|

시장보고서

상품코드

2073007

라식 안과 수술 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)LASIK Eye Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

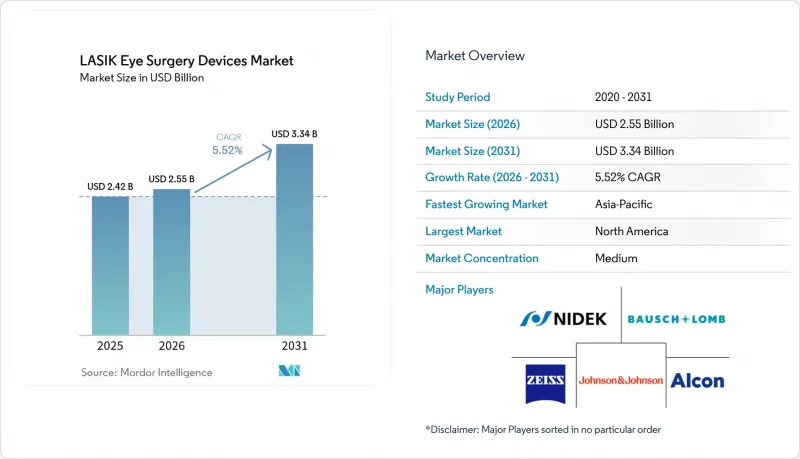

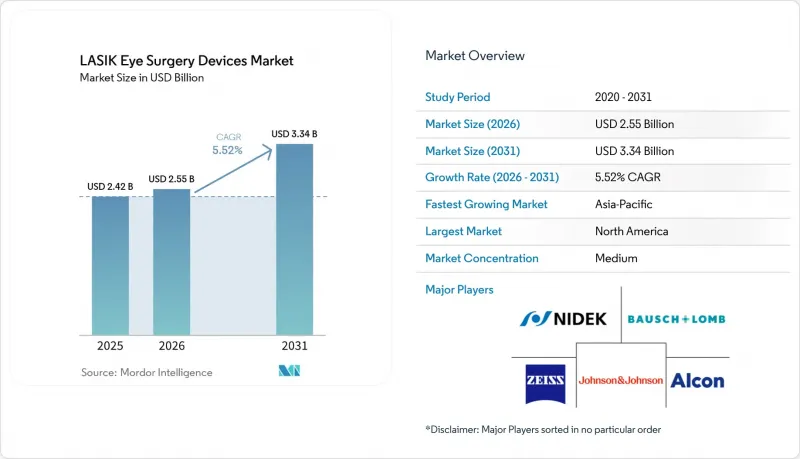

Mordor Intelligence에 의하면, 라식 안과 수술 기기 시장 규모는 2025년 24억 2,000만 달러로 평가되었고, 2026년에는 25억 5,000만 달러로 추정되고, 2031년까지 33억 4,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 5.52%로 성장할 전망입니다.

본 보고서는 제품 유형별(펨토초 레이저, 엑시머 레이저, 기타 장비), 기술별(파면 유도형, 파면 최적화형, 토포그래피 유도형, 기타), 용도별(근시, 원시, 난시, 노안), 최종 사용자별(안과 클리닉, 병원, 외래수술센터(ASC), 기타), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 라식 안과 수술 기기 시장 동향 및 인사이트

근시 및 난시로 인한 부담 증가

라식 안과 수술 기기 시장은 소아, 청소년, 젊은 성인층에서 근시 및 관련 굴절 이상이 꾸준히 증가하고 있는 데 힘입어 장기적인 호재를 누리고 있습니다. 2025년에 실시된 276건의 연구와 540만 명 이상의 참가자를 대상으로 한 메타분석에 따르면, 전 세계 소아 및 청소년의 근시 유병률이 1990년 24.32%에서 2023년에는 35.81%로 증가한 것으로 밝혀졌습니다. 이와 유사한 증거들은 이 환자들 중 굴절 교정 수술을 받을 수 있는 임상적 적정 연령대에 도달함에 따라 향후 치료 대상자가 더욱 크게 증가할 것임을 시사하고 있습니다. 동아시아는 여전히 가장 심각한 문제 지역이며, WHO의 지역별 데이터에 따르면 중국과 싱가포르의 특정 집단에서는 청소년의 근시 비율이 80%에 육박하고 있습니다. 근시에는 난시가 동반되는 경우가 많기 때문에 증례 수가 증가함에 따라 단순한 구면 교정에 그치지 않고, 보다 강력한 난시 관리 기능을 갖춘 플랫폼에 대한 수요가 높아지고 있습니다. 이러한 추세에 따라 라식 안과 수술 기기 시장은 대량 처리가 가능한 일반적인 사례뿐만 아니라, 보다 복잡한 시력 프로파일에도 대응할 수 있는 시스템으로 전환되고 있습니다.

블레이드 방식에서 올레이저 라식(LASIK)으로의 전환

라식 안과 수술 기기 시장은 블레이드를 이용한 수술에서 올레이저 치료 워크플로로 지속적으로 전환되고 있는 추세에 힘입어 성장하고 있습니다. 2025년 3월, 미국 FDA는 'WaveLight EX500 레이저 시스템' 및 'INNOVEYES Sightmap'의 조합을 승인했습니다. 이는 레이 트레이싱 기술을 활용한 맞춤형 라식 시스템으로서는 최초로 승인을 받은 것입니다. 알콘사는 이후 WaveLight Plus를 이용해 치료를 받은 환자 200명, 총 400안의 실제 임상 결과를 보고했습니다. 이에 따르면, 근시 환자의 100%가 수술 후 3개월 시점에서 교정 없이 원거리 시력 20/20을 달성했으며, 89%는 20/16에 도달했습니다. 또한, 2025년 『BMC Ophthalmology』지에 게재된 연구에서도 레이 트레이싱 가이드 방식의 LASIK이 표준 기법에 비해 과교정률을 낮추는 것으로 밝혀졌습니다. 이러한 결과로 인해 프리미엄 클리닉에 대한 환자들의 기대치가 높아지면서, 동등한 계획 정확도나 치료 정확도를 제공하지 못하는 구형 장비에 대한 압박이 커지고 있습니다. 따라서 라식 안과 수술 기기 시장에서는 하드웨어의 노후화뿐만 아니라, 치료 결과에 대한 기대와 소프트웨어의 기능성에 의해서도 기기 교체 수요가 형성되고 있습니다.

높은 초기 도입 비용 및 유지 비용

높은 초기 투자 비용은 특히 주요 도시권의 의료 집적 지역 이외의 지역에서 라식 안과 수술 기기 시장의 도입을 가로막는 가장 뚜렷한 장벽 중 하나로 남아 있습니다. 고급 펨토초 레이저 및 엑시머 레이저 시스템은 일반적으로 1대당 30만-70만 달러 이상의 초기 투자가 필요하며, 연간 서비스 계약비는 4만-8만 달러에 달할 전망입니다. 이러한 비용 구조는 시술 건수가 적은 시설의 경우 부담이 커, 구매 결정 시 업그레이드를 연기하거나 중고 시스템을 도입하도록 이끄는 요인이 되고 있습니다. 부담은 초기 구매 가격에만 그치지 않습니다. 엑시머 레이저 시스템은 특수 가스나 광학 시스템 지원에도 의존하고 있으며, 이러한 비용이 지속적인 운영비로 추가되기 때문입니다. 따라서 가동률은 매우 중요합니다. 시술 밀도가 낮은 시설에서는 장기적으로 자본 비용이나 서비스 비용을 회수할 여지가 제한적이기 때문입니다. 그 결과, 굴절 교정에 대한 임상적 수요가 증가하고 있는 상황에서도 비용에 민감한 지역에서는 새로운 플랫폼의 도입 속도가 둔화되고 있습니다.

부문별 분석

2025년, 펨토초 레이저는 라식 안과 수술 기기 시장에서 42.31%의 점유율을 차지했으며, 해당 시장에서 가장 큰 제품 부문이 되었습니다. 이러한 우위는 프리미엄 굴절 교정 워크플로우에서 블레이드리스 플랩 형성의 확립된 역할과, 재현성이 높은 절개 형태에 대한 강력한 수요를 반영하고 있습니다. 또한 외과의사들은 기계식 시스템에 비해 피판의 두께를 보다 정밀하게 조절할 수 있고, 상피 합병증을 줄일 수 있다는 점을 높이 평가했습니다. 하버드 대학의 조사에 따르면, 펨토초 레이저는 라식 전용 도구에서 보다 광범위한 각막 수술 플랫폼으로 진화하고 있으며, 이로 인해 도입된 각 시스템의 경제성이 강화되고 있습니다. 이러한 이용 사례의 확대는 설비 투자의 정당성을 높여주며, 경쟁이 심화되더라도 프리미엄 가격을 유지하는 데 도움이 되고 있습니다. 따라서 라식 안과 수술 기기 업계에서는 펨토초 레이저의 도입을 굴절 교정 분야의 자산일 뿐만 아니라, 보다 광범위한 안과 의료 역량에 대한 투자로 계속해서 인식하고 있습니다.

엑시머 레이저는 가장 빠르게 성장하고 있는 제품 부문이며, 이 부문의 라식 안과 수술 기기 시장 규모는 2026-2031년 연평균 성장률(CAGR) 7.38%로 확대될 것으로 전망됩니다. 최근 규제 당국의 승인으로 인해 적용 가능한 용도가 확대되었으며, 듀얼 플랫폼 도입의 근거가 더욱 탄탄해졌습니다. 보슈-롬사는 2024년 1월, 근시 및 근시성 난시를 위한 라식 시력 교정 수술용 'TENEO 엑시머 레이저 플랫폼'에 대해 FDA의 승인을 획득했습니다. 또한, FDA는 MEL 90을 라식용 승인 레이저 목록에 추가함으로써, 이 부문에서 진행 중인 적응증 확대를 뒷받침하고 있습니다. 이러한 승인으로 치료의 유연성이 높아짐에 따라, 과거에는 제한된 굴절 교정 기기에 의존하던 의료기관들도 펨토초 레이저와 엑시머 레이저를 병행하는 체제로 전환하고 있습니다. 이러한 전환은 수술 건수 증가세가 급격하지 않고 안정적인 경우에도 엑시머 레이저에 대한 수요를 서서히 끌어올리는 요인이 됩니다.

2025년에는 웨이브프론트 가이드 방식의 라식(LASIK)이 매출의 43.24%를 차지했으며, 라식 안과 수술 기기 시장에서 주요 기술로서의 입지를 확고히 했습니다. 이러한 대규모 도입 실적과 오랜 기간에 걸친 임상 실적이, 수술 건수가 많은 굴절 교정 센터 수요를 지속적으로 뒷받침하고 있습니다. 2025년에 실시된 대측안에 대한 전향적 연구에 따르면, 수술 후 12개월 시점에서 웨이브프론트 가이드 방식의 LASIK은 토포그래피 가이드 방식의 LASIK에 비해 20/12.5의 시력 결과를 달성한 비율이 통계적으로 유의미하게 높은 것으로 보고되었습니다. 이는 각막의 불규칙성이 제한적이며, 정확도의 일관성이 가장 중요한 표준적인 근시 사례에서 해당 기술의 역할을 입증하는 것입니다. 또한, 웨이브프론트 최적화 시스템은 치료 계획 수립 기간 단축과 처리 능력의 효율화를 중시하는 바쁜 의료 기관에서도 효율성 면에서 우위를 유지하고 있습니다. 라식 안과 수술 기기 업계는 현재 기술 관련 수익의 대부분을 여전히 이 기존 도입 기반에 의존하고 있습니다.

토포그래피 가이드형 라식(LASIK)은 가장 빠르게 성장하고 있는 기술 분야로, 라식 안과 수술 기기 시장에서 2026-2031년의 연평균 성장률(CAGR)은 6.52%로 예측됩니다. 이 부문은 외과의사의 조작감 향상, 환자에게 더 뚜렷한 차별화, 그리고 불규칙하거나 복잡한 난시 사례에 대한 적응성 향상과 같은 이점을 누리고 있습니다. 알콘사의 'Contoura Topo-G'에 관한 핵심 임상시험에서 93%의 눈에서 교정 없이 원거리 시력이 20/20 이상, 32%에서는 20/12.5 이상을 달성한 것으로 나타났습니다. 2024년에 실시된 확대 코호트 연구에 따르면, 파면 유도 방식 및 지형도 유도 방식 플랫폼 모두 약 90%에 가까운 눈에서 20/20 이상의 시력을 달성한 것으로 밝혀졌으며, 이는 여러 기술 경로가 임상적으로 신뢰성을 유지할 수 있음을 보여주었습니다. 다음 단계의 경쟁은 진단 정확도와 절제 계획을 더욱 밀접하게 연계하는 레이 트레이싱 시스템을 통해 이미 나타나기 시작했습니다. 즉, 라식 안과 수술 기기 시장에서 기술 경쟁은 단순한 치료 범주에서 치료 결과에 특화된 워크플로우 설계로 전환되고 있는 것입니다.

지역별 분석

2025년, 북미는 라식 안과 수술 기기 시장의 45.52%를 차지했으며 최대 지역 시장이 되었습니다. 이 지역은 수술에 대한 인지도가 높고, 굴절 교정 수술을 위한 인프라가 잘 갖춰져 있으며, 새로운 장비나 치료법의 업그레이드에 대한 승인 절차가 활발하다는 특징을 모두 갖추고 있습니다. 2024년 1월부터 2025년 3월에 걸쳐, TENEO 및 INNOVEYES Sightmap을 탑재한 맞춤형 WaveLight EX500 등 주요 플랫폼이 미국 규제 당국의 허가 또는 승인을 획득함에 따라, 프리미엄 시스템의 업데이트 속도가 더욱 가속화되었습니다. 해당 지역의 라식 안과 수술 기기 시장은 고성능 의료기기를 도입할 수 있는 외래 안과 의료 제공업체의 기반이 광범위하다는 점도 호재로 작용하고 있습니다. 남미 시장은 여전히 규모가 작지만, 민간 안과 의료의 집중과 의료 관광의 흐름에 힘입어 브라질과 아르헨티나가 이 지역에서 가장 활발한 시술 거점으로 자리 잡고 있습니다.

유럽은 독일, 영국, 스페인에서 활발히 이루어지고 있는 성숙한 굴절 교정 수술에 힘입어, 라식 안과 수술 기기 시장에서 여전히 2위 지역 블록의 위치를 유지하고 있습니다. 독일에서는 전문 클리닉이나 학술적인 굴절 교정 센터를 통해, 첨단 기능을 갖춘 플랫폼에 대한 수요가 지속적으로 유지되고 있습니다. 영국에서도 공적 보험 적용 대상이 아닌 자비 부담 LASIK 수요가 안정적으로 유지되고 있으며, 이것이 꾸준한 시술 건수를 뒷받침하고 있습니다. 이 지역 전체적으로 EU 의료기기 규정의 요건이 강화됨에 따라, 새로운 절제 프로파일이나 소프트웨어 업데이트 시장 출시까지 걸리는 기간이 길어지고 있으며, 이는 규제 대응 체제가 잘 갖춰진 대기업들에게 유리하게 작용하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역 부문이며, 이 지역의 라식 안과 수술 기기 시장 규모는 2026-2031년 연평균 성장률(CAGR) 7.45%로 확대될 것으로 전망됩니다. 중국과 인도는 두 시장 모두 확대되고 있는 민간 안과 의료 체계와 향후 대규모 치료 대상층을 모두 갖추고 있어, 계속해서 주요 성장 동력으로 자리 잡고 있습니다. WHO 서태평양 지역 데이터에 따르면, 동아시아의 일부 지역에서는 청소년의 근시 유병률이 매우 높아, 이로 인해 장기적인 환자 유입이 구조적으로 견고하게 유지되고 있습니다. 한국 역시 국내 굴절 교정 수술의 기반이 탄탄할 뿐만 아니라, 국경을 넘어 찾아오는 환자들에게 비용 경쟁력이 높다는 점에서 지역 성장을 뒷받침하고 있습니다. 중동 및 아프리카는 사우디아라비아와 아랍에미리트(UAE)를 필두로 소규모 기반에서 성장을 이어가고 있으며, 의료 관광, 가처분 소득 증가, 전문 의료에 대한 투자가 수술 수요를 뒷받침하고 있습니다. 신흥 지역 전체적으로는 여전히 꾸준한 성장세를 보이고 있지만, 자본 비용, 규제상의 진입 요건, 그리고 숙련된 굴절 교정 수술 팀의 필요성으로 인해 그 속도는 완만해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the LASIK eye surgery devices market size is expected to increase from USD 2.42 billion in 2025 to USD 2.55 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 5.52% over 2026-2031.

This report is Segmented by Product Type (Femtosecond Lasers, Excimer Lasers, Other Devices), Technology (Wavefront-Guided, Wavefront-Optimized, Topography-Guided, Other), Application (Myopia, Hyperopia, Astigmatism, Presbyopia), End User (Eye Clinics, Hospitals, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, and More). Market Forecasts are in Terms of Value (USD).

Global LASIK Eye Surgery Devices Market Trends and Insights

Rising Myopia and Astigmatism Burden

The LASIK eye surgery devices market is drawing long-term support from the steady rise in myopia and related refractive conditions across children, adolescents, and young adults. A 2025 meta-analysis covering 276 studies and more than 5.4 million participants found that global myopia prevalence among children and adolescents rose from 24.32% in 1990 to 35.81% in 2023. The same body of evidence points to a much larger future treatment pool as these patients move into the age band where refractive surgery becomes clinically suitable. East Asia remains the most intense pressure point, with WHO regional data showing adolescent myopia rates approaching 80% in some China and Singapore cohorts. Astigmatism often appears alongside myopia, which means rising case volumes are not limited to simple spherical correction and increasingly favor platforms with stronger cylinder management. That pattern is helping the LASIK eye surgery devices market move toward systems that can treat more complex visual profiles rather than only high-volume routine cases.

Shift From Blade-Based to All-Laser LASIK

The LASIK eye surgery devices market is also being lifted by the continued move away from blade-based procedures and toward all-laser treatment workflows. In March 2025, the US FDA approved the WaveLight EX500 Laser System with INNOVEYES Sightmap, the first ray-tracing personalized LASIK system to receive that clearance. Alcon later reported real-world results from 200 patients and 400 eyes treated with wavelight plus, with 100% of myopic eyes reaching 20/20 uncorrected distance visual acuity at 3 months and 89% reaching 20/16. A 2025 study in BMC Ophthalmology also found that ray-tracing-guided LASIK reduced overcorrection ratios relative to standard approaches. These results are pushing patient expectations upward at premium centers and raising pressure on older installations that cannot deliver the same planning depth or treatment precision. The LASIK eye surgery devices market is therefore seeing replacement demand shaped as much by outcome expectations and software capability as by hardware age.

High Upfront Device and Maintenance Cost

High capital cost remains 1 of the clearest adoption limits for the LASIK eye surgery devices market, especially outside major urban care clusters. Premium femtosecond and excimer systems usually require initial spending from USD 300,000 to more than USD 700,000 per unit, with annual service contracts of USD 40,000 to USD 80,000. That cost base is difficult for lower-volume centers to absorb and often pushes purchasing decisions toward delayed upgrades or second-hand systems. The burden is not limited to initial purchase price because excimer systems also depend on specialty gases and optics support that add recurring operating expense. This makes utilization rates critical, since centers with weaker procedure density have less room to recover capital and service costs over time. The result is a slower placement pace for new platforms in cost-sensitive regions even when clinical demand for refractive correction is rising.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of High-Volume Refractive Surgery Centers

- Higher Upgrade Cycles for Wavefront and Topography-Guided Platforms

- Limited Insurance Coverage for Elective Vision Correction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Femtosecond lasers held 42.31% of the LASIK eye surgery devices market share in 2025, making them the largest product segment in the LASIK eye surgery devices market. Their lead reflects the established role of bladeless flap creation in premium refractive workflows and the strong preference for reproducible incision geometry. Surgeons also value the ability to control flap thickness more precisely and reduce epithelial complications compared with mechanical systems. A Harvard review traced the evolution of femtosecond lasers from LASIK-specific tools into broader corneal surgery platforms, which strengthens utilization economics for each installed system. That broader use case supports higher capital justification and helps maintain premium pricing even when procedure competition intensifies. The LASIK eye surgery devices industry therefore continues to treat femtosecond placement as both a refractive asset and a wider ophthalmic capability investment.

Excimer lasers are the fastest-growing product segment, with the LASIK eye surgery devices market size for this segment projected to expand at a 7.38% CAGR from 2026 to 2031. Recent regulatory clearances widened their addressable use and improved the case for dual-platform adoption. Bausch + Lomb received FDA approval for the TENEO Excimer Laser Platform for myopia and myopic astigmatism LASIK vision correction surgery in January 2024. The FDA also lists the MEL 90 among approved lasers for LASIK, reinforcing the broader indication expansion underway in the category. As these approvals expand treatment flexibility, centers that once relied on limited refractive setups are moving toward combined femtosecond and excimer ownership. That transition supports incremental excimer demand even when overall procedure growth is steady rather than abrupt.

Wavefront-guided LASIK accounted for 43.24% of revenue in 2025, giving it the leading technology position within the LASIK eye surgery devices market. Its large installed base and long clinical track record continue to support demand at high-volume refractive centers. A 2025 prospective contralateral-eye study reported that wavefront-guided LASIK delivered a statistically significantly higher rate of 20/12.5 visual outcomes than topography-guided LASIK at 12 months. That supports its role in standard myopia cases where corneal irregularity is limited and precision consistency matters most. Wavefront-optimized systems also retain an efficiency advantage in busy centers that value shorter treatment planning and throughput discipline. The LASIK eye surgery devices industry still depends on this installed base for a large part of current technology revenue.

Topography-guided LASIK is the fastest-growing technology segment, with a projected CAGR of 6.52% from 2026 to 2031 in the LASIK eye surgery devices market. The segment is benefiting from stronger surgeon comfort, more visible patient-facing differentiation, and better fit in irregular or complex astigmatic cases. Alcon's Contoura Topo-G pivotal study showed 93% of eyes reaching 20/20 uncorrected distance visual acuity or better and 32% reaching 20/12.5 or better. A 2024 expanded cohort study found that wavefront-guided and topography-guided platforms both achieved close to 90% of eyes at 20/20 or better, showing that multiple technology paths can remain clinically credible. The next layer of competition is already emerging through ray-tracing systems, which connect diagnostic depth more tightly to ablation planning. That means technology competition in the LASIK eye surgery devices market is shifting from simple treatment categories into outcome-specific workflow design.

Complete Report Scope:

- By Product Type

- Femtosecond Lasers

- Excimer Lasers

- Other LASIK Devices

- By Technology

- Wavefront-Guided LASIK

- Wavefront-Optimized LASIK

- Topography-Guided LASIK

- Other Technologies

- By Application

- Myopia

- Hyperopia

- Astigmatism

- Presbyopia

- By End User

- Eye Clinics

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 45.52% of the LASIK eye surgery devices market share in 2025, which made it the largest regional market. The region combines high procedure awareness, dense refractive surgery infrastructure, and an active approval environment for new devices and treatment upgrades. Between January 2024 and March 2025, major platforms such as TENEO and the personalized WaveLight EX500 with INNOVEYES Sightmap received U.S. regulatory clearance or approval, reinforcing the pace of premium system renewal. The LASIK eye surgery devices market in the region also benefits from a large base of outpatient eye care providers that can absorb high-end capital equipment. South America remains smaller, with Brazil and Argentina as the most active procedure centers in the region, supported by private eye care concentration and medical travel patterns.

Europe remained the second-largest regional block in the LASIK eye surgery devices market, supported by mature refractive surgery activity in Germany, the United Kingdom, and Spain. Germany continues to support demand for advanced capability platforms through specialty clinics and academic refractive centers. The United Kingdom also maintains stable private-pay LASIK demand outside public reimbursement, which supports consistent procedure volumes. Across the region, stricter EU Medical Device Regulation requirements are extending commercialization timelines for new ablation profiles and software updates, which favors larger companies with stronger regulatory infrastructure.

Asia-Pacific is the fastest-growing regional segment, with the LASIK eye surgery devices market size in the region projected to advance at 7.45% CAGR from 2026 to 2031. China and India remain the main growth engines because both markets combine expanding private eye care capacity with a large future treatment pool. WHO Western Pacific data show very high adolescent myopia prevalence in several East Asian settings, which keeps the long-term patient pipeline structurally strong. South Korea also supports regional growth through a strong domestic refractive surgery base and cost-competitive appeal for cross-border patients. The Middle East and Africa continue to develop from a smaller base, led by Saudi Arabia and the UAE where medical tourism, higher disposable incomes, and specialist care investment are supporting procedure demand. Across emerging regions, growth remains real, but it is moderated by capital cost, regulatory entry requirements, and the need for trained refractive surgery teams.

- Alcon

- Appasamy Associates Private Limited

- Bausch + Lomb Incorporated

- BVI Medical

- Carl Zeiss

- iVIS Technologies S.r.l.

- Johnson & Johnson Vision Care, Inc.

- LaserSight Technologies, Inc.

- LensAR, Inc.

- Lumenis

- Moria S.A.

- Nidek

- Optikon 2000 S.p.A.

- SCHWIND eye-tech-solutions GmbH & Co. KG

- Topcon

- Trivitron Healthcare

- Ziemer Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Myopia and Astigmatism Burden

- 4.2.2 Shift From Blade-Based to All-Laser LASIK

- 4.2.3 Expansion of High-Volume Refractive Surgery Centers

- 4.2.4 Higher Upgrade Cycles for Wavefront and Topography-Guided Platforms

- 4.2.5 Specialty Gas and Optics Supply Chain Localization Risk

- 4.2.6 Substitution Pressure From Phakic Intraocular Lenses in High-Myopia Cases

- 4.3 Market Restraints

- 4.3.1 High Upfront Device and Maintenance Cost

- 4.3.2 Limited Insurance Coverage for Elective Vision Correction

- 4.3.3 Surgeon Training Depth and Case-Volume Requirements

- 4.3.4 Regulatory Friction for New Ablation Profiles and Software Updates

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Femtosecond Lasers

- 5.1.2 Excimer Lasers

- 5.1.3 Other LASIK Devices

- 5.2 By Technology

- 5.2.1 Wavefront-Guided LASIK

- 5.2.2 Wavefront-Optimized LASIK

- 5.2.3 Topography-Guided LASIK

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Myopia

- 5.3.2 Hyperopia

- 5.3.3 Astigmatism

- 5.3.4 Presbyopia

- 5.4 By End User

- 5.4.1 Eye Clinics

- 5.4.2 Hospitals

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Appasamy Associates Private Limited

- 6.3.3 Bausch + Lomb Incorporated

- 6.3.4 BVI Medical

- 6.3.5 Carl Zeiss Meditec AG

- 6.3.6 iVIS Technologies S.r.l.

- 6.3.7 Johnson & Johnson Vision Care, Inc.

- 6.3.8 LaserSight Technologies, Inc.

- 6.3.9 LensAR, Inc.

- 6.3.10 Lumenis Ltd.

- 6.3.11 Moria S.A.

- 6.3.12 NIDEK CO., LTD.

- 6.3.13 Optikon 2000 S.p.A.

- 6.3.14 SCHWIND eye-tech-solutions GmbH & Co. KG

- 6.3.15 Topcon Corporation

- 6.3.16 Trivitron Healthcare Private Limited

- 6.3.17 Ziemer Ophthalmic Systems AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment