적 위험을 지나치게 높일 수 있는 처치나 환경에서 그 도입이 가장 활발히 이루어지고 있습니다.

일회용 내시경 시장은 2031년까지 연평균 성장률(CAGR) 7.52%로 확대될 것으로 예상되며, 이러한 성장세는 제한적인 비상 대응 용도에서 보다 일상적인 조달 계획으로의 광범위한 전환을 반영하고 있습니다. 2024년 일회용 내시경에 관한 델파이 합의 결과, 현재의 도입 현황이 특히 다제내성균에 노출된 환자와 밀접한 관련이 있는 것으로 나타났으며, 보다 광범위한 활용을 위해서는 비용 대비 효과와 임상적 근거의 향상이 필요하다고 지적되었습니다. 이는 꾸준하면서도 여전히 선택적인 확대 경로를 시사하고 있습니다. 경쟁과 관련된 과제는 일회용 제품과 재사용 가능한 제품 간의 대립에만 국한되지 않습니다. 왜냐하면 본체는 재사용이 가능하고 끝부분은 일회용인 이러한 하이브리드 방식이 중규모 의료기관에서 매력적인 선택지가 될 가능성이 있기 때문입니다. 마이크로텍사도 일회용 제품 및 내시경 치료 관련 혁신 분야에서 꾸준한 성장세를 보이고 있으며, 2026년 4월까지 여러 건의 FDA 510(k) 승인을 획득했습니다. 이는 재사용 빈도가 낮은 워크플로우를 중심으로, 액세서리 및 중재 치료의 생태계가 더욱 광범위하게 발전하고 있음을 시사합니다. 제조 규모가 확대되고 대상 시술의 유형이 늘어남에 따라, 소화기 내시경 기기 시장에서는 감염 관리 비용의 일부가 재처리 인프라에서 기기 교체로 계속 전환될 가능성이 높다고 볼 수 있습니다.

지역별 분석

2025년, 북미는 소화기 내시경 기기 시장 규모의 38.22%를 차지했으며, 매출 측면에서 가장 규모가 큰 지역 기여도를 보였습니다. 이 지역은 선별 대장내시경 검사의 높은 보급률, 잘 갖춰진 외래수술센터(ASC) 네트워크, 그리고 예방적 소화기 계통 시술을 점점 더 중시하는 보험사 측의 지원 등 여러 이점을 누리고 있습니다. 미국은 여전히 주요 국가별 성장 동력으로 자리 잡고 있습니다. 이는 CMS(미국 의료보험의료서비스센터)가 2025년 1월부터 대장암 검진의 적용 범위를 확대하여 CT 대장조영술, 혈액 기반 바이오마커 검사 및 Cologuard Plus를 포함하게 되었기 때문입니다. 이로 인해 검사 절차의 초기 단계가 확대되었으며, 양성 판정 후 실시되는 추적 대장내시경 검사 수요가 유지되었습니다. 캐나다에서는 각 주가 대기 시간 및 수용 능력 문제를 지속적으로 해결해 나가고 있는 만큼, 공적 의료 시스템에 대한 수요가 더욱 안정적으로 증가하고 있습니다. 한편, 멕시코는 도시 지역 시장에서 민간 의료 투자의 혜택을 누리고 있습니다. 북미의 소화기 내시경 기기 시장은 텍사스주, 플로리다주, 애리조나주 등지에서 의사 주도의 ASC(외래수술센터(ASC))가 발전함에 따라 재편이 진행되고 있으며, 이로 인해 병원에서 외래 진료로의 전환이 가속화되어 중급급 영상 진단 시스템에 대해 보다 단기적인 교체 기회가 생겨나고 있습니다.

유럽은 여전히 프리미엄 기기 수요의 주요 원천이며, 독일, 프랑스, 영국에서는 차세대 영상 진단 기술 및 AI 연동 플랫폼의 도입이 진행되고 있습니다. EU의 MDR 2017/745는 소규모 공급업체에 대한 시장 진입 요건을 강화한 반면, 더 광범위한 임상 증거 및 시판 후 조사 의무를 충족할 수 있는 대기업의 입지를 강화하는 결과도 낳았습니다. 이탈리아와 스페인에서는 대장암 검진의 현대화가 진행되고 있으며, 이는 장기적으로 대장내시경 검사 건수와 일회용 소모품 수요 모두를 뒷받침할 것으로 전망됩니다. 중동부 유럽에서는 일부 지역에서 공공 조달 주기와 의료 인프라에 대한 투자가 개선되고 있어, 여전히 시장 진출의 여지가 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.65%를 나타낼 것으로 예측되며, 위장관 내시경 기기 시장에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 이러한 성장은 중국, 인도, 한국에서 선별 검사 활동이 확대된 데 더해, 다양한 수준의 병원에서 진료 역량이 확대됨에 따라 프리미엄급 및 가성비형 시스템 모두에 대한 수요가 증가하고 있는 점이 뒷받침하고 있습니다. 일본은 고령화의 진행과 조기 위암에 대한 ESD(내시경 점막하층 박리술)의 보급이 소화기 내시경 수요를 지속적으로 뒷받침하고 있기 때문에 구조적으로 중요한 시장으로 남아 있습니다. 중동 및 아프리카 및 남미는 여전히 시장 규모가 작지만, 의료 시스템의 현대화와 민관 협력을 통한 내시경 검사의 확대에 힘입어 검사에 대한 접근성이 점차 개선됨에 따라, 비록 다소 뒤처지기는 했지만 비슷한 궤적을 따라가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the gastrointestinal endoscopy devices market size is projected to be USD 20.85 billion in 2025, USD 22.24 billion in 2026, and reach USD 30.70 billion by 2031, growing at a CAGR of 6.66% from 2026 to 2031.

This report is Segmented by Product Type (Endoscopes, Visualization Equipment, Operative Devices), Reusability (Reusable, Single-Use), Age Group (Adults, Geriatrics, Pediatrics), Application (Diagnostics, Therapeutics), End User (Hospitals, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Gastrointestinal Endoscopy Devices Market Trends and Insights

Rising Colorectal And Gastric Cancer Screening Demand

The gastrointestinal endoscopy devices market continues to draw its core volume from colorectal and upper gastrointestinal cancer screening, and that demand base remains durable in 2026. The American Cancer Society estimates 158,850 new colorectal cancer cases in the United States in 2026, and one-third of the expected 55,230 deaths is projected to occur in patients younger than 65, which is pushing payers and health systems to broaden screening access across more age groups. A second demand layer comes from younger adults, because 22% of colorectal cancer cases in 2022 were diagnosed in people younger than 55, up from 11% in 1995, which increases lifetime screening and surveillance needs for a larger patient pool. Screening uptake is also moving in the right direction, as the U.S. rate rose from 59% in 2021 to 65% in 2023 among adults aged 45 and older, and total patients screened at health centers reached 3,617,246 in 2024. Positive results from noninvasive tests still drive patients into colonoscopy, so newer screening formats are not removing procedures from the gastrointestinal endoscopy devices market, but are instead adding a wider referral funnel into it. Fujifilm's 2026 investor material also supports that longer demand picture, as it expects the global gastrointestinal endoscopy field to sustain 4% to 6% annual growth on the back of aging populations and rising cancer incidence in both mature and developing markets.

Rapid Shift Toward Single-Use Endoscopy For Infection Control

The gastrointestinal endoscopy devices market is also being lifted by the wider shift toward single-use devices for infection control. The original case for disposable endoscopes began with duodenoscopes, but the same purchasing logic is now moving into bronchoscopy and selected gastrointestinal procedures where contamination risk carries greater clinical and legal weight. Evidence published in 2025 showed that high-level disinfection does not reliably eliminate microorganisms in real-world practice, with high-concern organisms and multidrug-resistant organisms still found on reprocessed devices. That evidence is shaping policy discussions and technology review work, including the AHRQ review of disposable endoscope use that was updated in September 2025. Another practical driver is training consistency in teaching hospitals, because single-use devices remove wear-related variation from one procedure to the next and reduce uncertainty linked to reprocessing quality. As more manufacturers widen indications and product lines, the gastrointestinal endoscopy devices market is likely to see durable demand for disposable systems in settings where safety assurance matters more than reuse economics.

High Capital Cost Of Capital Equipment And Imaging Towers

The gastrointestinal endoscopy devices market still faces a clear ceiling from the cost of premium imaging systems, processors, AI modules, and full tower setups. New platforms are adding clinical value, but they also raise acquisition cost at a time when many community hospitals and public systems remain careful with capital budgets. Fujifilm's ELUXEO 8000 reflects that direction, with 4K imaging, triple noise reduction, and Amber-Red Color Imaging aimed at more advanced procedures, yet the price of system-level adoption can limit uptake outside higher-volume facilities. Replacement timing adds another constraint because many hospitals refresh imaging equipment on a 7 to 10 year cycle, which is slower than the current push toward AI-ready platforms. The problem is more pronounced in emerging markets, where weaker service support and tighter procurement budgets can shift demand toward lower-cost local systems or modular components instead of full integrated platforms. This keeps part of the gastrointestinal endoscopy devices market tied to slower conversion cycles even when clinical demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Lesion Detection And Documentation

- Expansion Of Ambulatory And Outpatient GI Procedure Capacity

- Reprocessing Burden And Infection-Control Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endoscopes held the largest product type share at 38.31% in 2025, reflecting the central role of flexible colonoscopes and gastroscopes across diagnostic and therapeutic gastrointestinal workflows. Their scale is supported by routine use in screening, surveillance, and intervention, which gives them a broader demand base than any other product group in the gastrointestinal endoscopy devices market. Flexible products remain dominant inside this category, while disposable formats are expanding faster within specific infection-sensitive settings. Operative devices and accessories continue to provide recurring sales, because biopsy forceps, snares, clips, and electrosurgical tools are used across a large installed base and are less exposed to hospital capital delays.

Visualization equipment is projected to record the highest CAGR at 8.38% through 2031, which shows that the current upgrade cycle is increasingly tied to processors, monitors, towers, and software-ready platforms rather than only to scopes. Olympus supported that cycle when it received FDA 510(k) clearance in May 2025 for the EZ1500 series with Extended Depth of Field technology, which improved image sharpness at closer distances and created a practical reason to refresh compatible installed systems. Fujifilm's ELUXEO 8000 further reinforced the same pattern in 2026 with 4K imaging and Amber-Red Color Imaging aimed at more complex endoscopy work. The commercial appeal is stronger because imaging processors are now increasingly paired with annual AI software licenses, which raises total contract value and keeps customers inside one vendor ecosystem for a longer period.

Reusable endoscopes commanded 80.24% of revenue in 2025, supported by the deep installed base in hospital gastrointestinal labs and the lower cost per procedure that high-volume centers can still achieve with reuse. That installed base remains important because clinicians are familiar with reusable handling, hospitals already own the supporting infrastructure, and many advanced procedures still depend on reusable systems. Even so, the gastrointestinal endoscopy devices market is seeing faster growth in single-use formats where contamination risk is less acceptable or patient profiles are more sensitive. Adoption is strongest in procedures and settings where a reprocessing failure would create disproportionate clinical, financial, or legal exposure.

Single-use endoscopes are projected to grow at a 7.52% CAGR through 2031, and that pace reflects a broader move from narrow rescue use into more regular procurement planning. A 2024 Delphi consensus on disposable endoscopy linked current adoption most clearly to patients with multidrug-resistant organism exposure and noted that broader use will depend on more cost-effectiveness and clinical evidence, which suggests a steady but still selective expansion path. The competitive issue is not limited to disposable versus reusable, because hybrid formats with reusable bodies and single-use distal mechanisms could become an attractive option in medium-volume sites. Micro-Tech also showed continued momentum in disposable and endotherapy-linked innovation with multiple FDA 510(k) clearances through April 2026, which points to a wider accessory and intervention ecosystem developing around less reuse-intensive workflows. As manufacturing scale improves and more procedure types become eligible, the gastrointestinal endoscopy devices market is likely to keep shifting part of infection-control spending away from reprocessing infrastructure and toward device replacement.

Complete Report Scope:

- By Product Type

- Endoscopes

- Flexible Endoscopes

- Rigid Endoscopes

- Disposable Endoscopes

- Visualization Equipment

- Operative Devices and Accessories

- Endoscopes

- By Reusability

- Reusable Endoscopes

- Single-Use Endoscopes

- By Age Group

- Adults

- Geriatrics

- Pediatrics

- By Application

- Diagnostics

- Therapeutics

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Specialty Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.22% of the gastrointestinal endoscopy devices market size in 2025, making it the largest regional contributor by revenue. The region benefits from high screening colonoscopy uptake, a mature ambulatory surgery center network, and payer support that increasingly favors preventive gastrointestinal procedures. The United States remains the main national driver because CMS expanded colorectal screening coverage from January 2025 to include CT colonography, blood-based biomarker tests, and Cologuard Plus, which widened the front end of the procedure funnel and preserved follow-on colonoscopy demand after positive results. Canada adds steadier public-system demand as provinces continue to address wait times and capacity needs, while Mexico is benefiting from private healthcare investment in urban markets. The gastrointestinal endoscopy devices market in North America is also being reshaped by physician-led ASC development in states such as Texas, Florida, and Arizona, which is shortening the shift from hospitals to outpatient care and creating a nearer-term replacement opportunity for mid-tier imaging systems.

Europe remains an important source of premium device demand, with Germany, France, and the United Kingdom supporting adoption of next-generation imaging and AI-linked platforms. EU MDR 2017/745 has lengthened market entry requirements for smaller suppliers, but it has also strengthened the position of larger companies that can support broader clinical evidence and post-market surveillance obligations. Italy and Spain are moving ahead with colorectal cancer screening modernization, which should support both colonoscopy volume and demand for single-use accessories over time. Central and Eastern Europe still offer room for penetration as public procurement cycles and healthcare infrastructure investment improve across parts of the region.

Asia-Pacific is projected to grow at an 8.65% CAGR through 2031, which makes it the fastest-growing regional segment in the gastrointestinal endoscopy devices market. Growth is being supported by broader screening efforts in China, India, and South Korea, alongside demand for both premium and value-tier systems as capacity expands across different hospital tiers. Japan remains a structurally important market because aging demographics and the wider use of ESD for early gastric cancer continue to support gastrointestinal endoscopy demand. Middle East and Africa and South America remain smaller, but they are moving along a similar path with a lag as health system modernization and public-private endoscopy expansion gradually improve procedure access.

- Ambu

- Beckton Dickinson

- Boston Scientific

- Conmed

- Cook Group

- Erbe Elektromedizin

- FUJIFILM

- Johnson & Johnson

- Karl Storz

- Medtronic

- MICRO-TECH (Nanjing) Co., Ltd.

- Olympus

- PENTAX Medical America, Inc.

- Richard Wolf

- Smart Medical Systems Ltd.

- Stryker

- Teleflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Colorectal and Gastric Cancer Screening Demand

- 4.2.2 Rapid Shift Toward Single-Use Endoscopy for Infection Control

- 4.2.3 AI-Assisted Lesion Detection and Documentation

- 4.2.4 Expansion of Ambulatory and Outpatient GI Procedure Capacity

- 4.2.5 Reimbursement Support for Preventive and Early-Detection Procedures

- 4.2.6 Hidden Backlog From Deferred GI Procedures and Diagnostic Delays

- 4.3 Market Restraints

- 4.3.1 High Capital Cost of Capital Equipment and Imaging Towers

- 4.3.2 Reprocessing Burden and Infection-Control Compliance Costs

- 4.3.3 Shortage of Skilled Endoscopists and Procedural Support Staff

- 4.3.4 Pricing Pressure From GPOs, Tenders, and ASP Compression

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces, Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Endoscopes

- 5.1.1.1 Flexible Endoscopes

- 5.1.1.2 Rigid Endoscopes

- 5.1.1.3 Disposable Endoscopes

- 5.1.2 Visualization Equipment

- 5.1.3 Operative Devices and Accessories

- 5.1.1 Endoscopes

- 5.2 By Reusability

- 5.2.1 Reusable Endoscopes

- 5.2.2 Single-Use Endoscopes

- 5.3 By Age Group

- 5.3.1 Adults

- 5.3.2 Geriatrics

- 5.3.3 Pediatrics

- 5.4 By Application

- 5.4.1 Diagnostics

- 5.4.2 Therapeutics

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgery Centers

- 5.5.3 Specialty Clinics

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Ambu A/S

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Boston Scientific Corporation

- 6.3.4 CONMED Corporation

- 6.3.5 Cook Medical, Inc.

- 6.3.6 Erbe Elektromedizin GmbH

- 6.3.7 Fujifilm Holdings Corporation

- 6.3.8 Johnson and Johnson

- 6.3.9 KARL STORZ SE and Co. KG

- 6.3.10 Medtronic plc

- 6.3.11 MICRO-TECH (Nanjing) Co., Ltd.

- 6.3.12 Olympus Corporation

- 6.3.13 PENTAX Medical America, Inc.

- 6.3.14 Richard Wolf GmbH

- 6.3.15 Smart Medical Systems Ltd.

- 6.3.16 Stryker Corporation

- 6.3.17 Teleflex Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment